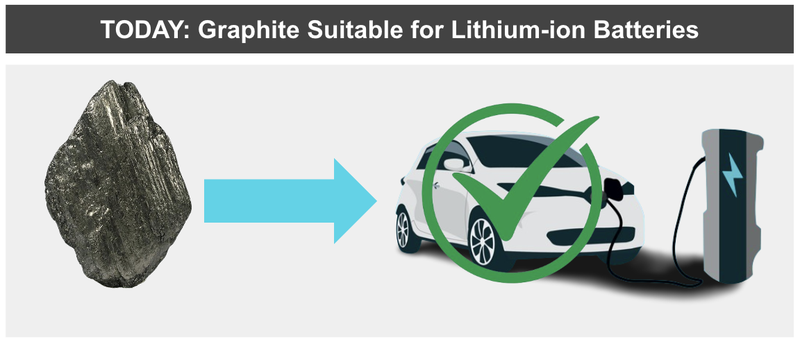

SGA’s graphite tested in batteries - consistently outperforming synthetic graphite

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,251,500 SGA shares and 1,466,250 SGA options, the Company’s staff own 18,000 SGA shares and 7,500 options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

It works.

In batteries.

Our graphite Investment Sarytogan Graphite (ASX:SGA) ticked off its biggest milestone yet.

SGA just showed that its graphite can be effectively used to make lithium-ion batteries.

AND it consistently outperforms synthetic graphite equivalents.

Today’s performance testing results were from SGA’s uncoated spherical graphite.

Test results from SGA’s coated spherical graphite should make the performance even better.

Now that we know SGA’s graphite works in batteries the next stage of work will be on optimising and then getting SGA’s graphite qualified by battery makers.

Ultimately, that's when the potential for offtake deals comes into play.

In the background, SGA is advancing its Pre Feasibility Study (PFS) which will get us a look at the project economics. We think the PFS could show a low cost operation relative to SGA’s peers...

(More on why we think that later).

SGA’s PFS is due in Q3 this year.

In today’s note we will provide an update on SGA’s news, what it's planning next, and provide an update on the macro environment for graphite following our attendance at a INDABA Cape Town presentation this week - key graphite companies Syrah (producer) and General Motors (buyer) were on the panel.

Sarytogan Graphite

ASX:SGA

We first introduced SGA to our Portfolio back in July 2022 and called it our Small Cap Pick of the Year in December 2022.

At the time SGA already had:

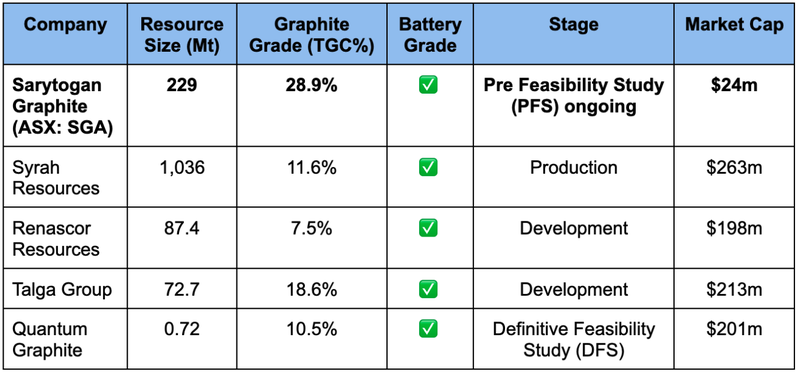

- The highest grade graphite resource on the ASX - Higher grades typically lead to lower costs of processing a resource into a final saleable product.

- The second largest graphite resource on the ASX in terms of contained graphite. Second only to Syrah Resources, which is capped at $263M.

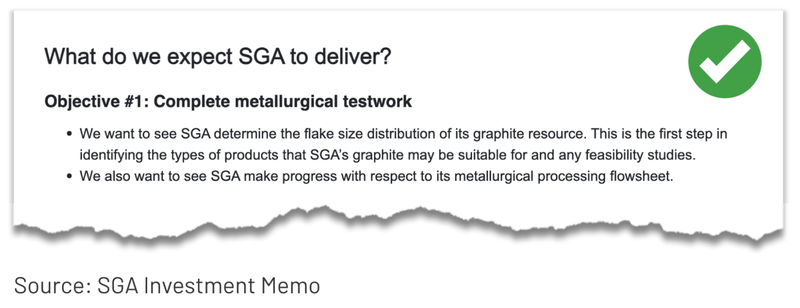

The key question mark over the project was the metwork and whether the graphite would be suitable for use in lithium ion batteries.

Metallurgical Testwork (or Metwork) is the process of taking samples of graphite and trying to reach an extremely high level of purity.

Over the last 18 months SGA systematically de-risked its project, achieving 99.998% battery grade purity.

Once achieved, the next stage is to see if the graphite is suitable for batteries.

Today SGA has demonstrated its graphite can be used in batteries.

With this, it marks the completion of the first objective we wanted to see SGA complete:

Next, SGA will run longer term battery performance steps to qualify its product even further.

The goal is to qualify its product with different battery makers to form the basis of future offtake agreements.

These offtake agreements we see as large potential catalysts for the company and a sign that SGA is advancing the feasibility stage of the company lifecycle.

On top of this, SGA is currently undertaking a PFS which is scheduled to be published for Q3 of this year.

So how did SGA’s graphite perform in the batteries?

For SGA to secure offtakes with different battery makers, it will need to show that its graphite is equal or superior to existing products - and for SGA it will want to make sure it can produce profitably - so the cheaper to produce the better.

So, how did the graphite stack up when it was put into a battery?

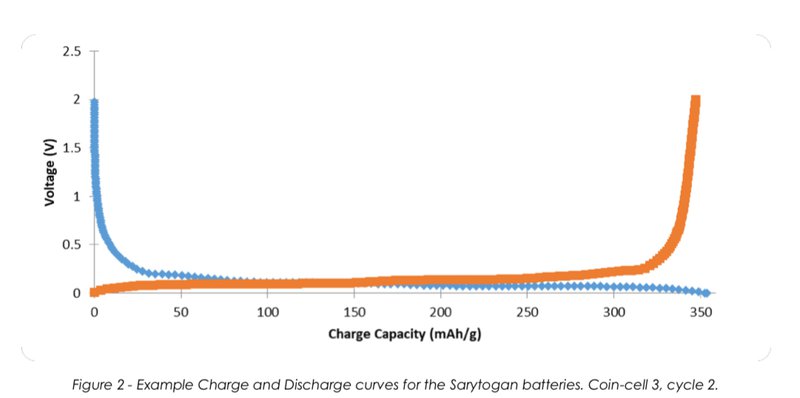

1. Strong performance relative to EV batteries

SGA’s graphite returned performance metrics of 342-347 mAh/g across six different battery tests.

This is higher than synthetic graphite products used in EV batteries, which typically return 330- 345mah/g.

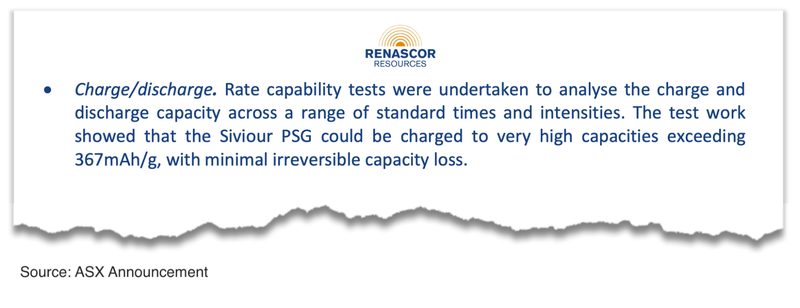

For context on the results - SGA’s peer Renascor Resources achieved performance metrics of 367mah/g after longer term testing.

(Source)

So SGA’s performance ranks amongst the results that much bigger companies are achieving... AND more importantly exceeding the capacities required for use in EV batteries.

For context, SGA’s market cap is just $24M, whereas Renascor’s is $198M.

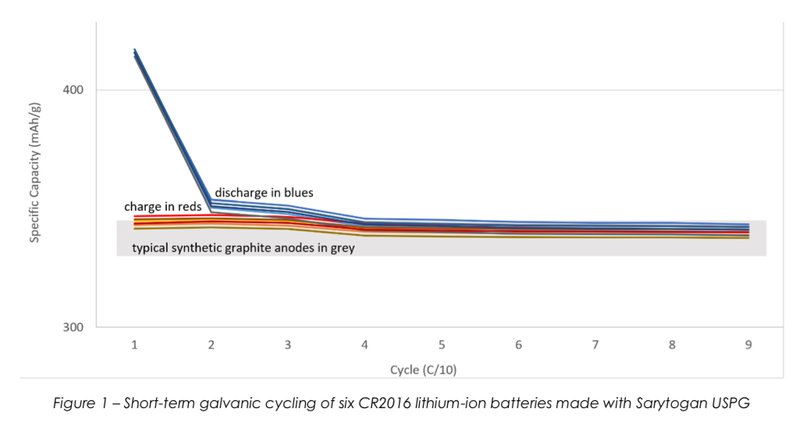

2. Consistent performance during charging/discharging

The cells made using SGA’s graphite showed no significant degradation over nine charge/discharge cycles.

Graphite that isn't suitable for batteries would have started to show signs of degradation as the rounds went on.

AND there is still room for improvement - SGA is still looking to turn its graphite into coated spherical graphite, which should improve battery performance even further.

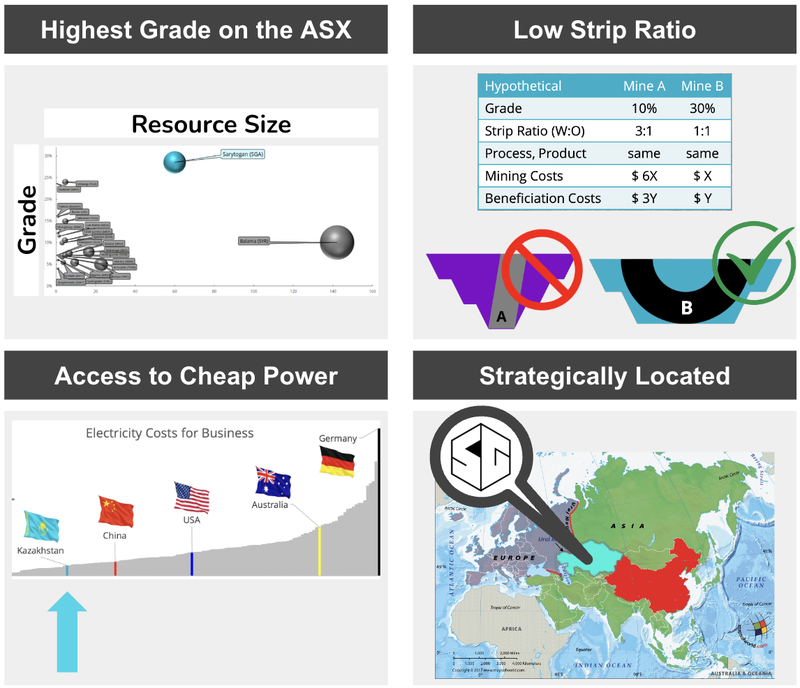

What makes SGA’s graphite so appealing

SGA’s graphite resource has three key differentials that make it unique from a resource perspective:

- The size of the deposit

- The grade of the deposit

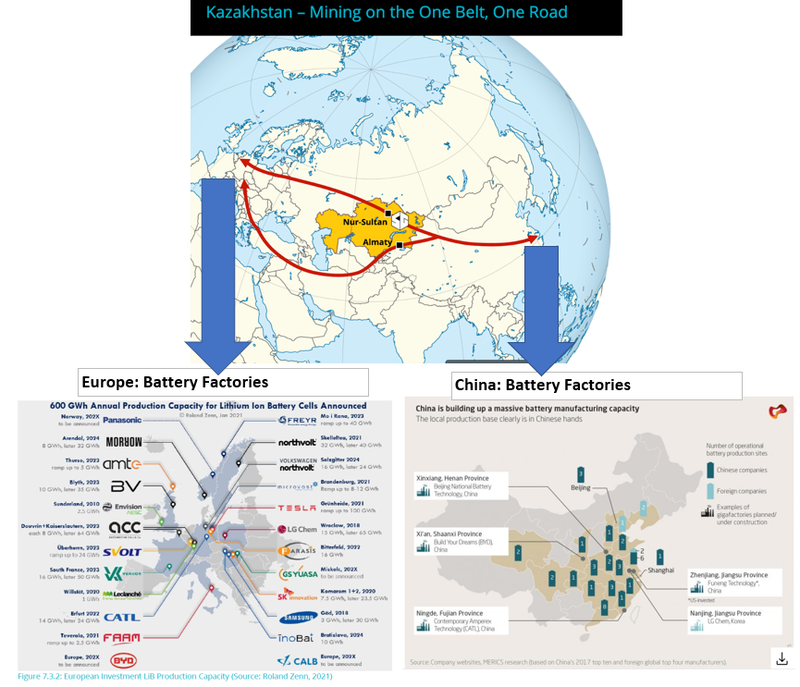

- Its proximity to end users

When it comes to mining, being able to produce a low cost product is one of the key things that helps a company thrive in the good times and weather the bad times.

To have a low cost of production, a resource needs a high grade, a low strip ratio and access to cheap power.

SGA’s graphite deposit has all three of those.

It is the...

- The highest grade graphite project on the ASX - meaning for every tonne of rock that is mined, SGA gets more graphite out then most of its competitors.

- Low strip ratio graphite project - Because SGA’s resource is mostly outcropping, meaning SGA just needs to dig the stuff out instead of mining waste rock before getting to the resource like most underground/open pit mines.

- Access to cheap power - Access to some of the cheapest power across China/US/EU and Australia.

- Strategically located between China and Europe - once the ore is mined, SGA can get it to key markets in Europe and China for the lowest cost.

We went on a site visit to the project in 2022 and were literally walking on top of the graphite resource - see our site visit write up here.

SGA is ticking a lot of boxes, but we will have to wait for the PFS to get a more accurate and specific idea of the economics of the project - due Q3 this year

Looking at it using first principles however, it appears that SGA’s project is cheap to mine and ship battery-grade graphite to end users considering its strategic location in between China and Europe.

How SGA ranks against its peers

Since making our first Investment in SGA in 2022, our view was that as the project was de-risked from a metwork perspective, the market would re-rate it to a market cap in line with its graphite peers.

Right now, SGA has done all of the testwork proving its graphite can perform well in lithium-ion batteries AND is now just a few months away from a maiden PFS.

However - the re-rate hasn't happened... yet.

We attribute this more to the macro environment being less conducive for riskier investments than anything related to SGA’s assets.

We continue to hold a large position in SGA.

SGA is currently capped at ~$24M, whereas most of its peers trade in the $200M range.

SGA’s key catalysts:

Beyond today’s result, here are some of the key catalyst that we think the market wants to SGA achieve for the company to re-rate against its peers:

Pre-Feasibility Study

This catalyst is expected in Q3 2024.

At this point, the project economics are largely unknown to the market.

We think if the Net Present Value (NPV) numbers are big, then the market could be wrong footed, depending on where SGA’s market cap is at the time.

SGA has mentioned a 50 year mine life in its recent quarterly, which is still only a small portion of its resource.

SGA also confirmed in the quarterly that the operation modelled in the PFS would aim to produce ~50,000tpa.

This scale is modular, and many future modules could be built - limited only by the size of the market and the availability of capital.

The initial 50,000tpa of concentrate can then be turned into three different products with different price points when it comes to selling.

- Micro-crystalline graphite at > 80% TGC after flotation for industrial uses

- USPG at > 99.95% TGC for lithium-ion battery anodes; and

- UHPF at > 99.95% for other battery and advanced industrial uses.

So SGA would be selling into three different markets and not just into batteries.

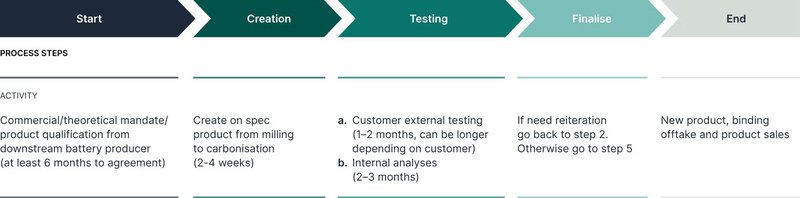

More Battery Testing Results

SGA is still going through the testing process for its Uncoated Spherical Graphite in batteries - we expect to see updates on longer term testing results over the coming months.

On top of that SGA mentioned that it would run further tests with Coated Spherical Graphite which should mean performance improves.

So we expect to see SGA improve on its already significant first pass results from today.

Offtake Agreements?

Now that SGA has demonstrated that its graphite is suitable for lithium-ion batteries, the company is likely getting close to starting product qualification/offtake discussions with battery manufacturers.

In today’s announcement, SGA makes mention of the need to hire a Marketing Manager, which will promote SGA’s graphite specifications amongst potential customers, and a move towards offtake agreements.

Sounds like they are getting serious on this front, and given the unpredictable nature of these types of negotiations, SGA could deliver an offtake announcement at any time.

Depending on the terms of any offtake agreement that SGA secures, if it is a favourable deal it could beat the market expectations.

Complimentary Projects

SGA has an established team in Kazakhstan, a jurisdiction that is very mining friendly.

It has a second exploration project that is in the very early stages and has been drill testing recently.

With a current downturn in sentiment for battery metals, SGA may be in a position to pick up an additional asset on the cheap in the country.

Our view is that as SGA delivers on some of the above catalysts, the more value is delivered into the project and the higher the market cap re-rates in line with its ASX peers - assuming the cyclical macro environment for investing in early stage stocks returns to an upswing.

Ultimately, we are long term SGA holders and want to see the company take its project through the feasibility study stage and into a position where the company achieves our “Big Bet”.

Our SGA “Big Bet”

“Given this graphite project’s strategic location in between China and Europe, we hope that if SGA proves out the size and economic extractability of the resource, it will generate interest from major mining companies, leading to a takeover of SGA for $1 billion+.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The Graphite Macro investing thematic - what’s happening?

Two of our team have been in Cape Town for Indaba this week.

They attended a presentation “Is graphite the forgotten green mineral?” - which had a range of interesting panellists, including a representative from General Motors and Shaun Verner the CEO and MD of Syrah Resources:

Here are the key themes that emerged from the discussion:

- The need for Inflation Reduction Act (IRA) compliance - the IRA has far reaching consequences for potential graphite producers and guides their decision making.

- The opaque nature of pricing - the current graphite market is not mature enough. If analysts can’t get a firm grip on prices, large, established financiers won’t step in.

- The need for more supply outside of China - suppliers want to ensure that the provenance of the graphite is sustainable and secure (especially in light of recent Chinese graphite export controls).

- And the big one...GM’s representative said candidly that the company's intention is to secure supply outside of China. (We’ve seen what a Tesla offtake did for Syrah Resources back in December 2021)

It all makes for a really interesting time for us to be Invested in graphite.

And for a long time now we have held the view that the graphite market could run...

Our view was that as demand for electric vehicles (EVs) increased, demand for graphite would increase with it, and graphite projects would be bid up the same way lithium explorers and developers were over the last few years.

So far it hasn't really played out that way with synthetic graphite substitutes coming on to the market and fixing any spikes in demand.

But we think that the graphite supply chain is one of the most fragile when it comes to battery metals.

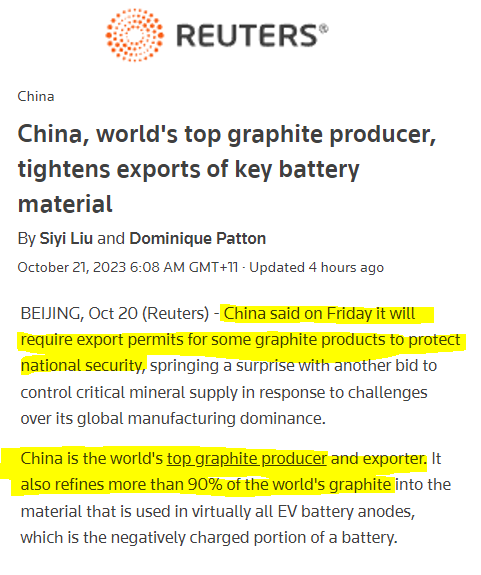

Over 80% of graphite and almost 100% of graphite battery anodes are currently produced in China.

AND the Chinese government recently announced export restrictions on some graphite products to “protect national security” potentially putting most of the world's graphite supply at risk.

(Source)

We wrote about why we think things might be starting to change for the graphite sector (for the better) in a previous SGA note here - Graphite macro theme about to go exponential?.

What are the risks?

After today’s announcement, SGA has de-risked its project from a metwork perspective in a big way.

BUT there is always still more work to be done.

SGA now needs to take its graphite and get it qualified by the battery makers.

That is where SGA takes its graphite products and the battery makers run their own tests to see if the product is suitable in their batteries.

This process can take a while to complete (up to 2 years in extreme scenarios) AND there is never a guarantee that SGA gets past the qualification stage.

So a key risk in the short-medium term will be “product qualification risk”.

To see more risks that we listed as part of our SGA Investment Memo click here.

Our SGA Investment Memo

Below is our Investment Memo for SGA, where you can find a short, high level summary of our reasons for Investing.

In our SGA Investment Memo, you’ll find:

- Our SGA Big Bet

- Key objectives went want to see SGA achieve

- Why we are Invested in SGA

- What the key risks to our Investment Thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.