Global shifts in bauxite demand and supply.

Published 18-JAN-2025 17:09 P.M.

|

14 minute read

- Commentary: Monday: New Pick of the Year Announced - a tier 1 bauxite deposit. What is bauxite? Why is the bauxite price running over the last few months?

- Quick Takes: SGQ, EXR

- This week in our Portfolios: SS1, KAU, CND, L1M

On Monday morning (around ASX market open) we are announcing a new Pick of the Year for 2025.

This Pick of the Year is in the category of “later stage resource companies”.

(where we have been having some good results over the last 12 months)

This company is developing one of the largest undeveloped, high grade, direct shipping bauxite deposits globally - in Cameroon, Africa.

It’s the 8th largest bauxite project in the world, with a 1.1 billion tonne resource + reserve.

High grade, low impurity bauxite - near rail for export.

What on earth is bauxite?

Bauxite is the bulk material used to make aluminium.

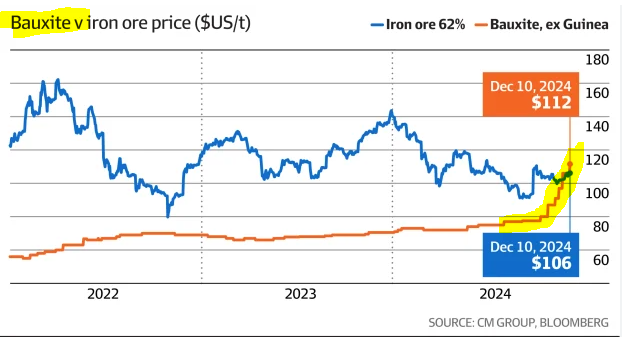

The bauxite price has been moving up strongly in recent months - a few weeks ago the bauxite price surpassed the iron ore price. We will explain why shortly.

Last week we wrote that global uncertainty is a key investment theme for us in 2025.

Part of that theme is defence supply chain raw materials as global uncertainty leads to increased defence spending in most countries.

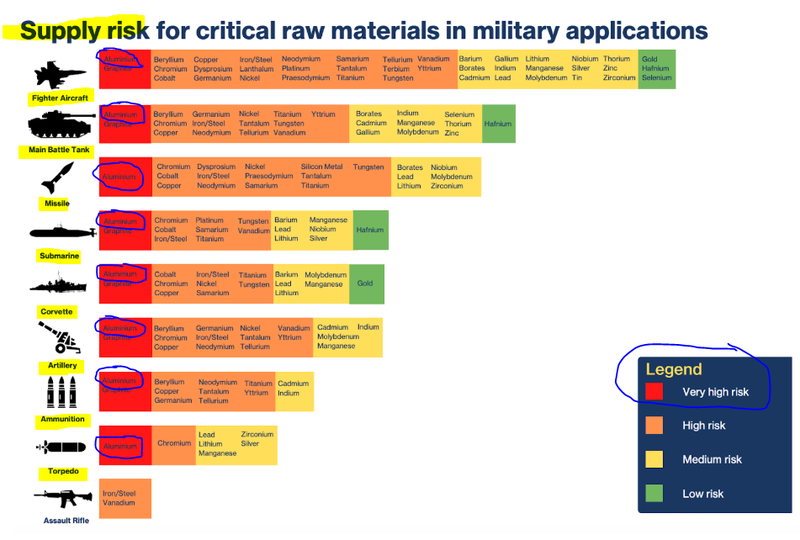

Aluminium is listed as a “very high supply risk” category in the 32 NATO member countries list of defence-critical materials for making tanks, fighter planes, submarines, artillery and ammunition.

You might have to squint to read aluminium in the image below - basically aluminium is a red ‘very high supply risk’ for almost every military application (we circled aluminium in blue):

(Source)

Aluminum is lighter than steel - it makes ships, planes and vehicles more efficient and faster.

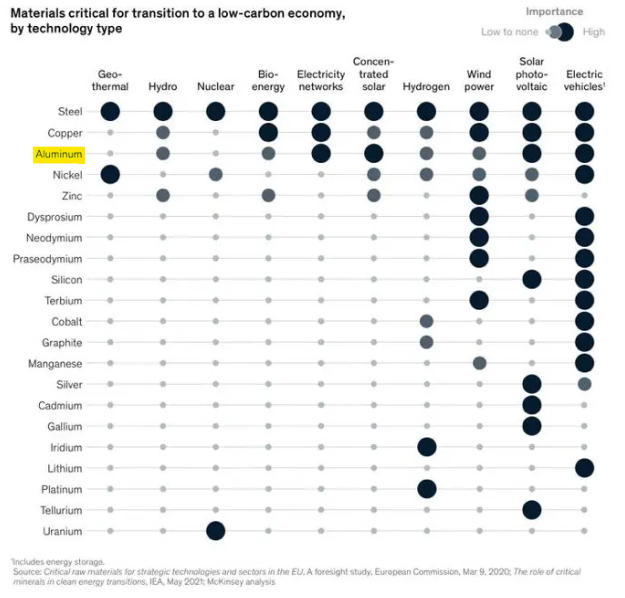

Aluminium is also a critical metal in electrification - electric networks and transmission, solar, and electric vehicles all use aluminium in some capacity.

(Remember this critical “electrification” metals list):

Not to mention aluminium’s use in all sorts of household items, construction materials and packaging.

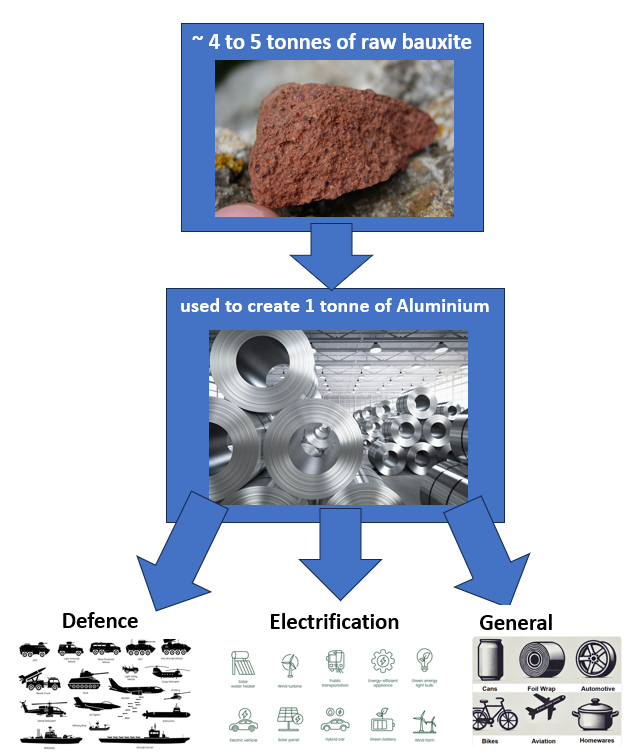

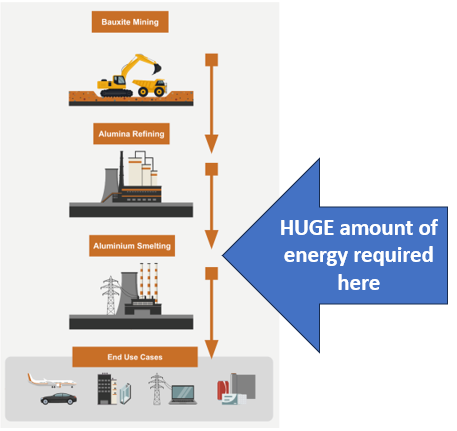

Aluminium is made by refining and then smelting a bulk raw material called bauxite.

It takes around 4 to 5 tonnes of bauxite to make ~1 tonne of aluminum.

(The only other way to make it is by recycling scrap metal)

400M tonnes per year of aluminium is sold globally.

The global aluminum market size was US$169 billion in 2023.

It is forecast to grow to US$311 billion by 2033.

Producing that amount of aluminium is going to need a LOT of new bauxite...

Over the last 3 months the bauxite price has been rising... and rising.

(Source)

Why?

Bauxite supply is depleting...

and certainty of supply risks from current, major bauxite exporters are materialising.

There are plenty of aluminium smelters in different countries around the world, happily turning bauxite into aluminium for all the end uses listed above.

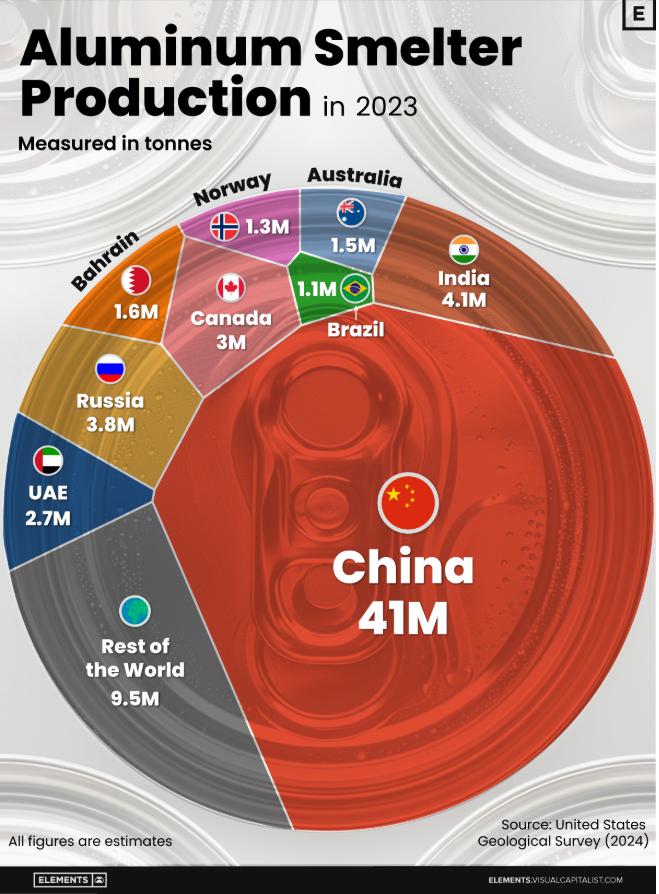

China produces over half of the world’s aluminium.

The 41M tonnes they produced in 2023 is critical to the total global supply of ~70M tonnes.

(certainly not an ideal situation for the security of aluminium supply for defence uses by the US and NATO)

Given it produces over half the world’s aluminum, China has lots of aluminium smelters and smelting capacity.

The growing problem for China is sourcing the bauxite needed to feed these smelters...

China’s in-country supply of raw bauxite (that had been feeding its smelters) has been depleting for the last 10 years.

(Source)

(Source)

To solve this problem, China now imports a lot of the bauxite it needs for its aluminium smelters.

Specifically from a country called Guinea, in western Africa.

From January to October 2024, China cumulatively imported 131.74 million tonnes of bauxite to make up its shortfall.

92.09 million tonnes of this bauxite was imported from Guinea, that’s 69.9% of China's total imports.

Enough that any supply disruptions from Guinea pose a material risk to China.

And to global aluminium supply.

(Source)

The supply risks out of Guinea started materialising last year, pushing up the price of bauxite:

(Source)

(Source)

(Source)

(Source)

Guinea is the world’s second largest producer of bauxite.

Real or potential supply disruptions out of Guinea are a big problem for China.

(and the broader global aluminium market).

So now aluminium producers are on the hunt to secure bauxite supply - pushing up the bauxite price over the last 2 years, especially over the last 3 months:

(Source)

On Monday we are announcing our first Pick of the Year for 2025.

There are very few “bauxite” stocks on the ASX.

This company is developing one of the largest undeveloped, high grade, direct shipping bauxite deposits globally - in Cameroon, Africa.

It’s the 8th largest bauxite project in the world, with a 1.1 billion tonne resource + reserve.

High grade, low impurity bauxite - near rail for export.

Why do some countries with producing bauxite mines restrict exports?

This is not the first time that export restrictions have disrupted the bauxite-aluminium market.

Back in 2022-2023, Indonesia (the world’s 6th largest producer of bauxite) announced bauxite export restrictions, cutting off almost 4.6% of global supply.

This was to buy time for Indonesian companies to build their own aluminium smelting and capture the downstream value.

Luckily for the market, the bigger producers could fill that 4.6% gap.

But there’s something bigger brewing in west Africa...

Guinea is the second largest producer of bauxite and top exporter.

If it ever happened, an Indonesia-like export ban in order to build up Guinea’s in-country processing capacity would leave a giant hole in bauxite supply.

(Source)

(Source)

So what’s in it for a bauxite exporting country to restrict/ban bauxite exports?

Countries that have their own bauxite mines AND have built smelters to process that bauxite into aluminium can capture more of the downstream value of aluminium demand.

(Source)

(Source)

Which is fair enough.

The problem is that it takes a couple of years at least to build an aluminium smelter/refinery.

And ongoing HUGE amounts of energy for the actual smelting process.

So bauxite suppliers that want to move into the smelting game are going to need time and energy supply to get there.

Which doesn’t help near term supply issues.

The daily demand for aluminium keeps rolling on.

A good chance for a new company with a giant undeveloped bauxite resource in a different country to step in and develop a mine to plug the supply gap.

Any supply disruptions to bauxite production in Guinea are a big problem for China and the rest of the bauxite market.

It's one thing absorbing disruptions from 5% of world supply like when Indonesia’s export restrictions kicked in, it's a whole other thing trying to fill a gap of ~28%.

If Guinea does what Indonesia did, then it could leave a GIANT ~97 million metric tonne-sized hole that needs to be filled with new supplies.

It is more the fear and uncertainty of export restrictions, more than anything else, that sent prices of bauxite running.

But if any export restrictions are ACTUALLY enforced, we think bauxite prices could push even higher.

In that scenario, where Guinea places export restrictions on bauxite production, then projects with size/scale potential could be funded to fill in the gap.

In late November Reuters reported Chinese mining company Chinalco was considering a US$426M investment into a bauxite project in South America:

(Source)

It appears that China can see the “writing on the wall”, and is positioning for ongoing export issues out of Guinea.

And looking for new sources to fill the potential gaps by diversifying supply.

Between 2010 and 2022 the aluminium market managed to absorb the bauxite export restrictions out of Indonesia...

But our view is that if the same were to happen in Guinea the market would be crippled on the supply side.

Either way the risk of future supply disruptions is now at the front of every aluminium producer's mind, so the hunt for new and diversified supply is on.

We think fear of further supply risks materialising from the current major bauxite exporter will push aluminium refiners to diversify supply sources, creating excellent funding conditions to build and bring online a new mega bauxite mine.

Like our new 2025 Pick of the Year that we are launching on Monday morning.

In the meantime, if you have a spare 90 minutes, check out this interview with bauxite and aluminium expert Alan Clark from a few months ago for a great primer on the industry and market dynamics:

What we wrote about this week 🧬 🦉 🏹

Sun Silver (ASX:SS1)

Our 2024 Small Cap Pick of the Year Sun Silver (ASX:SS1) just hit 102m of silver at an average grade of 111g/t silver equivalent.

This drill hole is part of SS1’s first drill campaign to expand its existing 423Moz silver equivalent JORC resource.

And it was at one of the furthest out extensional drill holes from the existing silver resource...

...which might mean the start of a new and high grade silver extension to SS1’s already huge silver deposit.

Read: ⛏️ Tell me more: SS1 hits +100m of higher grade silver... new high grade extension?

Kaiser Reef (ASX:KAU)

Discovered in 1861, the A1 gold mine has produced over 600,000 ounces of gold.

That’s ~$2.6 Billion worth of gold at today’s gold price...

Kaiser Reef (ASX:KAU) has put in years of work to reach the deepest and never before mined levels of the A1 mine.

And this week KAU released the first two new drill results from these never before mined levels.

Condor Energy (ASX:CND)

It's now one of the largest undeveloped offshore gas discoveries on the west coast of South America.

This week our 2023 Energy Pick of the Year Condor Energy (ASX:CND) announced it has more than doubled the size of its gas resource at its Piedra Redonda field in offshore Peru...

To a best estimate, a contingent resource of 1 trillion cubic feet of gas...

That’s a 157% increase.

Lightning Minerals (ASX: L1M)

In a few weeks, $7M capped Lightning Minerals (ASX:L1M) is going to drill into a wall of lithium bearing pegmatites they found in an artisanal mine...

This is south of the ground where LRS made the discovery that propelled it to a $448M takeover by Pilbara Minerals.

Read: ⛏️ L1M: Drilling in coming weeks - following up ~4% lithium found in artisanal mine

Quick Takes 🗣️

SGQ signs MOU with a major Chinese steelmaker

EXR contingent resource now at 1.7TCF

Macro News - What we are reading & listening to 📰

Defence:

What will happen to rare earth markets in 2025? (Fast Markets)

- Rare earth prices fell sharply in 2024, with major materials like dysprosium, terbium, and NdPr dropping up to 30%, causing widespread industry losses.

- Experts predict continued challenges into 2025 due to weak Chinese demand and geopolitical risks but expect price recovery by late 2025 or 2026.

Securing Critical Minerals Vital to National Security, Official Says (US Department of Defence)

- The Defense Department is bolstering critical mineral supply chains through domestic mining, processing, and partnerships with allies like Canada, the UK, and Australia.

- Recent adversarial actions, such as China’s export bans on key materials, highlight the urgency of securing resilient and secure supply chains.

Defence spending: Billions more needed to ward off China, say military experts (AFR)

- Experts are urging Australia to increase defense spending to 3% of GDP within three years, citing strategic threats from China and demands from allies like the US.

- Delays in key defense acquisitions, including an $11 billion frigate project, have raised concerns about preparedness amid calls for rapid military capability expansion.

Can the US match China’s critical mineral stockpiles? (The Oregon Group)

- China’s stockpiles of critical minerals, including copper and nickel, are over 35% to 133% of its annual demand, raising concerns in the West about supply chain vulnerabilities.

- The US is considering building a strategic reserve of critical minerals, with bipartisan support, to counter China’s dominance and mitigate supply disruptions.

Gold:

Podcast: Why Are UK Assets Spiraling Now? In the City Explains (Bloomberg)

- UK assets are under pressure as the pound hit a year-low, gilt yields surged, and investor confidence in fiscal control wanes.

- Concerns over Chancellor Reeves' budget and its ability to address debt and inflation are driving market jitters.

Graphite:

DOD Leverages Defense Production Act to Galvanize Critical Supply Chains (US Department of Defence)

- The US is ramping up domestic graphite production through projects like BamaStar and Graphite Creek to reduce reliance on China and strengthen defense supply chains.

- Defense Production Act funding and strategic initiatives aim to build long-term industrial resilience and secure critical materials for national security.

Lithium:

Five Key Charts to Watch in Global Commodities This Week (Bloomberg)

- Lithium prices remain low due to oversupply and slower EV demand, with recovery unlikely before 2025.

- Some suspended mines could restart if prices rise, but a surplus is expected to persist this year.

Silver:

US Metals and Oil Roiled as Traders Weigh Risk of Tariffs (Bloomberg)

- US metals and oil prices are rising as traders anticipate potential tariffs under Trump’s trade policies, with sharp price gaps emerging between US and international markets.

- Platinum and copper face the highest tariff risks due to US import reliance, while gold and silver are unlikely to be impacted.

Copper:

China Is Ramping Up Grid Spending After Green Power Supply Boom (Bloomberg)

- China is accelerating its renewable energy transition, with power transmission spending surging 19% to $72 billion in 2023, outpacing generation investments for the first time since 2018.

- Grid expansion is critical to integrate wind and solar capacity, which more than doubled from 2020 to 2024, driving demand for metals like copper, steel, and aluminum.

Iron Ore:

Russia War: EBRD Says It May Invest €1.5 Billion in Ukraine This Year (Bloomberg)

- The EBRD plans €1.5 billion in investments for Ukraine in 2025, focusing on infrastructure, energy security, private sector growth, and food resilience.

- Over 50% of EBRD’s record €2.4 billion investment in 2024 supported private businesses, with continued emphasis on agriculture and corporate governance reforms for reconstruction success.

Critical minerals: The China commodities super-cycle is over – will there be another boom? (AFR)

- China's steel boom has ended, with production falling and demand stagnating; a shift toward renewable energy metals like copper and lithium is driving the next commodities cycle.

- Global steel demand is slowing, while geopolitical competition for resources intensifies, shaping a new era of constrained and diversified growth.

- Iron ore is expected to trade below $US100/tonne for most of 2025, with new supply from Rio Tinto’s Simandou project adding to Chinese port stockpiles, while US tariffs dampen steel demand in China.

- Chinese stimulus measures in 2025 may cushion iron ore price declines, though oversupply and shifting policies are forecasted to keep prices under pressure, with averages predicted to fall to $US95/tonne.

Others:

Famous short seller Hindenburg Research shutting down

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.