Potential Lithium Comeback, Sydney RIU Conference and more...

Published 06-MAY-2023 16:00 P.M.

|

12 minute read

Next week a couple of us are heading to Sydney to attend the 2023 RIU “Resources Roundup” Conference.

We always say that meeting company management face to face is extremely important in small cap investing.

This includes watching them deliver investor presentations on the company's progress.

It’s the best way to gauge if a Managing Director is genuinely excited about what is coming up.

The RIU conference is a 3 day event, and our Portfolio companies attending and/or presenting include NHE, LNR, FYI, AKN, LRS, and OKR.

A lot of other companies, financiers and brokers appear to be coming to Sydney coinciding with the conference.

While in Sydney we are also meeting management from our Investments TG1, PUR, MEG, and GGE.

We will report back from the week's meetings afterwards.

We will be on the lookout for new Investments too.

We are keen to meet small cap companies in gold and battery materials, either already listed on the ASX OR private but looking to list.

If you are one or know one and are in Sydney let us know by replying to this email.

Finally, we are doing a presentation ourselves at the RIU conference on Thursday.

The presentation is part of the RIU ESG session and is about why, as fund managers, we think it’s important for our small cap Investments to disclose ESG.

(Spoiler alert: its to access broader pools of capital and to secure early offtake agreements with ESG conscious buyers)

If you want to see our presentation at the RIU conference ESG session this Thursday details are here.

Lithium comeback

...or did it ever even leave?

The lithium spot price has had a rough couple of months, but has been going up again over the last two weeks (more on this later).

The weakness in the lithium price hasn’t stopped some big, strategic investors who believe in lithium long term, cutting some big cheques.

Recent M&A activity in the lithium sector (Albemarle's move on Liontown Resources for example) indicates that smart money and big players are confident that smaller lithium companies still represent good value.

A few of our lithium Investments delivered some pretty epic financing agreements in the last couple of weeks too.

TYX secured a $31M financing package from $8BN Sinomine to progress its Angolan lithium project - plenty of money for a pretty early stage explorer - full details and our analysis here.

LRS surprised the market by raising $37.1M from various strategic funds giving it a total cash balance of ~$57M to continue its aggressive drilling program and accelerate feasibility studies on its lithium project in Brazil. LRS is following in the footsteps of its $6.2BN regional peer Sigma Lithium.

VUL raised $109M this week and is now funded to order long lead items to build its phase 1 lithium and geothermal plant.

A big capital raise from strategic investors makes it easier for companies to deliver share price re-rates. This is because the successful execution of milestones is often rewarded in the absence of a “looming cap raise overhang” on the share price.

We see the big money flowing into small lithium companies supporting our long-held view that lithium is a major part of one the defining macro themes of this decade - battery materials.

The big news recently was speculation over a potential offer for Liontown Resources which topped Albemarle's $2.50 offer.

The news saw Liontown’s share price move higher to finish the week at $2.85 per share.

Only six months ago Liontown’s share price was trading at ~$1.25 per share.

For us, the major takeaway from all of this is that while investor sentiment in the lithium space has been soft (primarily due to the spot price for lithium trading near 12 month lows), deep pocketed corporates interest in lithium projects are still extremely strong.

Further proof of this - Liontown isn't the only project Albemarle are interested in either...

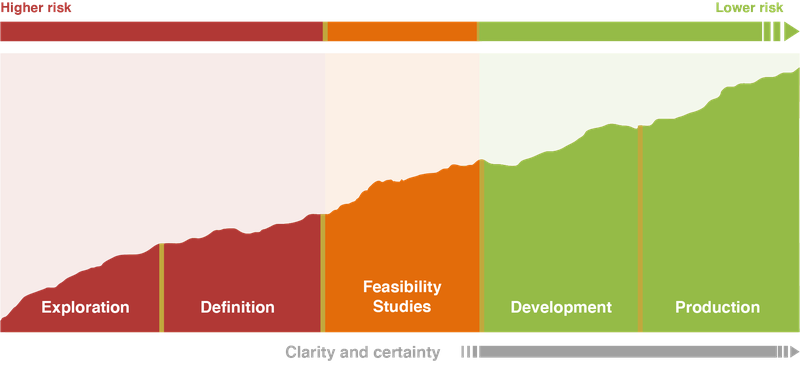

We want to see our small cap lithium companies move as fast as possible up the resource company lifecycle stages so they too can become a takeover target, which are generally happening at “development” or “production” stage in the image below.

We also suspect that M&A activity might start creeping into earlier stages of the lifecycle:

Takeover target Liontown is a “development” stage company.

We want to see our earlier stage lithium projects who are in the “definition” or “feasibility study” stage” progress to “development” stage as quickly as possible.

The more money they raise the faster they can progress through the stages, and the quicker we might see a takeover offer.

TYX (definition stage), LRS (feasibility studies stage) and VUL (nudging into development stage) are now cashed up and ready to put the foot on the electric car accelerator pedal (not the gas) to progress to the next lifecycle stage.

Lithium Prices - what’s going on?

While the lithium price has fallen by more than 65% from all time highs in November, it remains ~120% higher than when it was in the pits in 2020.

It’s very early days, but...and this is a big but... the bleeding may have stopped.

The lithium price managed to achieve its first price RISE in months over the last two weeks.

What we’re seeing is a very strange thing - big investments and M&A activity in lithium while the spot price for lithium is getting crushed.

Normally big investments and M&A happens at the top of the cycle, when a spot price is rising.

Perhaps the simplest explanation is the best here - extreme strategic competition in geopolitics is driving this “bizarro world” market.

For some more context on lithium spot prices, since China reduced electric vehicle subsidies in January prices have come down ~65%, demand for lithium has understandably come down and inventories increased.

Typically, when spot prices get hit as hard as lithium in a short period of time, it signals a structural change in the supply/demand for that specific metal/material.

The lithium space is a little bit different.

While in the short term, demand from China for batteries/electric vehicles and in turn lithium has come off, the medium to long term outlook is unchanged.

In 2022 for example, global electric vehicle sales were up 55% and are expected to grow another 35% this year.

In China sales were up 90% in 2022 and are already in the first quarter of 2023 electric vehicle production is up ~27.7% versus the same period last year.

American, European and Asian carmakers have all made commitments to completely electrify their vehicle fleets by the years 2030, 2040, or 2050.

Couple this with the demand coming from the battery energy storage industry which is expected to grow ~15x by 2030 and the supply/demand imbalance outlooks starts to look a lot worse.

We think that short term fluctuations in the lithium price will ultimately just be “noise” and we expect there to be demand in excess of supply through to the end of the decade.

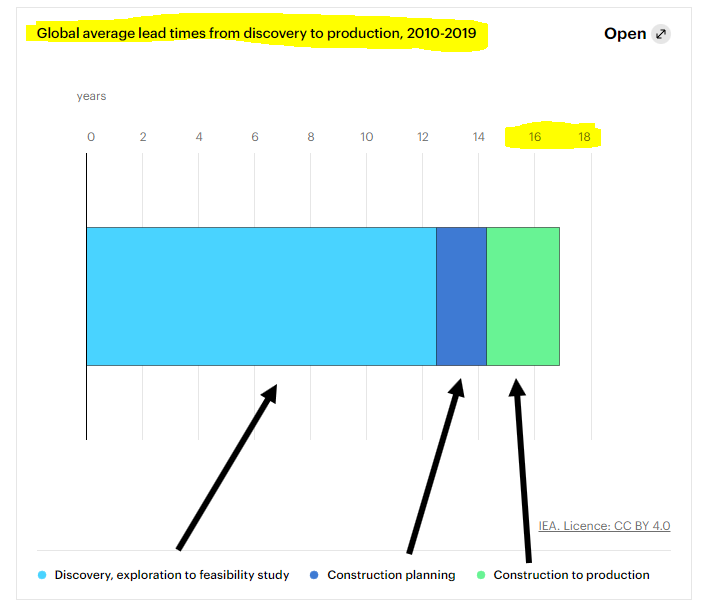

After all, it takes only ~2-3 years to build downstream processing/battery manufacturing facilities but it can take ~17 years to take a critical minerals project from discovery into production.

If we take 2016 as the starting point for the rush to secure lithium supplies it could mean the shortages persist through to ~2033.

A spanner in the works was the recent introduction to the US Inflation Reduction Act (IRA) in which tax credits for EVs were excluded for companies that don’t use raw materials from “friendly sources”.

The new IRA rules dictate that electric vehicles can only qualify for subsidies if more than 40% of the critical raw materials in the battery come from the US or a country it has a free trade agreement with the US.

Cars with batteries that are built with raw materials sourced from “unfriendly” countries would not be eligible for subsidies which would make them less competitive in the marketplace.

This phenomenon is called “friendshoring” and explains the fight for projects like Liontown’s in WA.

We see the lithium market being structurally short of supply over the next 5-10 years.

With critical minerals acts being put in place all across the western world we expect to see a rush from global automakers, corporates and governments to secure their own supply chains of materials like lithium from friendly nations.

See all the Lithium stocks we are currently Invested in and our outlook for lithium in 2023

This week’s Quick Takes 🗣️

PFE: Drilling completed, assays in six weeks

FYI: New development schedule for High Purity Alumina project

LNR: First phase drilling in South Australia XRF results

ALA: ALA’s laser-like focus on INkT cell therapy; costs cut

EV1: Drilling results are in - new graphite discovery made

MAN: MAN gearing up for sampling programs at its US lithium project

IVZ: IVZ looking to raise $10M through a Share Purchase Plan (SPP)

DXB: DXB Announce Rights issue to raise $12M for FSGS

Macro News - What we are reading 📰

US-Based Commodities

US Is Vulnerable to China’s Lock on Key Minerals, Biden Aide Says (Bloomberg)

China factory activity unexpectedly shrinks in April (Reuters)

Lithium

Mystery bidder tops Albemarle’s $2.50 offer for Liontown Resources (AFR)

An ugly truth about your phone’s key ingredient (AFR)

Argentina's lithium pipeline promises 'white gold' boom as Chile tightens control (Reuters)

Rio says lithium asset prices too rich for its M&A taste (AFR)

Albemarle has eye on lithium prizes other than Liontown (AFR)

Rare Earths

Rare Earths MMI: Prices Plummet as Rare Earth Demand Drops (AG Metal Miner)

Helium

Helium production in Australia is set to end. Could another source fill the gap? (ABC)

Gold

Gold trades to a new all-time high today (Forex Live)

Oil & Gas

ExxonMobil, Hess Announcements Add To Guyana’s Oil And Gas Bonanza (Forbes)

Copper

Copper Mine Flashes Warning of ‘Huge Crisis’ for World Supply (Bloomberg)

Biotech

How CSL went from ‘bloated bureaucracy’ to $145b global behemoth (AFR)

This week in our Portfolios 🧬 🦉 🏹

Tyranna Resources (ASX: TYX)

Our 2022 Catalyst Hunter Pick Of The Year Tyranna Resources (ASX: TYX) just signed a major financing agreement with $8.3BN capped Sinomine.

Chinese mining giant Sinomine is investing up to $31M in TYX and will have a first right of refusal on an offtake deal for 50% of TYX’s lithium production.

The deal values TYX’s project at ~A$100M, while TYX currently trades with a market cap of $60M.

With this new financing deal and strategic investor, TYX can focus on drilling and growing the resource with no looming capital raise overhang weighing on the share price.

This strategic financing deal has come out of nowhere, and really surprised us... and the market.

📰 See our full Note: TYX secures up to $31M in financing from $8BN giant Sinomine

Lanthanein Resources (ASX: LNR)

Our WA rare earths exploration Investment Lanthanein Resources (ASX: LNR) just kicked off its major drill program for 2023.

Over 10,000m of drilling across two types of rare earths targets.

LNR’s drilling is targeting the same type of rocks that host both Hastings and Dreadnought’s rare earths discoveries - Ironstones and carbonatites.

LNR is currently capped at $20M, and with that $5.2M cash in the bank has an enterprise value of ~ $15M. $258M capped Hastings sits ~2km away from LNR’s project and $200M Dreadnought is ~32km away.

- Shallow ironstones targets - these are the same type of rocks that host Hastings resources & Dreadnought’s discoveries to the east.

- Deeper carbonatite targets - Carbonatites are the same type of rocks that host $5.9BN Lynas Rare Earths giant Mt Weld deposit in WA - one of the highest grade rare earths deposits in the world.

📰 See our full Note: LNR Drilling for Rare Earths now

Noble Helium (ASX: NHE)

Our helium exploration Investment Noble Helium (ASX: NHE) just announced a “preferred bidder” has been selected and non-binding heads of agreement have been signed.

The deal could see the preferred bidder pay for:

- The FULL COST of NHE’s TWO upcoming exploration wells up to a maximum of US$20M.

- 50% of the exploration costs already incurred equating to ~US$5M to NHE.

NHE expects to finalise the terms of the deal in the coming weeks.

A successful farm-in deal is a material event for a small cap explorer. This is because in the market’s eyes, it reduces the likelihood of a large, discounted capital raise to fund an upcoming drill program, and the loose stock that inevitably comes with that raise.

This type of looming capital raise typically weighs down a company’s share price.

For this reason, strong farm-ins with favourable terms are coveted by small cap oil & gas explorers, and their shareholders.

📰 See our full Note: Preferred bidder selected for NHE farm out deal

Elixir Energy (ASX: EXR)

The Perth Basin has become a “billionaire's plaything” in recent years, as multiple families have gone into hard fought bidding wars over prime gas ground.

Stokes, Rinehart, and Ellison have each thrown money around to grab a stake in the Perth Basin following material gas discoveries.

On the east coast, billionaire interest in finding gas in Queensland’s “Taroom Trough” has only recently started.

Our Investment in Elixir Energy (ASX: EXR) is gearing up to drill its project in the region later this year.

📰 See our full Note: EXR drilling in the heart of the billionaire playground

⏲️ Upcoming potential share price catalysts

Updates this week:

- LNR: >10,000m drill program at rare earths project in WA.

- LNR kicked off its drilling program on Wednesday, see our note on the news here.

- IVZ: Drilling oil & gas target in Zimbabwe, Myuku-2 (Q3, 2023).

- IVZ is raising $10M at 12c per share via a Share Purchase Plan, see our Quick Take on the news here.

- NHE: Scheduled to drill two targets at its helium project in Tanzania (Q3 2023).

- NHE put out an update on its farm-in negotiations, see our take on the news here.

- DXB: Interim Analysis of Phase III Clinical Trial on FSGS (Q4 2023).

- DXB is raising up to $12M to finance its phase III trials, see our Quick Take on the news here.

No material news this week:

- KNI: Drilling 3/3 of its Norwegian battery metals projects in Europe.

- LCL: Maiden drilling underway at primary PNG copper-gold target.

- TG1: Drilling at its NSW gold project in May.

- TTM: Drilling campaign at flagship Dynasty gold project.

- GTR: Maiden resource estimates across two of its uranium projects in Wyoming, USA.

- GAL: Drilling at its Callisto PGE discovery in WA.

- TMR: Maiden JORC resource estimate for its Canadian gold project.

- BOD: Phase III clinical trial for CBD insomnia treatment.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.