EV1 Acts to Thaw US-China Battery Spat. Supply Chains Intact

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,928,612 EV1 shares at the time of publishing this article. The Company has been engaged by EV1 to share our commentary on the progress of our Investment in EV1 over time.

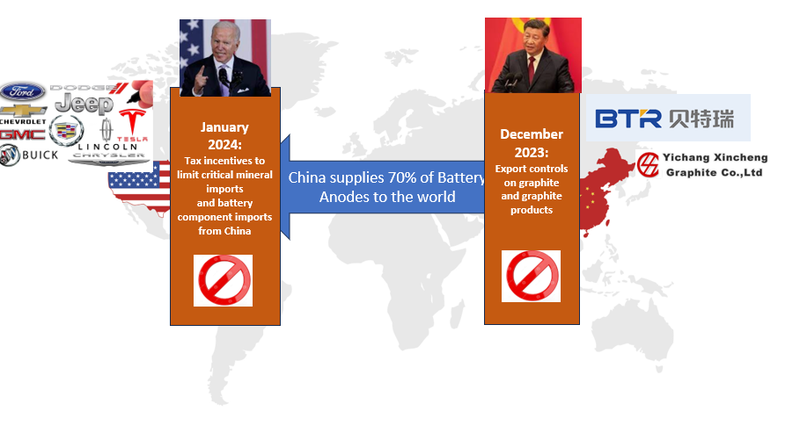

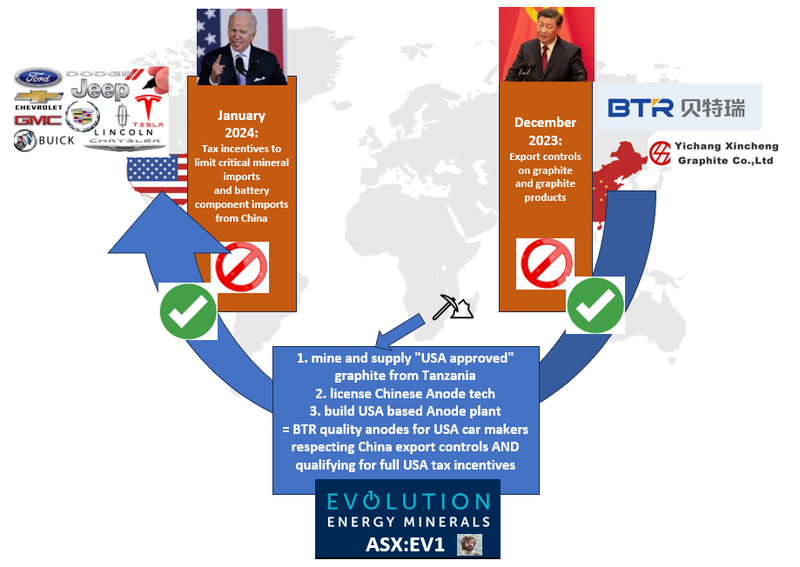

December 2023: China starts graphite export controls.

January 2024: USA tax incentives commence to limit Chinese materials into electric vehicles.

Suddenly major Chinese suppliers can’t sell to the US anymore.

US car makers can’t buy from them anymore.

...and how does the Tanzanian government and a junior ASX stock fit into solving all of this?

This $30M capped ASX company has leveraged these rising geopolitical tensions to position itself to become a key battery anode supplier to US car companies.

And with all of the above stakeholders in a “Game of Thrones” level of brinkmanship we think it would have taken some “Tyrion Lannister” levels of diplomacy, nous and deal making to have pulled this off.

Evolution Energy Minerals (ASX:EV1) started off with a sustainable, advanced stage graphite project in Tanzania.

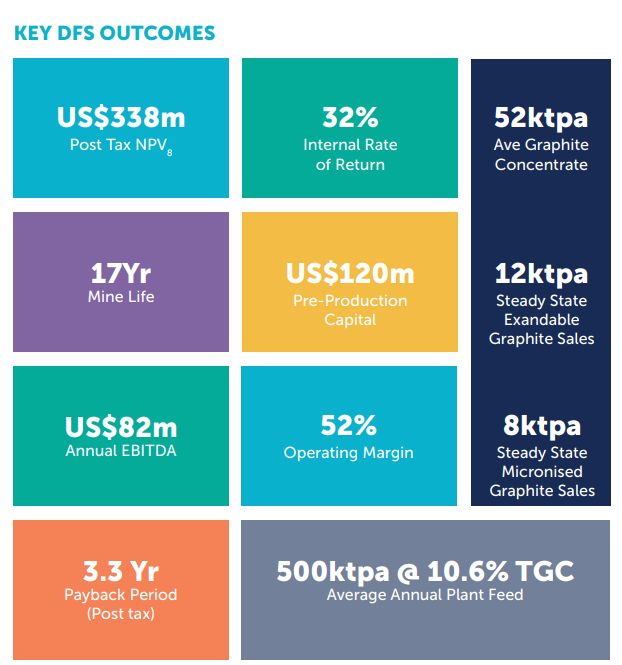

The project has a Net Present Value (NPV) of US$338M and a US$120M capital cost to develop.

So how did ASX listed graphite junior EV1 manage to cleverly insert themselves as a key player between US car makers and the world’s biggest battery anode producer against the backdrop of tit-for-tat trade policy jabs between China and the USA?

It's an extremely clever set of manoeuvres that keeps all suppliers, carmakers and geopolitical power players satisfied.

An innovative plan by EV1 that we think will soon try to be copied by many other battery materials hopefuls.

(We have been Invested in EV1 since 2021, first in at 20c then again at 36c - it last traded at ~14c.)

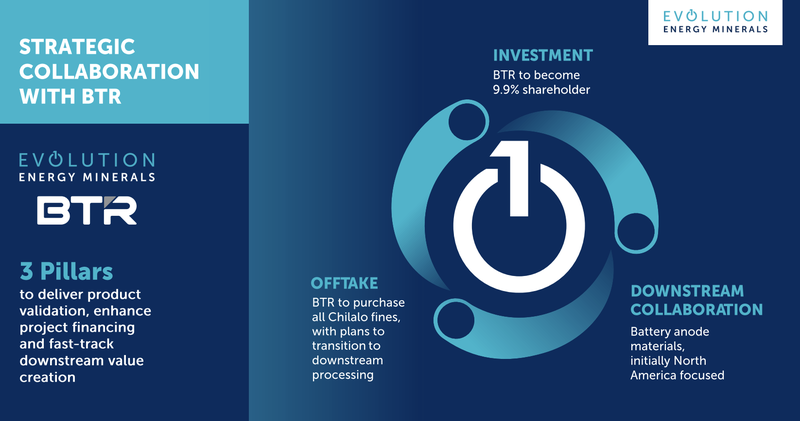

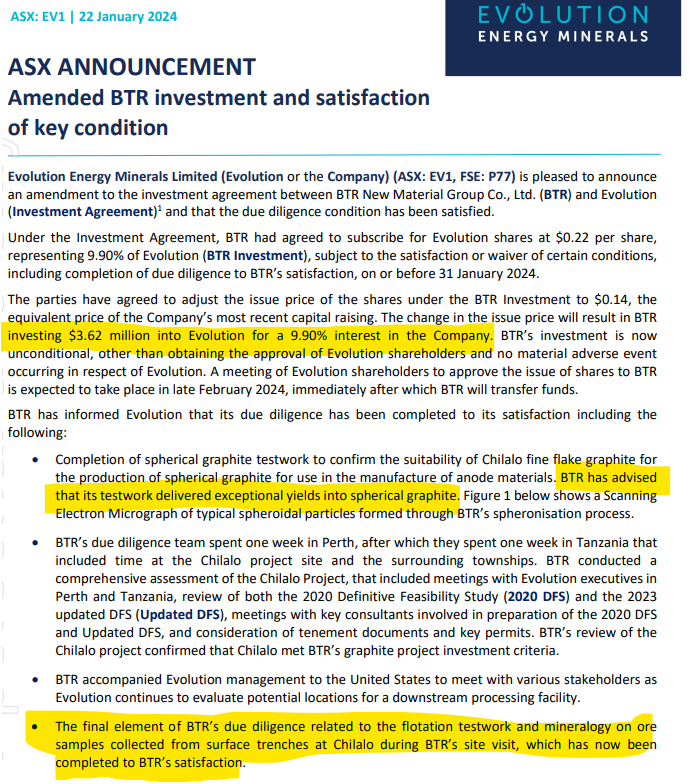

Today, EV1 announced that due diligence has been successfully completed by the world's biggest anode producer, China based BTR, for a strategic investment of ~A$3.6M into EV1 for a 9.9% stake.

(We will explain later why 9.9% is an important part of this plan.)

This deal includes an offtake agreement AND collaboration to build an battery anode plant in the USA.

(also an important part of the plan)

Before we get into more detail, here’s a 60 second summary of how EV1 leveraged recent geopolitical events to bridge the gap created by newly introduced US and Chinese trade policies.

(so let's start at the beginning...)

Quick background:

- A battery anode is 50% of an electric vehicle battery.

- Graphite makes up 95% of an electric vehicle anode.

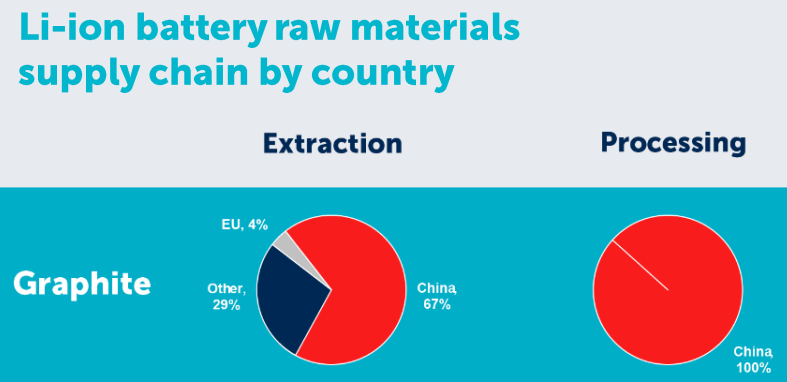

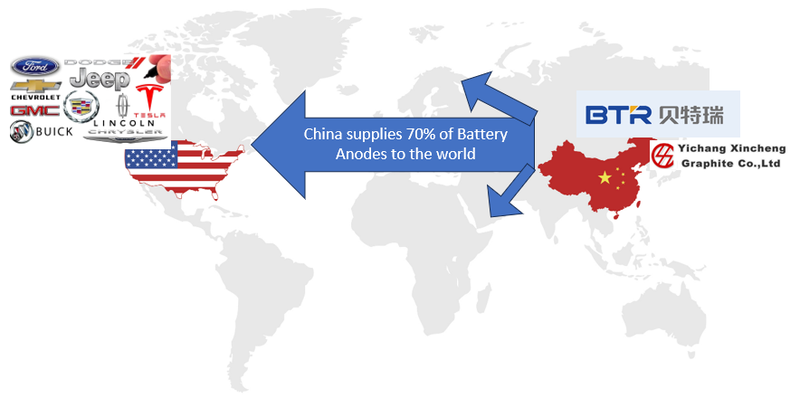

- China produces and supplies over 70% of the world's battery anodes.

- China also controls >90% of the world’s graphite processing capacity.

- China holds all the processing tech and makes the most advanced anodes used by car companies in the USA.

(Source)

For example, Chinese anode maker BTR alone is the world’s largest buyer of graphite and also the largest single supplier of graphite anodes for electric vehicle batteries.

BTR’s customers include household names like Panasonic, Samsung SDI, LG Chem, CATL, and yes, Tesla.

In recent years BTR has sold battery anodes to US car makers:

But recently US/China relations have been going downhill - there has been one export/import control after the other from both sides...

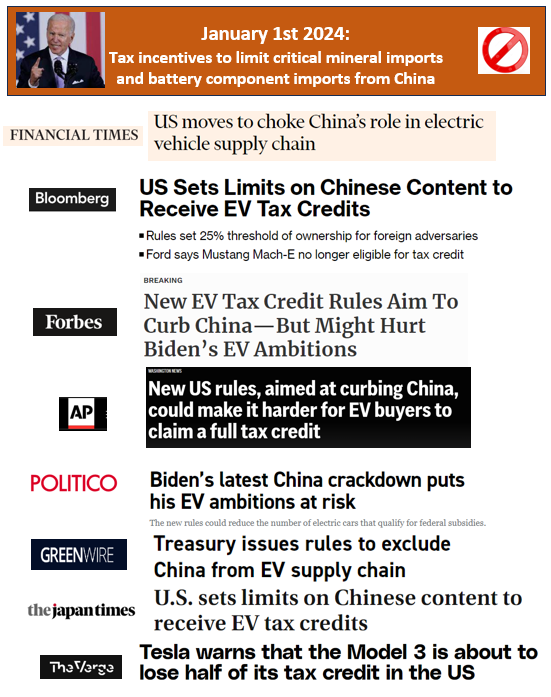

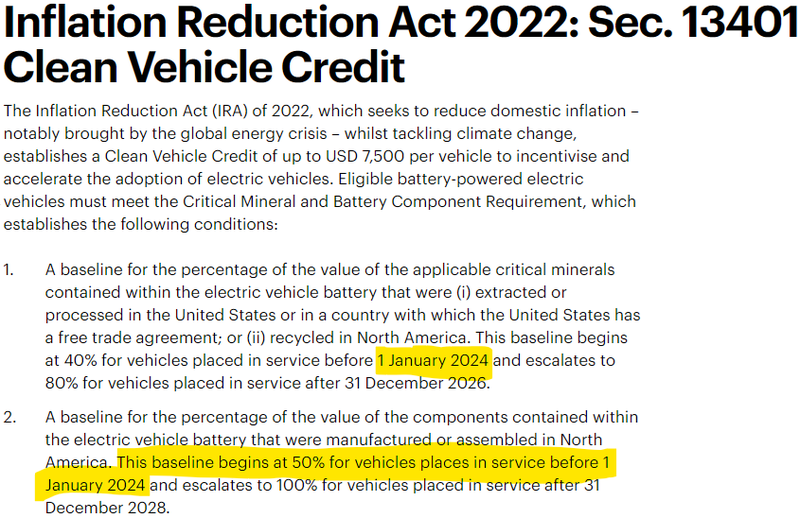

3 weeks ago, the USA’s “Inflation Reduction Act” electric vehicle tax incentives kicked in.

These new tax incentives are designed to reduce reliance on foreign critical raw materials and processing by introducing tax breaks for local or friendly supply.

(ie NOT in or from China)

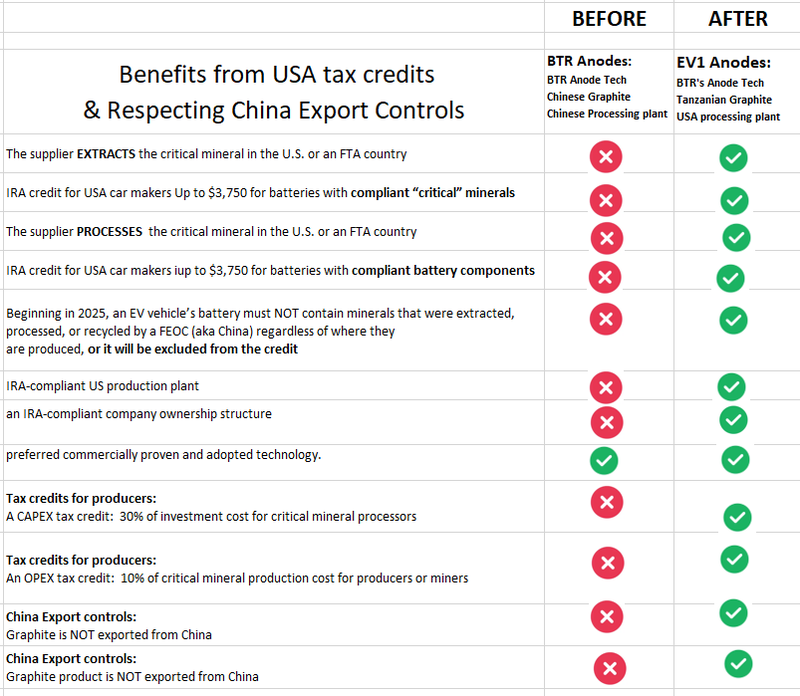

Basically this means that to qualify for an US $7,500 tax credit on an electric vehicle, materials and parts must meet the following criteria:

- The supplier extracts, processes or recycles the critical mineral in the U.S. or a US free trade agreement country

- The supplier is not deemed a Foreign Entity of Concern (FEOC)

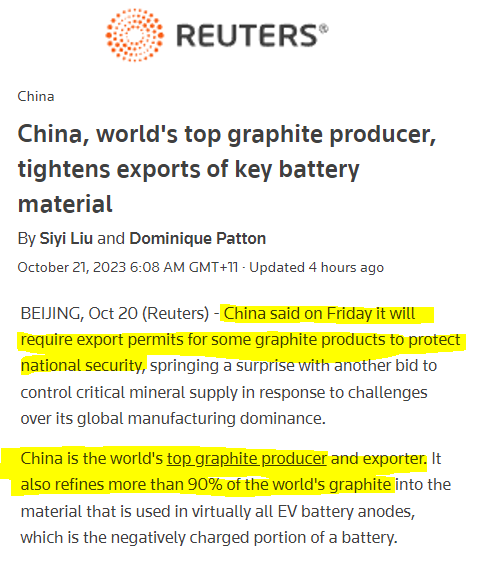

In December 2023 China announced export controls on certain graphite products:

These Chinese graphite export controls were originally announced in October 2023, kicking off positive sentiment in graphite stocks.

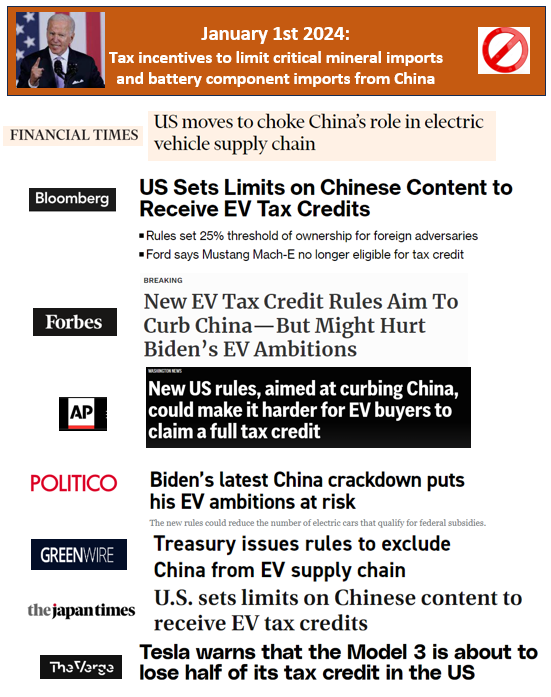

As a result - BTR, the biggest Chinese anode producer, and supplier of anodes to US car manufacturers is suddenly going to find it harder to sell in USA.

USA car companies don’t want to lose access to advanced, tried and tested, reliable BTR anodes at a reasonable price.

BTR doesn’t want to cede market share and allow competitors to catch up in technology and market share.

But China is now blocking graphite and certain graphite products from being exported.

And the USA is withholding precious tax concessions on graphite and graphite processing done in what it deems “non-friendly” countries (like China), making Chinese anodes too expensive (which is the goal).

We think today, EV1 has designed, brokered and sealed a deal that will solve the problem for Chinese Anode producer BTR and USA car manufacturers.

All while respecting rules set out in the new USA regulations AND the new Chinese export controls.

The problem:

BTR anodes are currently made using BTRs technology and know-how, in plants located in China, using Chinese graphite.

As of 2024, these products are not eligible for big tax concessions under new US rules AND are restricted from export under China export controls.

Now the solution:

ASX listed EV1 has a development stage graphite project in Tanzania.

(A USA-approved country from which to source raw materials.)

EV1 has just signed on a cornerstone investment from Chinese Anode producer BTR

(BTR holds under 10% shareholding, which qualifies for the USA tax concession.)

The deal between BTR and EV1 includes an MoU to collaborate on a downstream facility.

The downstream facility would combine EV1’s graphite with BTR’s processing technology and know-how on producing top quality anodes used and wanted by US car makers.

And guess where EV1 is planning to build a new anode manufacturing plant to combine its Tanzanian graphite and BTR’s Chinese Anode making technology?

EV1’s anode plant is going to be located in the USA.

Ticking all the boxes to qualify for the USA tax concessions AND respect Chinese graphite export controls:

So the anodes EV1 produces will tick all the boxes to fully qualify for all tax concessions under the US rules.

Because graphite is from Tanzania and processing is done in the USA, it should also satisfy China’s new export controls.

And the US car makers will be happy because they can still get access to BTR’s tried and tested battery anodes at competitive prices.

And BTR wins because they can maintain market leading position AND have a stake in EV1.

After all is said and done EV1’s anodes will solve for all of the problems BTR’s anodes are looking likely to face as follows:

EV1’s deal with BTR

Today EV1 took another step toward finalising its deal with BTR.

EV1’s three-part deal should be all wrapped up by the end of this quarter:

- $3.6M direct investment (due 31 January 2024) - BTR is investing $3.6M into EV1 at 14c per share. BTR will hold 9.9% of EV1 after the deal is done.

- Binding offtake agreement (due 31 March 2024) - BTR to purchase 100% of EV1’s fine flake graphite for 3 years with options for a further 3 years. This means that ~90% of EV1’s graphite is now under offtake agreements which is a big step toward financing its project.

- MOU to develop a downstream battery anode facility (due 31 March 2024) - Both parties to conduct initial work on a feasibility study on a plant in North America and other jurisdictions outside of China. The aim is to have an executed binding downstream agreement by 31 March 2024.

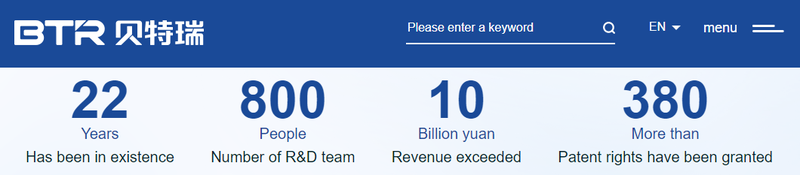

The deal is with the world’s biggest anode producer - US $3.4BN capped “BTR New Material Group Co”.

In the graphite anode market, there is no one bigger than BTR New Material Group Co.

It’s consequently the single biggest buyer of natural graphite in the world, controlling ~60% of the natural graphite anode market.

Some of BTR New Material Group Co’s customers include household names like Panasonic, Samsung SDI, LG Chem, CATL, as well as many other EV battery makers.

BTR operates ~20 graphite processing facilities across China but more recently has invested in:

- US$1.2BN to build an EV gigafactory in Morocco (source)

- US$478M to build an anode production facility in Indonesia (source)

And now it looks like they are going to back our Investment EV1.

EV1 has potentially found the cashed up big brother with deep expertise it needs to help it bring its project to reality.

EV1 already has a shovel ready graphite project in Tanzania.

The project has an NPV of US$338M and a CAPEX of US$120M to develop.

At the same time, EV1 has been working on developing a downstream facility in North America which will allow it to add more value to its products and charge higher prices.

EV1 started looking at a potential downstream facility back in late 2022 at around the same time the US IRA was announced and way before the Chinese graphite exports controls were announced.

Now with the incentives and export controls in place - the whole strategy looks to be bearing fruits for EV1 - attracting a big name partner like BTR to the company.

Adding the biggest name in natural graphite to its register is a big step for EV1 toward getting its project financed, into construction and moving downstream into the graphite processing industry.

Up until today, most of BTR’s international investments have been in the processing space.

This deal will be BTR’s first direct investment into a graphite mine and BTR is calling EV1 its “main overseas natural graphite partner”.

The deal was first announced back in August 2023 and since then BTR has been doing some pretty heavy due diligence on the project...

The deal was always conditional on BTR completing its due diligence work on EV1 but in today’s announcement we got an idea of just how extensive that due dilligence was.

In the announcement EV1 said the “The final element of BTR’s due diligence related to the flotation testwork and mineralogy on ore samples collected from surface trenches at Chilalo during BTR’s site visit, which has now been completed to BTR’s satisfaction”.

To us, this says that BTR were serious about checking whether or not EV1 is going to be able to do exactly what its DFS says it will - deliver high quality graphite to BTR and to any downstream plant the two develop together.

Going down to this level of detail is a pretty big signal of commitment to us...

About EV1’s graphite project?

We originally invested in EV1 back in November 2021 at 20c in the IPO, then again at 32c in August 2022 because we like the management, project and believe graphite will have a “lithium-like” run as the electric vehicle market takes off.

We’ve been Invested in EV1 since - we made it our Pick of the Year for our long-term Wise-Owl Portfolio because we believe that it could become an important player in the graphite market for many years to come.

Today’s deal with BTR makes that a real possibility - in large part because of some huge geopolitical forces at play in the battery materials market.

EV1’s project is a shovel ready, DFS level project with a:

- Project Net Present Value (NPV) of US$338M.

- EV1 will be producing coarse flake graphite in addition to its fines. The coarse flake sells for a premium to fines so EV1 will be receiving more revenue for every tonne of graphite produced relative to other producers who are producing a single product.

- Capital cost of US$120M to get the project into production.

- DFS assumptions led by former Syrah Resources’ team - we trust in the figures accuracy given the team’s graphite industry knowledge and experience.

- Project timed to come online with forecast graphite supply shortages.

Since we first invested in EV1 and it listed on the ASX in 2021, the company has been ticking off the milestones to reach a final investment decision for its Chilalo project.

Over the last ~3 years the company has nearly ticked off every single milestone in our initial Investment Memo, which hoped to see the company reach Final Investment Decision (FID):

- Binding offtake agreement with YXGC for 30,000tpa of “coarse flake graphite” for three years (around 50% of production) (Read: EV1 Signs Binding Graphite Offtake, Eyes Downstream Joint Venture for EU Market)

- Completed Front End Engineering and Design with CPC Engineering (same group that did major graphite producer Syrah’s project) (Read: EV1 Key Engineering Appointment - Following the Syrah Playbook)

- Proved that its graphite is suitable for EV batteries (Read: Increased Investment: “Value added” Graphite for Electric Vehicles and Nuclear)

- JV Agreement with YXGC to develop “value added” downstream graphite processing (Read: EV1 Locks in Binding Terms for Downstream Graphite JV)

- Extended existing graphite resource with two shallow high-grade graphite discoveries (Read: EV1 Begins Drilling - Targeting More Shallow High Grade Graphite and EV1 makes its second graphite discovery for the year)

- Updated DFS on graphite mine project in Tanzania (Read: EV1 releases DFS for its graphite project in Tanzania)

- Framework agreement signed with Tanzanian Government (Read: EV1 signs Framework Agreement for graphite mine in Tanzania)

- BTR Offtake & Cornerstone Investment announced (Read: EV1 signs with world’s biggest anode producer - investment, offtake and MoU for downstream)

Now with an updated DFS in hand, a Framework Agreement signed with the Tanzanian government completed in April 2024 (more on this later), EV1 is in a position to secure funding for the project and move into the “construction” phase.

Financing is the next big hurdle for EV1.

The DFS, FEED, and framework agreement are key requirements of financiers and mean EV1 can progress discussions with potential partners.

Financing a graphite mine has not traditionally been easy.

However there is increasing incentive to do so with Benchmark Minerals estimating that 97 new graphite mines are needed by 2035 in order to meet upcoming demand driven by batteries.

This was BEFORE Chinese graphite export controls came into play...

Here are the five things that EV1 has going for it as its progresses financing discussions:

- High margin project: EV1 will be producing coarse flake graphite in addition to its fines. The coarse flake sells for a premium to fines so EV1 will be receiving more revenue for every tonne of graphite produced relative to other producers who are producing a single product.

- Low cost: Relatively low CAPEX of US$120M compared to other DFS-stage graphite peers.

- High value applications: EV1 has been working with potential customers since 2015 - running testwork and qualifications processes. EV1's offtake agreements with two of the biggest names in graphite (BTR and YXGC) are testament to this.

- The EV1 team has done this before: Much of the EV1 team has previous experience in graphite development and operations — predominantly at Syrah Resources (previously a $1BN+ graphite producer). This de-risks development and ensures the assumptions made in the DFS are based on real world experience.

- Pressure to develop supply chains Ex-China - US IRA incentives kicked in on the 1st of January 2024 and the Chinese recently announced graphite export bans. Both macro events add to pressure all around the world to develop a graphite supply chain outside of China.

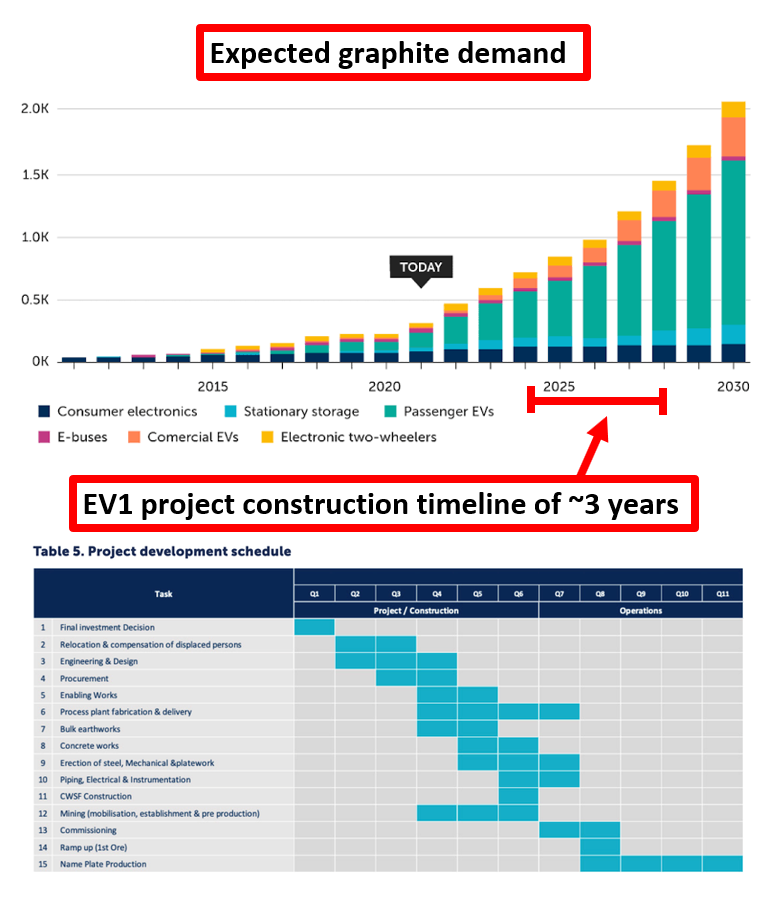

What’s interesting is that anticipated project development coincides with a forecast surge in graphite demand for use in electric vehicle batteries.

We’ve covered at length the growing demand for battery materials, but the outlook for graphite is particularly compelling.

With a looming supply shortfall in mind, there is an immediate need to develop new flake graphite supply

Located in south-eastern Tanzania, EV1’s Chilalo Project has a high-grade mineral resource estimate of 20.1Mt at 9.9% total graphitic carbon (TGC) for 1,991 Kt of contained graphite.

While EV1’s project has a relatively small defined deposit (to date) relative to some peers, it is the high purity and large flake size of its project that sets it apart from other graphite deposits.

We see the BTR deal with EV1 as confirmation of the quality of EV1’s deposit, especially considering all of the detailed due diligence on the graphite done by BTR.

It's not size that matters - its quality when it comes to generating high margins from graphite.

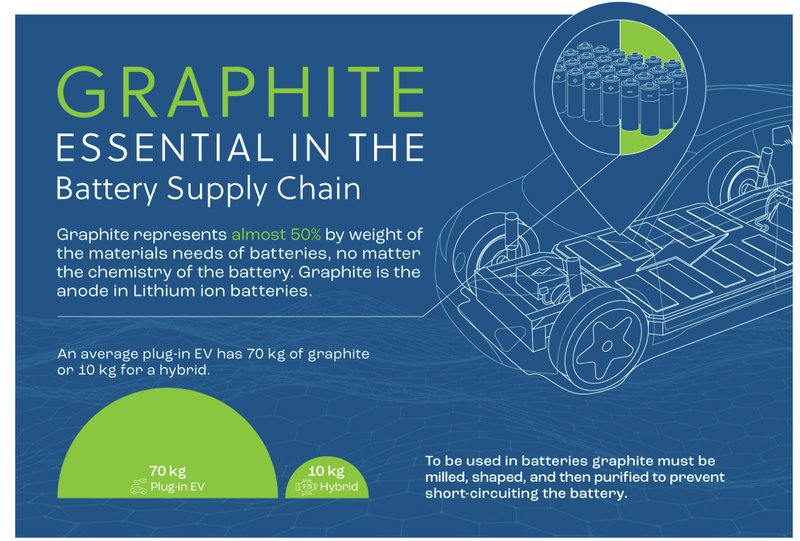

Graphite is used more than lithium in batteries

We think that 2024 could be the start of a multi-year graphite boom in large part because graphite is one of the most important inputs in an EV battery.

We have been calling a graphite run for quite a while now... it finally looks like it started kicking off back in October when all the Chinese graphite export controls were announced.

Graphite makes up ~50% of the raw materials in every lithium-ion battery and over 95% of every battery anode, one of two main parts of a lithium ion battery.

The average EV has some 70kgs of graphite in it while only having 8kgs of lithium - the material that makes up the cathode, the other main part of a lithium ion battery.

Lithium future production sources and mine development projects are scattered around the world - the geography of the lithium supply chain is diversifying very quickly:

(Source)

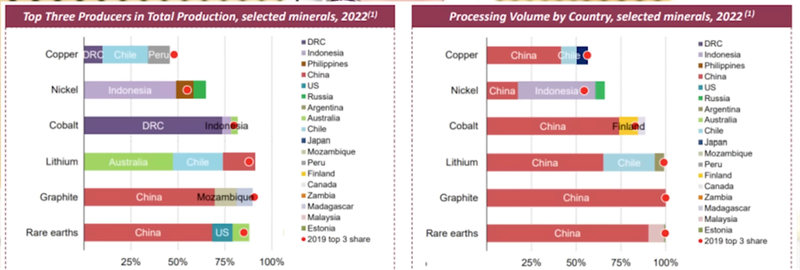

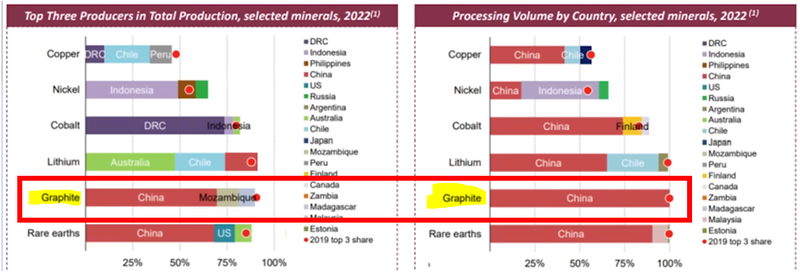

Graphite and graphite processing, on the other hand, is heavily concentrated in China.

Graphite processing and production is concentrated in China

Roughly 70% of graphite mining and >90% of graphite processing is done in China:

(Source)

When it comes to the graphite market - there simply isn't any supply available in any commercial quantity ex-China...

So any scenario where Chinese supply to the rest of the world is threatened there is a serious risk of a REALLY BIG shortage of graphite in the global supply chain.

Adding fuel to that potential risk is a response by China to the US IRA incentives...

China recently put in export controls on graphite

In October 2023, the Chinese government announced export controls on certain graphite products:

(Source)

When the export controls were announced, we said the following in our weekend edition:

“Diversity of supply overnight has become a problem with a serious sense of urgency...

Syrah Resources (which was deeply out of favour after it paused production at its graphite project) is up ~80% since the export controls were announced.

Our view is that the world needs to invest in more ex-China graphite supply to diversify global supply chains.

We think projects with size/scale & close to development will be the ultimate winners.”

Companies like EV1.

Then two months later, what we think to be the most important part of the US Inflation Reduction Act kicked in...

The most important part of the US IRA’s kicked in 1st Jan 2024

This is the key part of the US Inflation Reduction Act (IRA), which promises to entirely reshape US-China relations with regard to the battery materials supply chain.

As of 1 Jan 2024 US$7,500 in incentives became available for cars that met the IRA guidelines on where their critical raw materials are sourced from.

40% of critical raw materials from US or friendly countries after 1 Jan 2024 rising to 80% by 31 December 2026.

Any cars that don't meet those guidelines, don't qualify for the incentives.

At a very high level, we think that the incentives coming into play were the gun to start a two year race to secure critical raw materials either from inside the US or from somewhere with a free-trade agreement with the US....

Like Tanzania...

(Source)

And we think EV1 stands to benefit as the major graphite players move quickly to establish a beachhead in the US to ensure IRA compliance AND ensure its products are still the go to products for the US EV machine.

Why?

Because EV1’s project is in Tanzania (a free-trade listed country with the US) and EV1 is looking to build a plant in North America...

Rush to now secure downstream + mine production from neutral/pro-West sources

Tanzania is a Western leaning country, and geographically speaking, sits in between China and the US in the graphite supply chain.

Both the US EV makers, and Chinese anode/graphite companies want to find a solution that works, is IRA compliant, and respects Chinese graphite export controls so that the EV makers get their anodes and Chinese graphite companies can sell their products.

This is where EV1 comes in.

Its product will be extracted outside of China (tick for Chinese export controls) and processed somewhere in North America (Tick for the US IRA EV tax credits) under the terms of the EV1 deal announced today.

This is what is referred to as “downstream processing”.

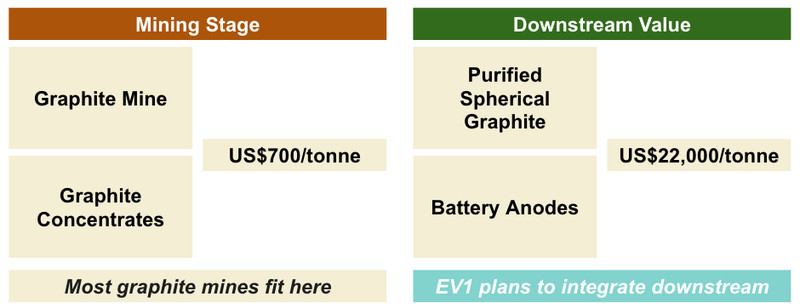

Namely, EV1 can either sell the graphite directly to consumers or value-add the product for a larger margin using downstream processing.

We think downstream processing is what makes this all work.

Again, here’s an image showing how this would all work:

EV1’s mine is ready to be financed and is making progress on a downstream facility

After the deal with BTR closes EV1 will be in a strong position to secure all of the financing needed to start construction on its mine.

When it comes to financing it really is all about whether or not a lender sees a path to getting repaid.

Financiers want as many assurances as possible that they will get their money (and their interest) back.

So a project’s economics HAVE to stack up.

EV1 completed an updated Definitive Feasibility Study, which lays out all the economics of what would be a profitable mine, even with inflation and the lower graphite prices at the time the DFS was published:

(Source)

To understand how profitable this mine could be, the “Post Tax Payback Period” in which the mine would have paid for itself is marked out as 3.3 years.

As a rough approximation, imagine buying a business and having the loan to acquire the business paid off in just three years...and, for the next ~14 years, making nothing but profit.

It's also worth keeping in mind that the DFS doesn’t include EV1’s downstream plans.

EV1 is also working on feasibility studies for a downstream processing plant in North America.

The plant once developed would take EV1’s graphite, work it up into “Coated Spherical Purified Graphite” which EV1 could then sell for multiples of raw graphite.

Again... EV1’s US$338M NPV EXCLUDES all of this...

What does the Tanzanian government think of all this?

EV1’s product is “shovel ready” after the Government of Tanzania approved a Framework Agreement back in April 2023, which provides regulatory certainty.

With the framework agreement signed, a major checkbox has been ticked for potential financiers as EV1 has established security of tenure over the project.

Below is a photo from the signing ceremony where Managing Director Phil Hoskins and Executive director Michael Bourguignon are before the President of Tanzania, Her Excellency Samia Suluhu Hassan:

There is a video of the full signing ceremony on Youtube - here a couple of our favourite screenshots:

At a very high level, EV1’s Framework Agreement is a government sanctioned document that provides certainty of tenure and outlines all rights/responsibilities for project owners inside Tanzania.

Think of it as like a mining permit - it gives EV1 the all-clear to develop its graphite mine and sets out the terms and rules for making decisions about the mine.

Most importantly, it provides EV1 (and potential project financiers) the certainty of tenure from the Tanzanian government.

EV1 mine unique - coarse flake & fines strategy

Within natural graphite (as opposed to synthetic) there are two main types of graphite products that will be produced from EV1’s prospective mine, “coarse flake '' and “fines”.

We think EV1 has a great mix of potential upside from both products.

At the moment ~90% of EV1’s graphite is under offtake agreements.

100% of EV1’s fines will go to BTR for battery anodes for at least the first 3 years of the mine's production to enable EV1s US downstream anode strategy.

EV1 has also executed a binding term sheet with its other China based offtake partner Yichang Xincheng Graphite Co (YXGC) for the downstream processing of its coarse flake graphite into value-added products:

YXGC is a global leader in the manufacture of expandable graphite and associated high-value graphite products, so this is another excellent string to EV1’s bow.

Particularly in light of some of the margins that could be available on these value-added graphite products...

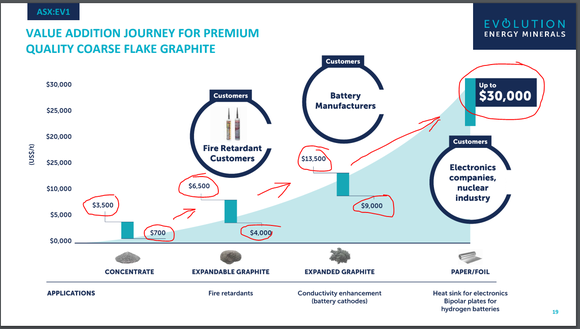

These include:

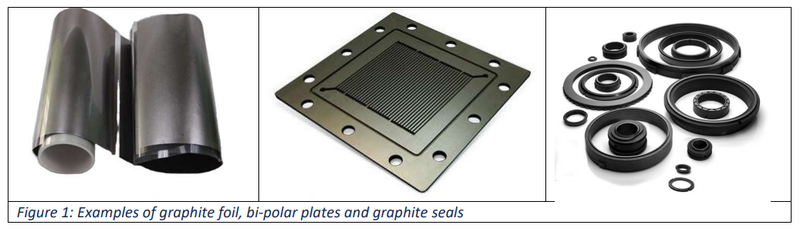

- Expandable graphite – Typically sold directly to Western fire retardant customers (up to US$6,500/t)

- Expanded graphite – Typically sold to battery manufacturers as a conductivity enhancement on the cathode side of the battery (up to US$13,000/t);

- Graphite foil:

- Typically sold to electronic device producers for use as a heat sink (up to US$30,000/t)

- Typically sold to hydrogen battery manufacturers for use in the bipolar plates housing the cathode and anode in hydrogen batteries

- AND - purified graphite for nuclear applications: EV1, achieved thermal purification of its graphite to 99.9995% Carbon - an extremely pure product that fetches US$30,000 per tonne. One type of new Small Modular Reactor (SMR) may need A LOT of this graphite - up to 60,000 tonnes of it as each 300 tonnes of graphite initially and 60-100 tonnes per year to operate.

End-users who purchase highly specialised graphite products don’t purchase it in concentrate form, rather they buy once it is processed and the manufacturer has made a substantial margin on the product.

EV1 intends to sell these products which fetch up to US$30,000/t) via a JV with another huge Chinese graphite company.

EV1 already has a binding offtake agreement with Yichang Xincheng Graphite Co (YXGC) for over 50% of its annual graphite production over the first three years and offtake discussions are progressing for its fine flake graphite.

These are lower-margin upstream products to get the ball rolling on EV1’s mine project over the first three years.

However the further downstream the company goes along the supply chain the better the economics.

It’s important to note that its current project economics don’t include profits from downstream “value add” products, so any development here is pure upside for the company.

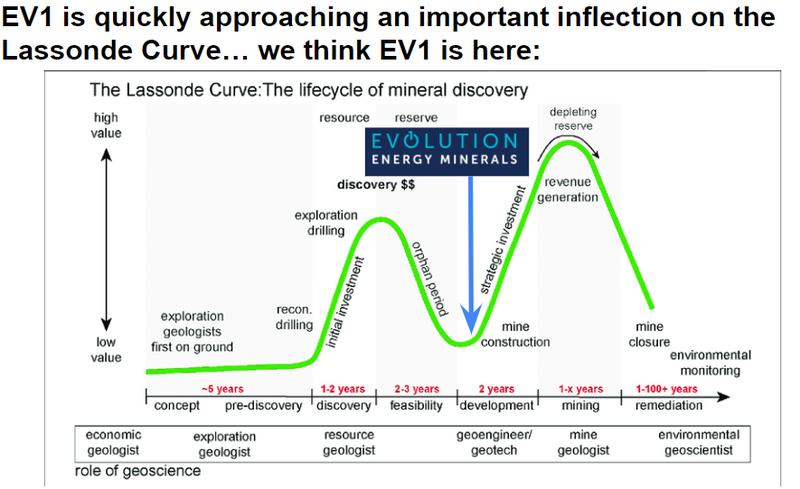

Lassonde curve - where EV1 sits right now

Every serious mining investor has heard of the Lassonde Curve.

It is a basic depiction of how the value of companies change as they go through the different phases that constitute a mining company.

From exploration all the way through to mine closure.

One thing the curve highlights is that often, the best times to be invested in a mining company is at the exploration stage (just before a discovery is made) OR right before the project starts getting into construction.

A large part of the way we Invest is inspired by the Lassonde Curve and we try to get in at both those points before looking to de-risk our positions in the mine discovery stage & the revenue generating stage when the value of the projects are highest.

Right now, EV1 is right at the bottom of the “development stage” and has just had its first strategic Investment signed with BTR.

Will graphite prices improve in 2024? And what’s the difference between natural and synthetic graphite?

Graphite sentiment looks to have improved since the Chinese export controls were announced in October 2023, after graphite prices were a bit limp throughout 2022 and most of 2023 AND sentiment across the sector was at rock bottom.

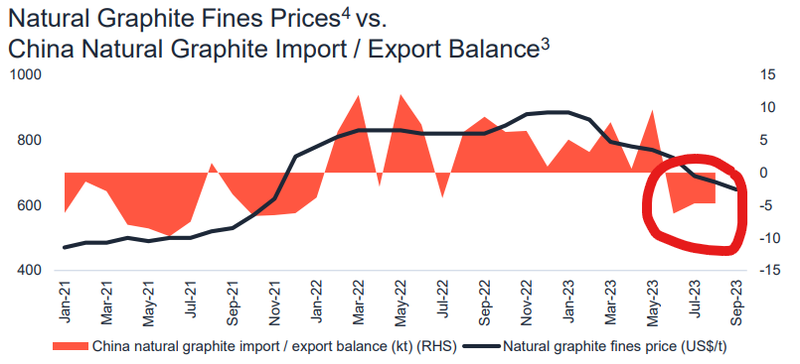

We think that graphite prices could eventually rebound strongly, particularly in light of the fact that China has recently become a net importer of natural graphite during a period of low prices - the first time that this has happened for a sustained period in the last 3 years:

(Source)

To understand the significance of this - here’s a little primer on the different types of graphite.

There’s two types of graphite, natural and synthetic or lab made graphite.

The primary factors for the slowdown:

- Graphite prices down for the year - Low energy prices made synthetic (lab produced) graphite out of China more competitive versus natural (mined) graphite.

- EV demand lower for the year - demand for electric vehicles was lower in the first half of the year because of temporary changes to Chinese EV subsidies.

So, the graphite market was hit with a perfect storm of lower demand for graphite from battery anode producers and cheaper supply from synthetic graphite producers in China.

Things looked dicey for the first three quarters of 2023, with graphite prices down and sentiment in the sector at rock bottom.

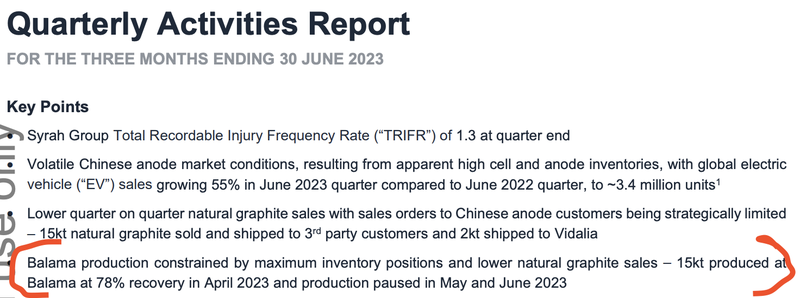

Sentiment and prices were so low that natural graphite producer, Syrah Resources, stopped production at its project in Mozambique, choosing to stockpile graphite instead of selling it into the market.

Syrah owns the world's biggest mine OUTSIDE of China, which is a good indicator of strength/weakness in the graphite market.

The overwhelming narrative in the market was that the world couldn't compete with low cost synthetic graphite out of China...

And then major investment bank UBS put out a note:

(Source)

Graphite stocks started responding, with most up 10-20% on the first day of trading after that news.

Since the news came out, Syrah Resources which is seen as the ASX’s indicator for health in the graphite sector added a peak of ~$358M to its market cap and was up over ~120%.

In the weeks before the news Syrah’s share price was ~42c (a 52 week low), it peaked around ~95c.

Then the graphite export controls were announced, later in October 2023.

Since then Syrah remains out of action, with the mine in Mozambique no longer being in operation.

Why is the outlook for graphite much stronger now?

It boils down to the same reasons that led the market lower in the first three quarters of this year.

- Energy prices have gone up A LOT - oil prices remain high and natural gas prices are also rallying. Tensions in the Middle East are boiling over and the Russia/Ukraine conflict is ongoing. Overall, the pressure is on energy prices to go higher and stay higher...

- A potential Chinese export ban puts ~80% of the market at risk - China produces ~70% of the world’s graphite and controls almost 100% of graphite processing. And without Chinese graphite anodes, the whole EV battery supply chain is at risk.

- Alternative supply isn't available - Outside of Syrah’s mine in Mozambique, there are no major mines that can be put into production to diversify supply IF China curbs exports in any major way.

Enter EV1, which we think will be the next new graphite mine into production outside of China.

EV1 has the right team to capitalise

Managing Director - Phil Hoskins

Phil has been responsible for the development of the Chilalo graphite project since 2014.

We like to see founders and people who have spent a significant amount of time on a project attached in senior and executive roles at a company for a couple simple reasons - for one, they know the project’s dynamics intimately, and for a second reason - they are usually deeply personally invested in the project’s success.

Phil also has extensive finance and commercial experience from exploration through to operations, in Africa and Australia.

On top of that, Phil is very familiar with the Chinese anode industry - and has travelled extensively throughout the country to meet with companies like BTR and YXGC.

Chief Operating Officer: Michael Bourguignon

Amongst a number of other successfully delivered projects, Michael was responsible for managing the construction of Syrah Resources’ Balama graphite project in Mozambique.

Older investors may remember Syrah Resources from 2016, when it's share price hit an all time high of $5.75, from ~10c 2011. Michael was a key part of the project’s development.

Having someone of Michael’s quality and experience supporting the board bodes very well for EV1, indeed Michael is the only person to have built a graphite project outside of China in the last ten years.

What are the risks to our EV1 Investment?

Sovereign Risk

Any Tanzania sovereign risk flare ups could spook investors and dampen share price.

Commodity Risk

Graphite prices could fall making the project harder to fund or uneconomical.

Financing Risk

Requires ~US$120M to develop the project, which could be difficult to secure if graphite market softens.

Delay risk

If EV1 enters a long period without newsflow, this could hurt the share price.

Deal risk

There is a chance EV1 is unable to turn the downstream MoU into a binding agreement, or other elements of its downstream strategy don’t work out. Alternatively, BTR’s investment still requires sign off from Chinese authorities.

Market risk

There is always a chance that the market sells off, or sells off graphite companies further, hurting EV1s ability to secure capital.

Regulatory risk

EV1s current strategy depends heavily on both US and China regulatory conditions - new leadership (for example a Trump presidency starting in 2024) could alter the dynamics at play. Regulatory conditions are not static and are subject to change.

What’s next for EV1?

BTR deal completion 🔄

- $3.6M direct investment (due 31 January 2024)

- Binding offtake agreement (due 31 March 2024)

- MOU to develop a downstream battery anode facility (due 31 March 2024)

Final Investment Decision (FID) 🔄

The next stage for EV1 is a Final Investment Decision (FID).

An FID is a firm commitment from a company to proceed with developing a project.

Sometimes it is declared after all the project financing is worked out, and sometimes it is done well in advance of financing.

In EV1’s case we expect the company to press on with other development items until a FID is officially declared - especially given the project CAPEX is relatively low at US$120M.

As conditions of BTR’s offtake the downstream agreement and FID must be completed by 31 March 2024.

BONUS: Feasibility study on a downstream plant 🔄

EV1 has previously flagged that it is completing a feasibility study on a potential downstream processing plant in an EV-friendly jurisdiction.

EV1 has specifically said it would look to commence a Scoping Study followed by a DFS on a downstream graphite processing plant.

At this stage, we don't know when this will be delivered and so if the news did drop it would be a pleasant surprise for us.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.