ONE: Med Tech into 18 new US hospitals and a sales pipeline of ~€53M in potential recurring revenue.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,382,258 ONE Shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

We just took a pretty big swing (by our standards) into ASX listed medical tech company Oneview Healthcare (ASX:ONE)’s just announced $19M capital raise (at 19c).

The raise was open and shut over a couple of hours on Friday after market.

ONE sells software technology to hospitals.

ONE’s tech connects various hospital systems and runs on hospital TVs, tablets, and mobile devices so patients can get information, control their room, and request help while giving staff better visibility and smoother workflows.

We think the recent and indiscriminate SaaS/tech sell off of the last couple of weeks/months (SaaSpocalypse) has been way overdone.

(especially for companies like ONE)

And thrown up some great valuations for companies that probably aren't going to be affected.

(like ONE, in our opinion)

Hospitals are notoriously hard to sell into. ONE already has plenty of sales traction AND has been going hard on using AI to develop its software since 2023, when AI first caught people’s attention.

(source)

So ONE has already been building a moat by being VERY early adopters of AI for software development.

(not to mention ONE’s moat of selling into hospitals - the sales timelines here are very slow in hospitals however they are sticky customers)

ONE’s FY25 revenues were ~A$21M (up 21% year on year) - recurring revenues are ~A$13.3M (up 7%).

(Note: ONE’s FY ends on December 31st like US companies, and the end of FY results were released in February this year for the year ending Dec 31st 2025)

At the same time, costs are coming down too - down 9% in H2-2025 vs H1-2025 (thank you AI productivity gains).

We Invested in this latest raise because we think ONE’s hit an inflection point for its business.

ONE started going after the US market a few years ago, and so far, growth out of the US has been relatively strong.

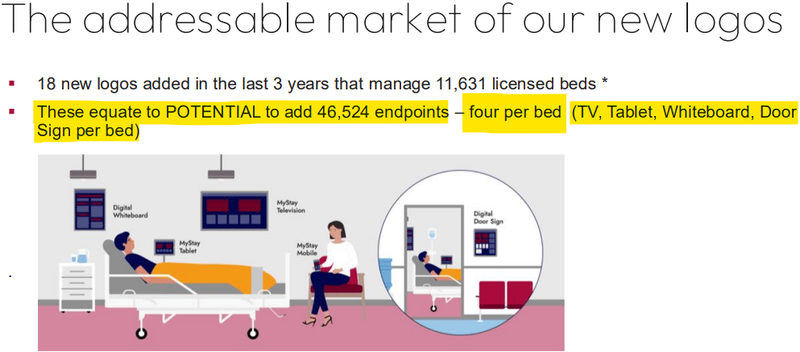

In the last 3 years, ONE’s added 18 new logos (for ONE, a “logo” is a new client health organisation) and ~90% of the beds from those logos are in the USA:

(source)

Other recent news that gave us the confidence to Invest in ONE again were:

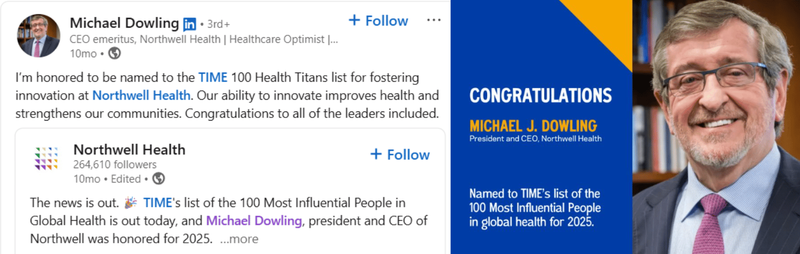

ONE’s new board member in November 2025 - Northwell Health’s long-time CEO Michael Dowling joined ONE’s board. Northwell is one of the largest health systems in the US with ~9,000 beds in New York and Connecticut. Dowling is an industry legend.

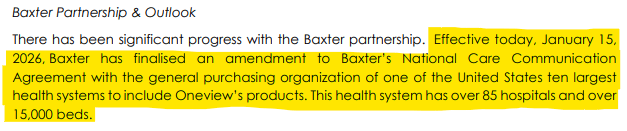

Two months ago - ONE announced it was added to the “Group Purchasing Organisation (GPO)” of a Top 10 US hospital network (~85 hospitals and ~15,000 beds).

Strong pipeline - In a recent earnings call, ONE CEO James Fitter made specific mention of the 180+ prospects and ~48,000 endpoints in ONE’s sales pipeline - of which there are ~156 qualified opportunities in the US and Canada alone.

(We think that number is material given ONE had 14,880 endpoints live at the end of Q4-2025). (source)

We saw what happened with our other tech Investment Rocketboots (ASX: ROC) when it announced a major pipeline conversion - it went from 8c to a high of 40c/share.

The past performance of Rocketboots is not an indicator of the future performance of ONE.

ONE is solving a major problem that hospitals all over the world face - nurse shortages and a workforce that can't keep up with demands.

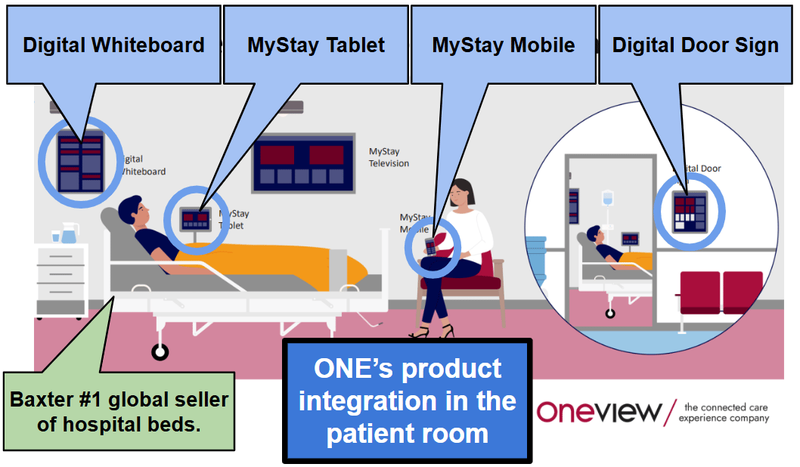

ONE has developed and sells the tech behind smart TVs, bedside tablets, digital whiteboards and virtual care systems in hospital rooms.

There are four “endpoints” in a connected care hospital room which ONE can offer a product and generate revenue - check them out in the image below.

- Digital Door Sign - Screen outside the hospital room showing patient/guest name and safety/status info.

- Digital Whiteboard - In‐room screen showing schedule, care team, and key updates.

- MyStay Tablet - In‐room tablet for info, service requests, and upsells.

- MyStay Mobile - Guest’s own‐device web/app for digital check‐in, keys, payments, and stay info.

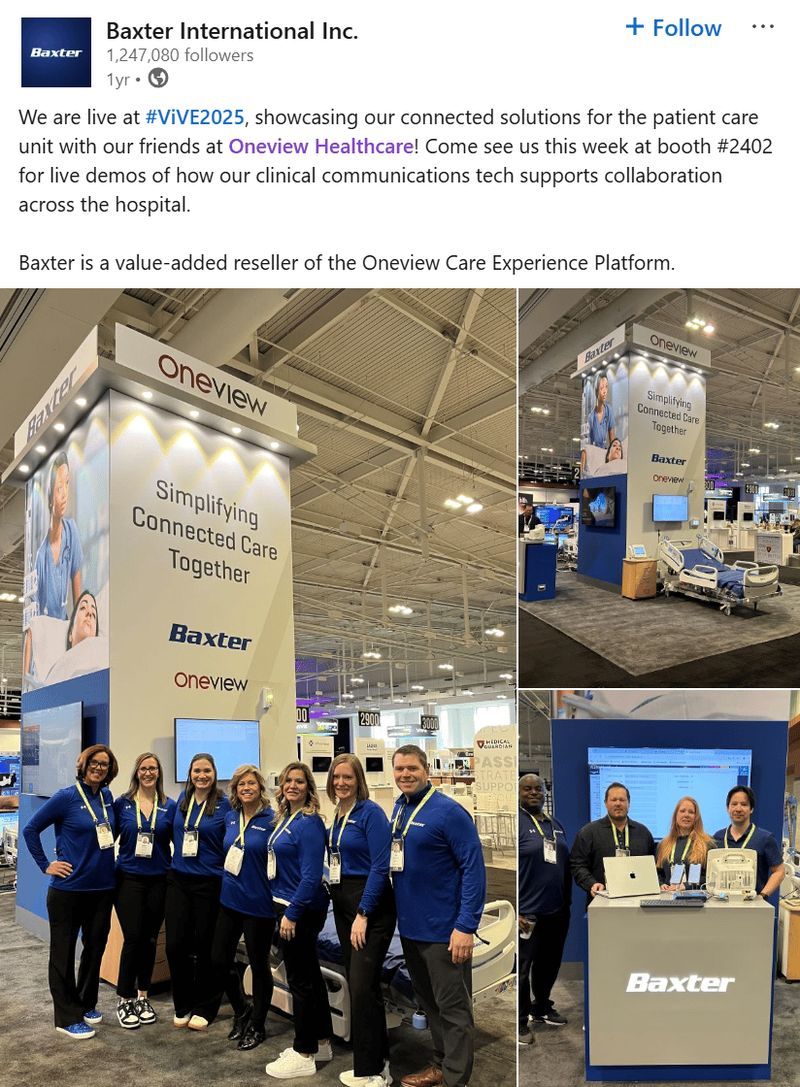

ONE has a Value-Add Reseller agreement in place with one of the world’s biggest hospital bed suppliers - A$13BN capped Baxter International (NYSE: BAX) - they team up to make new sales where Baxter sells the beds and ONE sells the bedside tech:

(source)

Remember, ONE’s customers are hospitals. Notoriously ‘hard to close’ enterprise sales customers that take years to get comfortable enough with a new service to buy it.

But once they do, they become very sticky customers.

For this reason we think the latest trends in technology around vibe coding product and “throwing” it into a hospital won’t work. We think ONE has a strong moat around any new AI vibe coding market entrant.

If anyone is going to get the biggest leverage from using AI coding to make products for hospitals, it's going to be a company like ONE - where it has existing clients and relationships into hospitals, deep domain knowledge... AND was a VERY early adopter of AI software development.

Then there is the big wildcard too - ONE’s AI powered care assistant - “Ovie”.

We think ONE has launched what might become the “Jarvis” (from Iron Man) for hospital networks - AI tech that sits between hospital staff and patients.

(source)

The four different endpoints (and potentially more when the AI ecosystem is in place) is why ONE keeps referencing its “land and expand” strategy.

Land = get one product into a hospital room.

Expand = sell the other endpoints to that same customer AND expand to more rooms.

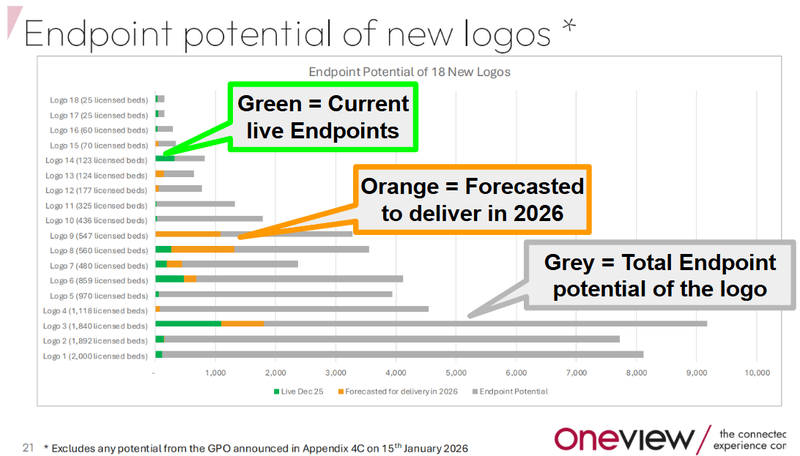

The chart below from ONE’s recent investor presentation summarises that strategy really well.

The green = the landing (getting the first product into the hospital room), orange = expanding (ONE’s confirmed upsells) and the grey is all the potential upside from additional “endpoint” sales:

(source)

Again, ONE’s FY25 revenues were ~A$21M (up 21% year on year) - recurring revenues are ~A$13.3M (up 7%).

At the same time costs are coming down too - down 9% in H2-2025 vs H1-2025 (thank you AI productivity gains).

We invested in this raise because we think ONE has hit an inflection point for its business.

We think ONE is now in a position where it can really streamline the business and take advantage of the leverage that previous years’ investment has provided them. We also think ONE”s long term use of AI internally can drive costs down even further.

Finally, there should be a big enough cash runway for the groundwork over the last two years to translate into signed big deals.

Of course, ONE is a small tech company, and it’s a speculative investment with no guarantee of success.

Today, we will run through:

- Why we took a big (by our standards) swing in the completed ONE capital raise announced today,

- More on ONE’s AI care assistant - "Ovie",

- More on ONE’s sales pipeline,

- More on the Baxter partnership,

- M&A in the hospital bed space,

- And our new ONE Investment Memo - outlining what we want to see ONE achieve over the coming 12-18 months.

Oneview Healthcare

(ASX:ONE)

ONE is solving for one of the biggest problems hospitals all over the world face - nurse shortages and a workforce that can't keep up with demands.

ONE sells its tech to hospital networks like the private hospital Epworth in Australia. (source)

BUT, the bigger market ONE is growing into is the US market.

ONE is already generating revenues in the US - selling to three of the top 25 hospital networks in the country AND it has a distribution deal with A$13BN, NYSE listed, Baxter International. (source)

(more on the Baxter partnership in a second).

The US focus is a big part of the reason why we like ONE.

Hospitals all over the world are under the pump, and at the same time are under pressure to maintain high “patient experience scores”.

Patient experience scores (called HCAHPS in the USA) matter because they directly impact hospital finances (through reimbursement rates).

Up to 30% of a hospital's reimbursement score depends on how patients rate their care experience.

(so a bad experience score = less funding and vice versa)

(source - Google search “why is HCAHPS important for hospitals in the US”)

So it's not just a "nice to have" in the US - digital tools that improve the patient experiences directly impact hospital top lines.

And we think ONE’s AI virtual assistant - “Ovie” - could be ONE’s dark horse, the AI assistant that patients and hospital staff use that is integrated into all hospital systems.

ONE is growing in the US through a partnership with A$13BN Baxter International - one of the biggest sellers of hospital beds in the world (with access to ~60% of the US market).

(source)

The Baxter partnership was signed back in June 2023 (and then extended to cover Canada too in October 2024).

So far, growth out of the US has been relatively strong - inside the last 3 years, ONE’s added 18 new logos and ~90% of the beds from those logos are in the US:

(source)

Each bed also opens up four different up-sell opportunities for ONE (that’s what ONE means by “land and expand” every time it mentions that phrase).

Basically, when ONE gets into a new “bed”, it can then upsell with 4 different “endpoints” (being the TV, tablet, whiteboard and digital door-sign).

Just focusing on those 18 new logos - 11,631 beds translates to ~46,524 endpoints - an addressable opportunity that sits WITHIN existing customers that ONE quotes at ~€25.6 million per year. (source)

That would be more than ~3x ONE’s current recurring revenue base of €7.7 million. (source)

(the question is how long it takes to get all those endpoints signed up - there is no guarantee ONE can get all four of its products into each bed)

ONE currently has 14,880 live endpoints generating €12 million in revenue in the last 12 months. (source)

(source)

All of the above is from the 18 new logos ONE’s signed in the last three years, it DOES NOT include:

- ONE’s new board member in November 2025 - Northwell Health’s long-time CEO Emeritus - Michael Dowling joined ONE’s board. Northwell is one of the largest health systems in the US with ~9,000 beds in New York and Connecticut.

- The deal signed in January 2026 - ONE announced it was added to the “Group Purchasing Organisation (GPO)” of a top-10 US hospital network (~85 hospitals and ~15,000 beds).

(source)

(source)

Between Northwell and the GPO, that’s ~24,000 beds (OR 96,000 endpoints).

Back of the napkin (very rough) calculations here, based on the assumptions in ONE’s latest investor presentation - but that’s an addressable market of ~US$53M in annual recurring revenue.

For $173M capped ONE (post-capital raise at 19c per share).

(These are very rough calculations and more of a way for us to get an idea of the addressable market opportunity - we could be way off the mark and the number could be a lot lower then we have estimated)

We have been Invested in ONE for over just over 5 years now, but finally we think ONE’s passed "peak innovation" - the heavy investment in Digital Whiteboard, Digital Door Sign, MyStay Mobile, and the new front-end is largely done.

Fun fact: ONE's team is using AI internally - 76% of ONE's engineers report saving more than 15% of their time through AI-assisted development.

We are starting to see that reflect in ONE’s financials too - operating costs declined 9% in H2-2025 vs H1-2025 and ONE is guiding more improvements in 2026. (source)

Now it's about deploying and selling.

Thanks to the “SaaSpocalypse” - it looks like ONE’s business may actually be streamlined.

AND give ONE more time/capacity to do what AI can't do well yet... deploying and selling ONE’s product offerings - where ONE can leverage the trust/delivery track record it's built with its hospital networks over decades.

That’s why today we are launching our new ONE Investment Memo which will cover:

- What ONE does

- The macro theme for ONE

- Our ONE Big Bet

- What we want to see ONE achieve

- Why we are Invested in ONE

- The key risks to our Investment Thesis,

- Our Investment Plan

(The full memo is at the end of today’s note)

Before then, here are the 10 reasons why we are Invested:

10 reasons why we are Invested in ONE:

- Proven tech, liked by customers

ONE is moving into the growth stage having proven out its tech products in a hard to enter sector (hospitals). Customers are sticky and sign long term contracts.

- Newly launched AI-powered care assistant (“Ovie")

ONE just launched their new AI powered ecosystem ("Ovie") which includes four products: Ovie Engage (context-aware patient prompts), Ovie Voice (language interaction), Ovie Console (real-time operational visibility for staff), and Ovie Rounds (guided experience rounding). We think ONE could be launching what might become the “Jarvis” for hospital rooms and is one of the first movers.

- Nursing shortages driving demand for healthcare solutions

There is currently a 3 million global nurse shortage and in the US there are more than 260,000 nursing positions unfilled. We think ONE’s products can help alleviate this problem.

- ONE is at an inflection point

We think ONE is at an inflection point for the business where it has reached “peak innovation” meaning all of the big ticket investment into hardware and software has happened and the company is now in sales/deployment mode.

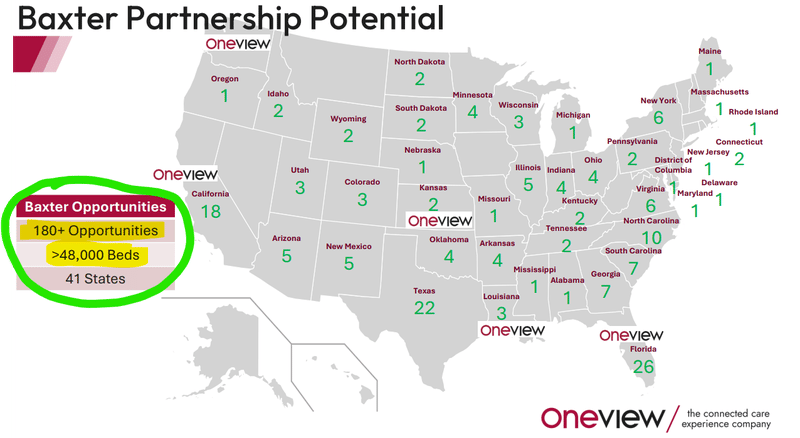

- Sales pipeline (180+ opportunities, 48,000+ endpoints, 156 qualified US/Canada opportunities)

ONE's sales pipeline is at an all-time high with endpoints that would be more than 3X ONE’s current installed base. A lot of the groundwork has been done building up the pipeline, now with the capital raised today ONE finally has a strong cash runway and opportunity to deliver big sales deals.

- US distribution partnership with A$13BN Baxter International

Baxter is one of the world’s largest hospital suppliers and in the US they sell to more than 60% of all beds inside the US. Baxter and ONE signed a Value Added Reseller agreement where Baxter resells and co-sells ONE's platform through Baxter's existing hospital relationships. The deal has since been extended to July 2027 and expanded to include Canada.

- Land and expand strategy means each hospital bed opens the door for multiple sales (endpoints)

We like ONE’s strategy of “landing” (getting one of its products/services into a hospital room) and then “expanding” by cross/up-selling its four different endpoints (TV, tablet, whiteboard, digital door sign). As a result, we think ONE can grow exponentially as it gets into new beds and add to that by upselling to existing customers.

- Added to the GPO of a top-10 US hospital network

In January 2026 ONE announced it was added to the Group Purchasing Organisation (GPO) of one of the United States' ten largest health systems. This network has over 85 hospitals and over 15,000 beds. That single network is an addressable market of ~45,000 different endpoints for ONE.

- Revenue growing, costs declining (thank you AI)

FY25 revenue hit €12.0 million (up 21% year-on-year). Recurring revenue reached €7.7 million (up 7%). On the cost side, cash operating expenses were down 9% in H2-2025 vs H1-2025. We think ONE is now in a position where it can really streamline the business and take advantage of the leverage that previous years investment has provided them. We also think use of AI internally can drive costs down even further.

- ONE a very early adopter of AI for software development (2023)

Hospitals are notoriously hard to sell into. ONE already has plenty of sales traction AND has been going hard on using AI to develop its software since 2023. If anyone is going to get the biggest leverage from using AI coding to make products for hospitals, it's going to be a company like ONE where it has existing clients and relationships into hospitals, deep domain knowledge... AND was a VERY early adopter of AI software development.

Ultimately, we are hoping a combination of these factors help ONE achieve our Big Bet as follows:

Our ONE Big Bet:

"ONE re-rates to a +$500M market cap as it converts its sales pipeline into signed contracts and/or attracts a takeover bid at a premium to its market value"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our ONE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

More on ONE’s AI care assistant - "Ovie"

The wildcard for ONE... its AI powered care assistant - “Ovie” that runs on patient TVs, tablets, and clinician devices.

(source)

There is a 3 million global nurse shortage right now.

In the US alone, more than 260,000 nursing positions are unfilled - and it's only going to get worse. (source)

We think ONE’s “Ovie” service offering could slot in nicely to solve the nurse shortage problem in the US especially.

Ovie is designed to help patients help themselves - ordering meals, controlling their room, asking questions - while giving nurses real-time visibility into patient needs and requests.

The Ovie ecosystem includes four products:

- Ovie Engage - context-aware patient prompts (launching at ViVE 2026)

- Ovie Voice - natural language interaction (pilot in 2026)

- Ovie Console - real-time operational visibility for staff (pilot in 2026)

- Ovie Rounds - guided experience rounding (future product)

We think Ovie is important for two reasons:

First, ONE can now sell an all encompassing AI solution on top of its existing platform.

Second, the AI ecosystem builds a moat around ONE’s platform.

IF Ovie becomes the assistant of choice for a hospital's staff and patients, then the ecosystem it runs on does too.

(imagine if you had Siri but no Apple devices to use it)

More on ONE’s sales pipeline

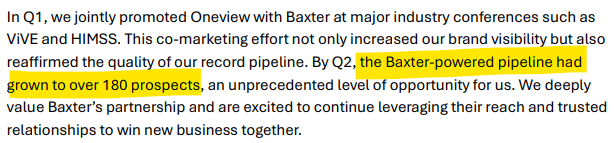

We listened in on the AGM back in December (see our key takeaways here) where ONE’s CEO James Fitter talked about how ONE’s sales pipeline was at an all time high.

He made specific mention of the >180 prospects and 48,000 endpoints in ONE’s sales pipeline - of which there are ~156 qualified opportunities in the US and Canada alone.

(We think that number is material given ONE had 14,880 endpoints live at the end of Q4-2025). (source)

Here is a nice slide from ONE’s most recent presentation, which shows that those 180+ opportunities could mean >48,000 beds.

(Source)

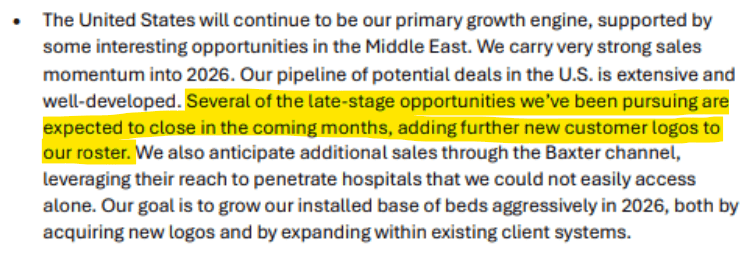

We also noticed this in ONE’s AGM announcement back in December - “Several of the late-stage opportunities we’ve been pursuing are expected to close in the coming months, adding further new customer logos to our roster”.

(Source)

So hopefully we see a few deal announcements inside the coming weeks & months.

We're not saying it's all going to convert tomorrow. Hospital procurement is notoriously slow - but we like that the size of the addressable opportunity is multiples of ONE’s current business.

More on the Baxter partnership - access to 60%+ of US hospital beds

We keep coming back to Baxter because we think it adds to ONE's distribution advantage in the US.

A$13BN Baxter International is one of the world's largest hospital suppliers. Its products - IV solutions, pumps, nutritional therapies - are in more than 60% of US hospital beds.

In 2023, Baxter and ONE signed a Value-Added Reseller Agreement where Baxter would resell (and co-sell) ONE's connected platform through Baxter's existing hospital relationships.

Then in October 2024, the deal got extended by two years through to July 2027 and Canada was added to the regions covered by the deal.

That was an early decision to continue the deal (only 15 months into the first 2 year term).

Clearly Baxter liked what they saw moving early on the extension (and expanding the deal to cover Canada).

We think the Baxter deal is important because it means ONE doesn't have to build a massive direct salesforce to knock on the doors of thousands of US hospitals, ONE has Baxter's salesforce doing all the introductions.

And it seems to be working so far.

In the last 3 years, ONE’s added 18 new logos and ~90% of the beds from those logos are in the US:

(source)

At least five of those deals came from the Baxter VAR deal:

(source)

And finally, on M&A in the hospital bed space

Part of why we think Baxter is very interested in expanding its relationship with ONE is due to two pressing factors.

First, is the need for hospitals to modernise - Baxter has previously signalled in its earnings presentations that it is going hard at improving its tech offerings so that it maintains market share.

Second, is the fact that if Baxter doesn’t keep pace on the tech front, its competitors will step in to provide these modernised products and services, ultimately eating into Baxter’s market share.

Baxter’s key competitor in the US healthcare market is the US$128BN Stryker which is a massive medical technology company.

Baxter and Stryker are major producers of hospital beds:

How to differentiate yourself from competitors when selling hospital beds?

Bolt on some digital technology to improve the patient experience and hospital staff efficiency.

Stryker has been on an almighty acquisition spree, making 54 acquisitions in the last decade or so, with an average deal value of US$743M. (Source)

Recently Stryker has been scooping up tech companies left right and centre to improve its offering - meaning Baxter needs to rise to the challenge by adding complementary products and services as well.

Two interesting acquisitions by Stryker include:

- $3BN for a hospital staff communications platform called Vocera, and

- September 2024 for a company that is an ‘AI-assisted virtual care platform’ called care.ai: an undisclosed amount in an acquisition completed in

Aggressive M&A from a competitor like Stryker would likely be getting Baxter’s attention.

If your biggest competitor is going hard on tech deals to improve its product offering - it would definitely become harder to sit and do nothing.

Especially for something like a hospital bed where sales are probably made on the margins.

Hospital beds are the centrepiece of hospital rooms but the differentiation happens on the margins - the tech that sits around it.

All of the technology that sits around a bed is what can be the differentiator in a company's product offering - so the tech can be an important way of getting ahead of a competitor.

The ONE and Baxter deal for now is a Value Added Reseller Agreement (VAR), where the companies collaborate to integrate and sell the combined products.

Baxter has spent the last two years showcasing the two systems together and training its sales staff (at which point they decided to extend the partnership for another two years - as mentioned earlier).

And now there is a 180 strong pipeline of opportunities to go after:

(source)

IF those pipeline opportunities start converting quickly into signed deals, then who knows how the partnership could change between the two (ONE and Baxter).

Oneview Healthcare

NEW Investment Memo: Oneview Healthcare (ASX:ONE)

Opened: 16-03-2026

Shares Held at Open: 7,382,258

What does ONE do?

Oneview Healthcare (ASX:ONE) is a health tech company that provides hospital networks the tools to build a virtual care and digital control centre for its patients.

ONE has developed the software that powers smart patient TVs, bedside tablets, digital whiteboards, digital door signs, virtual care, and mobile patient apps, all integrated into the hospital's clinical systems.

ONE also has a new AI-powered digital care assistant called "Ovie" designed to address the global nursing shortage.

What is the macro theme?

Nursing shortages are a systemic issue in hospital networks creating a problem for technology to solve.

Big tech companies like Google, Amazon and Microsoft are looking to enter the health tech space and companies with an early-mover advantage should thrive or become takeover targets.

We think AI will transform the standard of care in hospitals. Hospitals need to adopt AI but most don't have the internal capability to build it.

ONE is building its own AI care platform which we hope plays a role in that transformation.

Our ONE Big Bet:

"ONE re-rates to a +$500M market cap as it converts its sales pipeline into signed contracts and/or attracts a takeover bid at a premium to its market value"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our ONE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

10 reasons why we are Invested in ONE

- Proven tech, liked by customers

- Newly launched AI-powered care assistant (“Ovie")

- Nursing shortages driving demand for healthcare solutions

- ONE is at an inflection point

- Sales pipeline (180+ opportunities, 48,000+ endpoints, 156 qualified US/Canada opportunities)

- US distribution partnership with A$13BN Baxter International

- Land and expand strategy means each hospital bed opens the door for multiple sales (endpoints)

- Added to the GPO of a top-10 US hospital network

- Revenue growing, costs declining (thank you AI)

- ONE, a very early adopter of AI for software development (2023)

What do we expect ONE to deliver?

Objective #1: Sales pipeline conversion into signed contracts

ONE has 180+ opportunities and 48,000+ endpoints in its sales pipeline. We want to see this translate into new signed deals, new customer logos, and accelerating endpoint growth.

Milestones we are tracking:

- ✅ Added to GPO of top-10 US hospital network (January 2026)

- 🔲 First hospital wins from the Top 10 US hospital Group Purchasing Organisation network

- 🔲 New logo wins.

- 🔲 Installed beds converted into multiple “endpoints”.

Objective #2: Rollout of “Ovie” AI services

We want to see the Ovie AI product suite move from announcement to live deployment and start contributing to per-endpoint revenue uplift.

Milestones we are tracking:

- ✅ Ovie digital care assistant unveiled

- 🔲 Ovie Engage launching at ViVE 2026

- 🔲 Ovie Voice pilot commenced (2026)

- 🔲 Ovie Console pilot commenced (2026)

- 🔲 New user experience delivered (H2 2026)

- 🔲 First Ovie-related revenue contribution

Objective #3: Revenue growth and path to breakeven

We want to see ONE continue its consistent growth trajectory and demonstrate a clear path to operating cash flow breakeven.

Milestones we are tracking:

- 🔄 CY2026 live deployment growth of 20% (~17,850 endpoints per guidance)

- 🔄 Continued decline in cash OpEx through 2026

- 🔲 Breakeven achieved

Objective #4 (Bonus): Strategic interest or M&A activity

This is the complete wildcard - which we don't have a base case expectation - but if ONE can show enough progress and growth then it could become an M&A target for the bigger players in the hospital room products space.

What could go wrong?

Sales / pipeline conversion risk

ONE has a large and growing pipeline, but hospital procurement cycles are long and unpredictable at typically 18 months to 2 years. Being added to a GPO (Group Purchasing Organisation) doesn't guarantee purchase orders, it just means ONE is on the approved vendor list. ONE's pipeline of hospital opportunities may take longer than expected to convert into signed contracts, or may not convert at all. We see this is the single biggest risk to our investment thesis.

Baxter dependency risk

A key part of ONE's US strategy relies on Baxter's salesforce co-selling and reselling ONE's products. If Baxter moves slowly, reprioritises, or if the partnership doesn't deliver the volume of introductions we hope for, this could materially slow ONE's US growth. The Baxter-led pipeline is beyond ONE's direct control.

Funding risk / dilution risk

ONE had €4.6 million in cash at 31 December 2025 and has been consuming approximately €1.4 million per quarter in net operating cash outflows. Growth companies need cash to achieve their goals. ONE has raised $19M (plus has a planned $2M Share Purchase Plan for existing holders) to extend its cash runway, but if the company doesn't convert pipeline into revenue at the pace needed, further capital raises may be required, which would dilute existing shareholders. ONE has raised capital multiple times since listing in 2016.

Market risk

Tech stocks could fall in value again. Even if ONE does everything right from an operational standpoint, the market could always sell off or favour different sectors. ONE is a small-cap health tech stock and is subject to broader market sentiment.

Other Risks

Like any small-cap technology company operating in the healthcare sector, ONE carries significant risk, here we aim to identify a few more risks.

ONE’s technology must integrate seamlessly with complex, legacy hospital IT systems, including Electronic Health Records (EHR) and building management software. There is a high implementation risk that deploying these systems across large hospital networks takes much longer and costs more than anticipated, which can delay revenue recognition and frustrate clients.

The company also handles highly sensitive patient information and operates in a strictly regulated environment, primarily governed by HIPAA laws in the United States. Any data breach, cyberattack, or failure to comply with these stringent privacy regulations could lead to severe financial penalties, lawsuits, and irreversible reputational damage that would cripple the business.

While ONE’s new AI-powered care assistant, "Ovie," presents a significant growth opportunity, it also introduces new technology and adoption risks. There is no guarantee that overworked hospital staff or patients will actually adopt and use the new AI tools, or that the AI will perform flawlessly in a high-stakes clinical environment where software errors can have serious consequences.

Furthermore, hospital budgets are notoriously tight and heavily dependent on government reimbursement rates and private insurance payouts. If macro-economic conditions worsen, or if healthcare funding is cut, hospitals may freeze capital expenditure, causing ONE's target customers to delay or cancel their planned digital upgrades.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ONE Investment Strategy

We plan to hold a position in ONE for the next 3-5 years (and beyond) as it progresses its plan to gain significant market penetration in the lucrative US healthcare market, and (as always) may look to take some profit by selling up to ~20% of our holding if the company successfully delivers on the key objectives listed above and the share price hopefully re-rates again.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.