KAU early quarterly update: Record gold production… again. Now at a 46 day streak.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,381,210 KAU shares and the Company’s staff own 71,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

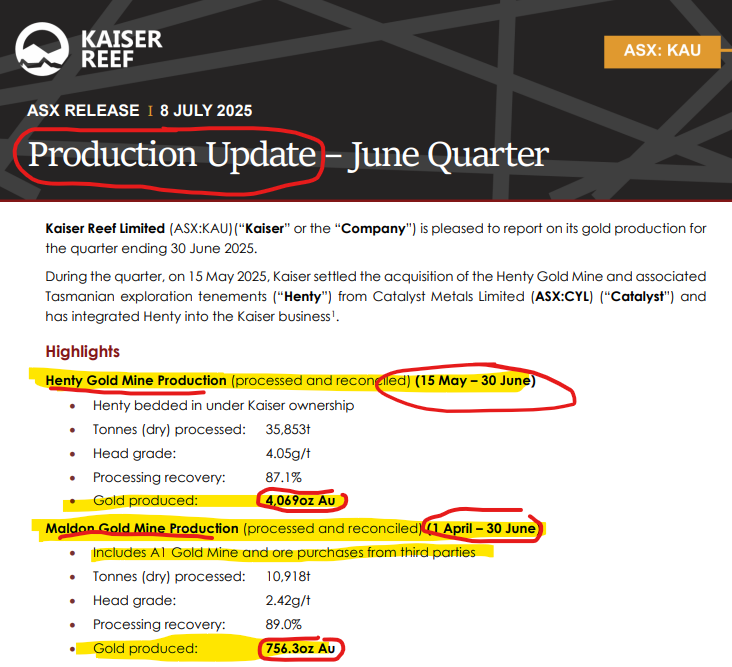

4,825 ounces of gold (~$24M worth at today’s spot prices) produced for the June quarter.

~$20M of that came from just HALF a quarter of production on one newly acquired mine...

Our gold Investment, the ~$106M capped Kaiser Reef (ASX:KAU),just put out its first quarterly update since the acquisition of the in-production Henty Mine in Tasmania.

(very early in July for a quarterly update... must be good news that couldn’t wait for the official quarterly report?)

The first thing that jumped out in today’s announcement is the 4,069 oz gold production from KAU’s first 46 days of owning the Henty gold mine.

KAU acquired the Henty mine from Catalyst Metals on the 15th of May, right in the middle of the April to June quarter reporting period.

KAU told the market the Henty mine is expected to produce 25,000 oz per year - which works out to be around 3,150 oz every 46 days.

So the 4,069 ounces produced in 46 days announced this morning is a lot higher than the market was guided to expect.

By our rough calcs (in AUD), even using the lower end of ~$5,050 per oz for the gold price, 4,069 ounces of production means ~$20.5M in revenue to KAU.

If we look at the mine's last production cost per ounce from the March quarter of $3,283/oz, that would be ~$7.2M profit to KAU.

Just from the last 46 days of production... (half a quarter of production)

These are our rough calcs only and we need to wait until KAU lodges its complete quarterly report later this month to get the actual costs. We take a more in depth look later in this article.

The ~$106M capped KAU is now a multi-asset gold producer targeting to produce ~30k ounces of gold per annum across its projects.

...with plans to grow that production number to ~50k ounces per annum

So far so good IF the Henty production numbers continue like this (no guarantee that they will of course)

How could KAU grow to 50,000 oz per year of gold production?

Profits made from the Henty mine can be used for:

- Exploration at Henty - which KAU is currently drilling (and recently said it already hit “108m intersection of strong alteration, 600m away from known mineralisation”)... KAU could announce drill results from Henty could drop at any minute.. (Source)

- Increasing production from the A1 Mine - In our opinion KAU A1 is overdue for a big production number, A1 is the reason we initially Invested in KAU and personally still want to see it reach its full potential.

- Exploration at Nuggety gold mine - This mine is famous for producing 301k ounces at 187g/t gold in 1856 to 1866... if KAU can find another high grade gold deposit here it can be processed and sold at KAU’s operational Maldon gold processing plant a few km away.

We should note that KAU took on $10M debt to pay for the Henty transactions costs, so profit from Henty may be used to pay that debt down faster than anticipated. We will get a better look at KAU’s financial position when the full quarterly is released by the end of this month.

Getting an early look at production numbers is a positive signal of how KAU’s assets are performing right now...

Across its Tasmania and Victorian assets, last quarter KAU produced a total of 4,825 ounces of gold, split:

- 4,069 ounces from its Tasmanian asset in half a quarter of ownership (Henty)

- 756 ounces from its Victorian assets (A1 and third party ores that were purchased)

(Source)

These numbers were better than the market was guided to expect, particularly from the Henty Mine where head grades were up by 31%.

Higher grades should mean stronger financial performance (we need to wait for the final quarterly report to confirm that).

At today’s gold price (A$5,070 per ounce) that would be ~$24M in gold produced for the June quarter...

From KAU, which is capped at ~$106M (at yesterday’s close price of 18c).

KAU has only owned the Henty mine for roughly 46 days of the full ~90 day quarter.

We’ll need to wait for the quarterly report to confirm exactly what sales revenue KAU generated from its gold poured in the June quarter and costs that were involved.

So while we will have to wait and see what today’s production numbers mean from a profitability perspective, here is why we think KAU’s quarterly could surprise the market to the upside:

Today’s results are stronger than we expected ...

At first glance today’s numbers looked really strong.

So we went back and compared the numbers to what has been reported in the past.

Results from KAU’s Tasmanian assets (Henty)

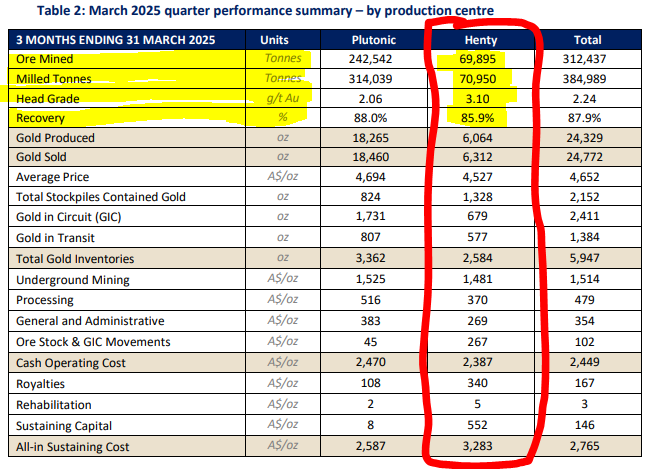

In the March quarter the previous owner of the project (Catalyst Metals) put out the following quarterly data on the asset:

(Source)

We can only compare what KAU announced today, which is how much material was processed, head grades and recoveries.

Here is how those numbers have changed under KAU ownership in the past 45 days:

So processed tonnes were slightly lower (based on a daily rate), BUT grades and recoveries were both higher.

Grade especially, was a lot higher than the Catalyst quarterly - IN FACT grade was up ~31%.

Looking at the Catalyst March quarterly, we can see Henty was producing at an “all in cost per ounce” of ~$3,283/oz (Source).

Based on the higher recoveries and higher grades KAU announced today we would assume costs are lower for the 45 days that KAU owned the asset...

Of course, there is no way to know where costs ended up for the quarter just yet - we will have to wait and see what the quarterly shows before the end of this month.

Even just using the $3,283 per ounce all in cost it could mean ~$7.2M in profit to KAU for the 45 days it has owned Henty....

That’s a big assumption by us, and there is no guarantee that the past all in cost per ounce that Catalyst achieved in March will be repeated this quarter by KAU.

There is no information in today’s announcement about exploration, development, capital, or admin/overhead expenditures KAU might have had during the quarter. KAU also has its debt position that it needs to manage.

We’ll need to wait for KAU to update the market on all of this in its upcoming full quarterly report.

Results from KAU’s Victorian assets (A1 + Maldon):

KAU produced the same amount of gold from its Victorian assets that it produced in the previous March quarter, 551 ounces of gold.

The major difference in this June quarter was that grades were up slightly (by ~5%) AND the realised gold price could be a lot higher than the $4,726/oz gold price that KAU secured in the March quarter.

(Source - March Quarter, Source - June Quarter)

The gold price spent most of the June quarter at between A$5,000 and A$5,200 per ounce:

AND KAU purchased and processed third party ores which delivered a further 205 ounces of gold, which would be another ~$1M in revenues at today’s gold prices...

During the March quarter, KAU burnt ~$4.5M in cash (including all capital expenditures) on ~$3.5M revenues.

With a higher average gold price over the quarter, higher grades at A1 and the extra production from the 205 ounces that came from purchased ore we are hoping KAU’s Victorian assets are a lot closer to breakeven this quarter.

Now targeting 30,000 oz per year gold production - Here’s what KAU owns

KAU is, for the first time ever, mining virgin sections of its Victorian A1 gold mine, and can now supercharge its cashflows with Henty in Tasmania.

What we want to see with our Investment in KAU is for the gold price to stay at current levels or keep going up... and for KAU to become extremely profitable.

While we hope gold prices rise and KAU delivers its guided production numbers, there is always a risk that the gold price falls and/or KAU runs into production issues on ramp-up.

Now that the Henty acquisition is completed, KAU holds:

- Gold mine in Victoria (A1 Mine, 100% owned) -The A1 gold mine is where KAU recently started mining never before mined parts of the project. KAU is targeting production of ~20k ounces per annum from this mine.

- Gold mine and processing plant in Tasmania (Henty, 100% being acquired) - a “plug and play” type asset, already producing ~25k ounces per annum and with over 5+ years of mine life in reserves (10+ years in resources).

- Gold exploration in Victoria (Maldon, 100% owned) - Inferred JORC resource of 1.2Mt @ 4.4g/t gold for ~186K ounce gold resource and reserve with exploration upside.

- Gold processing plant in Victoria (Maldon, $1.6BN Catalyst Metals has an option on a 50-50 Joint Venture with KAU) -Running at 20-30% capacity with the opportunity to ramp up to 350,000 tonnes per annum. Gold processing plants in Victoria are almost impossible to permit nowadays... Anyone looking to roll up assets in Victoria could see this as a strategically important asset.

The four catalysts we think could re-rate KAU’s market cap

Post the Henty acquisition, KAU is a completely different company to when we first Invested in the company last year.

Given KAU is now capped at ~$106M and with a new asset delivering most of the production, we think the catalysts that could re-rate the company are also different.

Our view is that one OR a combination of the 4 following catalysts could re-rate KAU’s market cap from where it is today to a higher level:

(at the same time, if the below things don't happen, the KAU share price may not go up and could in fact go down... )

1. Consistent production and strong cash flows

Now that KAU is producing a material amount of gold we think the market could start to value the company based on gold production and cashflows.

IF KAU can show a number of consecutive quarters of positive cashflows and strong revenue numbers, the market may start to value the company based on a multiple of profits generated from mining and processing gold.

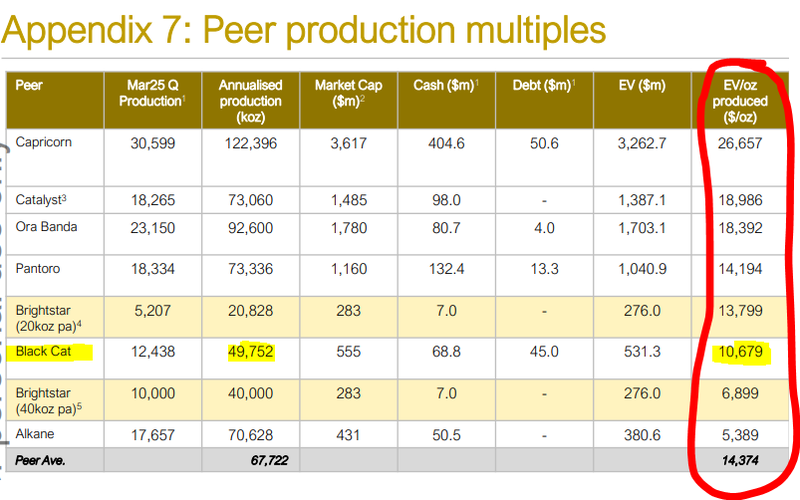

To get an idea of what this might look like, we pulled the following peer comparison table from a Brightstar Resources presentation.

On this table, producers with less than 100k ounces per annum of production trade at EV/ounce produced rates between $5,389 and $18,986/oz.

KAU based on the targeted 30,000 ounce annualised production target is currently being valued at an EV/ounce produced rate of ~$3,000/oz.

It’s early days for KAU but that looks like a decent valuation gap to catch up to - let's see how the next couple of quarters pan out.

(Source)

2. Exploration success at Maldon and Henty

We think KAU is highly leveraged to any exploration success because of the existing processing infrastructure already in place at both its Maldon and Henty projects.

If KAU’s exploration results deliver a new high-grade discovery, it may be monetised quickly through KAU’s existing infrastructure on the project.

(compared this to other exploration projects that need to undertake years of feasibility studies and expensive CAPEX buildouts of processing plants).

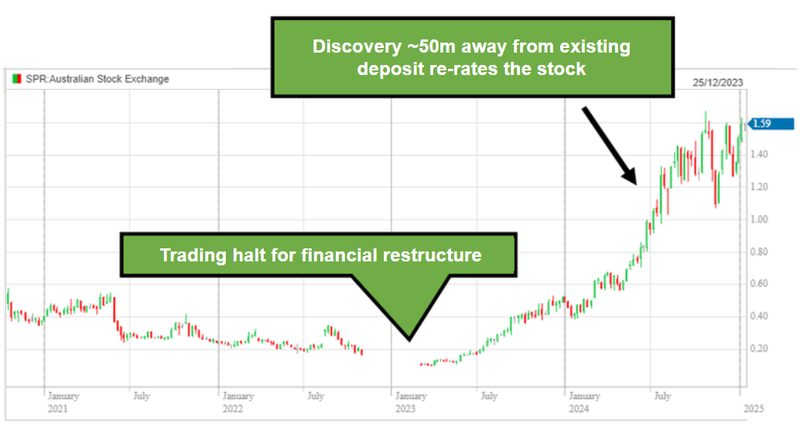

While there is no guarantee that KAU is able to identify more high-grade gold through its exploration programs, there is precedent for this type of success.

ASX-listed company Spartan Resources went from 10 cents to $2 per share off the back of a discovery ~50m from its processing plant that was under care and maintenance.

Spartan’s new discovery and all the drilling after it took the company to a market cap of A$2.4 billion when it was eventually merged with Ramelius Resources earlier this year. (Source)

There is no guarantee that KAU will achieve the same success as Spartan.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

See our deep dive on the exploration upside here: Exploration is still a big part of the story with producing ounces.

3. If the gold price keeps going up, this is good for KAU

KAU is now heavily leveraged to gold prices because it is producing gold and is currently unhedged.

Being unhedged means KAU has 100% exposure to a rising (and falling) gold price.

KAU’s forecast production is ~30,000 ounces per annum (with plans to increase that to 50,000 ounces in the coming years).

Any changes in gold prices should flow straight down into KAU’s bottom line.

For some context, if the gold price went up 5% from where it is today, assuming KAU could produce ~30,000 ounces of gold it could generate an additional ~$8M in revenues.

KAU being completely unhedged also comes with risks. Any fall in the gold price could impact

KAU’s bottom line negatively as well (a loss of -~$8M in revenues from a 5% fall) and there is

no guarantee that the gold price stays up or rises.

We think the gold price could keep going up - check out our last note where we explain why: We think gold price could keep running

4. Index buying could come into KAU

A common problem small miners face is they can't access the deeper pocketed institutional investors until they have reached a certain size (often market caps above A$150M, depending on the fund).

This is because fund managers have certain mandates to protect client capital and manage risk, and micro cap stocks are considered to be too “risky” and tiny positions may not be meaningful enough for their investors (again, depending on the fund).

We think KAU can get itself to a level where institutional buying comes into the stock through M&A (like it has done to date) AND through cashflows from its current assets.

However, if the company doesn’t grow to the size where it can access institutional capital, KAU may be reliant on cash flows from its operations, and the broader retail market.

See our take on how KAU can attract index buying here: M&A has built some of the ASX’s biggest gold companies - Why we like KAU’s acquisition strategy

Ultimately, we are Invested in KAU to see the company grow production and use cashflows to fund exploration OR M&A, which forms the basis for our Big Bet as follows:

Our Big Bet for KAU

“KAU can grow production at both of its projects in Tasmania and Victoria to >50k ounces per annum. Using that cashflow KAU can fund exploration OR M&A that leads to a re-rate in the company’s market cap to above $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and regulatory risk - just some of which we list in our KAU Investment Memo.

Success will require a significant amount of luck and good management. Past performance is not an indicator of future performance.

What’s next for KAU?

June quarterly report 🔄

Now that we know what the production figures are for KAU’s June quarter, we want to see how the quarter looked financially.

We are hoping KAU is able to deliver a big positive cash flow quarter and surprise the market to the upside.

Cost optimisation and exploration at Henty 🔄

The main thing we want to see at Henty is for KAU to increase production rates and optimise costs.

BUT at the same time we are looking forward to exploration drill results from the project.

KAU is currently drilling at Henty and has already hit a “108m intersection of strong alteration, indicating that the Henty style alteration extends 600m from the current known mineralisation”.

The main target for the drilling is to find extensions to the “Darwin Zone” which is where Henty has produced over 655k ounces of gold at average gold grades of 8.4g/t.

If we get big extensions to the south of that area and show that those numbers could be repeated into the future we think that will be a big win for KAU.

Here is a visual of where KAU is drilling (note those chequered sections “Darwin target zone” and “Darwin South”:

(Source)

Development and exploration update from A1 mine 🔄

The March quarter for A1 was all about transitioning from remnant mining to never before mined parts of the A1 mine.

KAU’s most recent presentation teased increased development which would mean KAU could mine out two levels per annum.

KAU also said the target at A1 was to increase the mine’s production run rate to “more than 20,000 oz per annum” - that would be an eightfold increase on the quarterly production numbers we got today...

(Source)

Exploration program at Maldon 🔄

KAU mentioned in its recent investor presentation that it is planning more drilling at Maldon.

The Maldon project is just ~4km away from KAU’s 350,000 tonnes per annum gold processing plant that is currently underutilised (running about 20-30% capacity).

We expect that any exploration success could be quickly monetized because of the access that KAU has to existing gold processing infrastructure.

Maldon was also home to Australia’s highest grade gold mine - Nuggety Reef - which produced ~301k ounces of gold at ~187g/t gold grades.

Although not guaranteed, a major discovery at Maldon (even 1/10th of the grades Nuggety produced at) could be a game changer for KAU primarily because of the proximity to a mill which is currently operating at 20% of its capacity:

What are the risks?

The three key risks to our KAU Investment Thesis in the short term are - “Production Risk”, “Commodity Price Risk” and “Exploration Risk”.

Production risk because, KAU now has two operating assets which carry significant costs.

If production rates fall materially, it could mean significant negative cashflows to KAU which would hurt the company’s share price.

Production Risk

The ability of the KAU to achieve production targets or meet operating and capital expenditure estimates on a timely basis cannot be assured. As a producer, KAU is subject to risks such as but not limited to, labour costs and availability, energy prices as well as KAU’s internal ability to forecast costs like these and budget effectively.

Source: “What could go wrong” - KAU Investment Memo 26 May 2025

Commodity prices (in this case gold) are also a risk to our KAU Investment.

KAU is a completely unhedged gold producer, any falls in the gold price would impact revenues directly.

If gold prices fell enough, we would expect it to impact the KAU share price negatively.

Commodity Price Risk

KAU is an unhedged gold producer, meaning all of its production is sold at, or close to, the spot price for gold at any given time. Any material fall in the gold price could hurt KAU’s share price significantly.

Source: “What could go wrong” - KAU Investment Memo 26 May 2025

Finally, even though KAU is a gold producer, we are still conscious of exploration risk because the company is still running exploration campaigns across both of its assets.

Poor exploration results from Henty in Tasmania could impact the market’s view on KAU’s ability to expand its current resources and mine life for the project.

Any negative results could mean the market starts to price in a limited mine life for the project.

Exploration risk

There is no guarantee that KAU’s drill programs are successful, and KAU may fail to find economic gold deposits.

Source: “What could go wrong” - KAU Investment Memo 26 May 2025

For the full set of risks we have identified and accepted in making our Investment in KAU, see our KAU Investment Memo below.

Other Risks

The company’s financial risk is also material, as it needs to generate sufficient internal cash flow to fund its production growth and exploration programs without resorting to dilutionary capital raisings.

Ambitious plans to grow to 50,000oz of annual production carry development risk, particularly at the A1 mine, which is still transitioning to new ore zones.

Additionally, KAU’s operations depend on attracting and retaining skilled labour, exposing it to personnel and operational capability risk, while evolving state regulations create regulatory and permitting risk, especially in tightly controlled jurisdictions like Victoria.

Finally, as a sub-$150M market cap company, KAU remains exposed to market perception and liquidity risk, where weak sentiment or negative news could disproportionately affect the share price due to limited institutional support.

Our KAU Investment Memo

You can read our KAU Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our KAU Investment Memo covers:

- What does KAU do?

- The macro theme for KAU

- Our KAU Big Bet

- What we want to see KAU achieve

- Why we are Invested in KAU

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.