Saudi Arabia's spending spree: From football to battery metals

Published 05-AUG-2023 12:00 P.M.

|

10 minute read

What do football superstars, golf and battery metals have in common?

Saudi Arabia is coming for them.

The Saudis recently offered French soccer player Kylian Mbappe US$1.1BN to play in their domestic league for just one year.

They have also signed a host of ageing stars to its local competitions for eye watering sums of cash.

Last year the Saudis signed Cristiano Ronaldo on a >$300M deal. In 2023 the Saudis spent over ~A$800M on other players.

Not to mention earlier this year they pretty much purchased the entire sport of golf.

But sport is not the only thing the Saudis are investing in...

Earlier this week a Saudi state owned company wrote one of the biggest cheques in the mining industry we have seen.

A US$2.6BN investment into Vale’s base metals (copper/nickel) business.

(Source)

The Saudis have been writing some mammoth cheques trying to diversify its revenue stream away from oil and into other markets.

Whether it's buying the best soccer player in the world, the sport of golf or a battery metals mining project, the Saudis appear to be on a big spending spree.

This deal with Vale was done through Saudi state owned mining company Ma’aden.

It also marks the first of what we think will be many investments by the Saudis in the battery metal space.

The battery metals space is going through the adoption cycle that is typical of high-growth industries over a 10+ year period:

- 2016-2018 the early speculators invest and get washed out after companies start going bust because the demand side is still in its infancy .

- 2018-2020 a few majors with strong balance sheets swoop up all of the good projects in the industry and position themselves as leaders in a down market - think Pilbara’s takeover of Altura out of administration, the assets of which have helped Pilbara build up a ~$3.3BN cash balance between now and then.

- 2020-2022 macro themes like the energy transition and de-globalisation drive real demand for the product and institutional and corporate investment capital flows into the sector - think the Stellantis investment into our portfolio company VUL (and later into KNI). European and US governments start passing legislation (with funding) to promote battery metals mining.

- 2022- 202X?, we are at the stage where the sector is big enough to absorb large amounts of capital, the big sovereign wealth funds & corporate balance sheets that previously saw the space as too small to make any meaningful investment can now start to get involved. Another round of M&A is starting to occur in the sector.

We see the Saudis’ first investment as further confirmation that the battery metals boom is here to stay AND that we will see more of these types of deals in the coming years.

It makes sense too.

The Saudis are using the (estimated) $1.2 trillion dollar war chest built off the back of oil and gas profits to enter into the new wave the energy transition.

Diversifying their portfolio, the Saudi Public Investment Fund is protecting the nation’s wealth from energy substitution risk.

The Saudis have been lurking in the shadows waiting to write cheques for a while... in 2022 the first ever Future Minerals Forum was run in Riyadh.

The conference signalled to the world that the biggest oil producer on the block was ready to enter the mining space.

We expect the Vale deal to be the first of many.

We think the Saudis will start with investments in the larger “blue chip” end of town and then slowly make their way down into smaller developers/explorers once they get their feet under the table.

For now, it will be the projects with scale and companies capped in the multi billions of dollars that are on the Saudi radar.

Big cheques being written for lithium projects

A level down from the state-backed Saudi Sovereign Wealth Fund is capital from big private companies.

This week the world's biggest lithium producer Albemarle announced a 66% increase in its profits - its cash balance now sits at US$1.6BN.

With the proceeds Albemarle invested CAD$109M into James Bay lithium explorer Patriot Battery Metals.

The Patriot deal is in addition to the now rejected $5.5BN offer Albermarle made for ASX listed Liontown Resources.

(Source)

Another major hunting for lithium deals is Rio Tinto - this week the company’s Chief Executive Officer (CEO) Jakob Stausholm said the mining giant was on the prowl.

He specifically mentioned that he “wouldn’t mind having lithium production in Canada”.

(Source)

Rio isn't the only giant lurking in the lithium space.

One of the world’s biggest oil producers Exxon also confirmed this week that it was in discussions with Tesla, Ford and VW on becoming a lithium supplier to the automakers.

(Source)

The discussions follow on from the Exxon US$100M buyout of US lithium developer Galvanic Lithium - Galvanic owned a lithium brine project in the Smackover Basin in Arkansas, USA.

The most surprising thing? - Exxon isn't the only oil and gas major looking at lithium assets...

French oil and gas major $137BN Equinor has previously invested in Lithium De France and US shale producer $82BN Occidental Petroleum which has a stake in TerraLithium.

Investment in lithium projects from companies like Albemarle and Rio Tinto makes perfect sense.

They are mining/chemicals giants with expertise in mining and producing battery grade chemicals.

It makes sense for them to take a stake in developers/projects, and use the years of mining knowhow, talent and operational IP to run these mines as profitably as possible.

The move from Exxon however seems more unusual... until you understand a bit more about how lithium is produced.

Oil and gas majors are specialists in extracting liquids/gases from underground, processing them into saleable products and then finding buyers for their products.

We think this is the reason why we have seen the investments going primarily into the lithium brine space.

For some context there are two types of lithium projects - hard rock and brine projects.

- Hard rock projects are mined using conventional mining methods (think blasting, digging, crushing). These are the types of projects that Albemarle and Rio Tinto like.

- Brine projects are mined using extraction wells, evaporation ponds and refining technologies. These are the types of projects that Exxon likes.

We have Investments across both types of projects and each of them come with their own risks and benefits.

But one thing is for sure, there are big players entering the lithium space, and we think that it is just the beginning.

We have put together a comprehensive ebook about the lithium stocks we are Invested in for 2023 and beyond:

✅ Our 10 Lithium Stock Investments: 10 lithium stocks that we’ve Invested in and believe are primed for growth in 2023 and beyond.

🔍 Market Trends & Analysis: We share our opinions on the current lithium market landscape. Learn how global trends, EV adoption, renewable energy initiatives, and technological advancements are shaping the future of lithium investments.

✅ Different types of lithium projects: We have collated our insights into the different types of lithium projects, and the effect of new technologies on lithium supply.

💡 Our Insights: We have been Investing in small cap stocks for many years and closely following the battery metals sector since 2018, we share what we have learned in this ebook

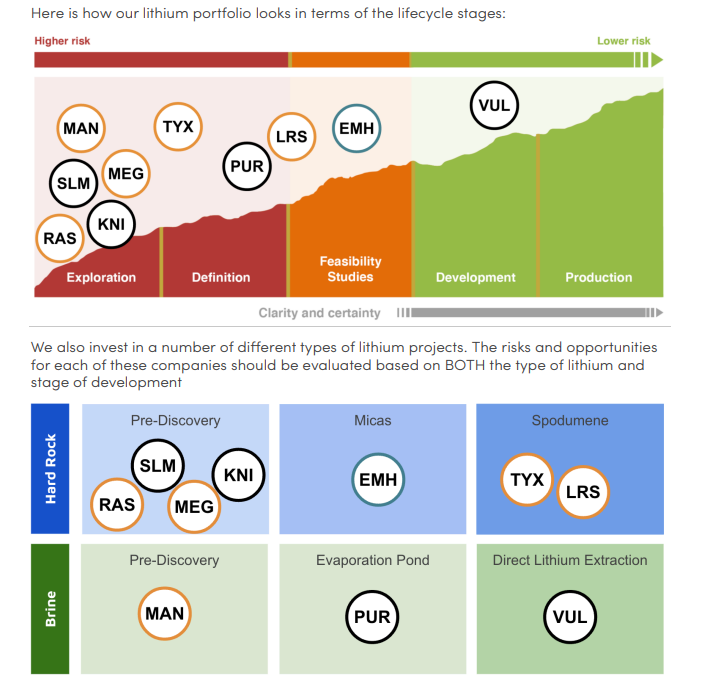

We are Invested in both hard rock and brine projects:

Not all lithium projects are built the same.

Where a project is located and the type of project it is (hard rock vs brines) has a big impact on the probabilities it one day becomes a mine/takeover target.

We take a portfolio approach to Investing in the lithium space and have exposures across different types of projects in a range of geographies.

Here is the list of the ten lithium stocks that we are invested in for 2023 and beyond.

- Vulcan Energy Resources (ASX: VUL) - Geothermal lithium brine project in Germany.

- Latin Resources (ASX: LRS) - Hard rock (spodumene) lithium in Brazil.

- Pursuit Minerals (ASX: PUR) - Lithium Brine in Argentina.

- Tyranna Resources (ASX: TYX) - Hard rock (spodumene) lithium in Angola.

- European Metals Holdings (ASX: EMH) - Hard rock (micas) lithium in the Czech Republic.

- Megado Minerals (ASX: MEG) - Hard rock in Canada

- Mandrake Resources (ASX: MAN) - Lithium brine in Utah, USA.

- Solis Minerals (ASX: SLM) - Hard rock (Spodumene) lithium in Brazil.

- Kuniko (ASX: KNI) - Hard rock lithium in Canada.

- Ragusa Minerals (ASX: RAS) - Hard rock lithium in NT, Australia.

To find out more about these companies and our take on the lithium market, read:

What we wrote about this week 🧬 🦉 🏹

GTR is leveraged to growth in US uranium demand

This week the US senate voted in favour of a law supporting the domestic uranium industry. The US was once the largest producer of uranium in the world; now it imports ~95% of its uranium supply. We put out a new GTR Investment Memo listing all the reasons why we are Invested in the company.

Weeks away: NHE drill rig is heading to Tanzania to drill large helium target

This week NHE confirmed that its drill rig is now on move and expected to be in Tanzania in late August/early September. NHE will be drilling its Mbelele-1 well later this quarter where its targeting a 15.7 billion cubic feet (BCF) prospective helium resource.

88E flow test this drilling season as rights issue announced

This week 88E launched a rights issue looking to raise $12M at 0.6c per share. With the flow test of its Hickory-1 well planned for later this year/early 2024 we will be taking up our rights and increasing our Investment in 88E.

Quick Takes 🗣️

IVZ: The latest from IVZ’s Managing Director Scott Macmillan

EXR: EXR update on its drill program later this year

HVY: HVY moves to secure funding via offering royalty interest

88E: 88E raising $12M through a rights issue

TG1: TG1 identifies rare earths and niobium drill targets in WA

GAL: GAL hits sulphides at Jimberlana - more assays on the way.

LYN: LYN granted West Arunta ground near $336M WA1 Resources

Macro News - What we are reading 📰

Uranium

France Looks to Block US Purchase of Velan’s Nuclear Business (Bloomberg)

Record level of US support for nuclear continues : Nuclear Policies - World Nuclear News (World Nuclear News)

First U.S. nuclear reactor built from scratch in decades enters commercial operation in Georgia (NBC News)

US Battery Metals

Arkansas town could become the epicenter of a U.S. lithium boom (Daily Mail)

Lithium

Ellison lashes China in unveiling new lithium strategy (AFR)

IGO’s battery chemical plant fizzes (AFR)

Helium

Hitting the Market Soon: The Entire Federal Helium System (Hart Energy)

US, Europe Growing Alarmed by China’s Rush Into Legacy Chips (Bloomberg)

EVs and Battery Materials

Five Charts That Show the Rise of BYD and the Global Boom in EVs (Bloomberg)

Cyber security

Russian hackers target govt orgs in Microsoft Teams phishing attacks (BleepingComputer)

Hydrogen

South Korea Kepco Joins Western Australia Hydrogen project – Argus (Hydrogen Central)

⏲️ Upcoming potential share price catalysts

Updates this week:

- GAL: Drilling at its Jimberlana & Mission Sill prospects at its PGE project in WA.

- GAL hit visual sulphides and put out the first assays from its Jimberlana target. More assays from the drill program are still pending, see our Quick Take on the news here.

- NHE: Scheduled to drill two targets at its helium project in Tanzania (Q3 2023).

- NHE started mobilising its rig in the lead up to the rig move to Tanzania. See our note on the news here.

- TMR: Maiden JORC resource estimate for its Canadian gold project.

- No news from TMR this week but we did see the following interview with TMR’s CEO Jason Bahnsen here.

- BOD: Phase III clinical trial for CBD insomnia treatment.

- BOD raised $1.9M through a placement at 0.9c per share. See the presentation BOD put out to go with the raise here.

No material news this week:

- TG1: Drilling at its NSW gold project in May.

- LCL: Drilling at its primary PNG copper-gold target.

- IVZ: Drilling oil & gas target in Zimbabwe, Myuku-2 (Q3, 2023).

- KNI: Drilling 3/3 of its Norwegian battery metals projects in Europe.

- SLM: Maiden drill program at its Brazilian lithium project

- LNR: >10,000m drill program at rare earth’s project in WA.

- DXB: Interim Analysis of Phase III Clinical Trial on FSGS (March 2024).

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.