Reflections on 2024: Markets, Moves, and Milestones

Published 22-DEC-2024 15:33 P.M.

|

12 minute read

- Commentary: Moving from $10M to $100M-$200M market cap, the sweet spot. 2024 New Portfolio Additions in review.

- Quick Takes: JBY, L1M, ION, TTM

- This week in our Portfolios: IIQ, BPM, PUR, WHK

Well, that’s pretty much it for the year.

Another bearish year for the small end of the ASX.

But at least the market managed to string together a few bright patches this year.

Most notably during October and November.

We saw a few solid, bull market style cap raises get up in the last quarter.

And it felt like that was the starting gun for a coming Santa rally this December...

Unfortunately, the last handful of trading sessions poured a big bucket of cold water on that idea.

Looks like we get another Santa no-show for the markets this year.

A big worthless lump of nickel in everyone's Christmas stocking.

Or even graphite.

But the Christmas cheer isn't “stolen” so to speak.

Usually a red day or week means the mood around the markets is negative...

This year feels a bit different.

Despite the sell off of the last week, we are actually going into 2025 quite optimistic.

A few of our companies are in seriously good shape from a balance sheet perspective.

(quite rare 2 years into a brutal bear market)

...and while share prices have broadly wilted in the last couple of weeks, they have overall performed well this year.

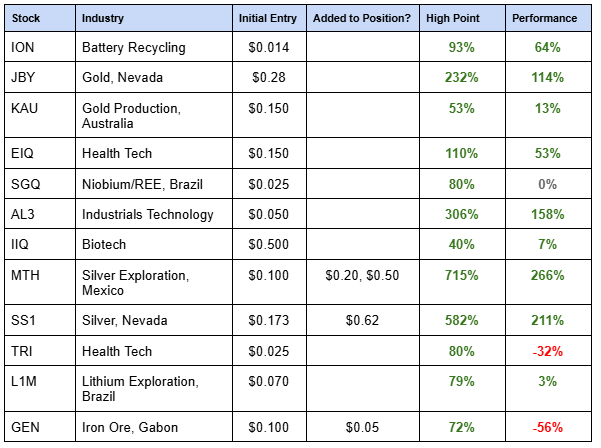

In 2024 we introduced 12 new companies into our Portfolio.

We usually do a max of 8 to 10 in a year, but wanted to slot in a couple of extra this year while company share prices are still beaten down (in our opinion) and in anticipation of a strong 2025.

Every year at some point, we find ourselves reflecting on the way we make Investments and the type of stocks we end up backing.

Our approach is to Invest in the parts of the market where few investors are looking...

And try to react to the border market conditions.

With a minimum 3+ year view.

For us a typical Investment has a market cap between $10M to $50M.

(even smaller sometimes).

The last two years of bear market conditions have thrown up opportunities in more advanced stage companies trading at (in our opinion) very low valuations.

In resources, this year we focused less on greenfield exploration and more on companies with an existing resource but still with exploration upside.

For 90%+ of the market, a sub $50M market cap is considered too small, too illiquid and too high risk to invest in.

For us early stage punters, leaving 5x to 10x on the table to enter an already de-risked company at a higher market cap does not compute.

... but for most investors, $200M market caps are considered “small caps” and the minimum market cap they will consider investing in.

The biggest funds wont touch anything sub $1BN market cap.

Our approach is to try and find the stocks that the market has overlooked and are still too early stage for the big money to come in.

Companies that could eventually deliver enough success to grow into market caps that attract capital from the bigger end of the investment community.

Broadly, we are looking to back companies that can go from a ~$10M market cap to $100-200M...

and then with a bit of management execution, right macro timing and luck... to $1BN.

This almost mythical 50x to 100x is a very rare result.

You need to “kiss a lot of frogs” to get one...

The first re-rate from ~$10M to $100-200M is generally our sweet spot.

We have followed, observed and Invested in many $10M to $100-200M stories over the years and have seen enough to have formed strong opinions.

On what needs to go right... and what can go wrong.

This is where we think we have the biggest edge in picking potential winners.

(based on our learnings from getting many wrong over the years)

We have been on fewer ~$200M to $1BN journeys.

At this point of a company's lifecycle the proverbial “grown ups” join the company board and big institutional funds come onto the cap table.

The company becomes less “entrepreneurial” and more about building and scaling a serious and real business.

In preparation to attract the next level-up of serious institutional investors.

So we grab the popcorn and watch while trying to learn a thing or two.

The year that was for our 2024 Portfolio Additions...

Like any typical small cap Portfolio there are a few winners and a few stragglers.

We have also seen how quickly fortunes can change for a company... for better or worse.

2023 was a year to forget for us (and most small cap investors).

2024 was a tough market but we think we had a decent year given the conditions.

Our strategy to switch focus to finding undervalued later stage companies seemed to work.

At the start of the year we placed a big bet on precious metals gold and silver.

SS1 and MTH were our two best performing stocks, delivering significant re-rates and bringing in big funds at higher prices to our Initial Entry Price.

It all fell into place for MTH when the company announced in September 33.00m @31.8g/t gold, 274g/t silver from surface.

These drill results sparked the share price rally from ~10c to a high of 81.5c.

For SS1, we got a little bit lucky...

We got in just before a solid run in the silver price.

SS1 became the largest undeveloped primary silver resource on the ASX this year after an upgrade to its resource...

SS1 also uncovered antimony on its project one week before China banned antimony exports.

(Antimony was the best performing commodity of 2024, growing 270% year on year).

It was a big year for two of our new tech investments as well, EIQ and AL3 both made significant progress.

AL3 launched its US operations selling 3D printing robots and 3D printed parts to the US Navy and other industrial users.

This was helped by a big $30M raise which allows the company to accelerate its growth.

(its always a strong sign to see “scale up” capital being raised, as opposed to “survival” capital that we are seeing from many companies)

EIQ also secured FDA clearance for its AI-based algorithm that can detect heart issues from echograms (heart images).

From that, EIQ secured a reimbursement code worth up to US$100-150 per scan, approximately double what the company had originally anticipated.

Next year is all about getting into more healthcare providers for EIQ, and it already has one big flagship US-based hospital as a partner.

Our most recent technology investment was ION, which has established a “dream team” to commercialise a battery metals recycling technology.

ION is a bit further away from commercialisation when compared with AL3 and EIQ, with a smaller market cap to reflect the earlier stage.

We think that the technology and the team behind it can deliver in 2025.

ION has been defying the broader market fade away over the last two weeks hitting another new high this week since we Invested.

Gold was one of the big movers of 2024, starting the year around US$1900 and getting as high as US$2800.

We made two big bets on gold this year - JBY and KAU.

KAU is the first gold producing company that we have Invested in.

As a mine turnaround story, KAU is heavily leveraged to a strong gold price and any upside discoveries that can be made from the existing A1 mine that has been around since the mid-1800s.

JBY is also looking to drill out its gold prospect in Nevada, USA.

We like Nevada as a jurisdiction (with the success from SS1), and we think that JBY’s gold project can deliver in a jurisdiction that puts some of the biggest gold producers on the map.

(Think Barrick’s Goldstrike project).

On the biotech front we Invested in IIQ.

IIQ delivered positive results from its cancer detection technology within the timeframe set by the company at the start of the year.

We think that 2025 could be a big year for IIQ as it advances these technologies and finds a partner to take its breast cancer monitoring tool to market.

In the medtech space we Invested in TRI.

TRI set new benchmarks for its AI-based algorithm to detect mental health issues from a person’s sleep.

Importantly, TRI published data that unlocked the potential for its product to be used in wearable technology like smart watches.

Although we have Invested in a lot more later stage companies this year, we did find space for at least one higher-risk, high-reward exploration play.

That company was L1M, exploring for lithium in Brazil.

For the past 12 months L1M has done all of the work to firm up quality assets and drill targets to set itself up for a big drill campaign that is set to commence in the first quarter of next year.

Like all early stage exploration, anything can happen.

From our 2024 vintage the most disappointing Investments at this point in time are probably GEN and SGQ.

GEN is a late stage iron ore company with an asset in Gabon.

We had hoped that GEN would make more progress this year towards a Final Investment Decision and announcing a financing package to build its project.

However, since our Investment at the start of the year the iron ore price has come off from US$135 at the start of the year to a low of $90, but now back to $105.

And GEN’s guided financing package still hasn't been announced.

So some macro bad luck and project financing delays forced GEN to do another cap raise at 5c, half of our 10c Initial Entry Price (we decided to participate in this 5c round too)

Like all our Portfolio companies, GEN is a long term Investment for us.

SGQ has also had a rough start in our Portfolio, with delays in finalising the acquisition of its advanced stage niobium and rare earths project in Brazil.

SGQ has been stuck in suspension purgatory while the capital raising to fund the project acquisition finalises.

We look forward to SGQ finally getting it done and then following the progress of the project in 2025.

So we had some good results and a couple of bad starts,

All in all we had more good results than bad this year.

And because the companies that did experience issues were later stage assets, the share price drops weren't as bad as you would see in a failed greenfield explorer.

Keeping in mind, a single year is not enough time to grade the performance of a small stock.

These stocks need time to execute their plan to deliver a material re-rate.

Our general plan is to hold for at least 3+ years to give the company enough time to make some serious progress.

And hopefully get some wind in the sails from a positive swing in sentiment for its macro theme...

And a broadly better small end market in 2025.

What we wrote about this week 🧬 🦉 🏹

Inoviq (ASX:IIQ)

Inoviq (ASX:IIQ) confirmed it has successfully completed stage 1 of its development program for an exosome therapeutic for breast cancer.

IIQ was able to engineer cells to continuously produce exosomes that specifically target and kill breast cancer cells.

After their Proof of Concept study, IIQ says to expect more valuable lab data to come in the first half of 2025.

Read: 🧬 IIQ: Exosomes successfully weaponised - cancer cells located and killed in proof of concept study

BPM Minerals (ASX:BPM)

In September, our micro cap gold explorer BPM Minerals (ASX:BPM) made a new gold discovery in WA.

The discovery hole saw BPM’s share price spike by ~200%.

(it has since come back down again...)

BPM’s next step after the discovery hole was to drill deeper underneath, to test if the gold extended 600m below.

BPM has just finished this deeper drilling.

...and gold assay results are due in the coming weeks.

Read: ⛏️ BPM: Drilling completed at Claw. Gold results due in a few weeks.

Pursuit Minerals (ASX:IIQ)

Last week PUR upgraded its lithium carbonate JORC resource to 1.1mt at 506mg/li.

Almost 3.5x higher than its previous resource estimate.

AND PUR is looking to have its 100% owned 250tpa pilot plant producing lithium carbonate in Q1 2025.

Read: ⛏️ PUR: Big Resource Upgrade. Plant Firing Up. First Production in a Few Months?

WhiteHawk (ASX:WHK)

Last week our micro cap AI and cybersecurity Investment, the A$5.7M capped WhiteHawk (ASX:WHK), signed a 2-year, US$2.4M contract extension

...with a “top 5 global social media company”.

(WHK can’t reveal the name due to sensitivity around cyber security... but you can probably guess who it is)

A contract RENEWAL of this size shows that the WHK’s AI cybersecurity tech is valuable to customers.

After a full year of usage, this giant organisation decided they like WHK’s tech enough to renew for 2 full years.

Quick Takes 🗣️

JBY finding more gold in old drillcores

L1M Reveals Lithium Drill Targets in Brazil

ION Partners with University of Adelaide in the ARC Battery Recycling Initiative

TTM provides Dynasty drilling update

Macro News - What we are reading & listening to 📰

Battery Metals:

Congo Sues Apple Alleging ‘Pillaged’ Minerals in Products (Bloomberg)

- The Democratic Republic of Congo filed lawsuits in France and Belgium accusing Apple of using "blood minerals" from conflict zones in its supply chain.

- Apple disputes the claims, highlighting its commitment to responsible sourcing, use of recycled materials, and suspension of mineral sourcing from the DRC and Rwanda due to conflict.

Graphite:

US backs graphite factory to loosen China’s EV supply chain grip (Financial Times)

- The US granted Novonix a $755M loan to build North America's first large-scale synthetic graphite factory, reducing reliance on China's 95% market share in battery graphite.

- The facility in Tennessee will produce enough graphite for 325,000 EVs annually by 2028, bolstering US supply chains amid China's export restrictions.

US Graphite Firms Seek 920% Duty to Thwart China on EV Material (Bloomberg)

- US graphite producers seek tariffs up to 920% on Chinese imports, citing unfair

- subsidies, risking EV battery cost spikes.

- China controls 92% of battery-grade graphite; US ramps synthetic graphite production but struggles to meet demand.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.