EXR: Gets $13.9M strategic investment for 19.43%. Takeovers and consolidation in the Taroom Trough next?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,036,850 EXR Shares and 2,567,021 EXR Options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

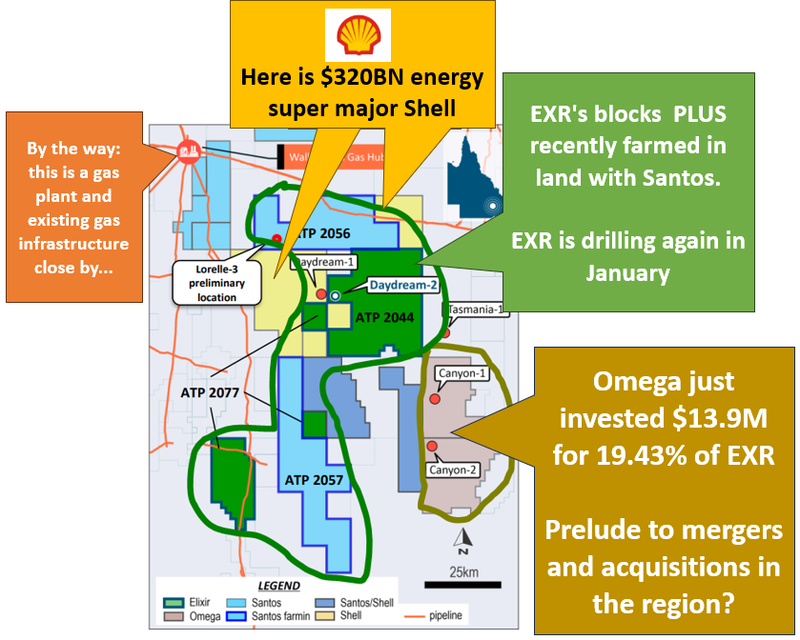

Some of the Australian oil and gas industry's heaviest hitters are increasing activity in the “Taroom Trough” in Queensland...

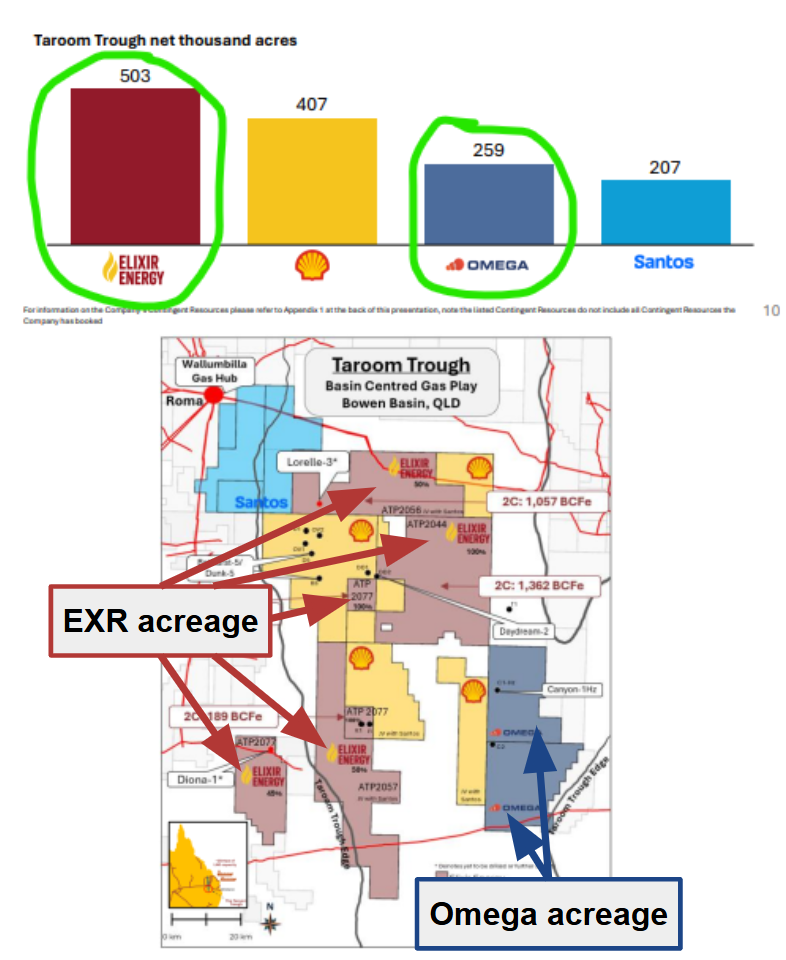

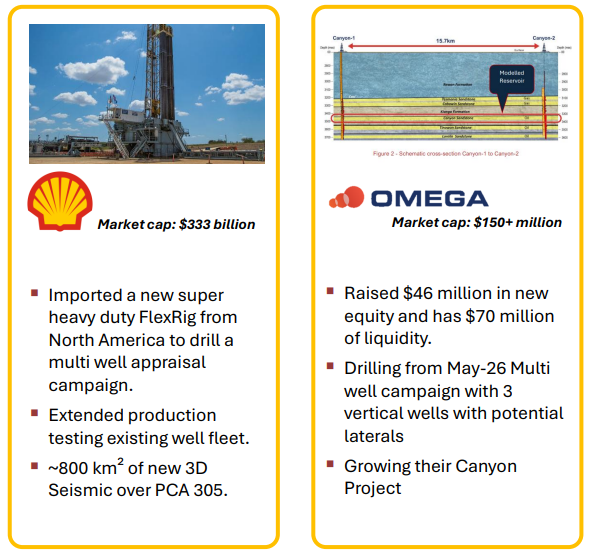

AND our Investment Elixir Energy (ASX:EXR) is the biggest net acreage holder in the region - second only to supermajor $320BN Shell.

EXR just did a deal with the #3 landholder in the region - Omega Oil and Gas.

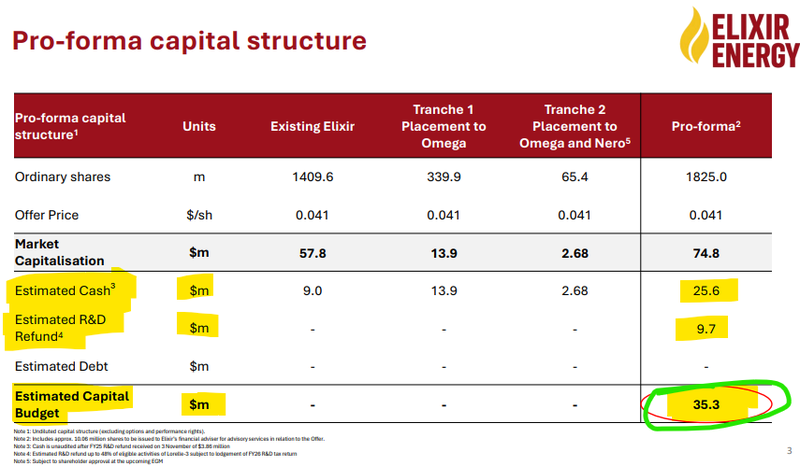

Omega took a 19.43% position in EXR in exchange for $13.9M at 4.1c per share.

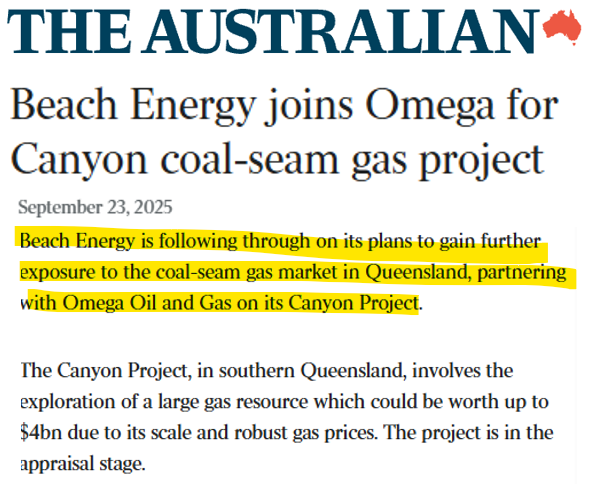

Omega is backed by Tri-Star (pioneers of the Queensland gas industry) and it recently did a deal with ~$2.8BN Beach Energy...

After the deal is completed EXR will have a $35.3M capital budget to work with.

Next, EXR is drilling a vertical well targeting a ~1 trillion cubic feet of contingent gas resource (estimate).

Drilling starts in January...

And then a horizontal section, with stimulating and testing will follow straight after.

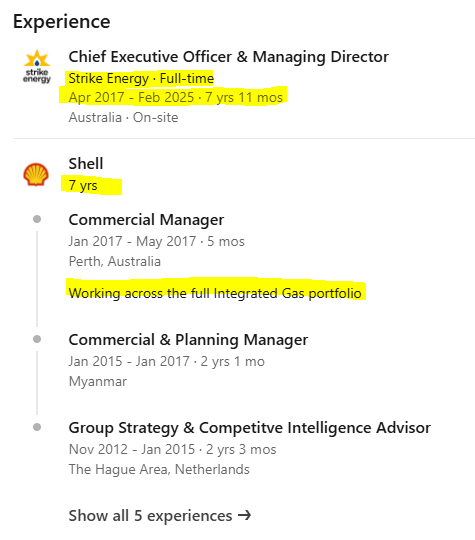

It all kicks off on the 12th of January according to the EXR MD and CEO Stuart Nicholls in a webinar a few days ago. (Source- watch it here)

(Stuart joined EXR in April, prior to this he was CEO and MD of Strike Energy taking it from a tiny micro cap explorer to becoming an ASX200 company capped at ~$400M today)

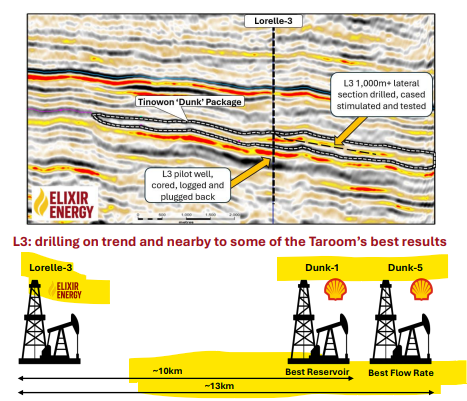

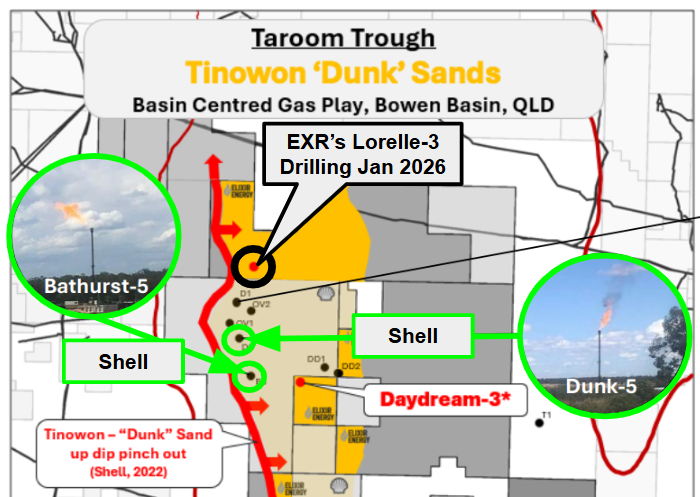

EXR’s main target for next year is Lorelle-3 which is ~10km away from Shell’s Dunk-1 well AND ~13km away from Shell’s Dunk-5 - two of Shell’s best wells in the region.

EXR expects drilling to start in January and then immediately roll into a horizontal well and testing...

The main thing we want to see is EXR prove commercial flow rates and upgrade the blocks ~1 trillion cubic feet contingent resource into reserves...

(which will make M&A discussions a lot more interesting for EXR shareholders)

(Source)

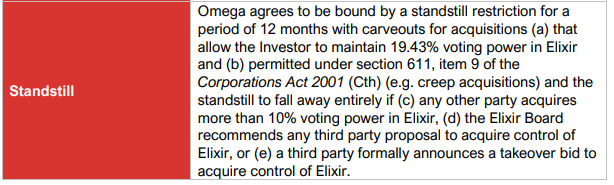

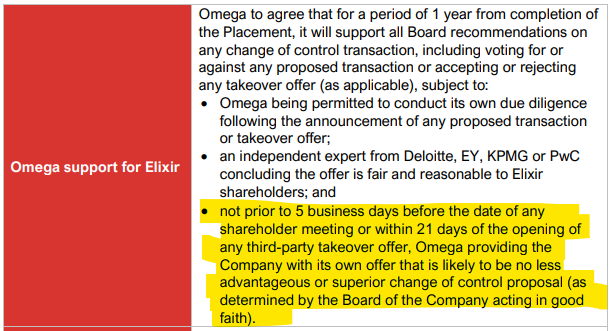

We also noticed that part of the conditions of Omega’s investment in EXR there were two specific conditions.

First the “standstill” - which means Omega can’t buy any more shares in EXR for at least 12 months - basically EXR being given a 12-month period to deliver material catalysts (like the Lorelle drilling and horizontal well)...

And second, the support condition - which basically means if EXR were to attract a takeover offer inside the next 12 months from someone OTHER THAN Omega, Omega wouldn't be able to block the transaction (UNLESS they are willing to match/beat the proposal).

We think this is a very good deal for EXR shareholders, especially if the January drill results come in...

After this week’s deal the clear front runners in the Taroom Trough are EXR/Omega and then $320BN Shell...

The way we see it, Omega and EXR will be the ones holding the keys to the basin if a supermajor (like Shell) ever wants to do a deal and take control of the region.

Now, between Omega and EXR the two hold by far the most acreage in the basin - second only to $320BN Shell.

(Source)

Now, the two can drill out wells, prove commerciality with some big horizontal wells before creating competitive tension amongst the supermajors who are watching the area...

As mentioned earlier, we already know Shell is active in the area.

Last year there were mainstream media articles talking about Shell’s wells in the Taroom Trough being flared. (Source)

Here are the flares from Shell’s wells relative to where EXR plans to drill in January 2026:

(Source)

And we also know Beach have shown an interest in the Taroom Trough by doing a deal with Omega to take 25% ownership in any new ground Omega stakes in the region.

That deal by Beach was done as a partnership on an “area of mutual interest”... (source)

(source)

There have been reports Beach are looking for big M&A deals around Australia (and specifically in the Taroom Trough) - so they might not be done here yet:

Maybe they are dabbling, before getting comfortable with the region and doing a bigger deal?

(Source)

We think the Taroom Trough (IF it can prove up commercial flow rates) could eventually attract interest from other supermajors - especially out of the US.

Just like the Beetaloo in the Northern Territory has managed to attract attention from US billionaires.

We note there have been some reports that US supermajor $167BN ConocoPhillips was looking at the region too:

(Source)

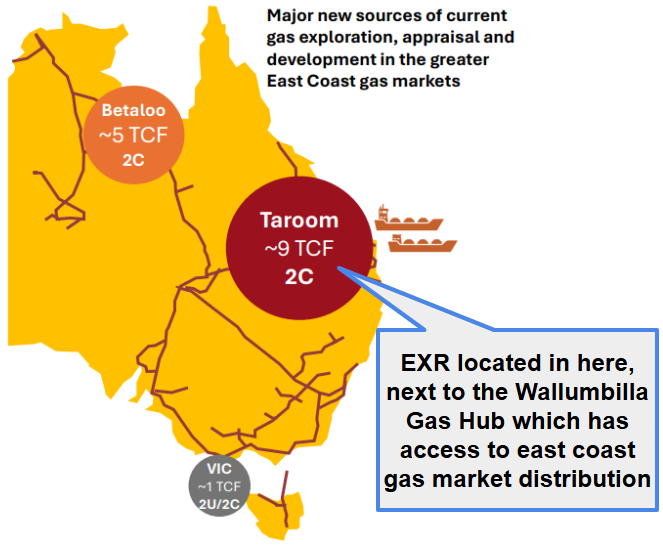

We think the Taroom Trough could end up being a lot more interesting (relative to the Beetaloo) first because the size/scale is larger and second because its much much closer to existing gas infrastructure and can tap into domestic and international markets a lot quicker.

For context there are three LNG plants in Gladstone that have never operated at full capacity and could take more gas feedstock to ship to international markets, and

EXR’s project sits next to the Wallumbilla Gas Hub, which distributes gas to the east coast market. The east coast of Australia is forecast to be short gas in 2028 and expected to start experiencing supply shortages beyond 2026.

(Source)

We think the new team behind EXR and guys running Omega will know what needs to be done to de-risk the region and make it interesting for a supermajor...

Again, EXR’s new MD and CEO Stuart Nicholls was previously the CEO and MD of Strike Energy taking it from a tiny micro cap explorer to becoming an ASX 200 listed company.

Strike is today capped at ~$400M.

Interestingly, Stuart has also held management roles with Shell (who are active next to EXR’s assets).

(Source)

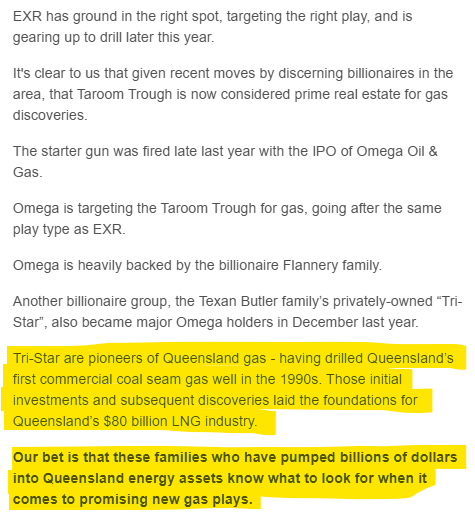

Omega is heavily backed by the billionaire Flannery family and another billionaire group - the Texan Butler family’s privately-owned “Tri-Star” are also major shareholders in Omega.

Tri-Star are pioneers of Queensland gas - having drilled Queensland’s first commercial coal seam gas well in the 1990s. Those initial investments and subsequent discoveries laid the foundations for Queensland’s $80 billion LNG industry. (Source)(Source)

We actually said this in a previous note back in May 2023:

(Source)

Omega and EXR’s chairmen also played a role in the early days of the QLD gas industry

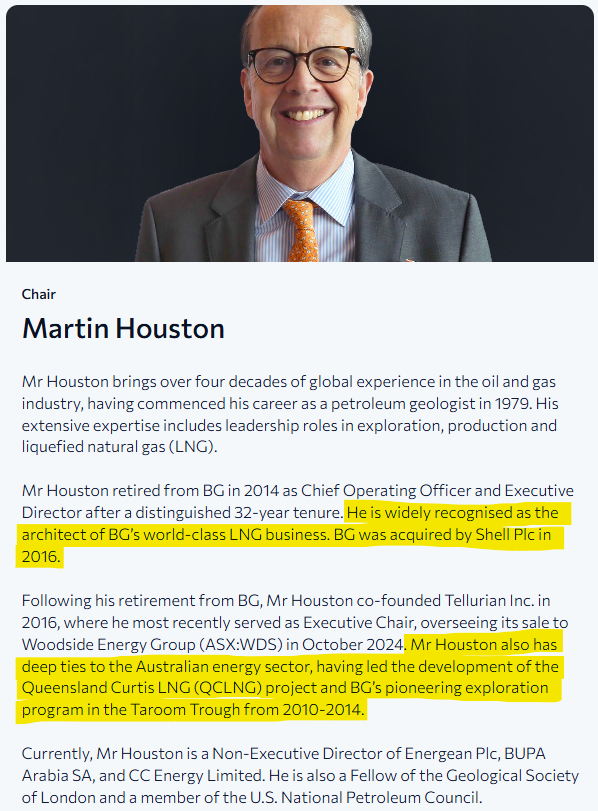

Omega’s new chairman, and EXR’s chairman also share some history...

Omega Chairman is Martin Houston who was the former COO of BG Group - which in 2008 acquired a company called QGC for ~$5.3BN...

QGC was the company EXR’s chairman Richard Cottee built as Managing Director from a $20M capped junior all the way through to the $5.3BN takeover back in 2008.

(Source)

Eventually in 2016 the combined entity (BG Group) was acquired by supermajor Shell for US$52BN.

(Source)

Now, just under a decade later, the two chairs are active in the same region again.

AND their old friend Shell is active next door to both companies...

Here is EXR’s chair’s background:

(Source)

And here is Omega’s chair’s background:

(Source)

All the region needs is some strong flow rates proven up in horizontal wells.

And then for a supermajor looking to increase its exposure to the Australian east coast gas market (and international LNG markets) to come in and take everyone out...

(like that Shell deal all those years ago).

IF that day ever comes, we think EXR and Omega will be the ones who will be handing over the keys to a major...

What comes next for EXR?

EXR will have ~$25.6M after this weeks deals are settled...

AND EXR got confirmation from blah that it’s Lorelle-3 drilling would be eligible for R&D refunds for up to 48.5% of costs (EXR estimates that at A$9.7M). (source)

So EXR will have a “capital budget” of ~$35.3M to fund phase 1 and 2 of its development plan.

(Source)

EXR’s plan is to drill a vertical well first (starting in January).

In a webinar a few days ago, EXR’s CEO and managing director said that the rig would start mobilisation on the 12th of Jan... so not long to go now.

EXR’s plan is to then immediately follow it up with a horizontal well and flow test to book reserves later in the year.

Alongside that EXR also plans to shoot some seismic and flow test the Diona-1 well that was recently drilled.

(Source)

The Lorelle 3 well is the one we are looking forward to seeing the most.

The well sits ~10km away from Shell’s Dunk-1 well which had the best reservoir characteristics in the whole region.

AND ~13km away from Shell’s Dunk-5 well which had the best flow rate.

Here EXR will be looking to convert a ~1.05 Trillion cubic feet 2C resource into reserves.

(Source)

Here is an image showing where EXR’s well sits relative to the wells Shell have been drilling:

(Source)

We think that with Lorelle, EXR could prove commerciality on its blocks and de-risk the rest of its ground...

(and maybe create competitive tension around acquiring EXR in its entirety)

We also noticed that part of the conditions of Omega’s investment in EXR there were two specific conditions.

First the standstill - which means Omega can’t buy any more shares in EXR for at least 12 months - basically EXR being given a 12 month period to deliver material catalysts (like the Lorelle drilling and horizontal well)...

(Source)

And second the support condition - which basically means if EXR was to attract a takeover offer inside the next 12 months from someone other than Omega, they wouldnt be able to block the transaction (UNLESS they are willing to match/beat the proposal).

Usually giving a controlling stake (like the 19.4% Omega took of EXR) takes away any competitive tension in terms of takeover potential, EXR has managed to retain that with these two conditions (which we like as existing shareholders):

(Source)

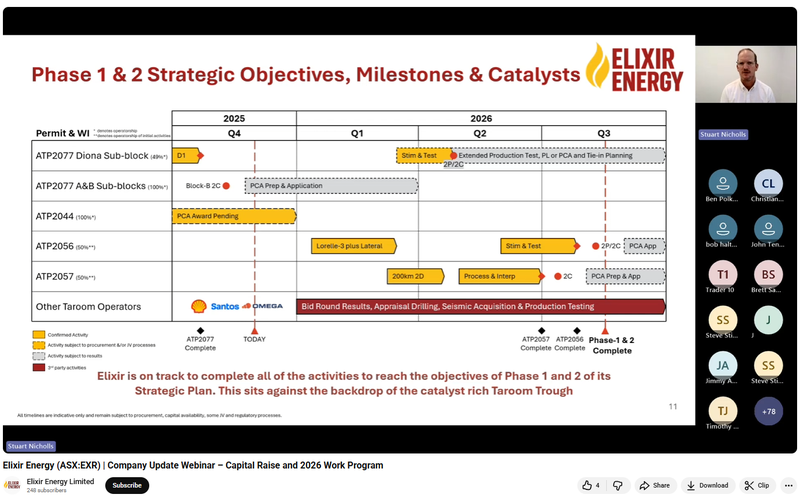

We listened to the webinar yesterday, where CEO and managing director Stuart Nicholls gave a really good run through on what’s coming:

(Source)

We will also be keeping a close eye on other activity in the region:

Now that Omega are EXR’s biggest shareholders - we will also be watching how they go with their upcoming Canyon horizontal well.

The first question in the Q&A section of yesterday’s webinar was actually about other activity in the region (at 26 minutes into the webinar):

Stuart actually talked about “expecting a multi-well campaign from Shell, 2 to 3, potentially 4 wells over the coming months or so”.

He then talked about the 3-well campaign that Omega are planning.

We think that any good news from these operators will be good for EXR, so fingers crossed we hear good news from them.

(Source)

What are the risks?

The key risk for EXR will be exploration risk.

The main target EXR is drilling in January already has a contingent resource, but there is no guarantee that EXR are able to confirm those resources OR that they can prove they can flow at commercially viable flow rates.

IF the well fails to deliver then the market could re-rate EXR lower.

Exploration risk

There is risk that EXR does not achieve a reasonable flow rate from appraisal drilling at its Daydream-2 appraisal well at its Queensland gas project.

Source: “What could go wrong” section - EXR Investment Memo 29 March 2023

Another risk to watch out for is “risk of mechanical failure”.

Things can and do go wrong with drilling, last year EXR’s flow test was delayed due to mechanical issues with the well.

Any delays caused by mechanical failure will be a set back for EXR.

To see all of the risks specific to EXR read our EXR Investment Memo.

Other risks

Like any small cap energy investment, EXR carries a range of risks that could impact the company’s valuation, including risks that are not foreseeable at this stage.

EXR is still in the early stages of proving commercial gas flow rates in the Taroom Trough. It is possible that the upcoming vertical and horizontal wells fail to demonstrate the reservoir quality or sustained flow rates required to underpin a commercial development.

The company’s strategy also relies on drilling outcomes from multiple operators across the basin. While positive news from Shell or Omega could support EXR’s valuation, disappointing results from nearby wells may have the opposite effect.

Commodity price risk is ever-present. A prolonged downturn in domestic or international gas prices, or changes to LNG export economics, could reduce the value of EXR’s acreage and limit the appetite of potential farm-in or M&A partners.

As a pre-production small cap, EXR is dependent on capital markets to fund its multi-well programs. Any future raising could dilute existing shareholders, particularly if drilling takes longer than expected, costs escalate, or market sentiment weakens.

Regulatory and permitting risks also apply. Changes in Queensland’s gas policy, environmental approval delays, or shifts in federal energy settings may impact project timelines or increase development costs.

There is also corporate and transaction risk. While EXR has attracted strategic shareholders like Omega, there is no guarantee this interest translates into a future takeover, farm-out, or development partnership, and conditions attached to major shareholdings may influence potential deal-making dynamics.

Execution risk remains material. Drilling, completing, and flow testing horizontal wells in a frontier basin is complex, and operational issues such as rig delays, mechanical failures, or formation challenges could affect timelines and outcomes.

Finally, as with all speculative energy explorers, EXR’s share price may already be factoring in anticipated future success, increasing the potential for volatility if drilling does not meet market expectations.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EXR Investment Memo:

Our EXR Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our EXR Investment Memo, you can find the following:

- What does EXR do?

- The macro theme for EXR

- Our EXR Big Bet

- What we want to see EXR achieve

- Why we are Invested in EXR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.