MNB reveals first glimpse of green ammonia project - Financiers now circling

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,645,000 MNB shares and 1,562,500 options at the time of publishing this article. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

Ammonia is the key ingredient in fertilisers and mining explosives.

The main ingredient in ammonia production is hydrogen which is made by burning fossil fuels.

Ammonia production contributes 1% to 2% of global CO2 emissions.

If the dirty hydrogen can be replaced with clean hydrogen produced from renewable energy, we get green ammonia.

Now, what if that renewable energy is some of the cheapest in the world and is readily available, so construction of a clean energy plant is not required...

With a view to create green ammonia, on 14 December 2022, Minbos (ASX:MNB) secured supply of some of the world’s cheapest clean energy via an MOU with the Angolan energy operator:

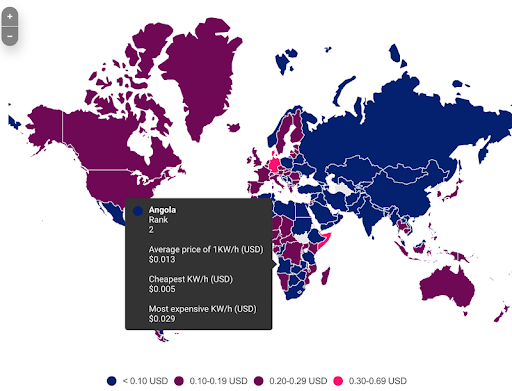

Angola’s abundant renewable energy capacity (hydroelectricity) ranks the country as having the second cheapest source of electricity on the planet.

That means, MNB’s input power costs will be about 1/16th of what Australian and US industry users pay.

MNB then appointed an expert green ammonia plant builder called Stamicarbon to do a technical study on how this cheap, available, clean electricity can be used to generate green ammonia.

Stamicarbon cranks out fertiliser projects - it has over 250 under its belt. It is a global leader in the field of green ammonia, and built the world’s first industrial-scale renewable energy ammonia project in Kenya.

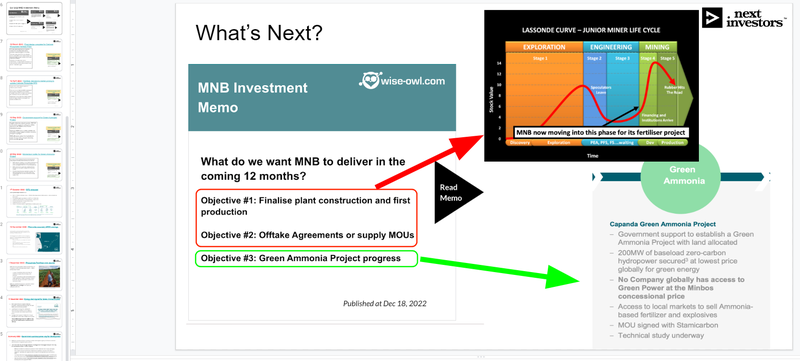

Today our 2022 Wise-Owl Pick of the Year, MNB, has released the results of Stamicarbon’s technical study.

The Stamicarbon study concludes that by spending €365 to €496M (CAPEX), MNB can build a green ammonia project that can generate 112,000 tons of green ammonia per year, to be used to produce ammonium nitrate for fertilisers and mining explosives.

Given this is a technical study (NOT a pre-feasibility study) no estimates of revenue or Net Present Value has been revealed yet.

For today, the roughest calculation and assumptions we can come up with to get a ballpark, potential yearly revenue figure is:

- Take production of 730 tonnes ammonia nitrate per day from 50% of the produced green ammonia (page 10 of announcement)

- We will assume 100% dedicated to production of ammonia nitrate (to make our calculation easier)

- 730 tonnes ammonia nitrate per day x 2 = 1460 tons per day

- Assume 95% plant availability (350 days per year) = 511,000 tons per year

- Assume lower band of publicly available ammonia pricing at US $300/t

- Assume full capture of inland African premium of US $200/t

- Ammonia Nitrate price to be used: US $500/ton

Multiply the estimated ammonia nitrate production tonnes per annum (511,000) by the assumed ammonia nitrate price (US$500).

Potential yearly revenue = ~US$255M

Now if we multiply this potential yearly revenue by the life of MNB’s cheap, clean electricity contract (25 years), we get:

US$255M x 25 years = ~US$6.38 billion

...over the life of the project - obviously this number is ignoring all costs to build and operate the plant, and also does not allow for the power contract to be extended beyond 25 years.

Note: These are VERY rough and basic calculations to get a ballpark idea of the potential revenue over the lifetime of the project. Assumptions have been made by us to arrive at this number - these assumptions could be wrong. It is for illustrative purposes only and should not be relied upon.

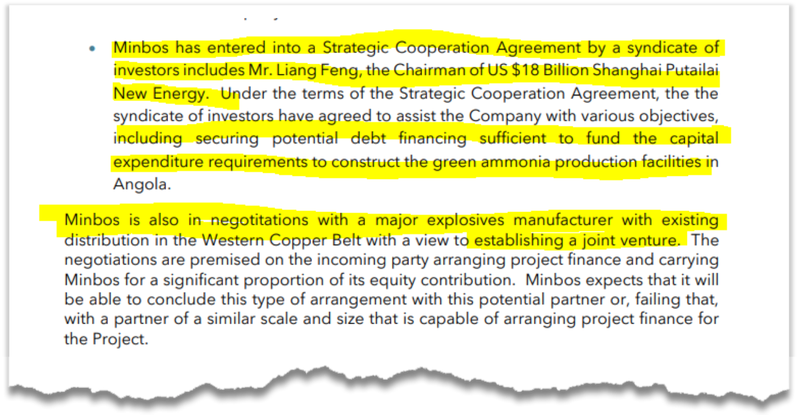

MNB has already said interest exists to fund the €365 to €496M CAPEX required.

With its next study, a pre-feasibility study (PFS), we will have actual numbers around the potential project value which should further assist in securing financing.

CAPEX funding is always on the minds of investors - we also noted from today’s announcement the following comments about CAPEX funding:

And

And

Today’s technical study was our first look at early economics around this project.

All up, the study found that MNB’s proposed project in Angola has all the pieces needed to be the premier viable Green Hydrogen-Ammonia Project globally:

- Extremely cheap installed green electricity pricing;

- A genuinely zero-carbon project;

- High quality water available nearby to produce hydrogen; and

- Proximity to customers.

The technical study details the proposed project’s feasibility from a (you guessed it) - a technical perspective.

It defines all the required process units, plant configuration based on the available renewable electricity, and estimates the CAPEX for the project.

As we noted above, the study has less of a focus on the project’s economics, but does consider potential end use markets for its ammonium nitrate products: fertiliser and mining explosives.

Here’s a summary of our key takeaways from the study:

- Key components locally available: One of the unique aspects of this project, compared to other green ammonia projects, is that all of the project elements exist within close proximity - hydropower for renewable energy, water for electrolysis, and location close to end markets.

- The ‘African Inland Premium’: MNB’s ammonia will deliver local African buyers (agriculture and mining companies) material cost savings when compared to exported ammonium nitrate due to extra costs from marine freight, insurance, packaging, customs and port fees. Or MNB can capture this premium.

- Preliminary Production Breakdown: MNB estimated production of 320 metric tonnes per day of Ammonium Nitrate, consisting ~980 MTPD of Calcium Ammonium Nitrate for use in the local fertiliser industry and ~730 MTPD of Low-Density Ammonium Nitrate for use in mining explosives.

- CAPEX of €365-€496M: This CAPEX estimate (mid-point €432M) is an early estimate for the purpose of concept screening. MNB says it has a "reasonable basis" to expect it will be able to fund the development of the project.

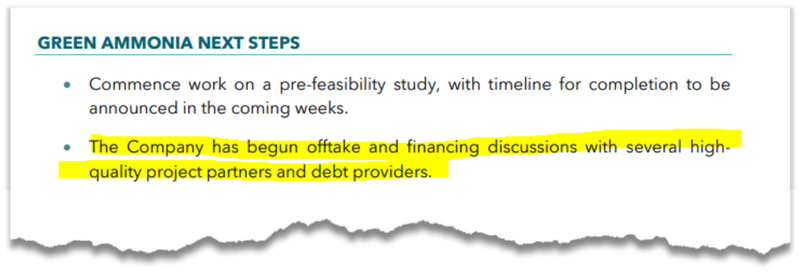

- Offtakers & Financiers circling: MNB has indicated that discussions have begun with potential project financiers and offtake partners, saying it has “received significant inbound interest from major potential funding partners” owing to its unique characteristics.

- Cost of Electrolysers: Electrolysers make up a big portion of the CAPEX and OPEX cost, 33% and 92% respectively. With the green hydrogen industry in the spotlight, we expect new technologies to emerge to drive these costs down which is an opportunity for the project.

MNB announced today a few different funding options that appear to have been in the works for a while now.

The next steps on MNB’s green ammonia project are:

- Commence the pre-feasibility study - where we get some actual revenue and NPV numbers;

- Offtake and financing discussions;

- End-market studies (where will they sell the green ammonia products); and

- Finalise negotiations on green ammonia plant site.

We spent six days in Angola in February meeting the MNB in-country team and visiting the key sites for MNB’s two key projects - read more about our site visit to Angola to visit MNB’s projects.

For the rest of today’s note we will take a deeper look at what’s been released in the technical study.

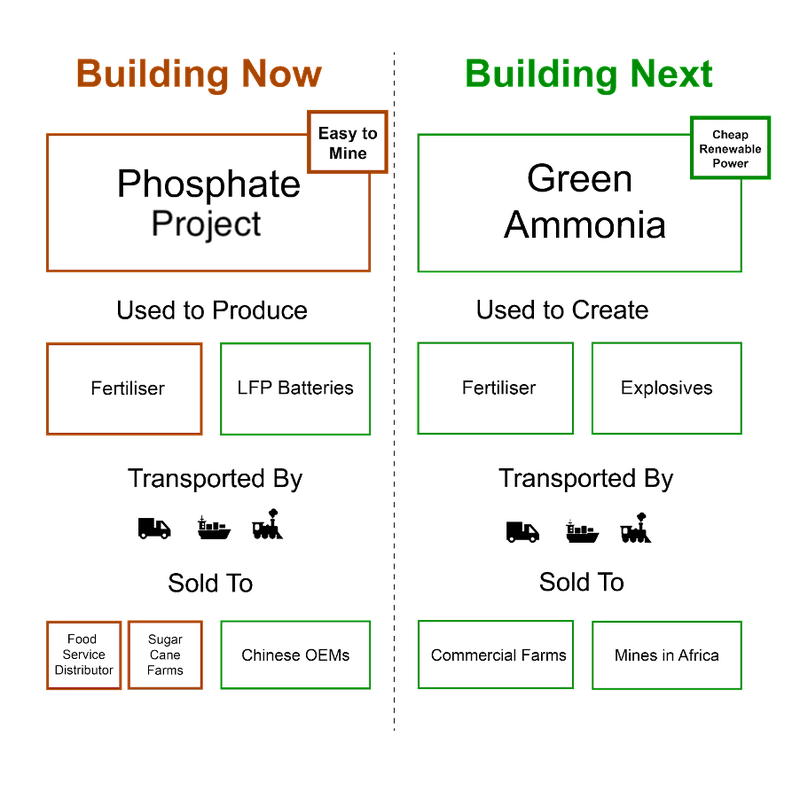

MNB is close to completing its phosphate plant, but today’s news is all about the green ammonia project.

The green ammonia project is MNB’s earlier stage, blue sky project, which is still a few years from production, compared to its phosphate project which is expected to be in production as early as this year.

Here is how the green ammonia project fits into MNB’s strategy that includes its phosphate fertiliser project which is now under construction:

We’ve been Invested in MNB for over 2.5 years. We first took a position back in August 2020 at 3 cents per share. We Invested again at 8 cents, then again at 11 cents during MNB’s most recent capital raise last July. We have Free Carried our first two Investments.

To see why we Invested - check out our Big Bet below.

At the end of the December quarter MNB had ~$17.5M cash in the bank. The company also has ~66 million 15 cent in-the-money options expiring at the end of April.

If these options are fully exercised or underwritten the company could raise up to another ~$10M.

With this cash balance we think that MNB is in a strong position to bring the phosphate project into production and progress the green ammonia project through the feasibility studies.

This brings us to our Big Bet for MNB:

Our Big Bet

“MNB delivers a 10x return by building a profitable phosphate project AND progressing its green ammonia project to construction phase.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MNB Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor the progress MNB has made since we first Invested and how the company is doing relative to our “Big Bet”, we maintain the following MNB “Progress Tracker".

See our MNB Progress Tracker here:

A Deep Dive into MNB’s Technical Study

The purpose of this study was to evaluate the technical feasibility of MNB’s Green Ammonia Project.

Specifically, the study evaluates the utilisation of 200MW of renewable energy power to create ammonium nitrate to sell to end users.

MNB has secured this renewable energy under a power purchase agreement with the Angolan energy operator.

The technical study was conducted by Stamicarbon which — with more than 250 fertiliser projects under its belt — is quickly bringing its technological expertise into the green ammonia space.

Stamicarbon is the innovation and licence company of Milan-listed Maire Tecnimont Group (market cap ~$1.4B) and is a pioneer in the field of green ammonia.

The company built the world’s first industrial-scale renewable energy ammonia project in Kenya.

Stamicarbon’s Director of Technology and Licencing, Dave Franz, said in June last year that MNB’s green ammonia project:

“not only [is] one of the best Green Energy-Powered-Projects globally, but potentially the first Green Ammonia project that is truly competitive with traditional fossil-fuel alternatives.”

The information provided in the technical feasibility study had a +/- 35% level of accuracy. As MNB progresses through the feasibility stages, the level of confidence in the information and assumptions will grow.

The estimated capital cost (CAPEX) to construct the project is €365-496M, however no project valuations (NPV) figures have been estimated yet.

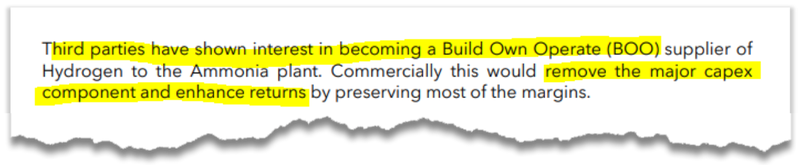

But if third parties follow through with their demonstrated interest in becoming Build Own Operate (BOO) hydrogen suppliers to the ammonia plant, CAPEX could be cut substantially.

We think this technical study is an important step for MNB to legitimise its green ammonia plans, which will help to secure important licences from the government and progress discussions with potential offtake and financing partners.

So, what actually is “green ammonia”?

MNB is aiming to produce green ‘ammonia’, or more specifically, green ‘ammonium nitrate’ (for simplicity we will use the two interchangebly).

Ammonia is used to make fertilisers and explosives.

MNB wants to produce green ammonia for sale into farming and mining sectors locally in Angola, and across Africa.

To make ammonia, hydrogen and nitrogen are combined at high temperatures.

Hydrogen is made by separating water in an energy intensive process called “electrolysis”.

To make the ammonia “green”, the hydrogen must be made using a renewable energy source.

The current process to make ammonia uses fossil fuels and it relies on ‘steam reforming’ which also emits large amounts of carbon dioxide.

Here are the three things MNB need to make “green ammonia”:

- Access to renewable energy

- Access to water to make hydrogen

- A facility to combine the hydrogen with nitrogen to make green ammonia

Project Benefit 1: Readily available green energy source

There were a lot of positives to take from the technical study, but the one thing that really makes it stand out from other green ammonia/hydrogen projects is MNB’s access to an existing renewable energy source.

The green ammonia project will utilise 200MW of local hydroelectric power to create ammonium nitrate for fertiliser and explosives used in the mining sector.

MNB has an agreement with the Angolan government’s energy operator for supply of hydroelectric power at some of the cheapest renewable energy prices on the planet.

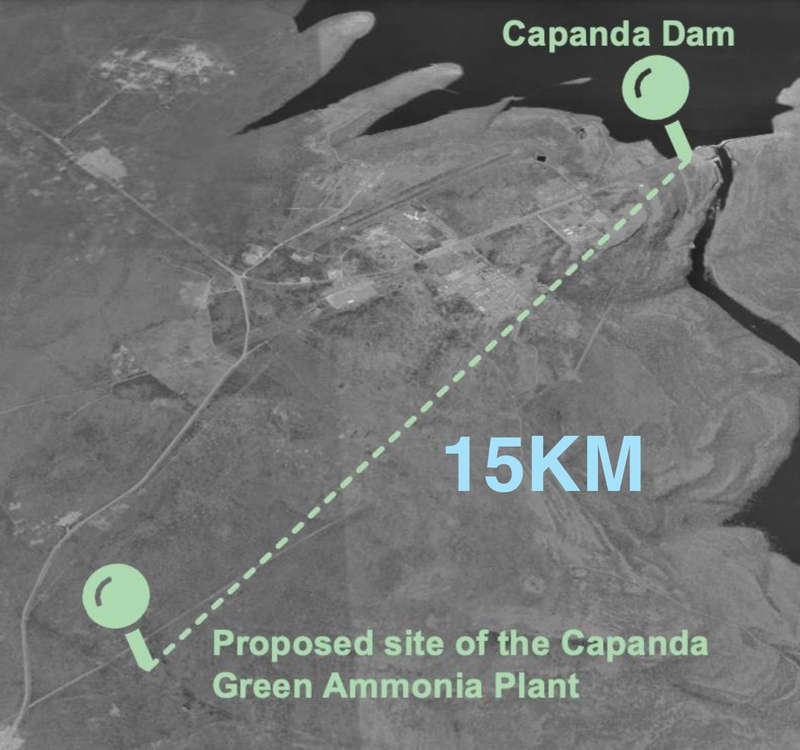

During our trip to Angola we visited the hydro-dam from where MNB will procure its renewable energy:

We spent six days in Angola in February meeting the MNB in-country team and visiting the key sites for MNB’s two key projects - read more about our site visit to Angola to visit MNB’s projects.

What makes this project different to other green ammonia projects is that MNB won’t need to build the renewable infrastructure. It can instead utilise Angola’s existing infrastructure to generate the green power needed to create green ammonia.

This provides MNB with an important point of differentiation - as most of the world's current ammonia supply is produced using fossil fuels (~90%), which comes with a heavy carbon cost.

In order to meet carbon reduction targets, the world’s biggest ammonia producers want to move away from fossil fuels.

To do so, many producers are looking to build renewable energy projects near their existing ammonia plants, which require huge upfront capital investment.

They will also also need a reliable water source, which might not exist in close proximity.

Take the Yara Pilbara’s Yuri Renewable Hydrogen and Ammonia Project, which received $42M in funding from the Australian government last May and has since reached a Final Investment Decision.

This project takes an existing ammonia plant in the Pilbara and replaces the component of ammonia production that uses natural gas to create hydrogen with renewable energy.

Scheduled to commence production in 2023, the project will generate 3,700 tonnes of green ammonia each year.

The cost of the project is around $87M for 3,700 tonnes per year (source).

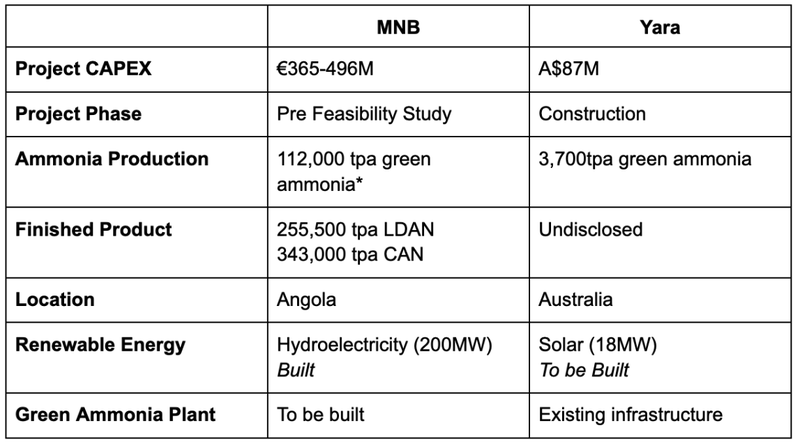

Compare this to MNB’s project which could produce ~598,000 tonnes per year of green ammonia nitrate (980t/d + 730/t/d x 350 days assuming 95% plant uptime) with an estimated project construction cost of €365-€496M (approx. A$600M-A$800M).

The reason MNB could build a project of this scale is that it has secured EXISTING 100% renewable and cheap power and has easy access to a water source.

This is unlike Yara’s Yuri project, which will need to build the renewable infrastructure from scratch.

*take ammonia synthesis number of 320 tons/day (page 10 of announcement) x 350 days per year at 95% plant uptime

How did MNB secure some of the world's cheapest renewable energy?

In 1987 the Russians built a hydroelectricity dam on the Kwanza River. It has a capacity of 520MW per day and generates more than half of all electricity in Angola.

Today, the dam is operated by an Angolan state owned company.

MNB was able to recognise and jump on this opportunity thanks to the many years that its management — in particular director Lindsay Reed — spent in Angola building relationships with stakeholders involved.

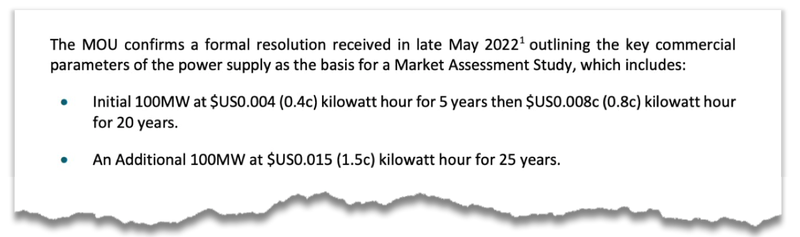

Back in December, MNB signed an MoU to procure renewable energy from this dam.

Energy from that dam is expected to cost MNB US$0.004 to $0.015 per kilowatt hour, with an average cost of power of US$0.011/kwh (1.1c) for the entire 200MW over 25 years.

For context, that’s a fraction of the ~US$0.16/kwh (16c) price paid by industry users in Australia and the USA last year...let alone the >US$0.50/kwh paid in Europe in early 2022.

That’s right - MNB’s input power costs are about 1/16th of what Australian and US industry users pay.

Ultimately, what makes MNB’s green ammonia project so unique is an ideal combination of:

- access to very cheap renewable power;

- a reliable fresh water supply;

- its location within an industrial zone; and

- ready access to agriculture and mining customers.

Benefit 2: Availability of high quality fresh water

In order to make ammonia, MNB will need to make hydrogen. This is done through a process called electrolysis which needs a water source.

MNB has access to a high-quality fresh water source, which is more suitable for electrolysis than saline groundwater or sea water.

Freshwater is more suitable because salt water can corrode the electrolyser and limit its lifespan.

It is also more suitable than desalination or treatment of the seawater/groundwater, as this can be an expensive extra step that increases the production cost.

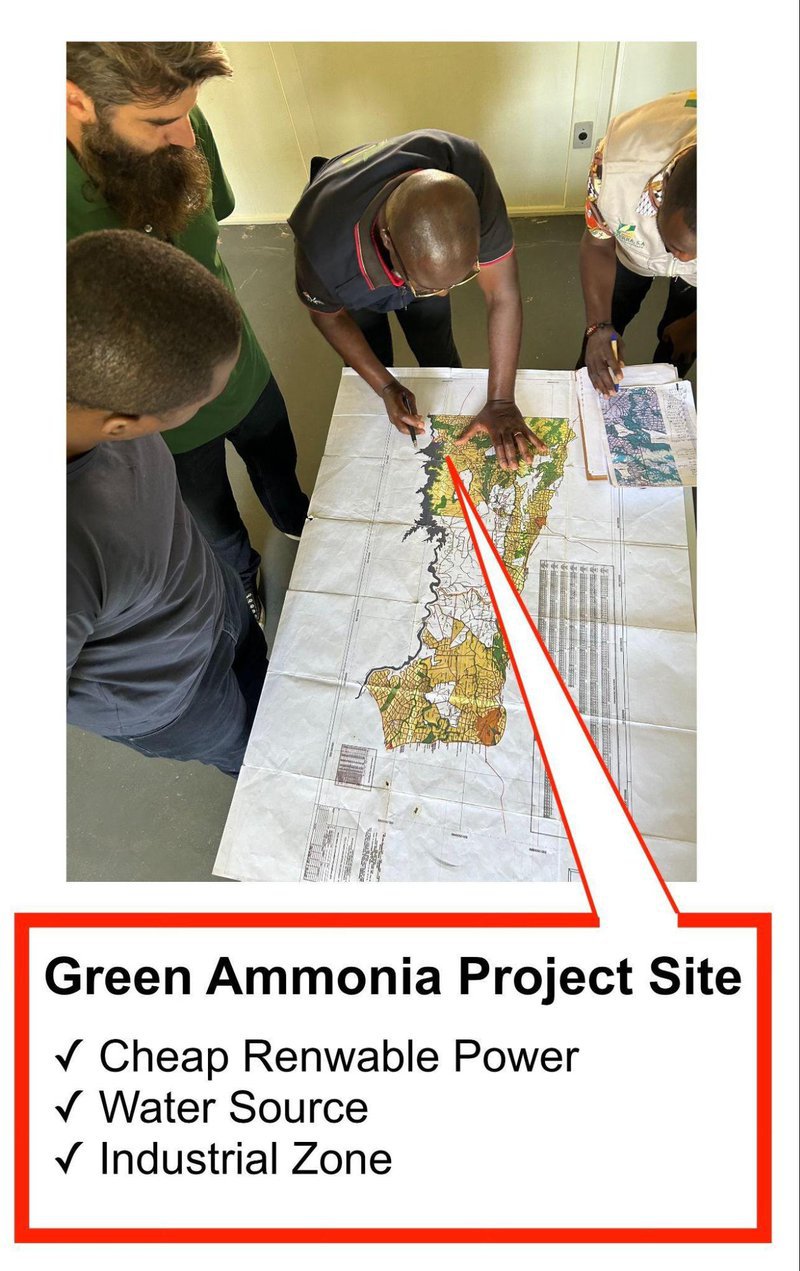

We visited the proposed site for the freshwater supply on our site visit, which is close to MNB’s planned ammonia plant and sits along the Kwanza River:

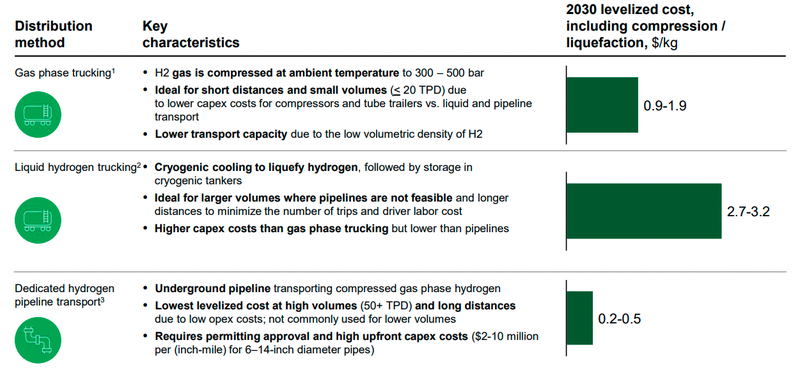

When producing hydrogen, proximity to the ammonia plant matters - because the cost of transporting hydrogen is expensive.

You can’t just make hydrogen anywhere.

According to the “Pathway to Commercialisation Report” by the US Department of Energy - trucking hydrogen can cost up to US$3.20/kg.

Compare this to the current cost to produce hydrogen which is around $3-6/kg today (and needs to be around $2-3/kg to be commercial) - you can understand why this transport cost can render hydrogen projects uneconomic.

Without the dedicated hydrogen pipeline infrastructure to transport hydrogen from the water source to the ammonia plant, green ammonia projects will need to build their plants next to the water source.

For existing ammonia plants, this can be difficult as a water source and/or renewable energy may not be available.

Until the hydrogen transport cost challenge is resolved, projects like MNB’s, that intend to build an ammonia plant in close proximity to BOTH water and renewable energy, will always have an advantage.

The best green ammonia projects will have the ammonium plant + clean water + renewable energy, all within a close distance.

Speaking of proximity, the most important part of MNB’s project is the end market - those who will be the ultimate buyers of MNB’s product.

Benefit 3: Close proximity to end market

There are two main end buyers for MNB’s green ammonia.

- Mining companies that use it for explosives

- Large commercial farms using ammonia fertilisers.

According to the technical study, these end-buyers are likely to be located within Africa,

MNB can capitalise on the “African Inland Premium”.

Essentially, the “African Inland Premium” is a ~$200/t cost saving on MNB’s ammonia products sold to buyers located in inland Africa.

The $200/t saving comes from the absence of costs around marine freight, insurance costs, and port fees.

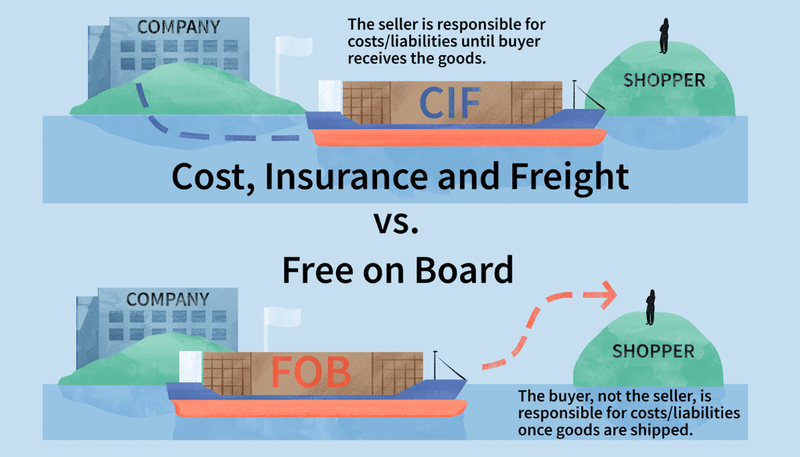

The fertilisers that MNB produce are expected to compete with shipped “free on board” products from West and North Africa.

Under a “free on board” freight system, inland buyers of these products would pay for costs like marine freight, insurance, customs, port fees, packaging costs and land transport.

However, because MNB’s goods are made inland, the end buyers may not have to pay this cost and save around ~$200/t on the green ammonia shipments.

Or the premium can be captured by MNB - we will find out more in the PFS.

There is also an environmental cost with shipping hydrogen long distances — it is “potentially worse for the climate than burning natural gas”, according to mining giant Rio Tinto which says it will only “produce hydrogen where we consume it”.

Because MNB is close to its end markets, it can capture the ‘Africa Inland Premium’ and save on the environmental costs associated with shipping ammonium products.

MNB will provide more details on the market feasibility in the PFS, however the “Africa Inland Premium'' provides us an insight into the potential value of MNB’s project to industries in the region.

Ammonium Nitrate for Explosives

In the technical study, MNB said that it will produce ~730tpd of Low-Density Ammonium Nitrate (LDAN) for explosives.

Explosives are important for the mining industry, used during the stripping of open pit mines. Instead of diggers and jackhammers doing the work, explosives are used to blow up large surface areas (in a controlled manner) to speed up the excavation process.

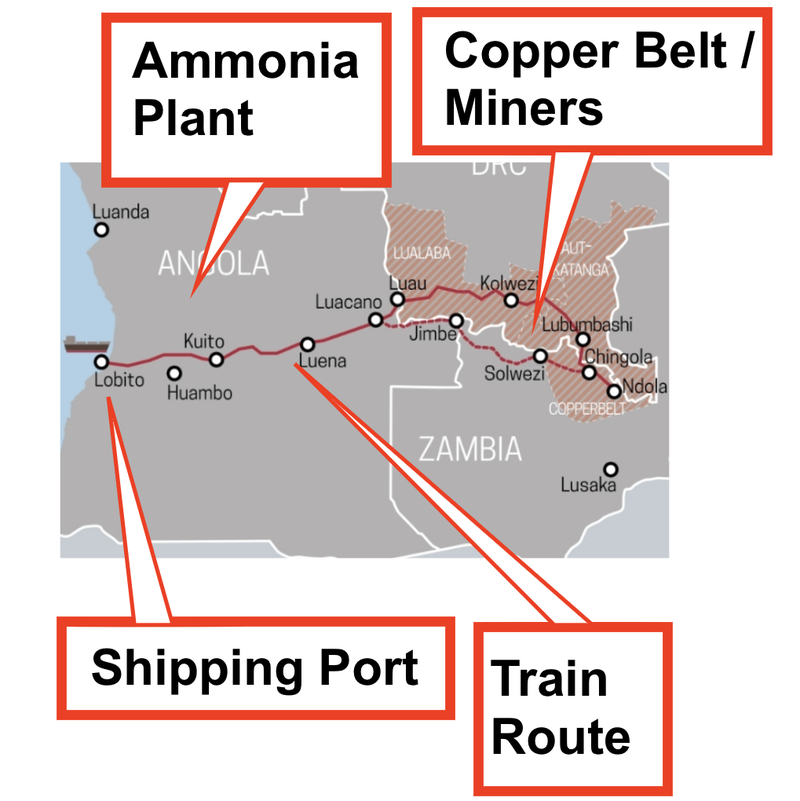

Many mines along the Zambia Copper Belt (which is right next to Angola) use explosives in their mining operations.

MNB will compete with alternative explosives providers from:

- South Africa, where MNB will have a land transport advantage of 1,000km, and

- Global explosives producers, where MNB will have additional marine freight and port cost advantages over seaborne competition.

For these mines, we think having security of supply from an inland African partner (like MNB) will be invaluable.

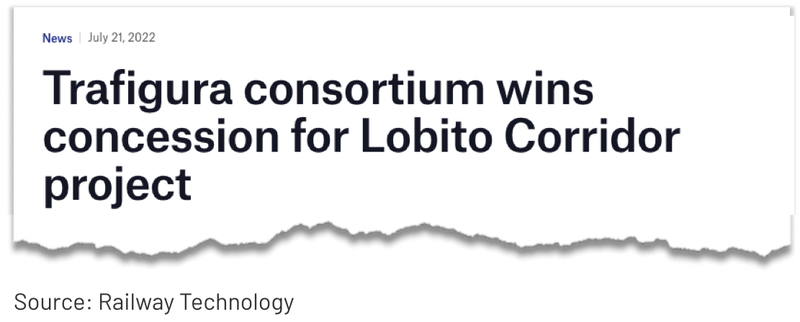

On this front, last November the Angolan government signed a concession to build a railway through the Lobito Corridor.

The Lobito Corridor is a crucial route that links Angola’s tier-1 Lobito Port to the mines that sit along the copper belt in and Zambia the Democratic Republic of the Congo (DRC) - giving better access to global markets.

We visited the Lobito Port which is a tier-1 port giving these miners much better access to the global trade markets:

Although the Lobito Corridor Railway is a long term project, it will provide direct access for MNB to sell its ammonium nitrate for explosives to miners in the area.

MNB will conduct a market feasibility study that will take into consideration the planned rail link.

Ammonium Nitrate for Fertiliser

In the technical study, MNB said that it will produce ~980 tpd of Calcium Ammonium Nitrate (CAN) for fertiliser.

The market for CAN fertiliser is well established and the product can be exported to large scale commercial farms.

However, MNB has noted that the agricultural aspirations of Angola are growing, which means that the market for fertiliser will grow within the country as well.

We think that MNB will be able to use its well established relationships with farmers, government and distributors within the country to build a strong market demand for its product within Angloa.

However, the company still has optionality to sell to large scale commercial farms, either throughout Africa (most of them are in South Africa), or around the world.

MNB will likely deliver its product to market through a mixture of truck haulage and shipping, utilising the access to top tier ports in Lobito or Luanda.

One of the biggest opportunities for the project is in capturing the “African Inland Premium” for nitrogen fertiliser.

MNB’s fertiliser will compete with FOB fertiliser products coming from north and west Africa will not bear the cost of marine freight and insurance, customs and port fees, product packaging and 300km of land transport.

Also, preliminary discussions with the government suggest it might be possible for MNB to produce High Density Ammonium Nitrate. This can serve as both a fertiliser and feedstock for emulsion explosives which make up the biggest share of the mining market. This product could enhance the African Inland Premium

What are the risks?

Permitting Risk

At this early stage of the project a lot of the work done is around permitting and licences.

MNB will need to negotiate with key stakeholders, namely the Angolan government, to secure the important licences to operate the project.

Project Economics Risk

There have been limited studies on the project economics so far.

As the cost of capital increases, funding for large infrastructure projects gets tighter - this coupled with inflation, may negaitivley impact MNB’s ammonia project economics.

What are we watching for next?

🔲 Pre Feasibility Study Commenced

MNB’s next step is to commence work on the project’s Pre Feasibility Study, which will hopefully provide us with more accurate information around the operating costs, revenues, the project value (NPV), and its commercial feasibility.

Market feasibility study

MNB intends to undertake a market feasibility study on opportunities to sell its green ammonia in Angola, and to take advantage of the recently announced Lobito Corridor rail link (Angola, Democratic Republic of Congo and Zambia).

The technical study found that by-product opportunities exist within the Nitrogen Plant, so MNB expects future studies to consider the option to produce oxygen and argon for the local market.

Like all feasibility studies, figures are based on assumptions, and there are still many milestones to progress and risks to avoid for MNB to develop its green ammonia plant.

If you would like to learn more about feasibility studies, how to read them, and what to watch out for, read this educational article here:

🎓Feasibility Studies Explained: Evaluating Project Viability

🔲 Binding power agreement Angolan power network operator

MNB signed an MoU with Angola’s National Electricity Transmission Network (RNT-EP) in December.

The signing was a global green first that outlined the framework and conditions for supply of 100% renewable and installed hydroelectric power from the nearby Capanda Dam and electric substation.

The MoU binds the parties to complete various studies (market assessment including the now-complete technical study, and financial feasibility study) and commit to enter contract negotiations for an Electrical Supply Contract once the project’s feasibility is demonstrated.

🔲 Sign technical, offtake, and investment development partners

We think that there is a big opportunity for MNB, who already has a foothold into the Angolan fertiliser industry to build upon its portfolio of projects and develop the green ammonia plant.

With many in-country relationships cultivated over many years we think that this green ammonia project could become a reality in the not too distant future. Today’s technical study is the first step.

As MNB’s project advances, we expect potential offtake and development partners to become more interested.

We think progress on these points will be made as MNB derisks its project from a technical and feasibility perspective.

Our MNB Investment Memo

Click here for our Investment Memo for MNB, where you can find a short, high level summary of our reasons for Investing.

In our MNB Investment Memo, you’ll find:

- Key objectives for MNB

- Why we are Invested in MNB

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.