Oil & Gas Supermajor TotalEnergies picks up ground next to CND

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 33,875,455 CND shares and 11,925,000 options at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time. Condor Energy (ASX:CND) was previously Global Oil and Gas (ASX: GLV) - a company name and stock code change happened in April. NOTE: We discovered incorrect shares held disclosures for CND, please see footer of our CND Investment Memo for the correction.

Guess who just signed three offshore exploration agreements next to Condor Energy (ASX:CND) in offshore Peru overnight...?

One of the five global oil and gas supermajors.

$260BN TotalEnergies.

Last year, long before TotalEnergies, CND signed exploration agreements for 4,858 km2 of acreage offshore Peru.

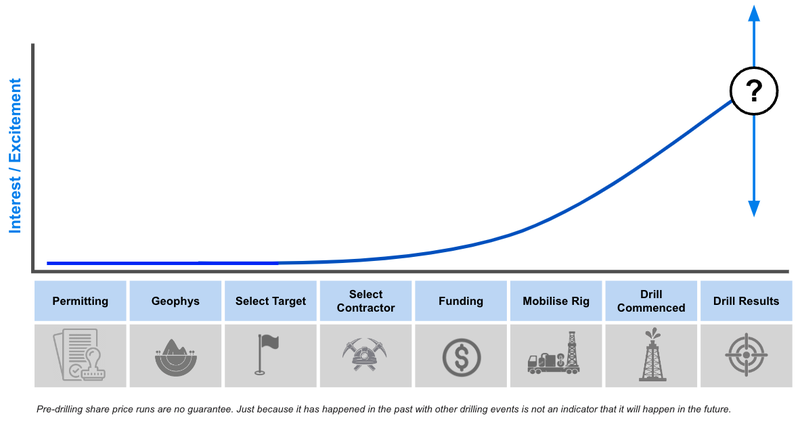

CND is aiming to make a large oil and gas discovery, and is going to spend the next couple of years defining a big drill target, then drilling it.

(We love a big “swing for the fences” oil & gas drill event.)

After its move into Peru, Invictus Energy MD Scott Macmillian joined the CND board, CND started re-processing existing 3D seismic (to identify drill targets), and changed their name to Condor Energy (from Global Oil & Gas).

And now TotalEnergies has moved in next door.

TotalEnergies will be doing their exploration in the same geological basins as where our Investment $22.5M capped CND has acreage.

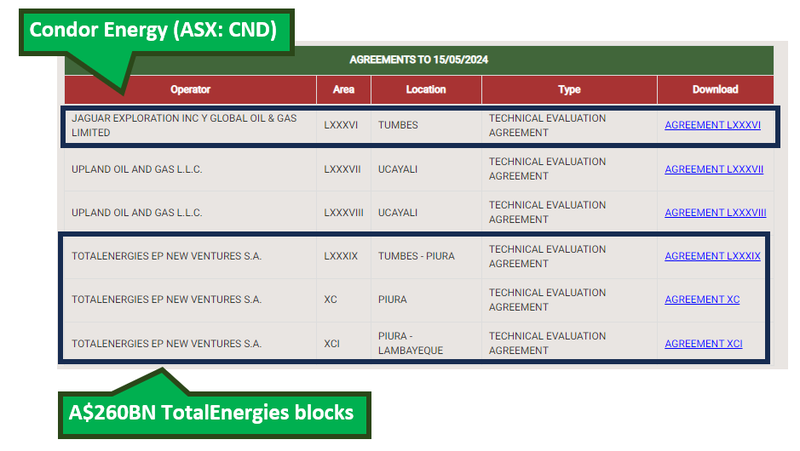

The French oil giant signed 3x Technical Evaluation Agreements (TEA) in northwest Peru with the state owned PeruPetro.

(Source)

Total’s entry into the region means CND is just one of three companies with TEA’s on blocks in Peru.

The move by TotalEnergies is a strong validation of the quality of CND’s exploration assets, and evidence they are hunting for a large oil discovery in the right place.

TotalEnergies has a vast balance sheet to spend on exploration, so we are hoping they see enough to drill test some targets as well - which would bring more interest into CND’s assets as well.

(See all of Perupetro’s TEAs here: Source)

Total's TEA is almost identical in structure to CND’s current agreement with the Peru oil and gas regulator.

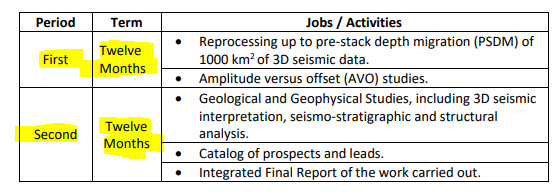

The TEA (Technical Evaluation Agreement) means that for an initial two-year period, companies can carry out desktop work on a defined area — reprocessing and analysing 2D/3D seismic data, as well as identifying and ranking drill targets.

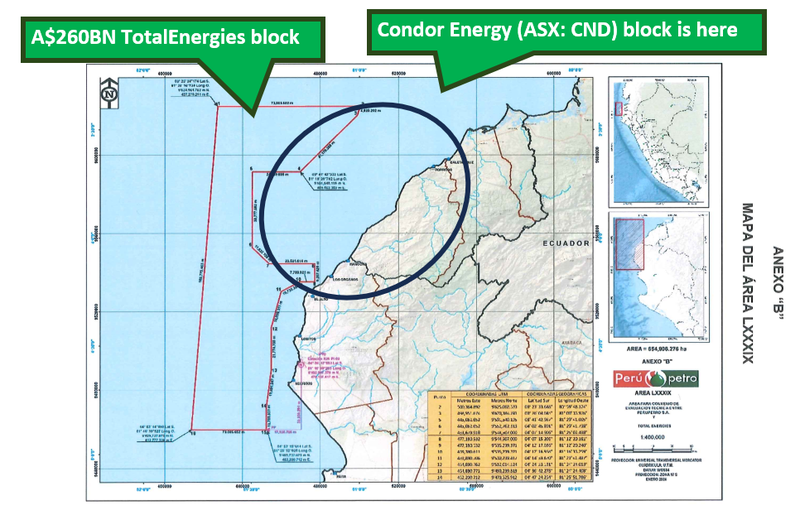

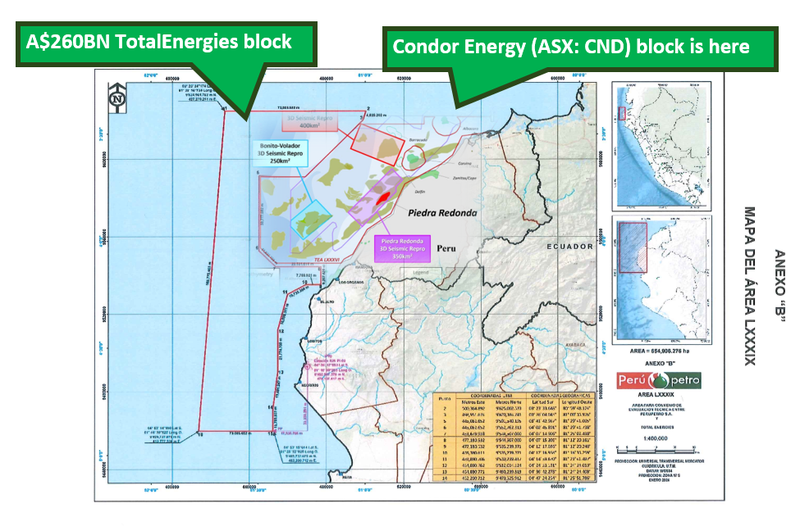

CND’s TEA covers ground across two separate basins - the Talara and Tumbes basins.

Talara on its own has had historical production of ~1.6 billion barrels of oil and oilfields still producing at ~3,000 barrels of oil per day right now.

Total’s TEA’s are focused on the exact same basins CND is working in...

We aren't geospatial professionals, but we did try overlaying the two maps to show just how close they are...

Both areas are big - and look very close to each other...

Here’s why we think Total’s presence in Peru confirms the potential of CND’s project...

Other than the link we found above, there weren't many details or mainstream news coverage of Total’s intentions with the move into Peru BUT we think the news is extremely positive for CND.

First of all, Total didn't pick up just one block but picked up three... a clear signal of intent they are interested in multiple areas offshore Peru...

The news also gives us a good idea of what an exit scenario or a drill funding plan could look like for CND.

A key part of our Investment Thesis in CND was to see it define giant drill targets over the 24-month Technical Evaluation Agreement (TEA).

We are following our typical oil and gas Investment Strategy which is to Invest early, hold most of our position leading up to a big drill program and de-risk/free carry along into results.

It’s important to note that increased excitement/interest shown on our chart below does NOT necessarily correlate to share price increases, which depends on many other factors and broader market conditions.

As CND gets closer to a maiden drill program - a big question mark is always going to be - how does little CND fund the drilling of an offshore well, which can run into the tens of millions of dollars?

That's where the Total news comes into play.

Now we have one of the five biggest oil and gas supergiants active in Peru.

AND with ground surrounding CND’s project.

We would expect Total to keep a close eye on CND to see what the company can deliver from its ground because ultimately, it would impact what Total is doing on its own ground.

We think that IF CND is able to show the market (and Total) big drill targets with strong geological fundamentals then it could make for an bolt-on acquisition target or a strong farm in partner.

OR the project could be the perfect option for another oil and gas supermajor to come in and take a position in the region.

Again - either via a farm-out deal or a takeover all together.

Of course it's still very early days here for CND. Its project is still only in the TEA stage, which means it will need to be converted into an exploration licence at the end of the two year work program.

After that there is still no guarantee Total and CND will ever do anything together, we just think the proximity of the two assets would surely put CND on Total’s metaphorical “watchlist”....

What do we already know about CND’s project?

CND’s project is huge, covering ~4,858km^2 offshore Peru.

The project sits across two basins - Talara and Tumbes - where multiple existing discoveries have been made and ~1.6 billion barrels of oil have been produced.

Remember these are the same basins TotalEnergies is now exploring.

CND’s project also has tens of thousands of km’s in 2D & 3D seismic data which in today’s money would cost 10’s of millions to acquire.

As mentioned earlier, CND is operating the project under a Technical Evaluation Agreement (TEA).

The TEA means that for 24 months, CND doesn't need to do any high cost drilling work - most of the work is limited to seismic reprocessing/analysis.

As part of the 24 month work program, CND has so far picked three priority prospects across its block where it will be focusing on.

AND CND has already managed to define a contingent/prospective resource on one of those three.

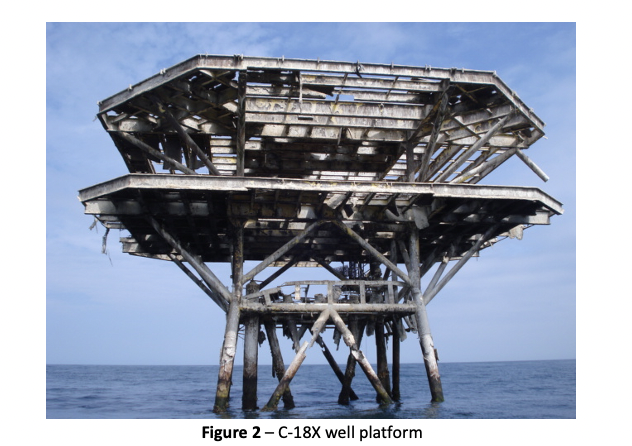

CND defined a 404 Bcf contingent and 2.2 trillion cubic feet prospective resource across its Piedra Redonda prospect (on a 100% ownership basis).

That was based on data from two old wells one of which flowed gas at 8.2 million standard cubic feet of gas per day - below is a picture of one of the well platforms:

We covered that news a few weeks back here: CND announces details of historical gas discovery - and it has already flowed...

Across its two other prospective areas, CND is currently focused on reprocessing 3D seismic data which we hope leads to newsflow similar to what we saw from Piedra Redonda.

What is CND up to now?

CND’s two-year TEA means the first 12 months is all about reprocessing seismic data across its project.

CND has already isolated three key areas of its project where it will be doing the reprocessing work.

In its latest announcement CND confirmed the reprocessed seismic data would be ready by “Mid-Year”.

(Source)

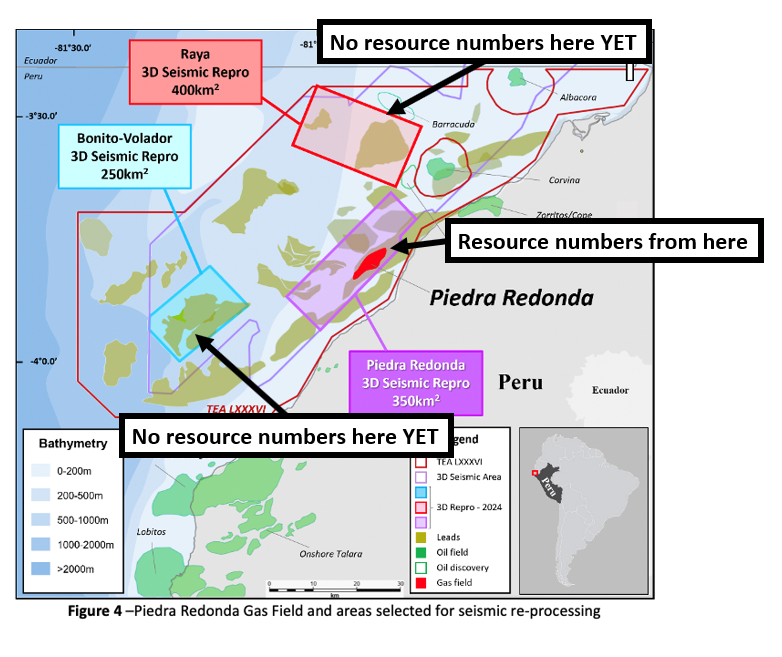

Below is the latest across all three areas:

Target #1 (Bonito-Volador prospect) 🔄

Across the first prospective area CND is currently reprocessing ~250km^2 of 3D seismic data.

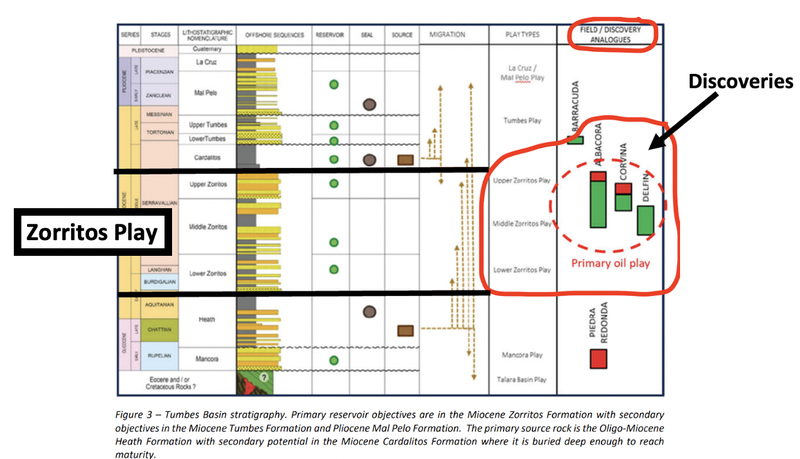

At Bonito, CND is targeting the “Zorritos Play” which is the primary reservoir across multiple discoveries in this part of Peru.

Previous exploration has almost exclusively focused on the “Upper Zorritos reservoir” but CND is going back in looking at the entire play which we think is a good move especially considering the deeper Zorritos reservoirs have produced oil/gas in the past...

Next for Bonito-Volador is the results from the reprocessed 3D seismic data.

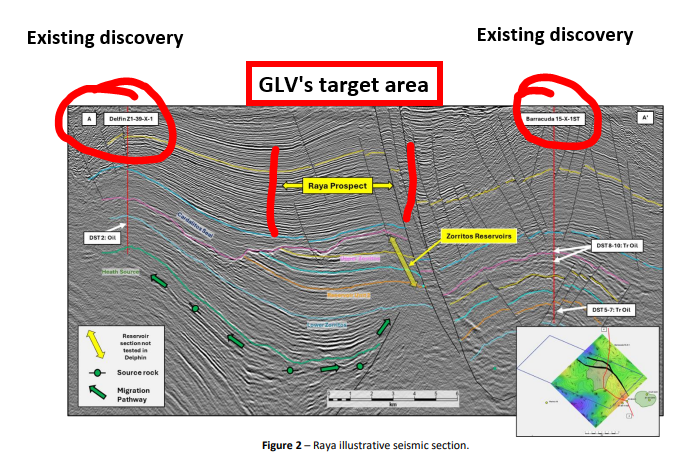

Target #2 (Raya prospect) 🔄

At the Raya prospect, CND is currently reprocessing ~400km^2 of 3D seismic data.

CND picked Raya as one of its three main targets primarily because this part of its project had the potential for similar “stratigraphic and structural traps” to the two nearby discoveries.

The two discoveries are - Barracuda and Delfin which were both confirmed oil discoveries.

Next for Raya is the results from the reprocessed 3D seismic data.

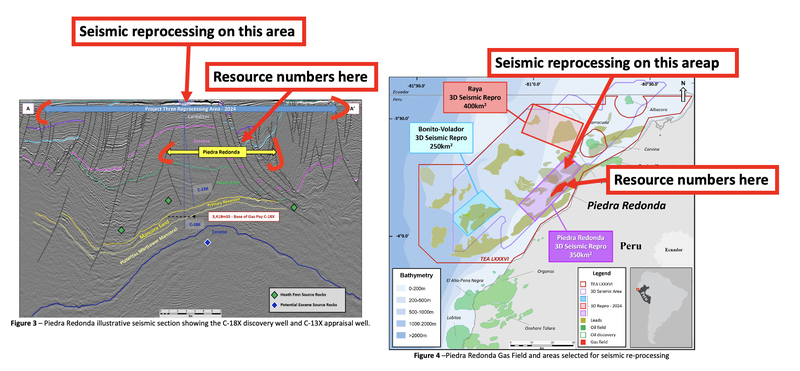

Target #3 (Piedra Redonda) 🔄

Here CND is currently reprocessing ~350km^2 of 3D seismic data.

As mentioned earlier, CND already has a 404 billion cubic feet of gas (Bcf) contingent resource and a 2.2 trillion cubic feet (TCF) prospective resource for Piedra Redonda (on a 100% basis).

At the moment CND’s resource numbers come from a small part of the overall prospect.

We think there is still plenty of scope to upgrade those numbers as CND does more desktop work on the prospect.

The image below shows how much of the project area the current resource numbers cover:

Ultimately, we think that as CND progresses its project from where it is at now to prospective resource numbers and onto high impact drill targets, the valuation hopefully re-rates to a level that is pricing in the potential upside from one of those targets.

All of that forms the basis for our CND Big Bet which is as follows:

Our long term CND Big Bet:

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What could go wrong?

Given that CND operates under a two-year “Technical Evaluation Agreement” the company faces no short-term exploration risk.

As a result we think the key risk in the short term is “market risk”.

For the duration of the two year TEA, we expect CND’s share price to be impacted most by overall market sentiment and underlying oil and gas prices.

Lower oil and gas prices could pull capital away from high risk explorers like CND.

Overall market downturns should also have a similar impact.

For now these are the two key risks we are most conscious of.

We touch on more risks to our CND Investment in our CND Investment Memo here.

Our CND Investment Memo

In our CND Investment Memo, you can find:

- CND’s macro thematic

- Why we Invested in CND

- Our CND “Big Bet” - what we think the upside Investment case for CND is

- The key objectives we want to see CND achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.