LRS now drilling west of its lithium JORC resource

Published 24-JAN-2023 10:23 A.M.

|

8 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,605,000 LRS shares at the time of publishing this article. The Company has been engaged by LRS to share our commentary on the progress of our Investment in LRS over time.

“On par” or “better than” the main deposit...

That’s what Latin Resources’ (ASX: LRS) geology manager said about LRS’s latest batch of drilling that's OUTSIDE OF the existing JORC lithium resource defined last year.

New intercepts are up to ~20.17m thick with lithium grades of up to 1.96% — well above our bull case expectation and the 1% lithium grade that is typically considered economically viable.

With drill hits like those released today, we can understand why the LRS geo is saying that the new Colina West discovery could be just as good or better than the original Colina discovery.

For some context, LRS’s first discovery hole at Colina measured 4.31m with lithium grades of 2.22% - starting the ~500% increase in LRS’s share price in March 2022.

Meanwhile the first discovery hole at Colina West was 18.71m with lithium grades of 1.32%.

It's now less than eight weeks since LRS released the maiden JORC resource estimate and LRS hasn't really stopped, its back out in the field drilling again and putting out more assay results.

LRS maiden JORC resource was for 13.3mt with a lithium grade of 1.2% and an exploration target of 22mt at Colina.

These numbers do not include the Colina West area and the assay results released today.

LRS now has eight diamond drill rigs on site, for a planned 65,000m, yes that’s 65km of diamond drilling.

It’s ‘Colina West’ that LRS is furiously drilling into right now - and so far it's delivering the goods, judging by today’s assay results.

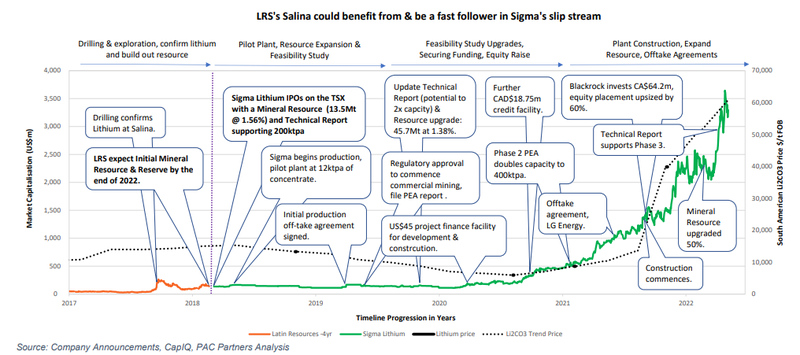

LRS already has the playbook for multi-billion dollar success in this part of Brazil for lithium - the $263M capped LRS is looking to emulate the success of its $4.7BN regional peer Sigma Lithium to the south.

Whilst LRS achieving the same on market success is no guarantee - the future lithium price is going to have a big influence in this, amongst a myriad of other factors outside of LRS’s control, it's worth looking at what Sigma has been able to achieve.

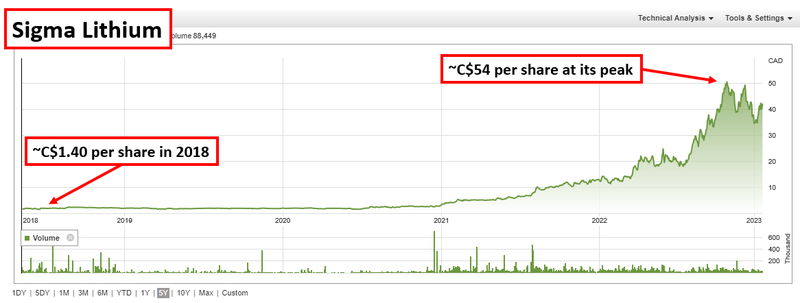

Sigma’s journey started in 2018 when the company first put out a resource estimate of ~13mt with lithium oxide grades of 1.56% - almost identical to LRS’s maiden JORC resource of 13.3mt at 1.2%.

Today, Sigma’s total mineral resource sits at ~85.6mt with lithium grades of ~1.43% across multiple discoveries.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

After several rounds of drilling, new discoveries and several resource upgrades, Sigma’s project now has a US$15.3BN net present value (NPV) and is only months away from first production.

Back in 2018, Sigma’s market cap was at a level that was very similar to that of LRS.

Almost five years on and Sigma is now up ~2,800%, trading with a market cap of ~A$4.7BN.

LRS is confident it will put out multiple resource upgrades over 2023 - aiming to drill out Colina West first and then hopefully make new discoveries.

LRS put out its maiden JORC resource estimate in December last year and immediately laid out its plan to follow Sigma’s playbook for going from micro cap explorer to (hopefully) multi billion $ lithium major.

LRS’s plan for the coming months is:

- ✅ Establish a maiden JORC resource - LRS completed this in December, delivering a similar maiden JORC resource estimate to Sigma’s first resource back in 2018.

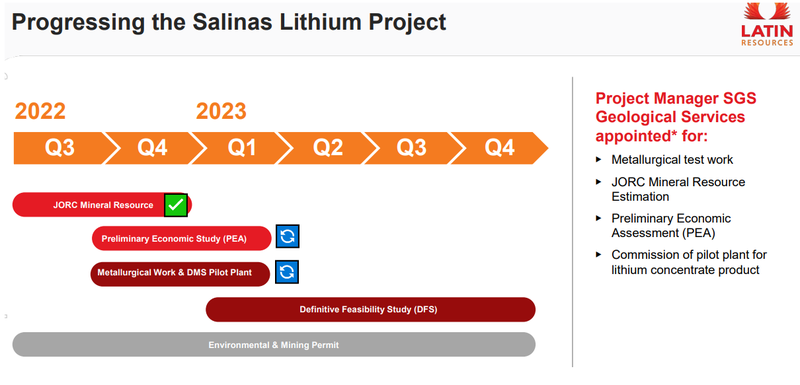

- 🔄 Complete a preliminary feasibility study - LRS is currently working on this and expects it to be completed by the end of Q1 2023. This should put some financial ‘colour’ around its current JORC resource and give us our first look at how profitable a potential mine could be.

- 🔄 Drilling to increase the size and scale of its project - LRS kicked off a 65,000m drill program with EIGHT diamond drill rigs only last week.

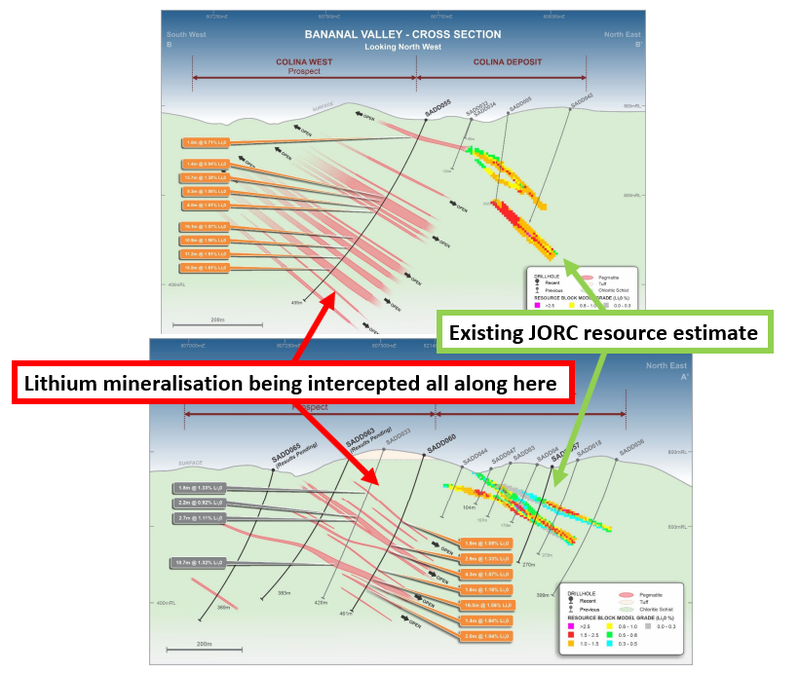

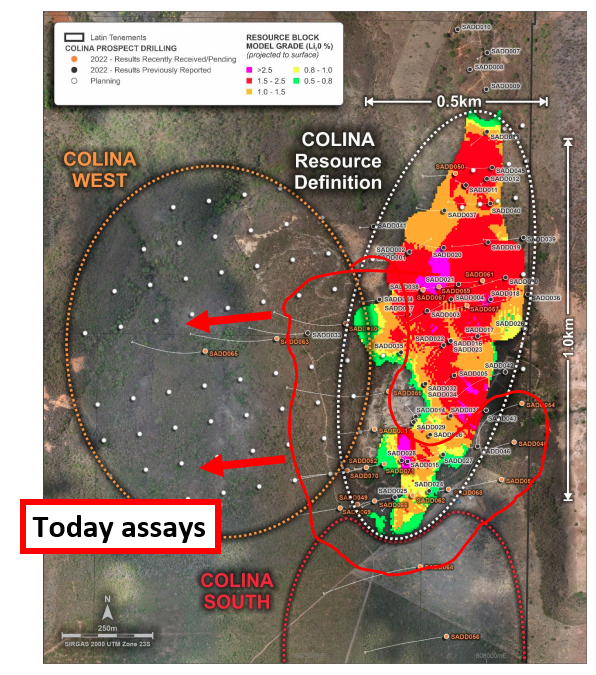

Today, LRS put out a batch of assay results from its resource expansion drilling program.

The results show that mineralisation extends into the areas to the west of its existing JORC resource with intercept thickness as high as 20.17m and lithium grades as high as 1.96%.

In drillholes completed late last year, LRS hit extensions to its current JORC resource in the direction of its Colina West discovery which sits ~500m to the west.

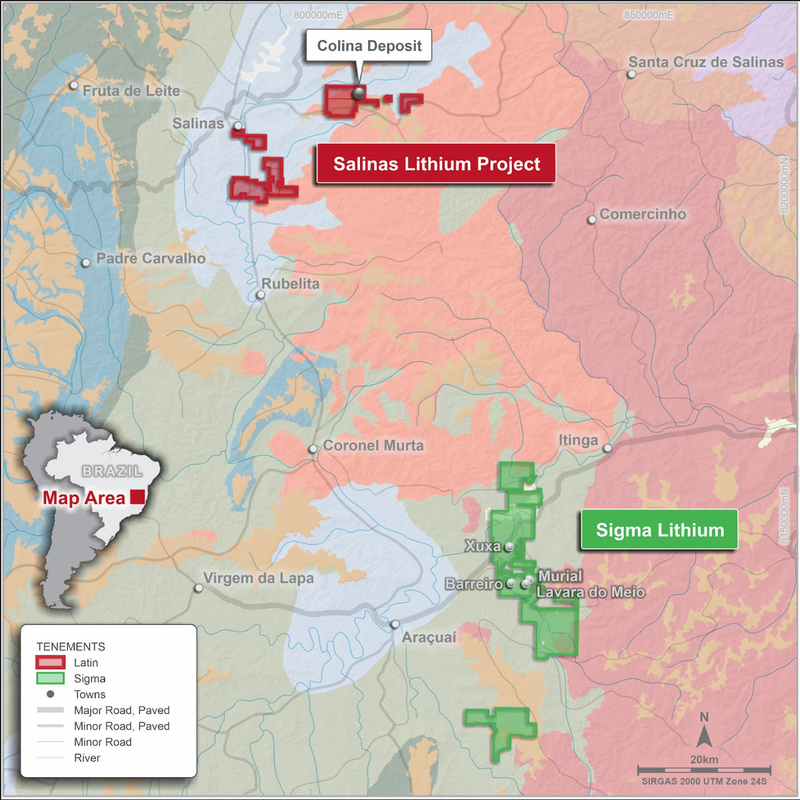

Below is an image showing where today’s assay results come from.

The light red part is where LRS’s assay results from today are and the highlighted section is where the existing JORC resource sits.

We are hoping LRS can continue to show hits like today’s and multiply the size of its resource.

Sigma’s resource, which started at a similar level to LRS’s, now sits at 85.6mt with lithium grades of ~1.43% five years later.

We are hoping with the current round of drilling, LRS will be able to take its resource to a level comparable with $4.7BN Sigma, if not one day even bigger.

This brings us to our “Big Bet” for LRS:

Our ‘Big Bet’

“LRS increases the scale of its lithium discovery to the level of its multi billion dollar regional peer - Sigma Lithium. With this we would expect the market to value LRS similarly.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LRS Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor LRS’s progress since we first Invested and track how the company is performing relative to our “Big Bet”, we maintain the following LRS “Progress Tracker”:

See our LRS Progress Tracker here:

More on today's assay results

Today’s assay results come from the drilling LRS completed late in 2022 - the primary focus of which was to test for extensions to the Colina West discovery that LRS announced last year.

Colina West sits ~500m west of LRS’s existing 13.3mt JORC resource and LRS’s theory going into these results was that:

A.) The two areas may come together to form one larger lithium deposit

OR

B.) The Colina West area could represent a large lithium deposit on its own.

Today’s assay results are starting to show signs of a combination of these two theories - which we think is good, considering it is still early into LRS’s drill program.

The assays show that LRS is continuing to hit lithium mineralisation immediately west of its existing JORC resource. But more importantly, that the lithium mineralisation extends along strike to the north, south and at depth.

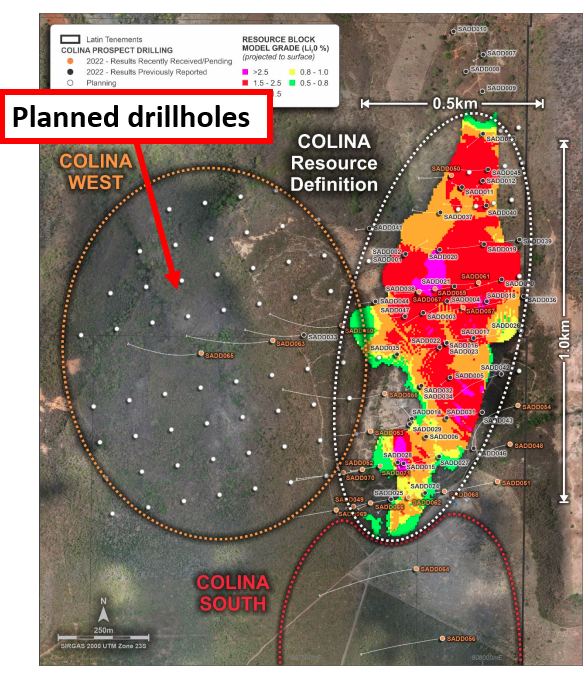

And LRS hasn't even had a go at drilling Colina South yet...

Another positive we mentioned earlier is that LRS continues to hit lithium intercepts with thickness (up to 20.17m), comparable to those from its existing JORC resource and with grades as high as 1.96% — well above the 1% grade that is typically considered economical for lithium deposits.

The highlight intercept from today's results came from drillhole 55, where LRS hit ~67m of cumulative lithium mineralisation with a peak thickness of 16.08m and a peak grade of 1.96%.

For some context, LRS’s first discovery hole measured 4.31m with lithium grades of 2.22% and 18.71m with lithium grades of 1.32% at Colina west.

LRS Geology Manager, Tony Greenaway, summarises the context pretty well with the following comment “ The thick high-grade mineralisation we have encountered here is on par with, or arguably better than the main Colina deposit”.

LRS has over 11 assay results pending and is currently drilling, meaning there is plenty of exploration newsflow to look forward to.

We hope the drilling continues to hit lithium mineralisation in and around both the existing JORC resource and the Colina West discovery, hopefully culminating in a significant resource upgrade at some stage later this year.

More on the Sigma Lithium playbook

We did a deep dive into the comparison between Sigma and LRS in our last note. We specifically touch on the following:

- Sigma’s journey from C$1.50 to a peak share price of C$54.23 per share — a ~3,500% return. Sigma had a similar market cap to LRS when it first announced its maiden resource estimate.

- Sigma’s initial resource estimate and how it compares to LRS’s maiden JORC resource estimate.

- LRS’s use of the same consultants Sigma is using to advance its projects.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

To see that note in full, check out the following link: LRS Delivers Maiden JORC Resource - Following $5.5BN Regional Peer’s Playbook.

For some context on location, here are LRS’s projects relative to Sigma’s:

What’s next for LRS?

Preliminary Economic Assessment (PEA) 🔄

The next major catalyst for LRS will be its Preliminary Economic Assessment (PEA).

This will set out a first pass set of financial metrics for LRS’s project and give investors an idea of the potential value of LRS’s resources.

LRS expects this to be ready for release to the market in Q1 2023.

65,000m drill program 🔄

LRS kicked off its 2022 drill program with six diamond drill rigs last week.

LRS has a further two drill rigs that it plans to add to the program in February, making for a total of eight rigs to complete the drill program.

Ultimately LRS is looking to expand its existing JORC resource and deliver further recourse upgrades before the end of this year.

What could go wrong?

Our 2022 LRS Investment Memo

Click here for our LRS Investment Memo, where you can find the following:

- Key objectives we want to see LRS achieve

- Why we are Invested in LRS

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.