LRS takes another step towards lithium production and becoming Sigma 2.0

Published 21-JUN-2023 13:19 P.M.

|

13 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,585,000 LRS shares at the time of publishing this article. The Company has been engaged by LRS to share our commentary on the progress of our Investment in LRS over time.

It’s big enough to be a lithium mine now.

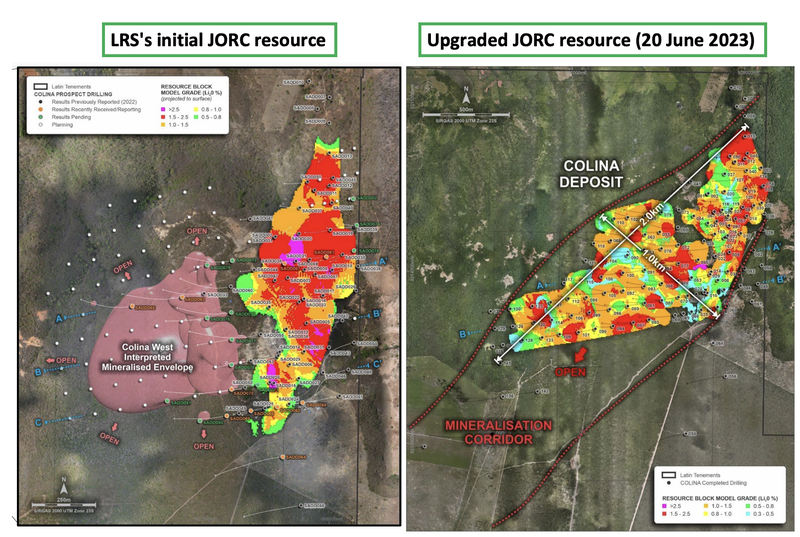

Yesterday our Investment Latin Resources (ASX: LRS) released its long awaited JORC resource upgrade on its Brazilian lithium deposit.

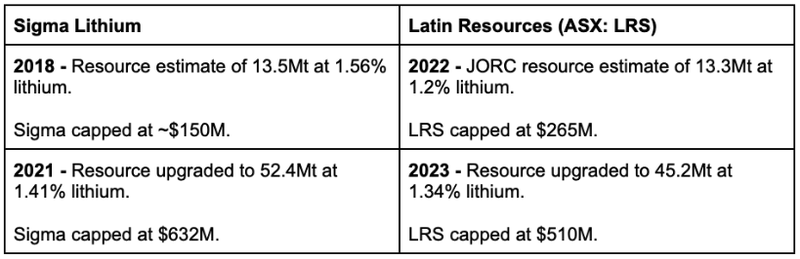

LRS resource has grown by 241% from the previous estimate, and it now sits at 45.2Mt with a lithium grade of 1.34%.

This resource is comparable to some of the biggest billion dollar plus Australian lithium producers.

But most importantly it’s another step towards LRS becoming “Sigma 2.0”.

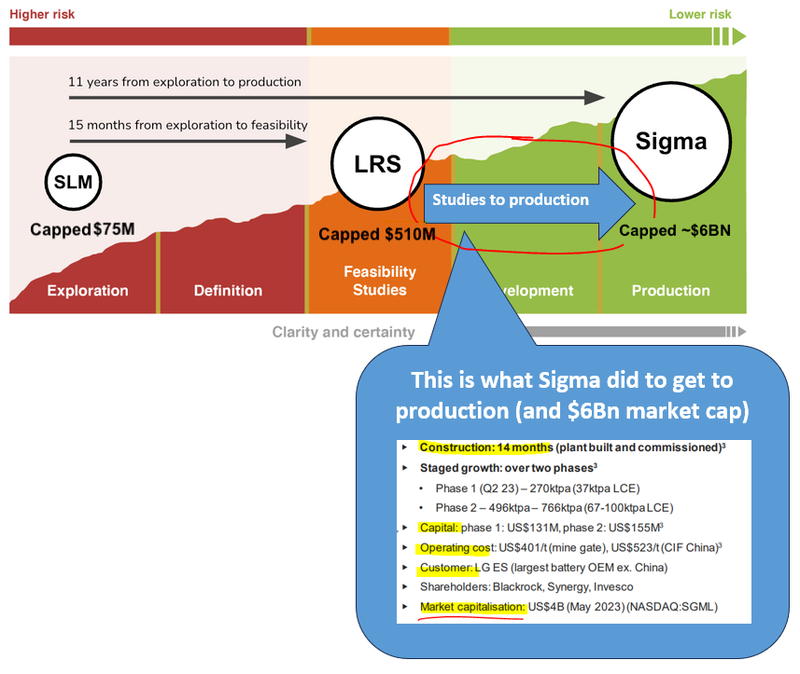

$6BN Sigma became Brazil’s first lithium producer in April and is the playbook that LRS is following.

The best thing is, LRS’s lithium resource is still growing.

With $50.1M in the bank (as of 28 April), LRS is running 8 drill rigs on site, and is in the midst of a 65,000m drilling campaign in order to grow the resource even bigger.

LRS’s lithium deposit remains open at depth, and along strike to the southwest, where LRS is running step out drilling.

LRS is getting more and more confident that one large, continuous, mineralised lithium system exists in the immediate project area.

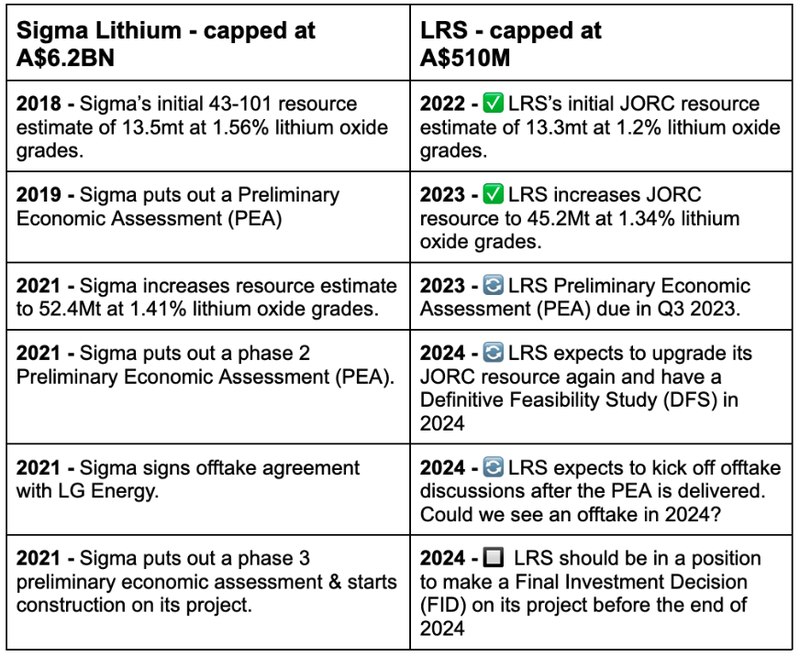

LRS is following the playbook of the first Brazilian lithium producer: Sigma Lithium.

LRS’s project is north of Sigma’s, in the same state of Minas Gerais.

Sigma Lithium is listed in both Canada and on the NASDAQ and is currently capped at US$4BN (~$6.2BN AUD).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

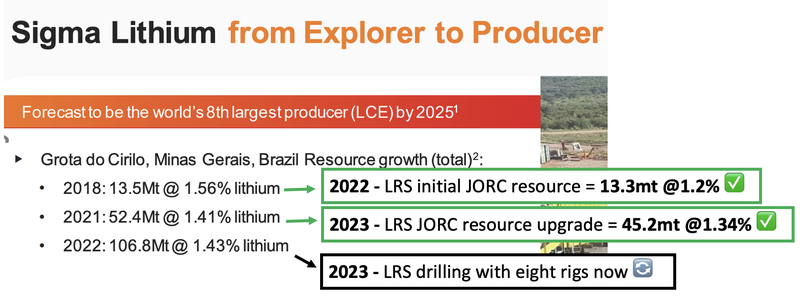

Sigma became Brazil’s first lithium producer in April and is forecast to be the eighth largest lithium producer on the planet by 2025.

LRS is capped at $510M - and is following the exact same path that Sigma tread in achieving its ~$6BN dollar valuation.

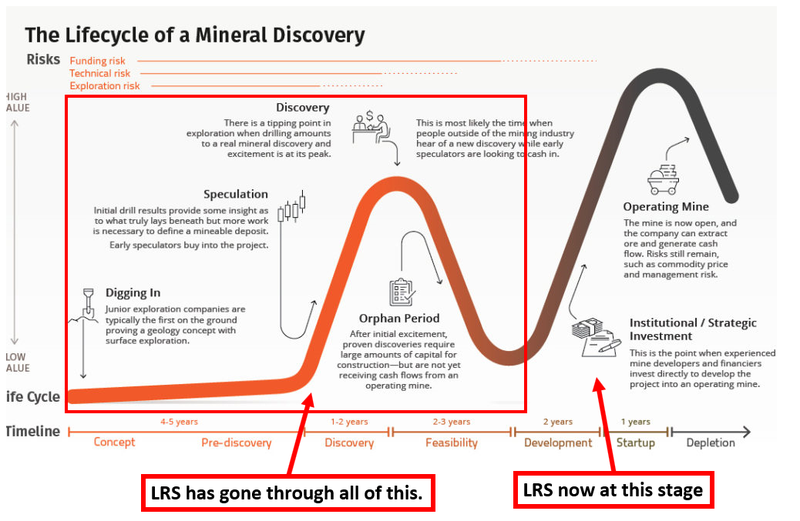

Sigma took just 14 months to build and commission its plant, and has steadily grown in market cap as it progressed through the mining company lifecycle (see image below).

With an upgraded 45.2Mt JORC resource now announced (roughly inline with Sigma’s original upgrade), we want to see LRS continue follow Sigma’s footsteps in Brazil through development and to production - and with that, we hope a comparable valuation:

Of course, success is not a guarantee here, there is a significant amount of development risk in pre production / pre revenue companies, and the success of one company does not mean success will follow in another.

LRS is being touted as “Sigma 2.0”.

LRS’s project is north of Sigma’s newly producing lithium mine in the state of Minas Gerais.

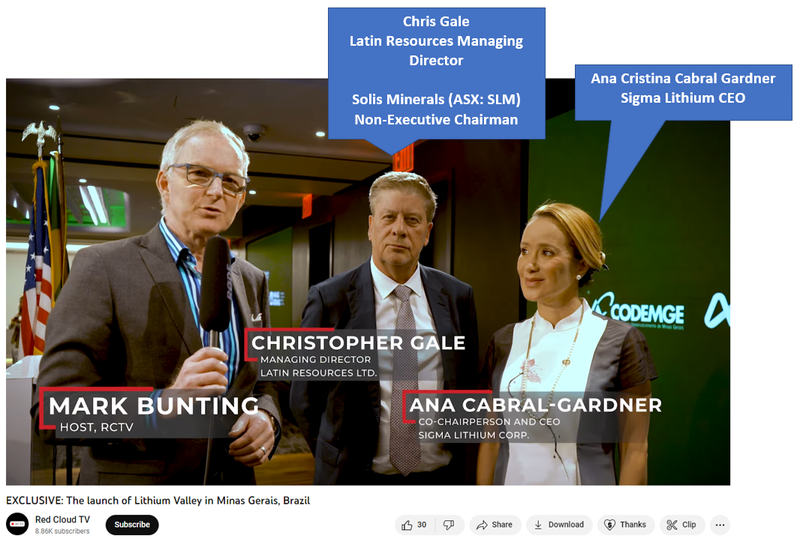

The multi-billion dollar NASDAQ listed Sigma is very supportive of LRS being called “Sigma 2.0” and achieving the same success.

In the below interview with LRS, Sigma CEO Ana Cabral-Gardner said “it’s an honour... for LRS to be called Sigma 2.0” and “you ought to collaborate”:

Watch the full Sigma and LRS interview here

You can also watch MD Chris Gale run through a Latin Resource investor presentation yesterday here.

Yesterday’s 241% JORC resource increase from LRS is almost exactly the same upgrade Sigma did back in 2021.

LRS’s resource now sits at 45.2Mt with a lithium grade of 1.34%.

LRS now has a “lithium mine scale” resource - and its is still growing

Importantly, LRS made very clear mention of yesterday’s resource upgrade not being the last.

Just like Sigma did in 2022, LRS plans to upgrade its resource again with eight drill rigs actively drilling right now.

On its own though, the 45.2Mt resource is big enough to form the base for a lithium mine, with some of the mines being developed across WA having smaller resources than LRS.

For example, Core Lithium, which is capped at $1.85BN, has a 30.6Mt resource with lithium grades of 1.31% - both lower grade than LRS and smaller in terms of size/scale.

So, LRS has a bigger lithium resource than Core Lithium, but is valued at less than half of Core Lithium - noting that Core is more advanced, having just shipped its first batch of spodumene concentrate.

Interestingly, Brazil has looked to WA to follow the same playbook in building a lithium industry - you can watch LRS Managing Director Chris Gale at NASDAQ discussing this in detail here, along with the Sigma playbook LRS is following:

OK so it's big already - but what’s next for LRS?

Today LRS is capped at $510M and is working toward multiple major catalysts within the next 6 months:

- Preliminary Economic Assessment (PEA) next quarter - The PEA will finally show the market what sort of economics and financials LRS’ project can deliver.

- Eight rigs drilling right now - LRS expects to upgrade its JORC resource again over the next 12 months.

- Offtake discussions to start right after the PEA - LRS expects to start shopping around an offtake deal for its lithium production after the PEA is released, which will help attract financing for construction of a mine.

Beyond that busy 6 months, the big milestones over the coming years will be a Final Investment Decision in 2024, construction in 2025, and production by 2026.

How did LRS get here?

LRS has been operating in Latin America for a decade, and was previously a diversified explorer with a number of exploration projects targeting a range of metals.

At one point in the depths of the COVID crash, LRS was a micro cap explorer capped at less than $10M - well done to all LRS investors that have held since then.

It feels like a long time ago now.

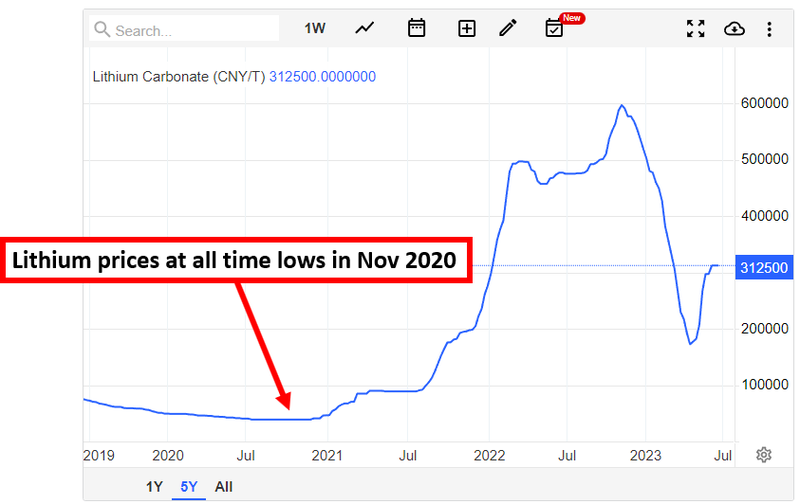

We first announced our LRS Investment in November 2020 at an Initial Entry Price of 1.8c.

At the time the lithium industry was on its knees with a soft lithium price, and LRS had temporarily pivoted away from focusing on its lithium projects.

For the first few months of our Investment, we were really most interested in LRS’ kaolin/halloysite project in WA as the main value driver.

In the background though, LRS Managing Director Chris Gale had kept his team of South American geologists in Brazil, looking for ground that had the potential for a hard rock lithium discovery with size/scale potential.

This was in the hope that the lithium price would return, and so that LRS could be ready when it eventually did.

Up until that point the Brazilian lithium space was relatively foreign to investors, there was no real major player outside of a small company called “Sigma Lithium”.

Sigma had come onto the TSX (the Canadian Stock Exchange) in 2017 through a Reverse Takeover (RTO).

🎓 RTO’s are when projects get vended into “shells”, read more - what is an ASX shell?

Sigma, at the time, had a pre-resource lithium project in the State of Minas Gerais in Brazil.

In June 2018 Sigma had a market cap of ~CAD$134M (at CAD$2 per share).

Initially Sigma did ~9,000m of drilling and put out an initial foreign 43-101 resource estimate.

In 2018 Sigma put out its initial JORC resource estimate of 13Mt with a lithium oxide grade of 1.56%, and the company was still capped at under $200M.

Around that period, Chris Gale, LRS’s Managing Director started searching around Brazil looking for projects that had the same potential as Sigma Lithium’s.

Over the next four years, through the entire lithium bear market of 2018-2020, Sigma kept drilling its project.

At the same time, LRS kept picking up new ground, doing due diligence on new opportunities and curated a portfolio of projects it thought had the potential to emulate Sigma’s success...

Everything sounds relatively logical so far BUT let's not forget that LRS was doing this in a lithium bear market.

In 2018 through to the first half of 2020, the majority of small cap companies had moved on from looking for lithium projects, the whole sector was out of favour, the major producers were going bust, and investors didn't want to fund new project development opportunities.

LRS stuck to its guns and built a portfolio of prospective (but untested) ground immediately to the north of Sigma.

We covered all of the work LRS on its now half a billion dollar lithium resource long before it made the discovery:

- March 2021 - LRS Set to Drill Lithium Assets in South America

- August 2021 - Latin Resources eyes lithium potential at Salinas Project

- Sep 2021 - LRS strengthens lithium story with commitment to ESG

- Oct 2021 - Great Time to Look for Lithium - LRS Building Lithium Footprint in Brazil

- Feb 2022 - Spodumene alert: Has LRS just made a new lithium discovery?

- March 2022 - LRS Keeps Showing Us More Spodumene

- [Discovery] March 2022 - Large fresh green crystals everywhere - is this a new lithium discovery?

Three years after first picking up ground in Brazil, in late March 2022, LRS drilled its first drillhole at the project and made its hard rock lithium discovery.

This was when the comparisons to Sigma started to gain traction in the market and LRS validated its name as Sigma 2.0, and next in line for becoming a Brazilian lithium producer.

Since the discovery, LRS has been moving quickly to define its lithium resource and move towards feasibility studies.

Wasting no time, in just 18 months LRS has managed to:

✅ Deliver a maiden resource estimate of 13.3Mt at 1.2% lithium oxide grades

✅ Complete over 50,000m of drilling

✅ Upgrade its resource (241% higher than the first) - 45.2Mt at 1.34% lithium oxide grades

✅ Raised a total of ~$72.1M in capital to develop its project ($35M at 16c + $37.1M at 10.5c)

LRS has followed the Sigma playbook almost to a tee...

In April this year, Sigma produced its first spodumene concentrate (lithium product), and the company’s market cap reached a peak of ~A$6.5BN.

It took Sigma ~5-6 years to go from <A$200M market cap junior to the multi-billion dollar lithium industry leader it is now in Brazil - keeping in mind ~2-3 of those years were during a bear market for lithium companies.

LRS is now ~18 months on from its discovery and has already made up ground FAST.

LRS’s market cap has gone from ~$43M pre-discovery to now sit at $510M after yesterday’s resource upgrade.

We think that given some time and a few more major milestones ticked off (offtake/preliminary economic assessment studies and a DFS), LRS can continue to get bigger and really grow into its “Sigma 2.0” nickname.

The Sigma story forms the basis for our LRS Big Bet which is as follows:

Our LRS Big Bet:

“LRS increases the scale of its lithium discovery to the level of its multi billion dollar regional peer - Sigma Lithium. With this we would expect the market to value LRS similarly.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LRS Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor LRS’s progress since we first Invested and track how the company is performing relative to our “Big Bet”, we maintain the following LRS “Progress Tracker”:

More on LRS’s resource upgrade

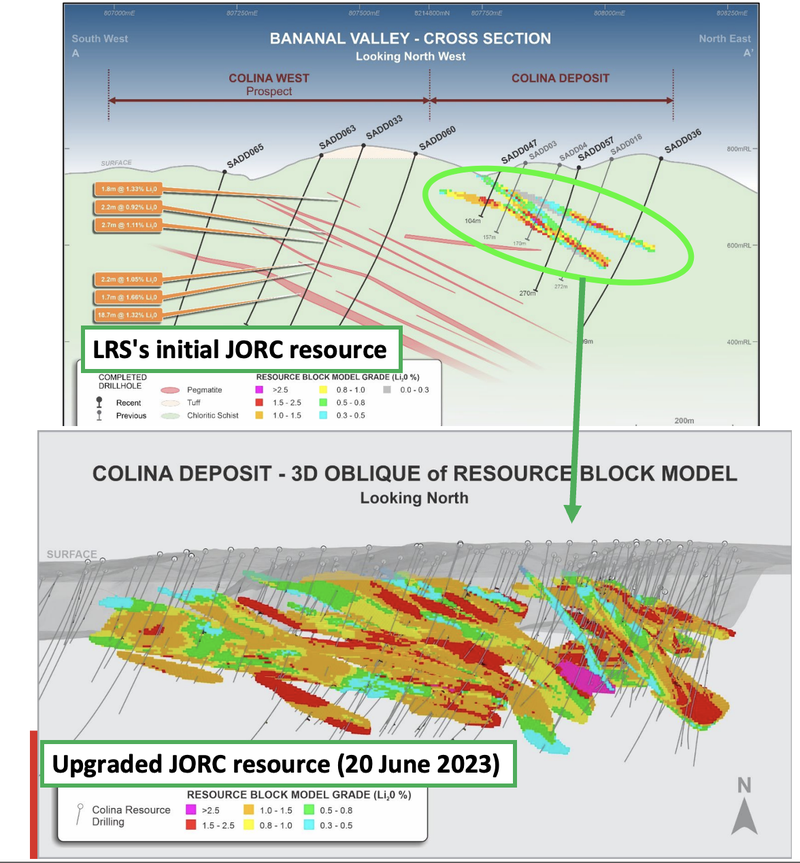

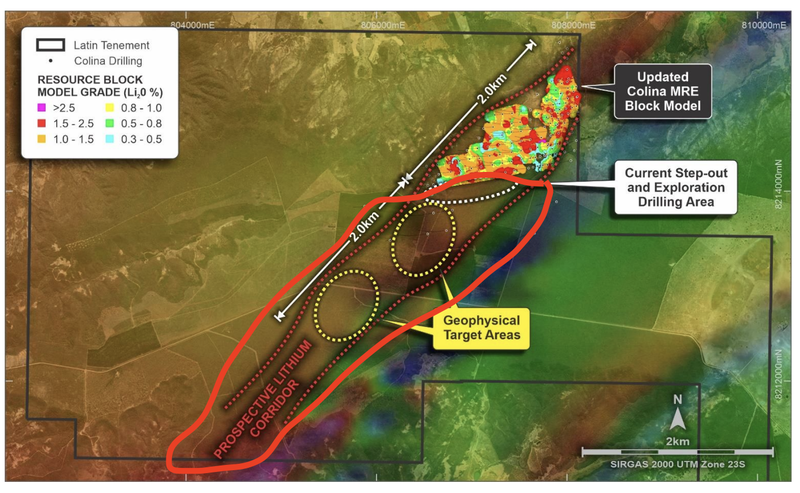

Broadly, LRS’s latest resource upgrade came from drilling to the southwest of its existing JORC resource.

Here is a before and after look at the resource:

The focus for LRS will now be on growing the resource by drilling at depth and along strike to the southwest.

The image below shows just how much of the prospective area to the south west there is still to drill out.

Ultimately LRS has enough exploration potential for it to prove an even larger lithium resource.

If LRS can drill out a resource that even remotely resembles Sigma’s 106.8Mt, then we think LRS’s project will start to get a lot more market interest.

Our LRS Investment Strategy

In line with our Investment Strategy, we have taken some chips off the table over the duration of our Investment, given the continued positive re-rates of LRS across recent years but hold a material position as LRS progresses through the later stages of the mining life cycle.

Our general strategy is to sell 20% of our holdings in a company if the company re-rates on material news.

In the case of LRS, the company has re-rated over 1,000% and delivered on multiple company-making results:

- The initial lithium discovery hole

- Fully funded capital raise of $35M

- The initial JORC resource which nearly hit our Bull Case scenario

- Fully funded capital raise of $37M

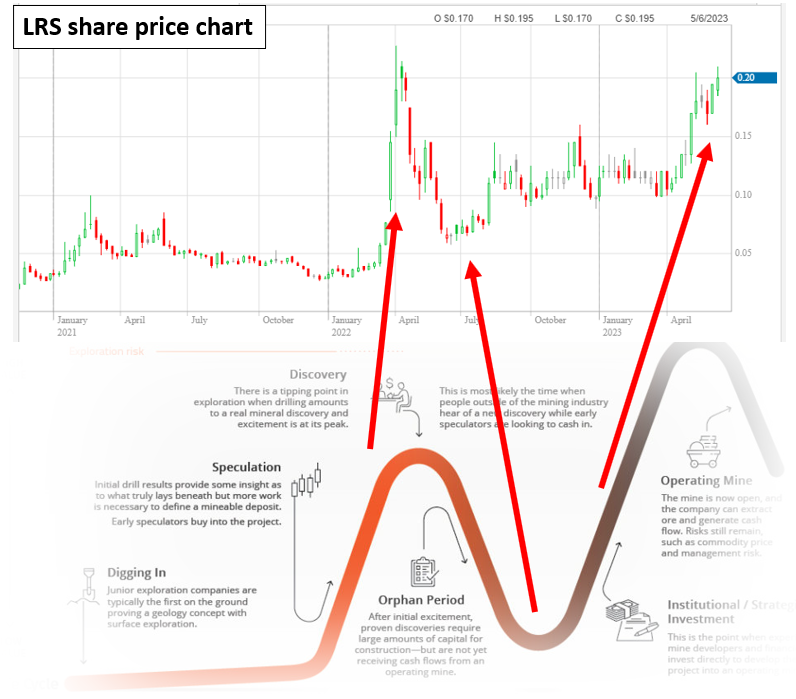

Our Initial Entry Price in LRS was 1.8c. The current LRS share price is 20c, at its current $510M market cap.

We increased our position again at 4.5c and again at 3c.

Today LRS is backed by big institutions that want to make multiples on the current LRS share price, and are investing for LRS to get into production and start delivering cash flow.

We hold 3,585,000 shares in the company and look forward to seeing what the company can deliver over the next few years.

In the early stages, junior exploration Investing is high risk / high reward, and things can change very quickly for a company.

Our investment strategy is to Invest in a number of high-risk high-reward stocks, with the outsized returns of a few, to make up for the potential losses in the rest of the Portfolio.

For us, LRS is one of those 10-bagger Investments that sustains our investment strategy, and each year we hope that at least one Investment in our Portfolio 10-bags.

We have found that early stage exploration stocks this is the Investment approach that works best for us:

- Invest early, before major exploration catalysts - like we had done in LRS back in November 2020 at 1.8c per share.

- Be ready for exploration failure and either continue to back the company or cut the Investment - LRS drilled a few projects before eventually making its lithium discovery. We continued to back the company with additional Investments at 4.5c and 3c.

- Top Slice the Investment when the company delivers something material - this part is usually the hardest because we are forced to sell when the “blue sky” discovery potential is being talked about, but it is important for us to free up capital for new investment opportunities.

- Be ready for volatility as the company defines the size/scale of its discovery - Typically the market starts to get bored of the story here, and the share price can often come down significantly. Need to be ready for this to happen.

- Always hold a material position in the stock even after the company has successfully executed the “Big Bet” - LRS successfully re-rated 10x on our standard Big Bet for early stage exploration stocks. We hold on to a position to be leveraged if LRS goes on and completes the next phase of development (and our next Big Bet) to see the company move into feasibility studies and justify lithium production.

A famous fund manager once said that “the final doubling in the share price is the most important and impactful. It’s important to have a material position in place if that happens”.

We are hoping LRS can continue to deliver in as it moves through the next two stages of the mining life cycle into production.

These patterns we described in the above points (1) to (6) can be summarised in the Lassonde curve:

What’s next for LRS?

Over the next six months, we are watching for the following three main catalysts:

Preliminary Economic Assessment (PEA) 🔄

The next major catalyst for LRS will be its Preliminary Economic Assessment (PEA).

This will set out a first pass set of financial metrics for LRS’s project and give investors an idea of the potential value of LRS’s resources.

LRS expects this to be ready for release to the market in Q3 2023.

Metallurgical testwork and pilot plant operations 🔄

Ultimately the network/pilot plant results will form the basis for the Preliminary Economic Assesement (PEA) that LRS’s releases.

The stronger the recoveries from the testwork, the stronger the financials of the project are likely to be.

See our deep dive on the preliminary metwork results here: Metallurgical testing looking strong

More drilling results 🔄

LRS still has eight drill rigs active on site.

Most of the drilling is to the southwest of its current JORC resource where the company has over ~4km of strike to test.

We will be monitoring the drill results that are released.

Ideally, we will see more lithium being intercepted to the southwest and at depth which could ultimately lead to another resource upgrade.

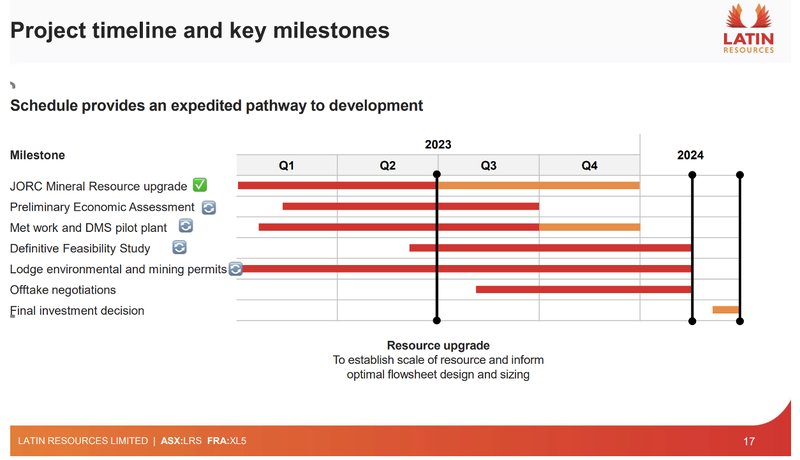

Here’s the detailed project timeline, in the lead up to a Final Investment Decision in 2024:

Our LRS Investment Memo:

Click here for our LRS Investment Memo, where you can find the following:

- Key objectives we want to see LRS achieve

- Why we are Invested in LRS

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.