EXR: Flow test results from neighbour Omega any day now…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,136,850 EXR Shares and 2,567,021 EXR Options and the Company’s staff own 40,000 EXR Shares and 13,333 EXR Options at the time of publishing this article. The Company has been engaged by EXR to share our commentary on the progress of our Investment in EXR over time.

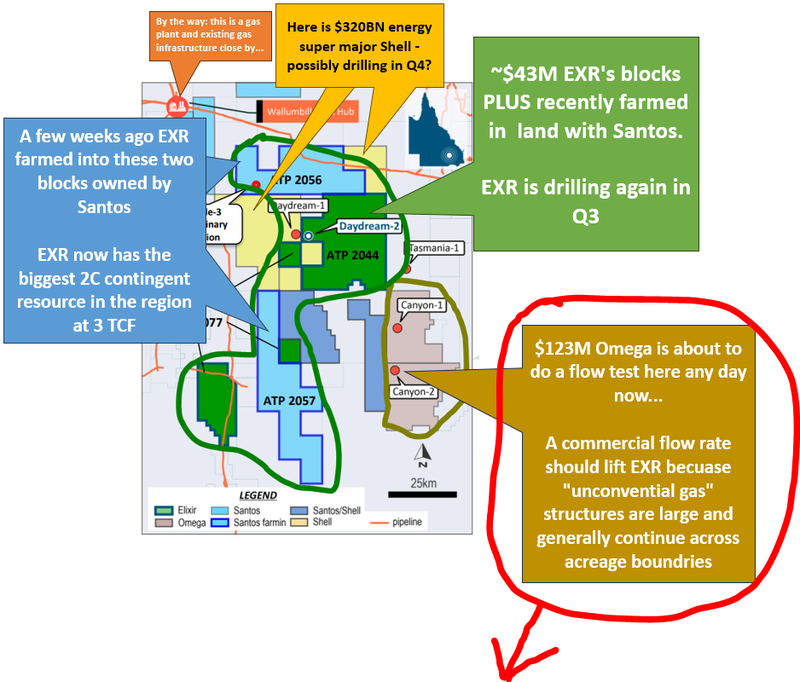

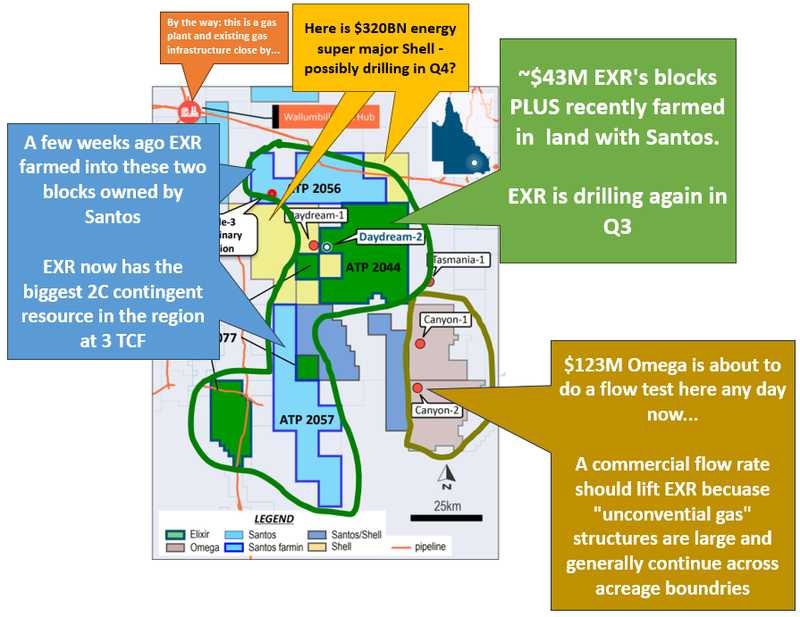

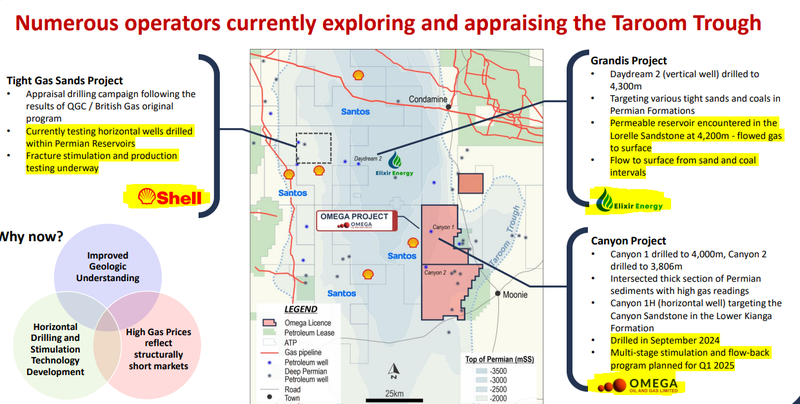

$42M capped Elixir Energy (ASX:EXR) has the biggest acreage holding in the Taroom Trough in Queensland, Australia.

EXR's neighbour, $140M capped Omega Oil and Gas is currently flow testing its first horizontal well next door...

We are expecting initial flow results from Omega any day now.

(Source - LinkedIn post from one week ago)

Omega’s share price has been rising in anticipation of the results - so there is clear market interest in what they are doing.

We think an above expectation flow result for Omega would be a share price catalyst for neighbouring EXR.

Why?

This region is highly prospective for “unconventional” gas - which is different to “conventional” gas.

Conventional gas collects up in isolated “pockets” under a trap and seal.

Unconventional gas is widely spread out and trapped through a giant, sprawling underground structure.

A structure that easily transcends acreage boundaries between neighbours.

If a neighbour has success and you are sitting on the same unconventional gas structure, it's highly likely you will have the same gas and be able to obtain similar flow rates using similar techniques:

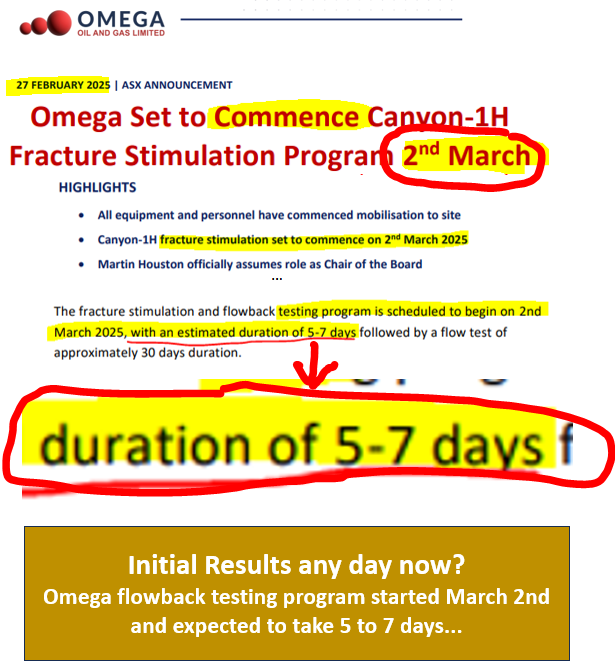

(Source - OMA ann Feb 27th - Image edited to highlight key information)

As EXR shareholders, we’re closely watching (and cheering for) this upcoming result from Omega.

The market anticipation is already building, with Omega’s share price steadily rising:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Currently, EXR is capped at ~$42M and Omega at ~$140M.

EXR has almost double Omega’s contingent resource - EXR has ~3TCF, Omega has ~1.7 TCF.

AND EXR is the biggest landholder in the region - even bigger than $320BN Shell, the energy supermajor that is flaring gas from some of its wells in the region (according to media reports).

Beyond the Omega flow test, EXR has its own well planned for Q3 of this year.

When could these initial Omega results come out?

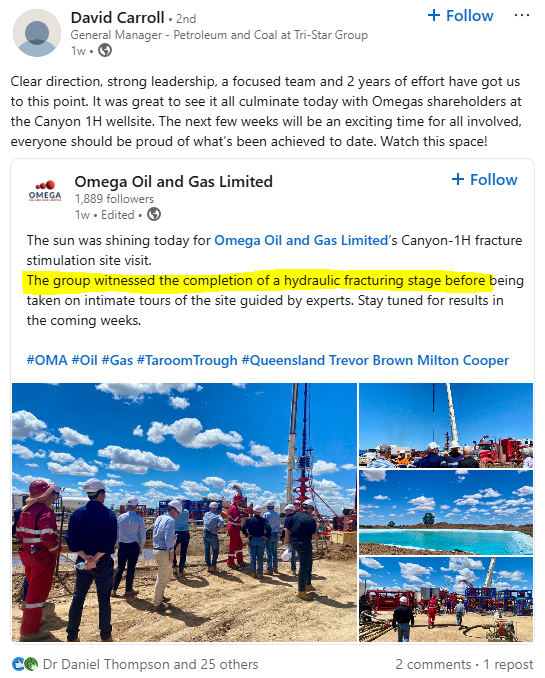

Last week we saw a LinkedIn post by Omega about an investor site visit to its well site.

That post said Omega had completed a “hydraulic fracturing stage” - which means the fracture/stimulation work has been happening for over a week now.

(Source)

We think that could mean an ASX announcement from Omega might not be very far away...

Omega said that the fracturing/stimulation program would take 5-7 days, and then the company would start a 30-day flow test.

Within the next few days, we might get some early stage flow rates from Omega...

With the Omega catalyst upcoming, we increased our Investment in EXR in the recent 3.5c placement.

EXR has also launched a Share Purchase Plan open to existing holders that allow holders to participate on the same terms as the placement.

The SPP is at the same price as the placement with the same free options. (link to the SPP, more on this later).

While the current EXR share price is trading below the SPP price, the SPP doesn't close until April 15th, which is plenty of time for Omega to potentially deliver material news and with it re-rate EXR in parallel.

We intend to participate in the Share Purchase Plan (SPP).

Omega’s flow test could open up the region...

The reason we are so interested in Omega’s result is because of the type of geology in the Taroom Trough.

The type of gas Omega is targeting is the same “unconventional” gas that EXR is going after.

So EXR and Omega are both drilling the same play...

If a neighbour has success and you are sitting on the same type of geology with the same unconventional gas structures, it's highly likely you will be able to flow gas at similar rates too.

So good news for Omega should be good news for EXR...

If someone can prove up strong flow rates in the region, then our expectation would be to see interest increase from majors who were watching from the sidelines.

Shell and Santos are already active in the region, and Beach was rumoured to have eyes on the region.

Which (if there is more good news) can only be good for EXR.

(Source)

(Source)

Again, here is our visual summary of everything happening in the region:

(NOTE: This image was created two weeks ago; Omega is now capped at $140M)

Ultimately, we are Invested in EXR to see its QLD gas asset drive a re-rate in the company’s valuation to ~$500M. This forms the basis for our Big Bet, which is as follows:

Our EXR Big Bet:

“EXR to achieve a $500M market cap through successfully advancing its Queensland gas project”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our EXR Investment Memo.

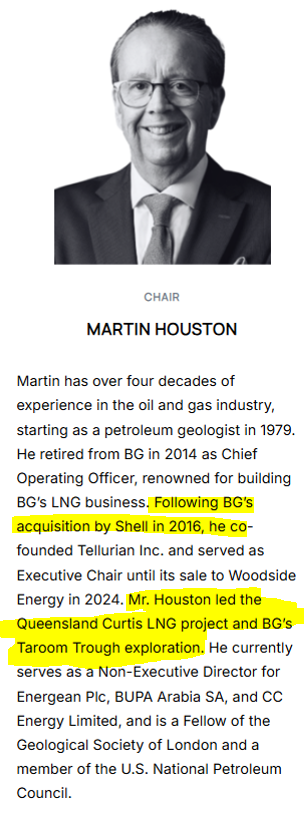

Omega and EXR’s chairman have some history...

Omega’s new chairman, and EXR’s chairman also share some history...

A few weeks ago Omega appointed Martin Houston as its new Chairman.

Houston was the former COO of BG Group - which in 2008 acquired a company called QGC for ~$5.3BN...

QGC was the company EXR’s chairman Richard Cottee built as Managing Director from a $20M capped junior all the way through to the $5.3BN takeover back in 2008.

(Source)

Eventually in 2016 the combined entity (BG Group) was acquired by supermajor Shell for US$52BN.

(Source)

Now, just under a decade later, the two chairs are active in the same region again.

AND their old friend Shell is active next door to both companies...

(Source)

Here is EXR’s chair’s background:

And here is Omega’s chair’s background:

All the region needs is some strong flow rates proven up in horizontal wells.

Whatever happens, for the next 6-9 months there will be plenty of newsflow to follow in the Taroom Trough.

EXR in a region that can tap into domestic and international gas markets

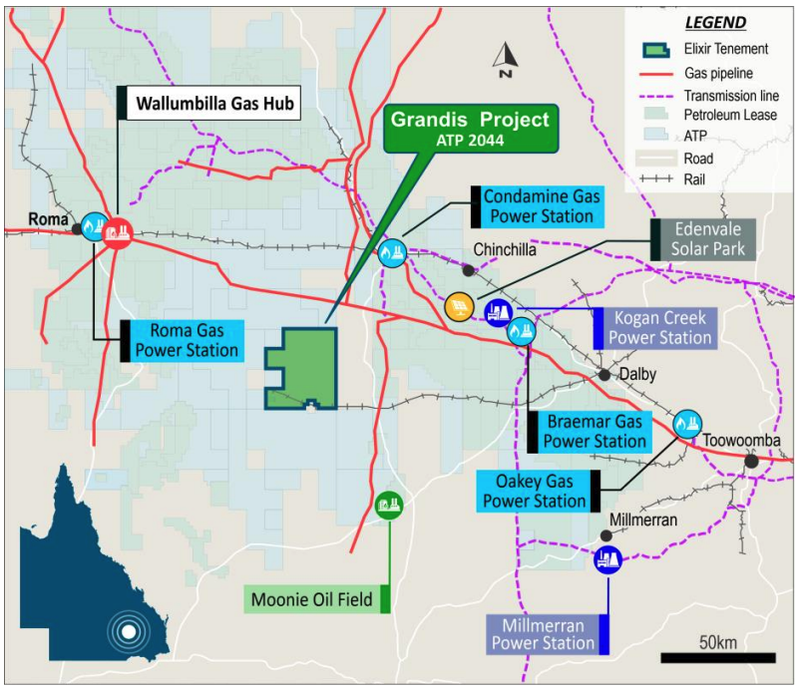

We briefly wrote about it earlier, but the big differentiator for the Taroom Trough as a whole is how easily it can be tied into existing infrastructure.

The region (if unlocked technically) is right next to already built gas pipelines, road and rail:

Most importantly, the infrastructure means any gas produced in this part of Australia can be diverted to both the domestic market & international LNG markets.

There are two major markets for this gas to sell into:

- International markets through nearby LNG Plants - there are three LNG plants in Gladstone near EXR’s project that have never operated at full capacity and could take more gas feedstock to ship to international markets.

- Domestic market (east coast of Australia) - EXR’s project sits next to the Wallumbilla Gas Hub, which distributes gas to the east coast market. The east coast of Australia is forecast to be short gas in 2028 and expected to start experiencing supply shortages beyond 2026.

EXR’s MD Neil Young gives a really good overview on the Taroom Trough in his recent interview with Crux Investor.

It’s a good listen, and the interviewer asks some solid questions:

(Source)

More on EXR’s Share Purchase Plan

We increased our Investment in EXR at the most recent placement.

That placement was done at 3.5c and came with 1:2 free listed option exercisable at 12c, with a 17 October 2026 expiry.

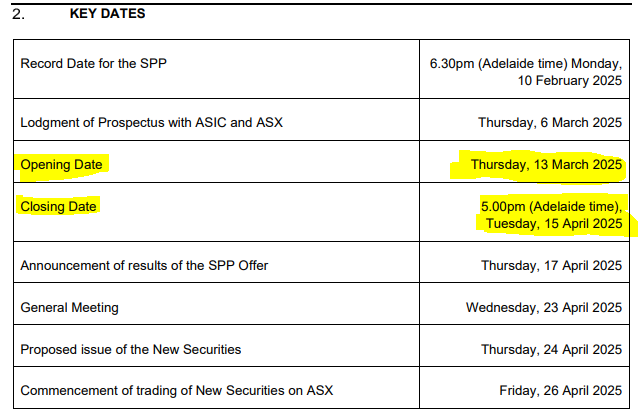

Now EXR is looking to raise up to an additional $2M via a Share Purchase Plan (SPP) on the same terms.

SPP’s are a slightly different way of raising capital, they give existing shareholders the opportunity to purchase up to $30,000 in new shares off market on the same terms as the recent priced round.

In EXR’s case, any shareholders who held shares as of the 10th of February 2025 will be able to participate.

Buying into EXR now, does not make a shareholder eligible to participate in the SPP.

We intend to participate in that offer and increase our Investment again.

EXR is currently trading at 3c which is below the 3.5c SPP price, however the SPP comes with options, and there are no brokerage fees that need to be paid.

We think that Omega’s activity over the coming weeks could see EXR begin to trade above the 3.5c SPP price, if Omega manages to deliver an above expectation flow test result.

(which of course is no guarantee, all sorts of things can go wrong with flow tests)

The EXR SPP offer opens tomorrow (13th of March) and closes on the 15th of April.

(Source)

What’s next for EXR?

🔄 News from EXR’s neighbour Omega

In the short term our focus will be on watching what happens with Omega’s flow test next door.

As mentioned earlier in today’s note, we should be getting close to some news from Omega.

Progress in the region is Objective #3 in our new EXR Investment Memo:

Objective #3: Regional progress

This objective is less specific to things EXR can control, but we think it is important for the EXR story overall. We want to see EXR’s regional peers progress their projects and prove up commercially viable flow rates across the region.

Milestones:

🔄 News from EXR’s peer Omega Oil and Gas

🔄 News from Shell

🔲 News from Santos

🔲 BONUS - New entrants into the region

Source: “What do we expect EXR to deliver?” - EXR Investment Memo 24 Feb 2025

🔄 Share Purchase Plan to raise up to $2M

What could go wrong?

In the short term we think the company’s SPP could put a bit of pressure on EXR’s share price.

Usually with SPP’s because shareholders can apply for a $30,000 allocation of shares off market, they may look to sell their current holdings (assuming the share price is above the offer price).

Usually the selling happens only if the share price is above the SPP price. In EXR’s case because the offer comes with free options we think there could be selling close to or just below the SPP too.

So if EXR’s share price pops up close to OR above the SPP, we would expect some selling to come into the stock.

The offer is set to close on the 15th of April which will be when this overhang is removed.

Funding risk

To drill its Queensland appraisal well, EXR must still secure funding, which it is now pursuing but is not always guaranteed on favourable terms.

Source: “What could go wrong” - EXR Investment Memo 24 Feb 2025

Our EXR Investment Memo

In our EXR Investment Memo, you can find the following:

- What does EXR do?

- The macro theme for EXR

- Our EXR Big Bet

- What we want to see EXR achieve

- Why we are Invested in EXR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.