LRS Delivers Maiden JORC Resource - Following $5.5BN Regional Peer’s Playbook

Published 08-DEC-2022 10:00 A.M.

|

12 minute read

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 4,605,000 LRS shares at the time of publishing this article. The Company has been engaged by LRS to share our commentary on the progress of our Investment in LRS over time.

From lithium discovery to maiden JORC resource estimate in under nine months.

Our Catalyst Hunter Portfolio’s lithium Investment Latin Resources (ASX: LRS) is no longer a junior explorer chasing a new discovery — it now has a sizable established in-ground JORC lithium resource.

Today LRS announced a maiden JORC resource estimate of 13.3Mt grading 1.2% lithium oxide for its Colina lithium deposit in Brazil.

Of that 13.3Mt resource, 2.1Mt sits in the indicated category and the remainder in the inferred category.

This came as a welcome surprise as very rarely do you see a maiden resource feature the more confident indicated estimate.

LRS’s independent resource consultants also gave an Exploration Target of 13.5-22 Mt with a grade range of 1.2-1.5% from inside the area where today's JORC resource sits.

Interpretations are that modelled pegmatites increase in both thickness and grade at depth.

LRS’s regional peer in Brazil, Canadian-listed Sigma Lithium, makes for a good comparison to see what might now be in store for LRS.

Sigma defined a maiden resource estimate back in 2018 of 13Mt with a lithium oxide grade of 1.56% — very similar to LRS’s maiden resource announced today of 13.3Mt grading 1.2%.

At that time Sigma’s market cap was at a level that’s very similar to that of LRS today.

Almost five years on and Sigma is now up ~3,500%, trading with a market cap of C$5BN (~A$5.5BN).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Just like Sigma in 2018, we think today is just the beginning for LRS.

LRS has an exploration target of up to 22 Mt at its existing resource, plus whole new discoveries that it plans to drill out in 2022 with an eight rig, 65,000m drilling program.

Brazilian neighbour Sigma is expected to be producing by April 2023 which will bode well for LRS who has a Preliminary Economic Assessment due at around the same time.

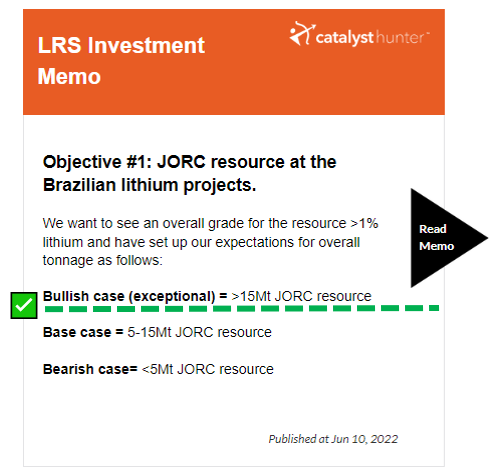

Today’s maiden resource estimate came in at almost our bullish case, ranking as an ‘upper base case’ in terms of our expectations we set out for LRS back in June.

As we indicated above, there are plenty more drill holes to come over 2023, and a number of targets, so we expect this resource to grow over time in the same way Sigma’s resource grew over time.

Today's news was the major catalyst we have been waiting for as it allows for the comparison of LRS against other lithium players with established resource numbers.

Here’s the key takeaways of where LRS is at in terms of the size of its lithium resource:

- An analogous maiden resource estimate - LRS’s initial resource sits at 13 Mt with lithium grades of 1.2%. Sigma’s was the same tonnage but had a slightly higher grade.

- 13.5 Mt to 22 Mt exploration target - LRS can increase the size of its existing resource by drilling out this exploration target to define a resource of up to 13.5-22 Mt.

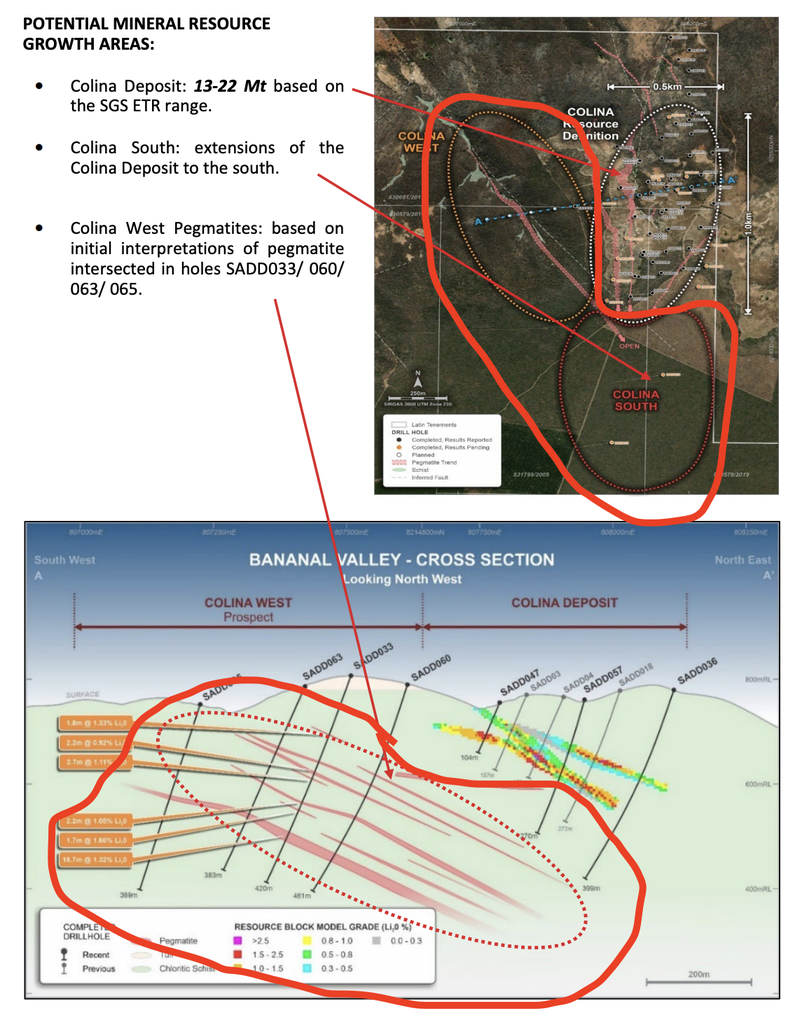

- Additional discoveries OUTSIDE of current resource - LRS’s Colina West discovery is located just ~500m west of its new Colina resource. This area of the project is OUTSIDE of, and in addition to, the current resource and the exploration target.

- 65,000m of drilling with eight different rigs planned - LRS isn't slowing down and intends to drill aggressively in 2023 to bring forward a mineral resource update by Q3-2023.

The image below shows just how big LRS’s project is and highlights the untested areas to the west and south (Colina West and Colina South) of its current JORC resource.

This brings us to our “Big Bet” for LRS:

Our ‘Big Bet’

“LRS increases the scale of its lithium discovery to the level of its multi billion dollar regional peer - Sigma Lithium. With this we would expect the market to value LRS similarly.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LRS Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor LRS’s progress since we first Invested and track how the company is performing relative to our “Big Bet”, we maintain the following LRS “Progress Tracker”:

See our LRS Progress Tracker here:

More on the Sigma & LRS comparison

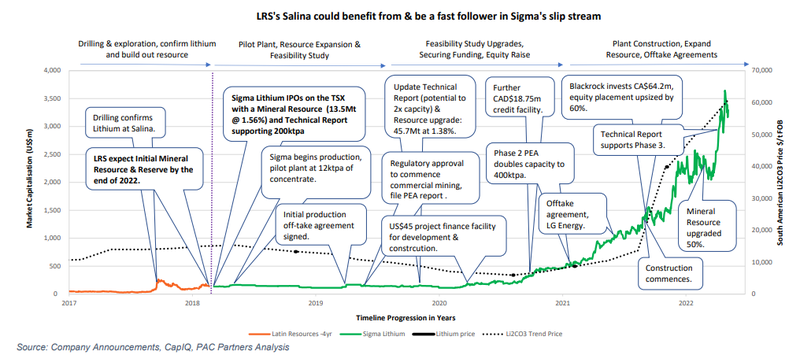

LRS’s JORC resource estimate has been almost perfectly timed.

Not only has the lithium price hit new record highs this month, but this week Sigma announced a 63% increase to its resource estimate, lifting the project’s net present value (NPV) to US$15BN.

Sigma’s resource now sits at ~85.6 Mt with a lithium oxide grade of 1.43%.

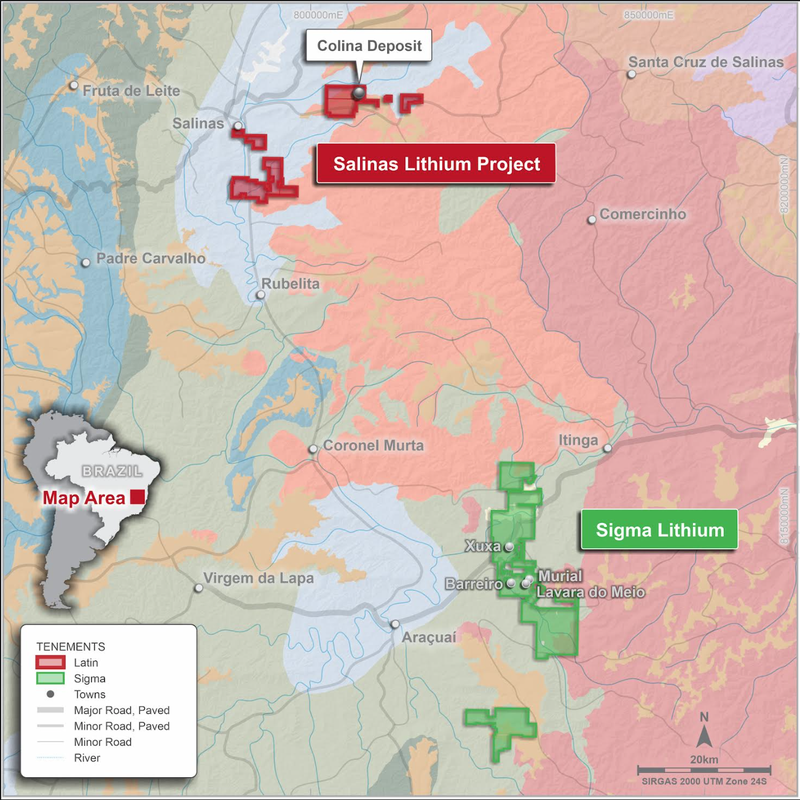

Here is LRS’s projects relative to Sigma’s:

Similar to LRS, Sigma’s project started from a much lower base with its first ever mineral resource estimate being an almost identical 13 Mt.

In the five years since Sigma announced its initial resource estimate — when it was trading at a similar market cap to LRS’s now — the company has made new discoveries and drilled out extensions to known discoveries.

This saw Sigma increase its resource, first to ~21 Mt, then 47 Mt and again to ~85.6 Mt this week.

While at an earlier stage, LRS is following in Sigma’s footsteps, today announcing its maiden JORC resource estimate of 13.3 Mt with a grade of 1.2% lithium.

One difference is that LRS has already made a NEW discovery, at Colina West which is only ~500m west of its current JORC resource at Colina.

This addition alone has potential to significantly grow LRS’s resource number.

LRS has a 65,000m drilling program planned for 2023 with eight drill rigs and intends to upgrade its JORC resource by the third quarter of 2023.

LRS is also working on a Preliminary Economic Assessment and is targeting completion of a DFS by the end of 2023.

LRS had $19M in cash at the end of the September quarter, which gives it plenty of runway to continue to grow the resource base and advance its economic studies.

LRS’s grand plan is similar to Sigma’s pathway to success, who over the almost five years since its maiden resource, completed multiple technical and feasibility studies laying out the overall economics of its lithium project.

LRS is also engaging all the same consultants that Sigma used to bring its mine into production - which will no doubt accelerate the permitting processes.

Starting in January 2018 when Sigma put out its first resource estimate, its share price has risen from ~C$1.50 to a peak of C$54.23 per share — a ~3,500% return.

This is the sort of upside we hope LRS can capture from where it is today — even before reaching the production stage.

Below is an image showing what happened to Sigma (in green) after its maiden resource estimate, and how LRS is tracking in comparison (in orange).

Sigma is only now putting its project into production and expects it to be fully operational by April 2023.

We believe this to be a case of what is good for Sigma is good for LRS.

As a major player in the hard rock lithium space, Sigma will put Brazil on the global map when it comes to lithium production.

This should bring increased investor interest to other hard rock players in Brazil.

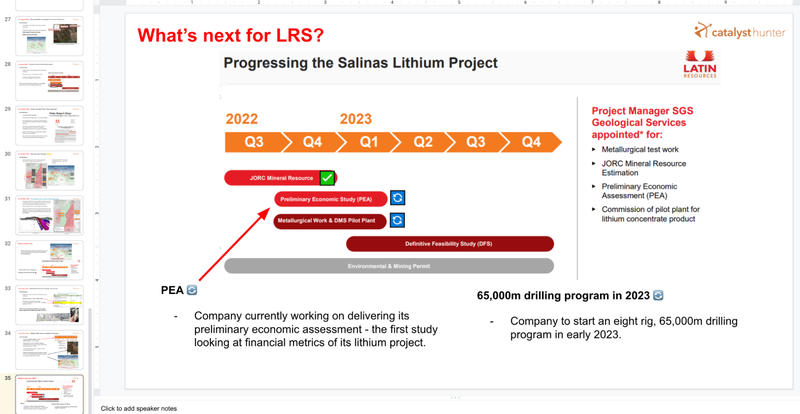

Metallurgical testing looking strong

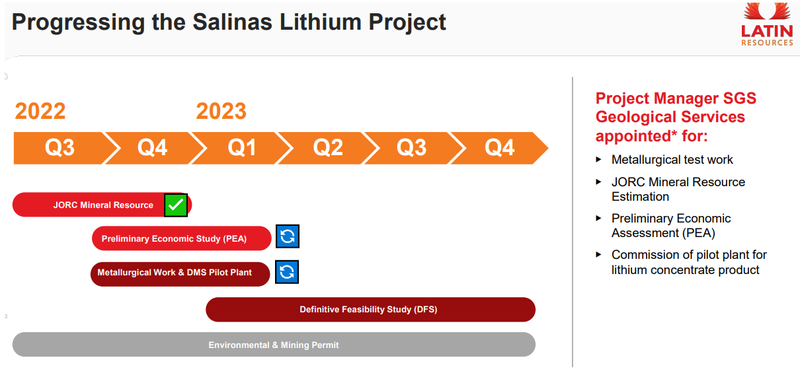

In today’s announcement, LRS said its Preliminary Economic Assessment (PEA) is well underway, and it is targeting a Definitive Feasibility Study (DFS) by the end of 2023.

Today’s resource provides a base to start modelling the financials of its discovery, while LRS has been undertaking metallurgical test work in the background that provides further key information.

Having a resource is a major step forward, but it’s the metallurgical testing that can be the dealbreaker for new commodity discoveries.

Without an effective processing solution projects can be deemed uneconomic. Conversely, finding an efficient, low cost highly scalable solution should improve a project’s economics as compared to similar resource sizes that lack a processing solution.

LRS put out an update on this front just two days ago.

Our key takeaway was that it can produce high grade lithium concentrates using a simple Heavy Liquid Separation (HLS) processing method, resulting in high recovery rates and high grade concentrates:

High recovery rates

The HLS processing resulted in high recovery rates of ~80.5% lithium oxide using a simple processing setup with a low level reliance on flotation.

Importantly, this simple processing method should translate to lower operating costs when it comes time to mine and produce lithium from LRS’s project.

Further, LRS achieved these recovery rates with a low level reliance on flotation, which is usually necessary to achieve a high lithium recovery rate.

The benefit is that any future plant design could have a much smaller flotation circuit footprint, requiring lower upfront costs relative to other lithium projects.

We expect all of this to have a positive impact on the overall project economics.

High grade concentrates

LRS produced lithium oxide concentrates grading as high as 7.96%, with average grades across the testwork program of ~6.3%.

For a gauge on what that means, LRS’s results are only slightly lower than the theoretical maximum pure spodumene grade of ~8.03%.

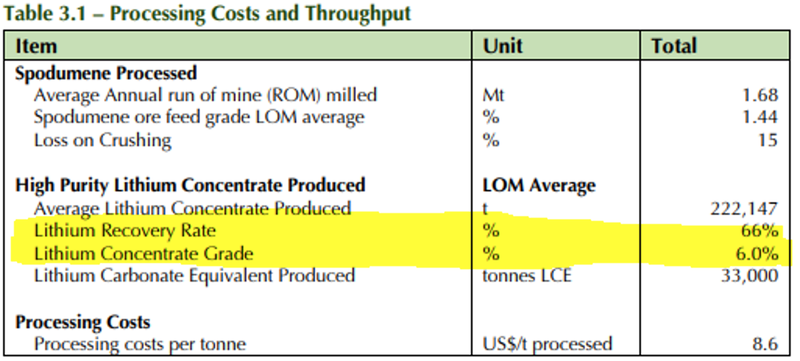

We also like that preliminary results of LRS’s processing solution stack up strongly versus its Brazilian neighbour, Sigma Lithium.

Sigma’s preliminary metwork results, announced back in 2021, showed recovery rates ranging from 66-70% with spodumene concentrates grading ~6%.

Again, LRS has recovery rates of ~80.5% and it is producing spodumene concentrate grades averaging 6.3%.

Sigma has since proven up an economic resource and is now heading into production. This certainly bodes well for LRS when considering it’s production economics and processing flowsheet since it’s metwork results are on par with Sigma’s.

Here are Sigma’s processing costs and lithium recovery rates from its Preliminary Economic Assessment (PEA) in June 2021:

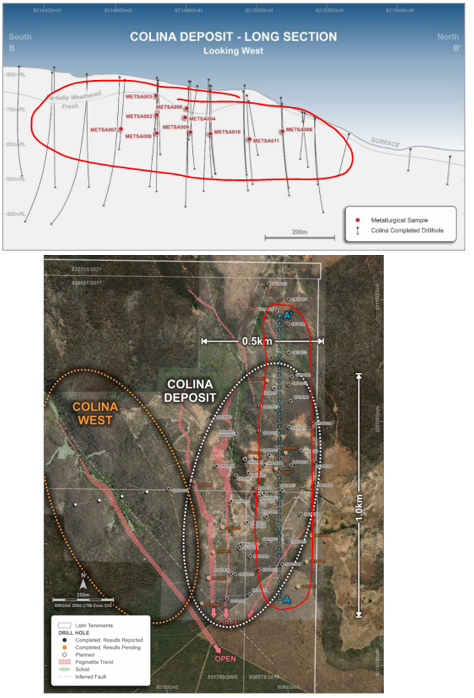

We also note that LRS’s metwork results also display consistent performance right across the resource area.

The processing results came from a batch of 10 samples taken across LRS’s project in a north-south direction covering ~500m of mineralisation.

These images show where the 10 samples were taken from:

The notable caveat here is that the testwork has only been done at lab scale — there is no guarantee that the results will carry over to a processing plant at size/scale of the project.

However, LRS can now apply its metwork results to its JORC resource to model out its Preliminary Economic Assessment study (PEA).

Strong cash balance to fund studies and more drilling

In addition to the maiden JORC resource estimate, today LRS announced some major work its going to deliver over the course of 2023:

- ~65,000m drilling program with eight rigs on site

- Preliminary Economic Assessment by Q1-2023

- Updated resource estimate by Q3-2023

- Definitive Feasibility Study by the end of the year

All of this will require capital, especially considering how large that drilling program will be.

To this end, LRS ended the September quarter with ~$29M in the bank and still has ~$3.42M in options in the money that could be converted.

This should be more than enough cash to see LRS through the next few quarters.

But on the back of today’s news and with the company committing to a big 2023, we think that if LRS’s share price was to re-rate significantly higher (i.e multiples of the current share price) over the coming months, it may be prudent to raise more funds.

This has become somewhat of a theme in the lithium space, where other much larger capped companies are choosing to top up the bank account following strong share price performance.

Recent raises in the lithium space on the ASX:

- Global Lithium (capped at $584M) raised $100M, adding to its already chunky $28M cash pile (at 30 September).

- We also saw Red Dirt Metals (capped at $170M) take advantage of a recent spike in its share price to raise $55M last week.

As long term investors, we’d much prefer for LRS to raise capital to finance the progression of its projects when its share price is high than wait until its cash balance is low and it is under pressure to raise.

We want to see LRS monitor its share price as well as institutional interest in the lithium space and to take advantage of any major share price re-rate to get more funds through the door.

LRS attracts analyst coverage

Now that LRS’s market cap is well over the $100M mark, currently edging $300M, the company is increasingly being considered “investable” by larger institutional investors.

Our approach to micro cap Investing involves following the journey of what are often sub-$20M capped companies as they re-rate first into $100s of millions and then into billion dollar companies.

As our Portfolio companies grow in size and value, we expect cash to begin flowing in from larger institutional investors.

We wrote about our reasons why and what fund managers look for in a previous weekend email, which you can view here: How do Fund Managers Invest in Small Cap Stocks?

LRS has already attracted cornerstone investment from experienced lithium investors, Canada-based Waratah Capital’s “Electrification and Decarbonization Fund”, which took $15M of the $35M raise completed earlier in the year at 16c per share.

Waratah Capital manages over C$3 billion in assets and is also behind “Lithium Royalty Corp”, which holds royalty investments in lithium explorers including Core Lithium, Sayona Mining and, interestingly, LRS’s Brazilian neighbour Sigma Lithium.

And now, the following brokers have initiated coverage on LRS. You can access the PAC Partners and Bell Potter reports via the links below:

- Canaccord Genuity: price target for LRS of 25c.

- PAC Partners research report: price target for LRS of 24c.

- Bell Potter research report: price target for LRS of 18c.

LRS was trading at 14.5c at last close, so the analysts are predicting some upside ahead.

However we note that analyst reports and price targets are based on a number of assumptions that may not eventuate. Never invest in a company based on an analyst price target alone, do you own research and seek your own professional advice before investing.

What’s next for LRS?

Preliminary Economic Assessment (PEA) 🔄

The next major catalyst for LRS will be its PEA.

This will set out a first pass set of financial metrics for LRS’s project and give Investors an idea of the value LRS’s resource may have.

LRS expects this to be ready for release to the market by Q1-2023.

Our 2022 LRS Investment Memo

Click here for our LRS Investment Memo, where you can find the following:

- Key objectives we want to see LRS achieve

- Why we are Invested in LRS

- What the key risks to our Investment thesis are

- Our Investment plan

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 4,605,000 LRS shares at the time of publishing this article. The Company has been engaged by LRS to share our commentary on the progress of our Investment in LRS over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.