EV1 releases DFS for its graphite project in Tanzania

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,453,125 EV1 shares at the time of publishing this article. The Company has been engaged by EV1 to share our commentary on the progress of our Investment in EV1 over time.

The world is racing to secure new sources of battery materials.

Graphite is half of all the material that goes into an EV battery and is the single largest battery component by weight.

Given the coming demand, 2024 is predicted to be the year the graphite market enters a long term supply shortage...

And that means higher prices for longer.

Benchmark Minerals predicts 97 new graphite mines are needed just to keep up with demand.

But mines don’t appear overnight. It takes years of work and capital to get a mine up and running.

Our graphite Investment Evolution Energy Minerals (ASX:EV1) has a graphite project that can be in production by early next year.

EV1 just released an updated DFS, and is holding an investor webinar at 11:30AM AEDT / 8:30AM AWST today to discuss it — you can register to listen here:

This timing could prove perfect given the imminent graphite shortage.

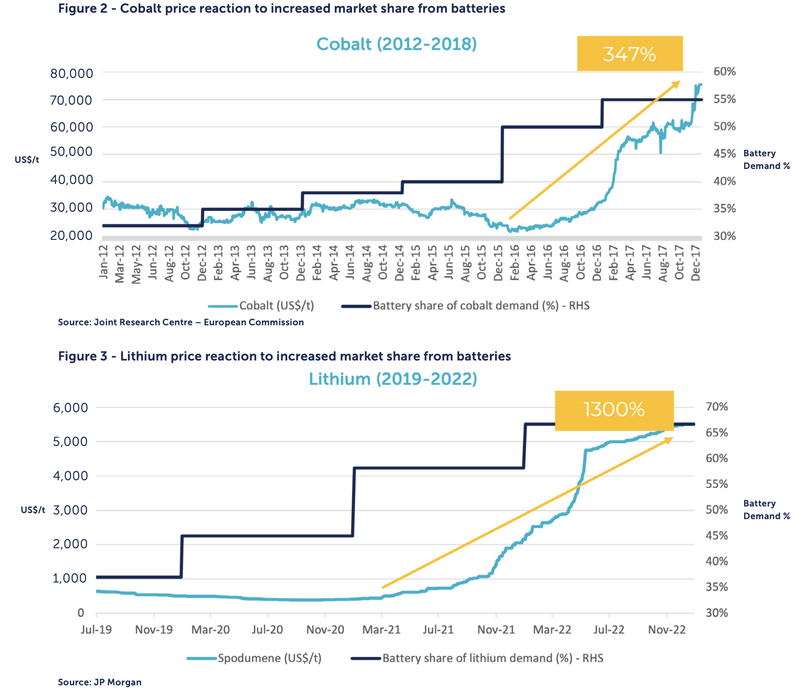

We’ve seen this happen before with another battery material - lithium. A run in lithium prices delivered big returns for lithium companies in recent years.

Consider these lithium companies that have re-rated substantially over the last three years as they get closer to production:

- Vulcan Energy Resources - now capped at $860M (one of our Investments)

- Lake Resources - capped at $730M

- Core Lithium - capped at $1.5BN

- Sayona Mining - capped at $1.9BN

Now, we think, it’s graphite’s turn.

A looming supply shortage of graphite — the other key commodity required for batteries — could deliver big returns for graphite companies, especially those with development ready, high quality projects.

Today EV1, our 2021 Wise-Owl Pick of the Year, released its updated Definitive Feasibility Study (DFS) for its Tanzanian graphite project.

This is the last step before a final investment decision is made.

The DFS, including updated Front-End Engineering Design (FEED), confirmed EV1’s Chilalo project as a standout high-margin, low-cost and development-ready graphite project.

Here are our quick takeaways from EV1’s updated DFS:

- Project NPV increased to US$338M, up from $323M in the initial 2020 DFS.

- High operating margin of US$841/t (52% operating margin) driven by its world-leading coarse graphite flake size.

- The CAPEX of US$120M is higher than the $87M estimated in the original DFS, however it remains low compared to other development-ready graphite projects - and its using up to date cost inputs that reflect a realistic higher inflationary environment.

- OPEX remains steady - even in this inflationary environment.

- DFS assumptions led by former Syrah Resources’ team - we trust in the figures accuracy given the team’s graphite industry knowledge and experience.

- Environmental improvements that reduce ESG risk.

- Project timed to come online with forecast graphite supply shortages.

Since we first invested in EV1 and it listed on the ASX in 2021, the company has been ticking off the milestones to reach a final investment decision for its Chilalo project.

Now with an updated DFS in hand, together with the formal signing of the (now agreed upon) Framework Agreement with the Tanzanian government expected this month, EV1 is in a position to secure funding for the project and move into the “construction” phase.

Financing is the next big hurdle for EV1. The DFS, FEED, and framework agreement are key requirements of financiers and mean EV1 can progress discussions with potential partners.

Financing a graphite mine has not traditionally been easy.

However there is increasing incentive to do so with Benchmark Minerals estimating that 97 new graphite mines are needed by 2035 in order to meet upcoming demand driven by batteries.

EV1 is positioning itself to be a near term profitable producer of graphite — just as a surge in demand is predicted.

Here are the five things that EV1 has going for it as its progresses financing discussions:

- High margin project: EV1 will produce higher priced coarse flake graphite, with high operating margins (US$841/tonne or 52%) at current prices.

- Low cost: Relatively low CAPEX of US$120M compared to other DFS-stage graphite peers.

- High value applications: EV1 has been working with potential customers since 2015 - running testwork and qualifications processes. EV1 is therefore confident its product is suitable for high value applications, meaning there are likely quality buyers waiting for EV1’s graphite. An example of this is the signed offtake agreement that already covers over 50% of production and 70% of forecast revenue over the project’s first 3 years.

- The EV1 team has done this before: Much of the EV1 team has previous experience in graphite development and operations — predominantly at Syrah Resources (now a $1BN+ graphite producer). This de-risks development and ensures the assumptions made in the DFS are based on real world experience.

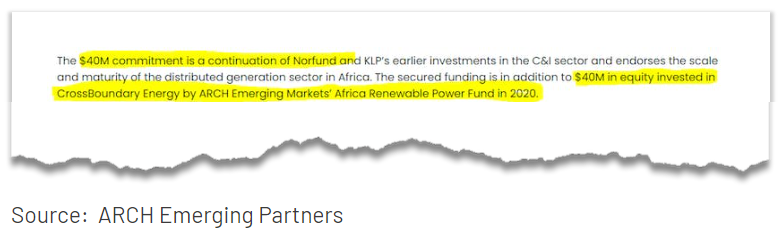

- EV1’s sustainability focus has attracted cornerstone investment from ARCH Sustainable Resources Fund, who hold 24.7% of EV1. ARCH wantsto follow their investment through to project financing. Last year ARCH was able to help secure a US$40M investment from Norwegian Sovereign Wealth Fund in another African renewable energy project. So we hope ARCH can help lead EV1 to strong funding partners.

What’s interesting is that anticipated project development coincides with a forecast surge in graphite demand for use in electric vehicle batteries.

We’ve covered at length the growing demand for battery materials, but the outlook for graphite is particularly compelling.

The graphite market is facing a deficit as demand from batteries surges to 50% of all graphite consumed. As such, Benchmark Minerals Intelligence predicts the need for 97 new graphite mines by 2035.

With a looming supply shortfall in mind, there is an immediate need to develop new flake graphite supply.

However, due to the recent and ongoing inflationary environment, to be considered development-ready by potential financiers a project must have recently released capital and operating cost updates...such as EV1’s updated DFS.

This brings us to our our Big Bet for EV1:

“EV1 will achieve first production of the world’s most sustainably produced graphite by early 2024 (including value adding processing) coinciding with the onset of a long-term supply shortage in the graphite market.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EV1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The announcement also supports our Objective #1 as outlined in our EV1 Investment Memo:

Located in south-eastern Tanzania, EV1’s Chilalo Project has a high-grade mineral resource estimate of 20.1Mt at 9.9% total graphitic carbon (TGC) for 1,991 Kt of contained graphite.

While EV1’s project has a relatively small defined deposit (to date) relative to some peers, it is the high purity and large flake size of Chilalo that sets it apart from other graphite deposits.

It's not size that matters - its quality when it comes to generating high margins from graphite.

EV1’s Updated DFS: an overview

The economic landscape has changed a lot since January 2020 when EV1’s first DFS was published.

The demand for battery materials has increased significantly in that time - which means sale prices for graphite are going up.

However, the inflationary environment — and in particular energy and fuel costs — means that project costs have increased as well.

We think that EV1 has done well to lift the project’s NPV given this inflationary environment, while modestly increasing the CAPEX of the project from the original DFS completed three years earlier.

What really stands out to us in the DFS is the high operating margin of 52%, or US$841/t — a result of the project’s coarse flake size that commands high prices that are expected to continue to rise.

We also note that EV1 has predominantly retained the flowsheet used in the previous DFS.

This is a strong vote of confidence in the technical work undertaken, including substantial variability testwork and pilot plant tests, confirming that the Chilalo project can produce a high value concentrate product.

Here are the key outcomes of the DFS published by EV1:

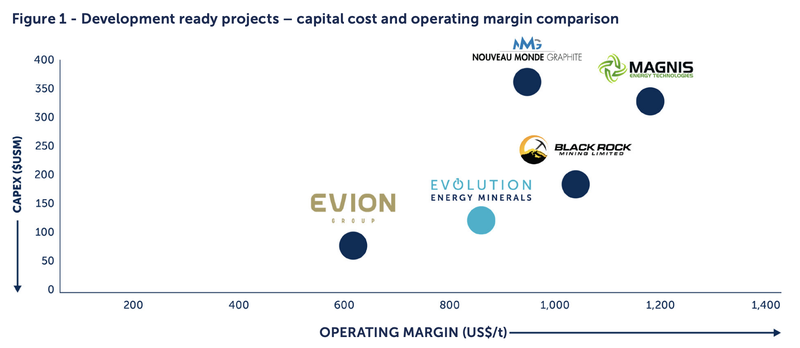

Compared to its peers, we think that EV1 has one of the lowest capital and highest operating margin development ready graphite projects, making it an attractive project for potential investors and financiers.

In addition, what is outside of the DFS are several downstream “value added” opportunities that could further enhance the overall project economics.

Why operating margins are important

High-margin, low-CAPEX projects are important in inflationary environments as the cost of operating increases. Essentially companies will need to make more with less, which can be supported by selling higher margin products.

The chart below compares the capital costs and operating margin for all development-ready graphite projects.

Operating margin is the meaningful comparison for flake graphite projects given the average sales price will vary depending on the differing products produced.

What we can take from it is that EV1 has a high-margin project with a low and financeable capital cost.

EV1 currently has a market cap of ~$51M, compared to the peers featured on this chart:

- Magnis Energy Technologies ($300M)

- Black Rock Mining ($108M)

- Nouveau Monde Graphite ($372M)

- Evion Group ($17M)

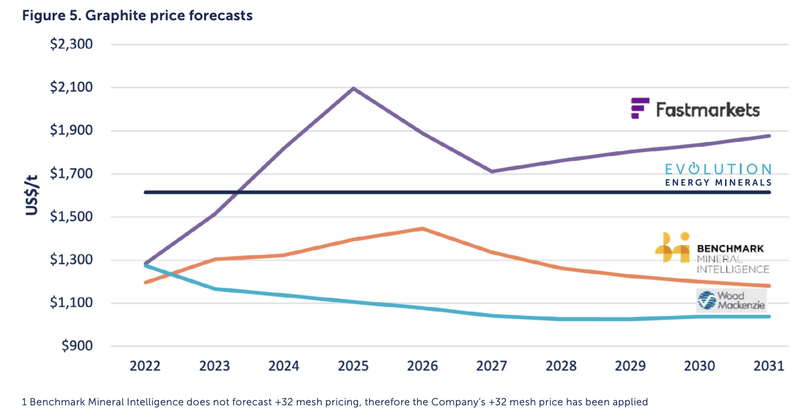

Graphite pricing

We hope EV1 can reach first production right as the graphite price is surging.

Graphite is the largest component of lithium-ion batteries, comprising over 50% of every lithium-ion battery and over 95% of a battery’s anode.

The value of EV1’s project (NPV) is sensitive to movements in the graphite price. The higher the price, the more valuable the project.

Not all graphite is created equal, however, and graphite as a product needs to be qualified and fit for purpose.

This means the better the graphite, and the more suitable, the more EV1 can sell it for — qualified graphite is needed for lithium ion batteries.

The large flake size of the graphite at EV1’s project may open the door to specialty end markets and attract associated premium pricing.

Graphite represents approximately half of a battery’s mass (some 7-10 times the amount of lithium).

As such, and as widely reported, battery demand is experiencing rapid growth — expected to grow from ~50% of the graphite market to ~70% of the market in the coming 24 months.

By comparison you can see similar inflection points for cobalt and lithium in 2016 and 2020, resulting in the lithium price gaining 1,300% and cobalt ~350% over the ensuing 24 month period.

In its updated DFS, EV1 set a price around US$1,600/t. This was based on the weighted average sales price of the different types of graphite in its deposit.

EV1 based its graphite pricing assumptions on a number of factors, including discussions with customers, its own data analysis, and external graphite analysis.

As explained in the DFS, graphite analysts face significant challenges in forecasting a graphite price for each type of graphite.

That’s because not all graphite is created equal and graphite can command higher or lower prices depending on its attributes.

Also, unlike say gold, graphite is not an exchange-traded commodity. There is no set ‘price’ for graphite nor does it trade in a transparent market.

As such, individual graphite contracts must be negotiated privately between buyers and sellers.

This makes estimating graphite prices difficult and means the underlying assumptions made when selecting a price must be tested.

We think that over the long term the demand for graphite will increase, driven by sales in electric vehicles and supply shortages from mines not coming online quickly enough.

EV1 already has a binding offtake agreement with Yichang Xincheng Graphite Co (YXGC) for over 50% of its annual graphite production and offtake discussions are progressing for its fine flake graphite.

The key, however, to EV1’s premium pricing is its downstream value adding opportunities.

End-users who purchased highly specialised graphite products don’t purchase it in concentrate form, rather they buy once it is processed and the manufacturer has made a substantial margin on the product.

EV1 intends to be the ultimate seller of this graphite product (which fetches up to US$30,000/t) and engage the processing company for a fee.

We also note that EV1 has also executed a binding term sheet with its offtake partner YXGC for the downstream processing of coarse flake concentrate into value-added graphite products.

As this is not contemplated in the DFS economics, we think it is a big opportunity for EV1 to add value to its project.

We go into more detail on the downstream opportunities in this article: Increased Investment: “Value added” Graphite for Electric Vehicles and Nuclear.

What is a DFS and why does it matter to EV1?

Click here to learn more about feasibility studies.

When developing a large-scale project such as a mine, companies will undertake feasibility studies to estimate the expected return on investment and cost of developing the project.

This is an important step that financiers and investors want to see before committing capital to construct the mine and processing facilities.

A Definitive Feasibility Study (DFS) outlines in great detail all of the plans and assumptions made by the company to come up with the headline figures including the project’s net present value, capital cost, operating cost, annual production and return on project investment.

Yet a DFS is only as good as the assumptions it is based on.

Incorporated into EV1’s updated DFS were the results of a Front-End Engineering Design (FEED) process.

The FEED is a process used by companies to ensure that a project is construction ready. It evaluates opportunities to improve plant design, optimise and update estimated capital costs, and improve efficiency.

Key deliverables of the FEED work for EV1’s project included detailed engineering, cost estimation, schedule optimisation, development of Project Execution and Operational Readiness plans, and tenders for long lead equipment items.

What’s important to note is that EV1 now has an experienced team assembled to carry this project forward with Michael Bourguignon, former project manager for construction and commissioning of Syrah Resources’ Balama operation.

Bourguignon will be invaluable in applying his years of learnings from building a graphite mine for the $1BN+ capped African graphite producer Syrah Resources.

The FEED was completed by CPC Engineering, which was also Syrah Resources’ engineering firm for its Balama Graphite Project in Mozambique.

CPC has an extensive in-house database on previous projects, scopes of work, equipment, schedules, costs and specifications, that ensures the efficient use of personnel and relevant data.

It has completed a large number of bankable feasibility studies and has a successful and proven track record in executing project design and construction developments delivered on time and within budget.

For Chilalo, a significant improvement from the FEED process was to reduce energy costs, which lowered the assumed operating expenses of the mine.

Specifically, EV1 highlighted the use of 20% solar power as a way to cut energy costs — an important cost saving considering the rising price of energy.

Another design change was in regards to the handling of waste material, or tailings.

Rather than using tailings dams, EV1 intends to implement dry-stacking of tailings — a more efficient and environmentally friendly way to dispose of waste material that reduces the risk of an environmental disaster.

These design improvements, coupled with an updated costings for the project, means EV1 is now ready for project financing and construction.

Since May 2022 the company has been working with Auramet International to help secure financing for the project.

According to EV1 “numerous parties responded with an expression of interest”.

The company’s major shareholder ARCH Sustainable Resources Fund (who owns around ~25% of the company) may also provide funding support in this next stage of the project.

We also note a deal from mid-2022 where a company that ARCH invested US$40M in got a further US$40M investment from the Norwegian Sovereign Wealth Fund.

A big part of the reason we made EV1 our 2021 Wise Owl Pick of the Year was ARCH’s substantial shareholding. Our view was that they could help introduce large financing partners to help EV1 with project financing.

There’s also the company’s binding offtake agreement with YXGC for over 50% of its annual graphite production and offtake discussions progressing for its fine flake graphite.

With the DFS and FEED now updated, and the Framework Agreement agreed upon with a formal signing ceremony expected this month, EV1 is ready to secure the funding needed to construct the project.

What’s Next for EV1?

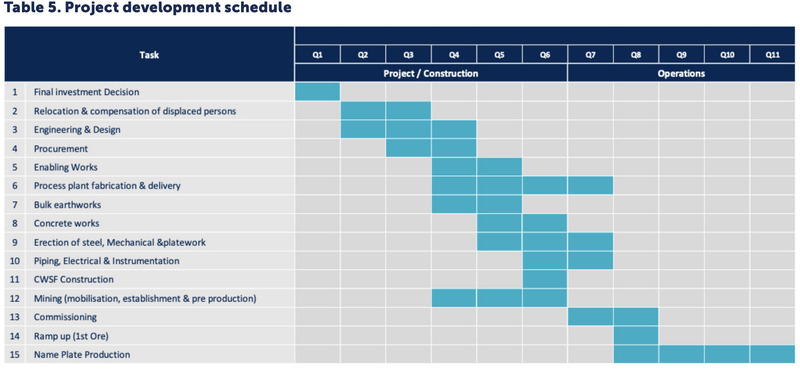

In the DFS, the company announced a project timeline, outlining the next steps of the project.

The final stage before EV1 transitions from a “Feasibility Company” to a “Development Company” is a Final Investment Decision (FID).

However, we expect the company to press on and prepare for construction while FID runs in the background, with the first stage being the execution of the Resettlement Action Plan.

Framework Agreement with the Tanzanian government 🔄

EV1 announced two weeks ago a Framework Agreement and Shareholders agreement between the company and the Tanzanian government.

EV1 expects official signing of this agreement later this month - March 2023.

We think the Framework Agreement with the government is a big catalyst for EV1 as it provides a clear regulatory pathway to production - the ultimate goal for EV1.

Drilling results 🔄

EV1 completed a RC exploration drilling program late last year that comprised 44 holes for 5,440 metres. Assay results remain pending but had been expected during the coming quarter.

This could further improve the figures in the DFS if exploration can add more near-surface material to the mine-plan, potentially reducing costs in early years, adding to the mine life, or justifying a larger build.

Note that none of the extensional drilling that was undertaken has been included in the DFS project economics.

Feasibility study on a downstream plant (bonus) 🔄

Feasibility studies on a downstream processing plant in an EV-friendly jurisdiction — a possible location in Europe or the Middle East had been mentioned by EV1.

In recent announcements, EV1 has specifically said it would look to commence a Scoping Study followed by a DFS on a downstream graphite processing plant.

Our EV1 Investment Memo

Below is our EV1 Investment Memo where you can find a short, high level summary of our reasons for Investing.

In our EV1 Investment Memo you’ll find:

- Key objectives for EV1

- Why do we continue to hold EV1

- What the key risks to our Investment thesis are

- Our Investment plan

For a high level summary of how EV1 is tracking relative to our Memo we also maintain an EV1 Progress Tracker which you can see here:

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.