Microcap CND: 1 Trillion cubic feet of gas - now one of the largest undeveloped offshore gas discoveries on the west coast of South America

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 33,040,455 CND Shares and 11,925,000 CND Options at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time.

It's now one of the largest undeveloped offshore gas discoveries on the west coast of South America.

And it last traded at ~$11M market cap.

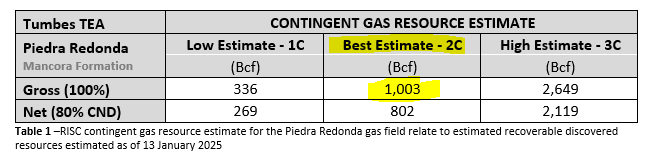

This morning our 2023 Energy Pick of the Year Condor Energy (ASX:CND) announced it has more than doubled the size of its gas resource at its Piedra Redonda field in offshore Peru...

To a best estimate, contingent resource of 1 trillion cubic feet of gas...

That’s a 157% increase.

This is a CONTINGENT resource... meaning it is drawn from known gas accumulations - stuff that’s already there.

And still with significant additional upside to be targeted in future appraisal drilling campaigns up-dip of Piedra Redonda in areas where potentially even more gas has migrated over time.

This increase is on CND’s Piedra Redonda field which is a shallow EXISTING GAS DISCOVERY made in 1978 and has ALREADY FLOW TESTED at a maximum 8.2mmcf per day...

from 32 feet of net pay out of 152 feet total net pay.

This is a development ready field.

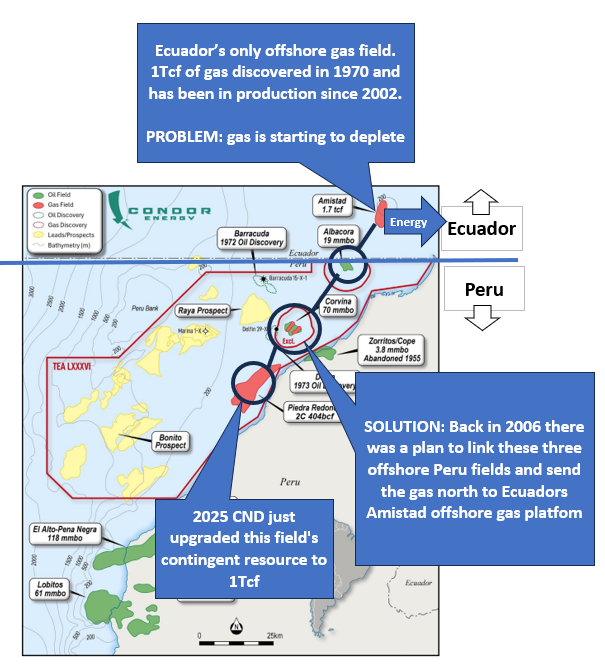

In fact, back in 2006, it was almost developed...

CND’s Piedra Redonda field was part of a development plan to help solve Ecuador’s energy shortages.

The Ecuador border is directly to the north of CND’s Peruvian acreage.

(and recently the Ecuador energy crisis has got a lot worse.)

Here is our rough image showing the 2006 gas to power development plan to “daisy chain” Piedra Redonda, Corvina and Albacora gas to the north via tie-in to the Amistad gas field platform just over the border in Ecuador:

The project even had even had backing from the World Bank International Finance Corporation who was going to partially fund it (Source)

BUT...

The previous owners at the time (a US company called BPZ) decided to also focus on oil and took on a huge amount of debt to develop their oil projects...

However a 2015 oil price crash eventually caused BPZ to declare bankruptcy - which led to a fire sale of their offshore Peru assets.

These events eventually led to ~$11M capped CND now owning 80% of the advanced stage, 1 TCF contingent resource Piedra Redonda.

As well as a huge amount of surrounding, highly prospective acreage.

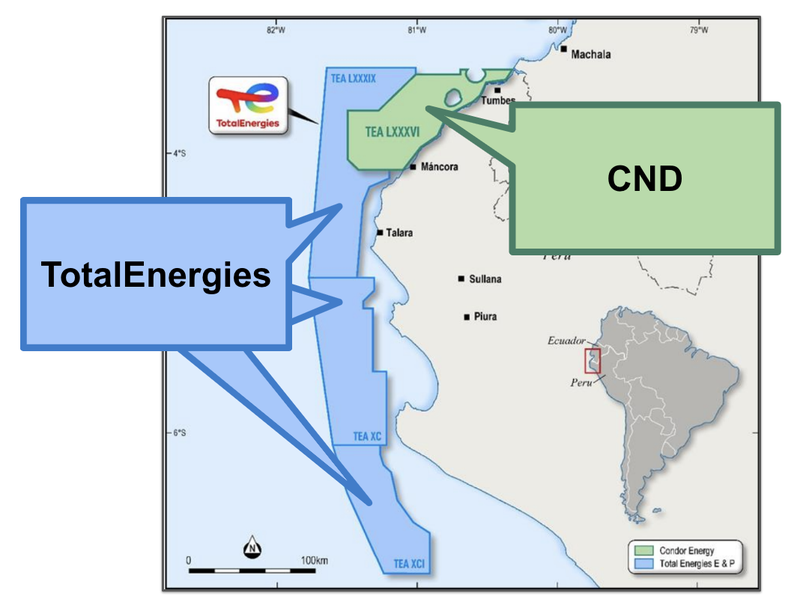

Which also happens to be surrounded by energy supermajor TotalEnergies SA.

Gas prices have doubled in the past 4 months:

... and Ecuador's energy crisis getting worse:

Given all of the above, we think CND’s now 1TCF development ready Piedra Redonda field could attract development interest from new partners.

More on CND’s assets

The Piedra Redonda gas field sits within CND's enormous 4,858km2 of prospective licences in offshore Peru.

CND also has two blue sky oil & gas exploration prospects within this license area.

On the two exploration prospects, we are waiting for CND to release maiden prospective resources.

And eventually define some blue sky oil & gas exploration drilling targets on these two prospects...

Which can often leads to nice share price runs in anticipation of a major new discovery.

CND is surrounded by historical hydrocarbon discoveries with numerous excellent leads.

CND’s acreage sits inside an oil producing basin with historical production of ~1.6 billion barrels of oil

Back in May 2024, $222BN global energy super-major Total Energies liked offshore Peru so much that they snapped up almost all the acreage around CND’s project:

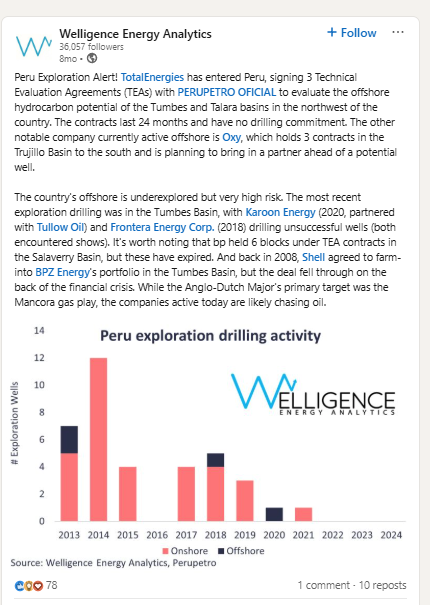

And after a long dormant period, Peruvian exploration is finally kicking off in earnest again with majors like $79BN capped Occidental Petroleum moving in as well:

(Source)

This land grab by TotalEnergies was a strong validation of the quality of CND’s exploration assets, and evidence it is hunting for a large discovery in the right place.

And offshore exploration in Peru has attracted big ticket farm-ins before...

KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) in 2009 signed a deal worth US$900M for projects to the south of CND’s block.

Piedra Redonda - a 1 TCF contingent resource - that could get bigger...

As early stage oil & gas Investors, we have been chasing oil & gas discoveries and commercial flow rates for over 20 years.

With the associated emotional (and financial) high and lows.

CND already has a DISCOVERY and material flow rate on one part of its acreage, in the area where the resource upgrade was published today.

That discovery (Piedra Redonda) was made in 1978 (when gas was way out of favour) AND it has already been flow tested at 8.2 million cubic feet per day from 36m of net pay.

CND also says that “A significant amount of pay in the C-18X well was not tested due to program constraints and presents additional deliverability upside”

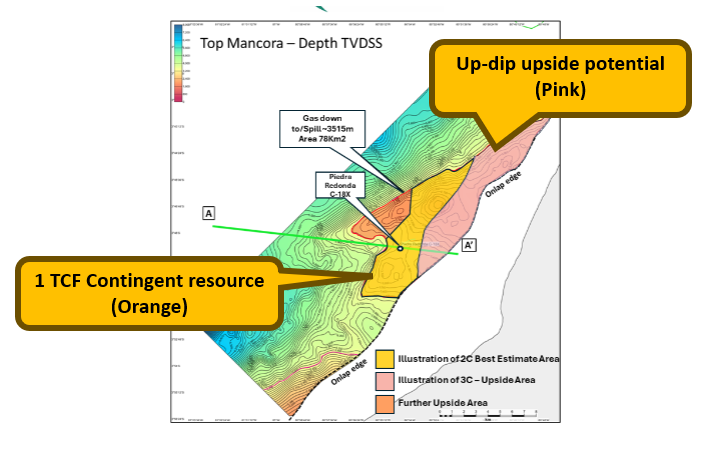

An important thing to note is that the discovery drill hole and flow rate was “down dip” of the structures underground.

Because gas by its nature “wants to move upwards” AND there is confirmed gas down-dip, it’s highly likely there is more gas up-dip.

The previous owners DID try to drill up-dip...

But mechanical problems meant that it wasn’t able to reach total depth or conduct a flow test.

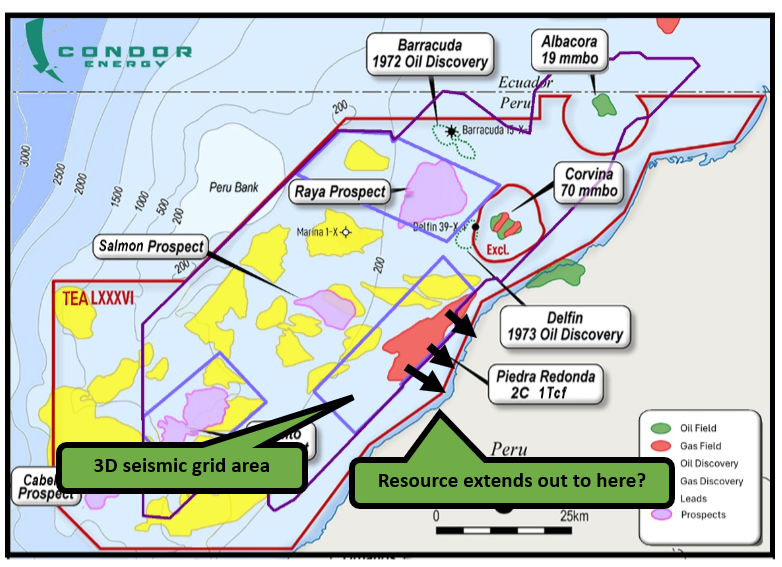

We also noticed that the entire resource estimate for Piedra Redonda is currently limited by the areas of CND’s project that are covered by seismic data.

At the moment, the seismic data cuts off before the edges of CND’s acreage.

Oil and gas resources are unlikely to be constrained by human determined seismic grids...

We think there is a chance the resource actually extends to the edge of CND’s acreage which could mean Piedra Redonda is a lot bigger than the resource estimate is showing right now.

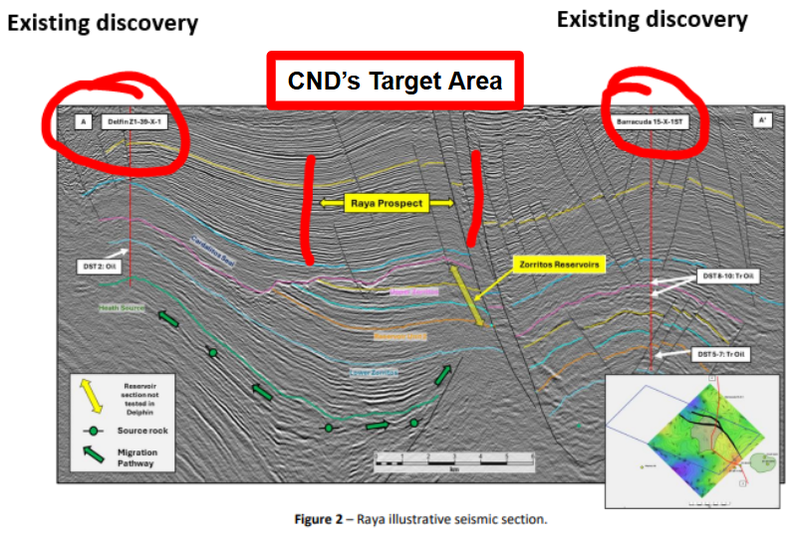

Here is what we mean in visual form:

Ecuador is hungry for Peruvian gas next door... CND the answer?

Ecuador and Peru are direct neighbors.

Ecuador only has one offshore gas field (Amistad) which has 1Tcf of gas and has been in production since 2002 - its right near the maritime border with Peru (and CND’s Peruvian acreage).

But the gas from Ecuador's field is starting to deplete and the Ecuadorian industrial sector is in need of more...

Amid recent blackouts, the country is in quite the bind:

Ecuador is moving quickly to address the crisis.

Last year, Ecuador launched a tender inviting investors to participate in an offshore natural gas field located in the Gulf of Guayaquil (in Ecuador). (Source)

But it also looks like energy from Peru will be a big part of the solution.

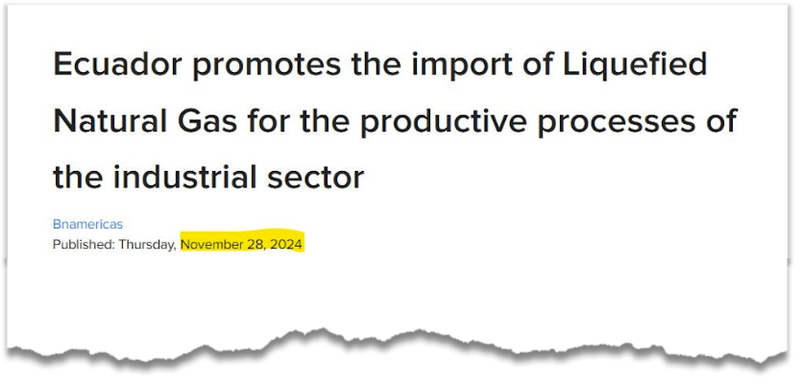

Less than three months ago the Ecuadorian Minister for Energy & Mines approved the import of 7.3 billion cubic feet of LNG from Peru:

(Source)

This recent move to import LNG from Peru indicates that exploration is not moving fast enough to meet the country's demand.

As we mentioned before, the good news is that CND’s most advanced prospect, the Piedra Redonda, is development ready.

With an existing flow rate and an upgraded resource today we think that CND is development ready.

Especially after the company’s recent technical review identified scalable development options like gas-to-power and compressed natural gas (CNG) for industrial/domestic use. (Read the Quick Take)

We mentioned that this project has been on the cusp of development before.

We did a bit of digging on CND’s overall project and found out that under previous ownership (BPZ Resources) the project had come incredibly close to being developed and put into production with the help of the IFC/World Bank. (Source) (Source)

BPZ first started drilling in 2006, with a gas to power plan intended to link up with Ecuador’s Amistad gas field to the north.

BPZ Resources ultimately went bankrupt in an oil price crash, and with Ecuador currently in an energy crisis, CND is well placed to develop the project where others have failed.

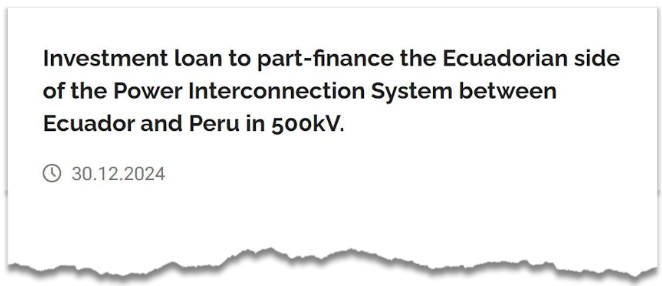

Adding further impetus to CND’s project is the fact the European Investment Bank is contributing US$125M to the construction of a power interconnector between Peru and Ecuador:

(Source)

We think all of this adds up to a powerful set of regional macro forces that will provide tailwinds for the development of CND’s project.

CND feels a bit like IVZ 2.0...

A big reason why we Invested in CND is because of board member Scott Macmillan (MD of Invicitus Energy).

Scott Macmillan has “been there” and “done that” when it comes to making a big drill event a reality.

We think that by the time CND is ready to drill a high impact oil & gas exploration well the company could follow the same trajectory as Invicitus Energy in terms of excitement and interest around the stock.

Here is what happened to IVZ:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

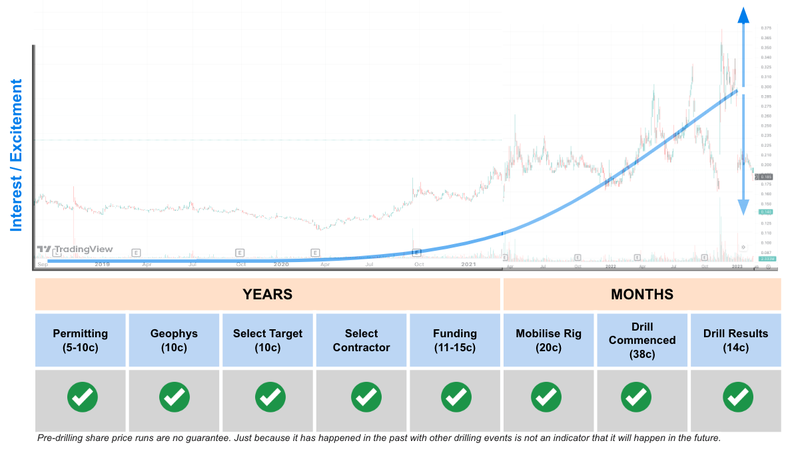

Small cap exploration companies with big drilling events often see a run in share price in the lead up to drilling (often, but not always).

As drilling and results approach, interest and excitement builds in the lead up to drilling results, and speculators may enter the stock expecting a positive result.

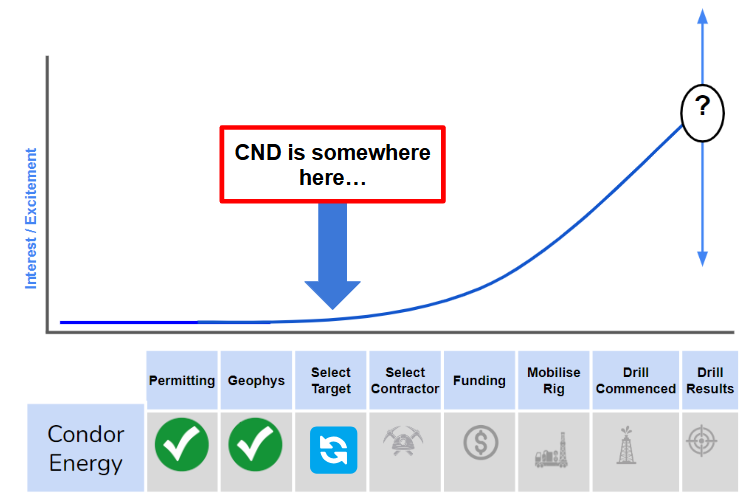

CND is getting closer to the end of its two year Technical Evaluation Agreement (TEA), and closer to where its prospects will all be drill or deal ready...

The TEA should be ending in the second half of this year which means we are getting pretty close to a step away from desktop studies and more high impact exploration.

Here is where we think CND sits on that ‘excitement’ chart from earlier:

In a sign that CND is getting serious about moving forward with an exploration program the company appointed Serge Hayon as managing director.

Serge spent 20 years at $7BN NYSE listed Murphy Oil Corporation where he was in charge of Murphy’s Vietnam operations.

There, Serge led the company’s entry into and Final Investment Decision (FID) on the Lac Da Vang offshore oilfield.

(which has gross recoverable resources of 100 million BOE).

So Serge knows how the majors think and what is needed in a project.

Where is CND relative to our Oil and Gas Investment Strategy right now?

One of the main reasons we announced CND as our 2023 Energy Pick of the Year was because of where the company sat relative to our tried and tested Oil & Gas Investment Strategy.

For those who have been following our Investments for a while with oil and gas explorers we tend to follow a five step investment plan.

Of course, before we show you our plan, we need to stress that there’s never a guarantee of success with speculative oil and gas investing. We recommend consulting with a professional financial advisor before choosing to invest in small cap stocks like CND.

Our general plan is to Invest early, and eventually, as a drilling event draws closer over the coming years we expect to see broader investor interest increase, and with that, growth in the company’s valuation.

Our plan is usually to:

- Invest early, as the company is in the early exploration work stage.

- Increase our Investment, as the company de-risks the project through permitting, geophysics and target generation.

- Top Slice, if the share price runs in anticipation of exploration results

- Free Carry, into results while still maintaining a large position to be leveraged for a discovery

- Evaluate our position post-drilling.

Our broader thinking is that as an oil and gas explorer gets closer to a major catalyst like a drilling event, investor interest increases in the stock and the company’s valuation starts to move higher as expectations get baked into its share price.

We made CND our 2023 Pick Of The Year at 1.9c per share - at the time CND’s market cap was ~$7M.

Now, after 11 months, CND’s market cap is $11M (prior to last close) and the company is ~14 months into its 24 month TEA.

Which means it is starting to approach a point where CND will need to make a decision on a drilling program OR do a deal to have its share of the drilling funded.

So we know there is at least another 10 months before a drilling program and CND’s market cap is just $11M now.

In terms of market interest/excitement we think CND currently sits here:

Ultimately, we are hoping that as CND puts out prospective resources and outlines a development/drilling timeline the company’s valuation re-rates in line with our Big Bet which is as follows:

Our CND Big Bet

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for CND?

Maiden Prospective Resource #1 (Bonito-Volador prospect) 🔄

CND has completed ~250km^2 of 3D seismic reprocessing over this area and next we want to see CND define a maiden prospective resource.

Maiden Prospective Resource #1 (Raya prospect) 🔄

At the Raya prospect, CND has completed ~400km^2 of 3D seismic reprocessing.

CND picked Raya as one of its three main targets primarily because this part of its project had the potential for similar “stratigraphic and structural traps” to the two nearby discoveries.

The two discoveries are - Barracuda and Delfin, which were both confirmed oil discoveries.

Here we want to see CND announce a maiden prospective resource estimate.

What could go wrong?

Every speculative oil and gas investment carries risk. CND is no different.

Given that CND operates under a two-year “Technical Evaluation Agreement”, the company faces no short-term exploration risk as it is not required to drill test its asset quickly.

In the short term we think the main risk for CND is “Funding Risk”.

CND had $1.4M cash in the bank at the end of the September quarter and we should get an updated number in the next couple of weeks on the December cash balance.

(Quarterly reports are due at the end of this month)

CND generally has a low cash burn, however the company may look to shore up its balance sheet depending on how the December cash balance looks.

From a market risk perspective, fluctuations in market sentiment/oil & gas prices could impact CND’s share price and investor interest in the story.

To see more risks read our CND Investment Memo here.

Our CND Investment Memo

In our CND Investment Memo, you can find:

- CND’s macro thematic

- Why we Invested in CND

- Our CND “Big Bet” - what we think the upside Investment case for CND is

- The key objectives we want to see CND achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.