EV1 signs with world’s biggest anode producer - investment, offtake and MoU for downstream

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,125,000 EV1 shares at the time of publishing this article. The Company has been engaged by EV1 to share our commentary on the progress of our Investment in EV1 over time.

Our graphite Investment Evolution Energy Minerals (ASX:EV1) has just signed a three part deal with the world’s biggest battery anode producer.

The deal includes:

- $4.9M investment for 9.9% ownership of EV1 (at a premium to the last traded price);

- a binding offtake agreement; AND

- an MoU to develop a downstream battery anode facility.

The direct investment close date is 31 October 2023 and the offtake/downstream MOU needs to be signed before the 31 March 2024 contingent on certain conditions being met.

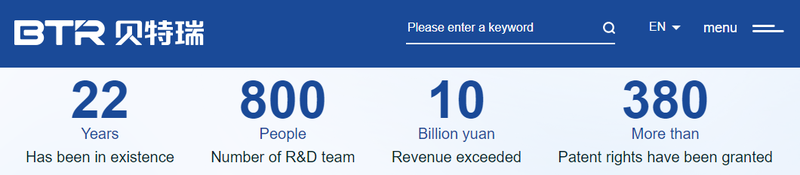

The deal is with the world’s biggest anode producer - US $3.4BN capped “BTR New Material Group Co”.

In the graphite anode market, there is no one bigger than BTR New Material Group Co.

It’s consequently the single biggest buyer of natural graphite in the world, controlling ~60% of the natural graphite anode market.

Some of BTR New Material Group Co’s customers include household names like Panasonic, Samsung SDI, LG Chem, CATL, as well as many other EV battery makers.

BTR operates ~20 graphite processing facilities across China but more recently has invested:

- US$1.2BN to build an EV gigafactory in Morocco (source)

- US$478M to build an anode production facility in Indonesia (source)

And now it looks like they are going to back our Investment EV1.

EV1 has potentially found the cashed up big brother with deep expertise it needs to help it bring its project to reality.

EV1 already has a shovel ready graphite project in Tanzania. The project has an NPV of US$338M and a US$120M capital cost to develop.

At the same time, EV1 is also looking at developing a downstream facility in North America which will allow it to add more value to its products and charge higher prices.

Today’s deal transforms EV1 by adding the biggest name in natural graphite to its register - a big step toward getting its project financed, into construction and moving downstream in the graphite processing industry.

Up until today, most of BTR’s international investments have been in the processing space.

Today marks BTR’s first direct investment into a graphite project developer and BTR is calling EV1 its “main overseas natural graphite partner”.

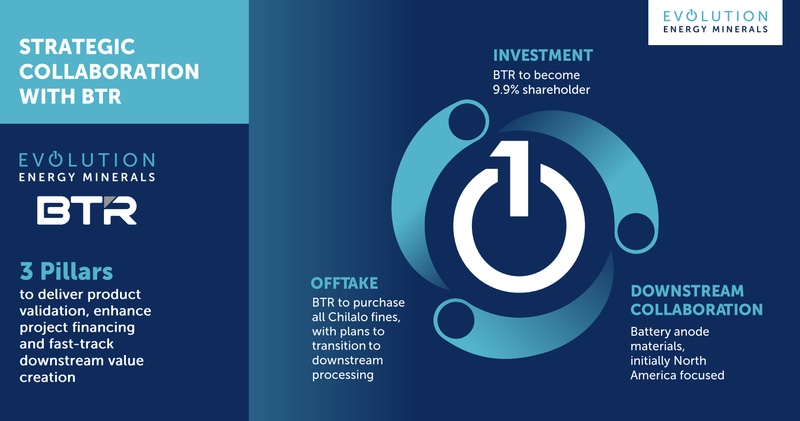

The deal between EV1 and BTR is made up of three key parts:

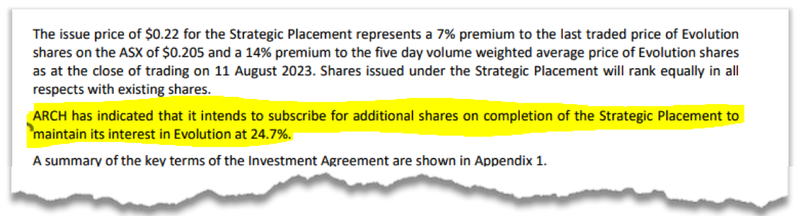

- $4.9M direct investment - BTR is investing $4.9M into EV1 at 22c per share. BTR will hold 9.9% of EV1 after the deal is done. At a premium to the last traded price.

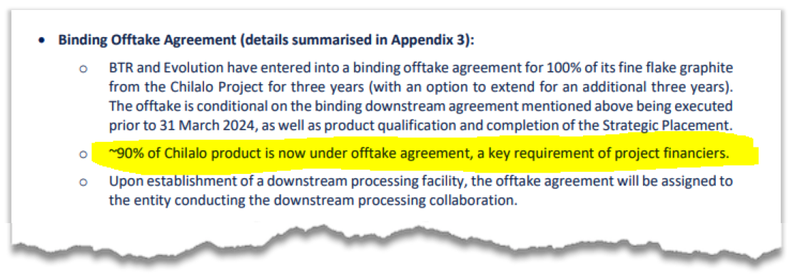

- Binding offtake agreement - BTR to purchase 100% of EV1’s fine flake graphite for 3 years with options for a further 3 years. This means that ~90% of EV1’s graphite is now under offtake agreements which is a big step toward financing its project.

- MOU to develop a downstream battery anode facility - Both parties to conduct initial work on a feasibility study on a plant in North America and other jurisdictions outside of China. The aim is to have an executed binding downstream agreement by 31 March 2024.

BTR’s direct investment into EV1 is expected to be completed on or before 31 October 2023.

The offtake agreement and downstream partnership are expected to be finalised by March 2024, subject to certain conditions.

EV1’s production and vertical integration strategy

For anyone following the graphite macro thematic closely, the news from the world's biggest graphite miner Syrah Resources can be confusing.

The electrification thematic is still strong, new electric vehicle sales are rising, more lithium ion battery packs are being produced...

BUT - graphite prices are going down....

In response, Syrah has recently started stockpiling its production instead of selling it at a loss.

This is where we think business strategy matters.

For now Syrah is a pure play mining company where it digs graphite out of the ground, concentrates it and then sells it.

That's where Syrah’s involvement in the supply chain ends.

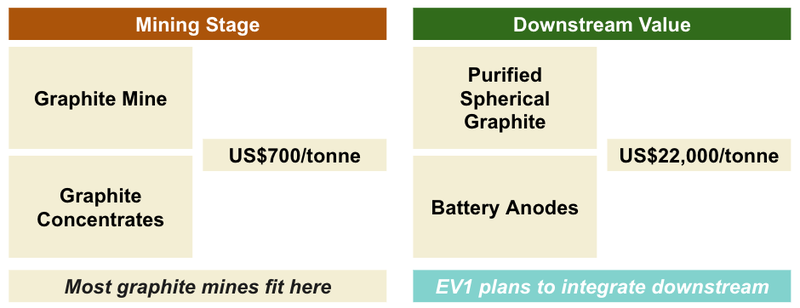

EV1 on the other hand has always been focussed on becoming a “vertically integrated graphite company”.

Vertical integration means instead of just selling the graphite, EV1 will take it from the mine, into a downstream processing plant, and then produce final products to sell.

Moving higher up in the value chain is important when it comes to battery materials.

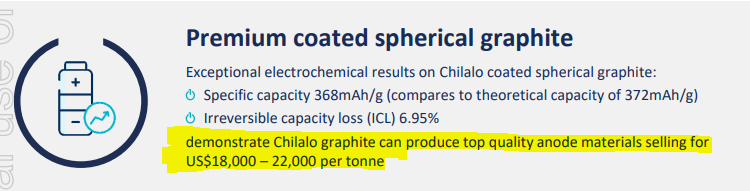

For context - fine flake graphite typically trades for ~US$600-700/tonne, whereas the high-quality battery anode materials sell for US$18,000-22,000 per tonne.

That’s up to 31x higher sale prices by adding downstream value.

It is no surprise that Syrah have recognised the need to go downstream and are building a battery anode plant in Louisana, USA.

We are seeing the same type of vertical integration happening in the lithium space right now.

The producers are mining lithium spodumene concentrates and selling them for US$3,500 per tonne. However the companies with downstream hydroxide operations are able to process and then sell the lithium for >US$35,000 per tonne.

No surprises that Pilbara Minerals is looking at deploying its $3.3BN cash balance into hydroxide processing capacity, and other majors like IGO/SQM/Albemarle are heavily invested in hydroxide processing.

We think the same will happen in the graphite space and this has always been a key reason for why we are Invested in EV1 over other graphite developers.

EV1’s mine has the type of graphite that can produce a range of value-add graphite products and has low enough CAPEX to bring into development a lot quicker than a mega scale project would.

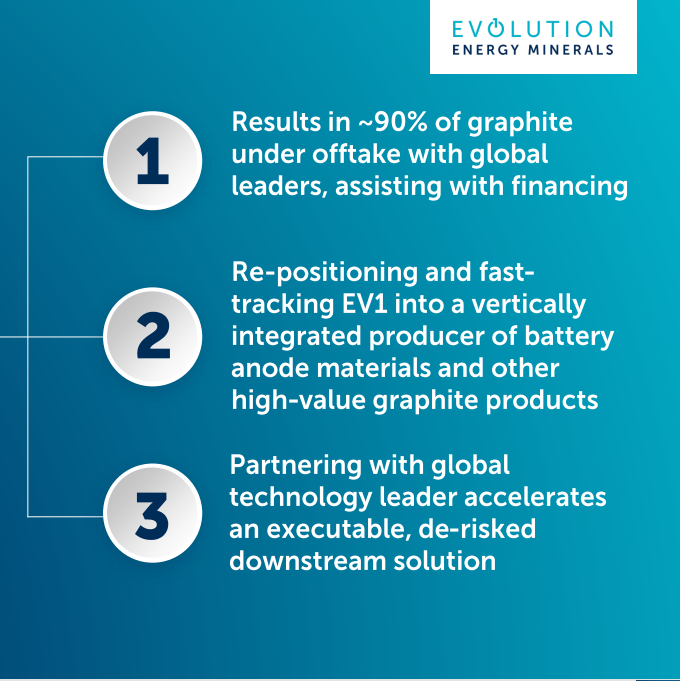

How today’s deal helps with EV1’s vertical integration strategy:

(Source)

Here is how we think today’s deal fits in with EV1’s overall strategy:

Our take on BTR’s $4.9M cornerstone investment

First of all, the direct investment means that BTR now has ‘skin in the game’ and are incentivised to see EV1 bring its project into development.

BTR is investing $4.9M at 22 cents per share, a premium to EV1’s current share price.

The deal is expected to be done on or before 31 October 2023.

At the same time, EV1 also gave BTR an explicit “Participation Right” - where if EV1 raises more cash it has to offer it to BTR on the same terms first.

EV1’s biggest shareholder, mining development ESG fund ARCH has also committed to maintaining its 24.7% interest in EV1, by subscribing for additional EV1 shares at the same 22c price.

The actions of both cornerstone investors ARCH and BTR tell us that when it comes time to raise more money to fund development, both will be ready and willing to deploy funds into EV1 to at the very least maintain their shareholdings in the company.

In a market where getting capital raises over the line is becoming more difficult, having deep-pocketed major shareholders taking up over 34% of the register is a strong validation of for EV1’s plans.

EV1’s project already has a definitive feasibility study (DFS) completed, so the next stage is all about securing the US$120M CAPEX funding needed to put the project into development.

(Source)

Our take on the binding offtake agreement

An offtake agreement is always good news for a company looking to put a project into development BUT, EV1’s offtake agreement helps the company in three different ways.

First, the offtake agreement means that ~90% of the production from EV1’s project is now subject to binding offtake agreements.

Offtake agreements show project financiers that there is genuine demand for a company’s product and make it more likely that financing is given to start developing a project.

Second, the offtake agreement was locked in AFTER EV1 gave BTR a bulk sample of graphite concentrate.

This tells us that BTR have tested EV1’s graphite and see it as high enough quality to be used in developing battery anode materials.

To us this de-risks EV1’s product from a technical perspective as well as a sales perspective.

Third, the offtake agreement will be with a downstream entity that EV1 will have an ownership stake in, meaning EV1 gets certainty of sales for its graphite AND some of the upside when the graphite is processed and sold at much larger prices.

We also like the fact that EV1 has set a deadline for the offtake deal at 31 March 2024.

Our take on the MOU to develop a downstream battery anode facility

EV1 has already been progressing a potential downstream processing facility in North America.

In May, EV1 brought onboard Stacy Newstead to lead the US downstream venture.

Stacy has experience in the battery supply chain inside the US and has worked at US$9BN Huntington Ingalls Industries and US$15BN Textron Systems.

Now EV1 will look to build on all the work it has done to date with BTR as its partner.

When it comes to processing tech we think it's important to partner with companies that have been there and done it all before - BTR fit that bill with a market share >60% in natural graphite anodes.

BTR already owns and operates ~20 graphite processing facilities across China and Indonesia.

As part of the partnership EV1 will be responsible for delivering the graphite and BTR for product qualification and sales.

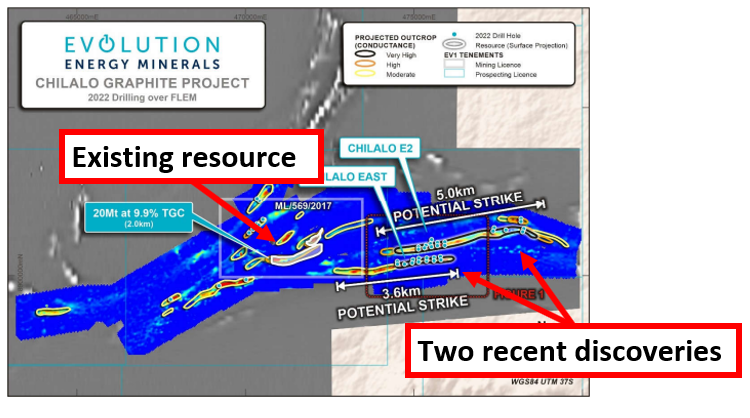

Interestingly, as part of the downstream deal, EV1 also teased that it would be investigating “expansion options” for its project - this is where the recent drill results, and new discoveries EV1 has made comes into play.

EV1 recently made two new discoveries right next to its existing 20Mt resource AND should the partnership require it, could look to bring this into its mine plan.

(Source)

The downstream MOU is closely tied to the offtake agreement whereby EV1 will be supplying natural graphite into the facility.

That means that BTR are incentivised to also get EV1’s project into development which explains the commitment to “work together to procure the finance for development” of EV1’s project.

One thing that stood out to us was that the deal has a hard deadline of 31 March 2024, similar to the offtake agreement which it is codependent on.

This means EV1 needs to wrap up project financing, a downstream co-op agreement AND the binding offtake all inside the next ~8 months.

Overall we see today’s deal as a key de-risking event from a technical, financing and partnership level for EV1’s entire business strategy.

The deal puts EV1 in as strong a position as it could hope to get its project financed and put into production.

We see the deal as a big step toward EV1 achieving our Big Bet which is as follows:

Our EV1 Big Bet

“EV1 will achieve first production of the world’s most sustainably produced graphite by early 2024 (including value adding processing) coinciding with the onset of a long-term supply shortage in the graphite market.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EV1 Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for EV1?

Final Investment Decision (FID) 🔄

The next stage for EV1’s project is a Final Investment Decision (FID).

An FID is a firm commitment from a company to proceed with developing a project.

Sometimes it is declared after all the project financing is committed to, and sometimes it is done well in advance of financing.

In EV1’s case, we expect the company to press on with other development items until an FID is officially declared - especially given the project CAPEX is relatively low at US$120M.

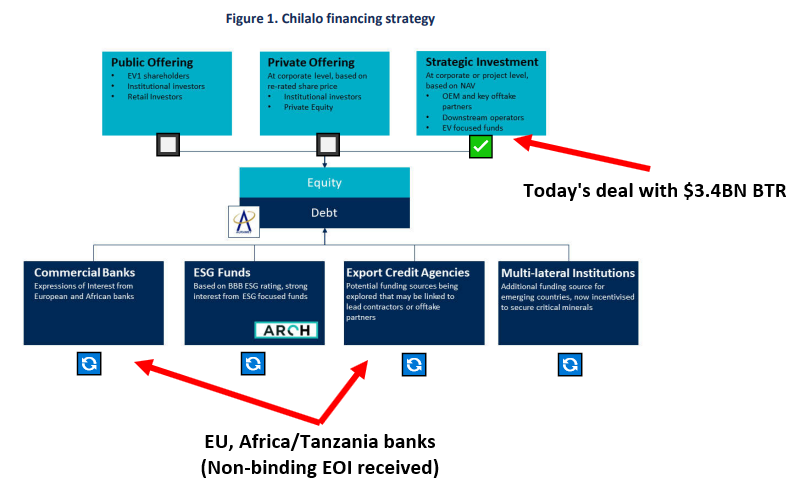

After today’s deal EV1 has outlined the first of its project financing strategies.

In the background EV1 is still working on securing debt financing - in the most recent quarterly EV1 said it had received non-binding expressions of interest from African, European and Tanzania banks.

EV1 has also appointed independent technical/environmental consultants on behalf of the parties interested in financing the project, which tells us they are serious enough to start doing due diligence on the project.

Here is how EV1 plans to finance the project:

(Source)

BONUS: Feasibility study on a downstream plant 🔄

EV1 will now be looking at developing its downstream processing plant together with BTR in North America.

Today’s deal with BTR should mean EV1 can move a lot quicker on this front now.

The next stage for the downstream plant will be about picking a site location and then running feasibility studies.

As part of today’s deal with BTR, EV1 has given itself until 31 March 2024 to get all of this work done.

More on the deal terms:

1) Direct Investment Agreement

BTR is investing $4.9M in EV1 at 22c per share.

The deal also comes with a “participation right” which means BTR get offered a position in all future capital raisings EV1 does.

The deal is expected to be completed before 31 October 2023 and is conditional on:

- BTR getting Chinese governmental approvals

- EV1 getting shareholders approvals for the deal.

- BTR doing due diligence on EV1 and EV1 does not lose its mining rights for the project.

2) Binding offtake agreement

EV1 to sell all of its -100 mesh flake graphite concentrate to BTR.

The deal would be for ~3 years with options to extend the agreement for another 3 years.

Graphite prices would be based on market prices at the time of delivery.

The deal is expected to be completed before 31 March 2024 and is conditional on:

- EV1 and BTR agree to a Downstream Cooperation Agreement before 31 March 2024.

- EV1 securing project financing OR construction on its project starting before 31 March 2024.

- BTR completing all product qualification tests.

- BTR’s $4.9M investment into EV1 being completed.

3) MOU to develop a downstream battery anode facility

The MOU between EV1 and BTR will be to develop a natural flake graphite downstream plant with an initial focus on a facility inside North America.

EV1 and BTR will eventually look to transition the MOU into a “Downstream Co-operation Agreement”.

The co-op agreement is contingent on BTR’s direct investment in EV1 and a feasibility study into a downstream facility being completed.

The Downstream Co-operation Agreement is expected to be put in place before 31 March 2024.

The next step for the downstream MOU will be to:

- Feasibility studies into a site in North America initially and then anywhere outside of China.

- Transition the MOU into a downstream co-op agreement.

- BTR to supply processing tech to the Joint Venture (JV) - subject to Chinese government approvals.

- BTR to manage product qualification/sales of products to customers in North America.

What are the risks?

EV1 is now at the stage where it is looking to get project financing for its project.

Given the deadlines on the deal today of 31 March 2024 the key risk in the short term is “Funding risk”.

To see all the risks we listed in our EV1 Investment Memo click on the image below:

Our EV1 Investment Memo

Below is our EV1 Investment Memo where you can find a short, high level summary of our reasons for Investing.

In our EV1 Investment Memo you’ll find:

- Key objectives for EV1

- Why do we continue to hold EV1

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.