EU Automaker Stellantis Snaps up 19.99% of EU Battery Metals Explorer KNI

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,582,223 KNI at the time of publishing this article. The Company has been engaged by KNI to share our commentary on the progress of our Investment in KNI over time.

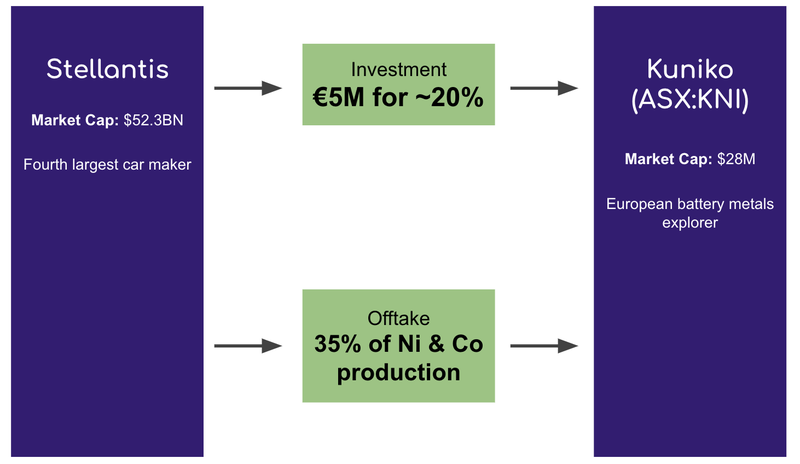

The fourth largest carmaker in the world, the $85BN Stellantis, just invested in our portfolio company Kuniko (ASX:KNI).

Getting an automaker to buy 19.99% of your company is pretty impressive for a $28M capped pre-resource exploration company like KNI - we aren't sure a deal like this has happened before.

The other part of the deal with KNI is an offtake term sheet. Stellantis wants 35% of KNI’s future nickel and cobalt production from its Norway projects for nine years (assuming production happens of course).

Stellantis might be the biggest car maker you have never heard of. Stellantis owns a bunch of household car brands like Fiat, Jeep, Chrysler, Alfa Romeo, plus many more.

Here’s the details of the Stellantis deal with KNI:

- Direct Investment - €5M (A$7.843M) direct investment in KNI for a 19.99% stake in the company. Stellantis’ is buying 16,794,726 KNI shares at 46.7c per share.

- 4.5 year escrow - Stellantis’ Investment is escrowed until 31 December 2027 - or until KNI makes a final investment decision on one of its Norwegian projects.

- Offtake term sheet signed - With a binding offtake agreement to be signed no later than December 31 2027 where KNI would sell ~35% of its nickel and cobalt production for a period of 9 years.

In another sign of Stellantis’ long term commitment to KNI, Stellantis also reserves the right to extend the deadlines for the offtake agreement AND reserves the right to maintain their 19.99% ownership in KNI if and when KNI raise capital in the future (which we would expect given KNI is not yet generating any revenues)

KNI now has two sticky, long term, cornerstone investors that control almost the majority of KNI shares on issue:

- Stellantis owning 19.99% of KNI, and

- Vulcan Energy Resources owning 20.45% before this deal (as per the latest KNI presentation).

This means what was already a tight share register, is even tighter.

Plus given the Stellantis entry price of 46.7 cents, we think this could help form a baseline valuation for KNI in the near/medium term.

With around 40% of the shares on issue in the hands of long term cornerstone investors, KNI does not have a lot of tradable stock.

This means that the share price can move quickly on material news, which it already has done in the past (remember the few weeks after the IPO?).

Stellantis (NYSE:STLA) was formed in 2021 when Peugeot and Fiat Chrysler merged.

It currently has a market cap of €52BN ($85BN), and owns the following 14 car brands:

(Source)

It’s a clear statement of intent from the automaker and validation that the European critical minerals thematic is stronger than ever.

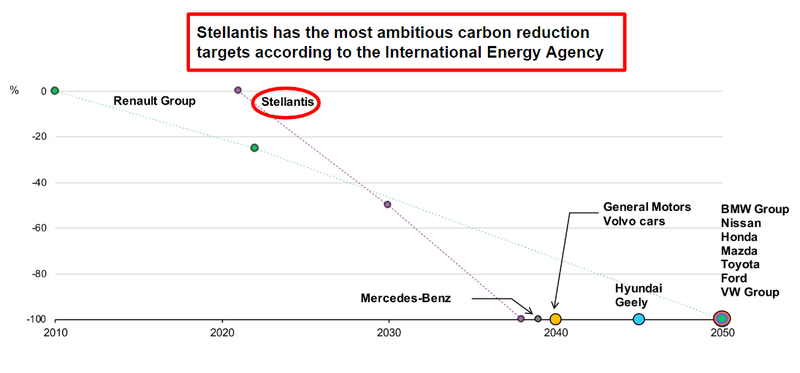

Stellantis has the most ambitious carbon emission reduction targets of all the major automakers:

(Source)

Now, KNI could play a role in helping Stellantis achieve this ambition.

To our knowledge, this is as far upstream in the critical minerals value chain that we have ever seen an equity investment made by a car maker.

The fact that Stellantis has invested in KNI, which has yet to define an economic resource, means Stellantis is serious about securing domestic, ethical supply of battery materials like nickel and cobalt in the EU.

We’ve been Invested in KNI since their August 2021 IPO after spinning off from our best ever Investment, Vulcan Energy Resources (which again, owns more than 20% of KNI).

Whilst this to us looks like the earliest stage investment Stellantis has made, the car maker has got a few deals with other mining companies.

This is the same Stellantis that signed an offtake agreement with Vulcan back in 2021 and a €50M investment in the company in 2022.

When Stellantis invested in 2022 the company owned 8% of Vulcan, it now owns 20.45%.

Vulcan’s strategy is to achieve Zero Carbon lithium production and KNI has the same Zero Carbon remit - which we think is perfect for the EU battery supply chain.

There’s been considerable effort in Europe to decarbonise the battery supply chain and source critical raw materials ethically.

The Zero Carbon approach of both companies we think makes both companies more suitable for institutional investment by large ESG focussed funds.

An offtake and equity stake from a car maker like Stellantis in an explorer like KNI is virtually unheard of - in fact this we think has likely never happened before.

As we noted above, there are additional benefits from having Stellantis onboard as a cornerstone investor in KNI.

For one, it means this large 19.99% chunk of KNI shares are tucked away in Stellantis’ hands, reducing the free float in the market - at the same time KNI now has $8M more to continue exploring its current projects or looking for additional projects to acquire, removing any risk of a near term capital raise.

Again, Stellantis took the position in KNI at 46.7 cents, which we hope helps put a floor under the KNI share price and a base to build from.

Should KNI achieve further exploration success, we think KNI’s capital structure is geared to re-rate.

But despite some early exploration success, there are no guarantees that KNI can find more or enough critical minerals on its projects to justify a mine - small caps like KNI are risky and commodity prices can hurt share prices even if the company finds valuable mineralisation.

With that said, there’s a second reason we like KNI’s agreement with Stellantis - it confirms that the European critical minerals push is stronger than ever before.

We think KNI took a significant step towards our Big Bet today:

Our KNI ‘Big Bet’

“To develop a sustainable battery metals mine within European borders that is of strategic importance - and hence highly valuable as an acquisition target.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our KNI Investment Memo.

For our summary of KNI’s progress over time and how today’s announcement contributes to our Big Bet see our KNI Progress Tracker:

Deeper dive on KNI’s deal with Stelantis

Here are the key terms of the offtake and equity stake agreement between KNI and Stellantis:

Key terms of direct investment by Stellantis:

- Direct investment - Stellantis is Investing €5M (A$8M) in KNI at 46.7c per share. After the deal closes, Stellantis will end up owning 19.99% of KNI.

- 4.5 year escrow - Stellantis’ investment is escrowed until 31 December 2027 or until three months after KNI makes a final investment decision on one of its Norwegian projects.

- Nominee Director - Stellantis has the right to appoint a director to KNI’s board.

- Cash to be used on Norwegian projects - As part of the agreement, KNI is to use the funds on advancing the company’s Norwegian battery metals projects.

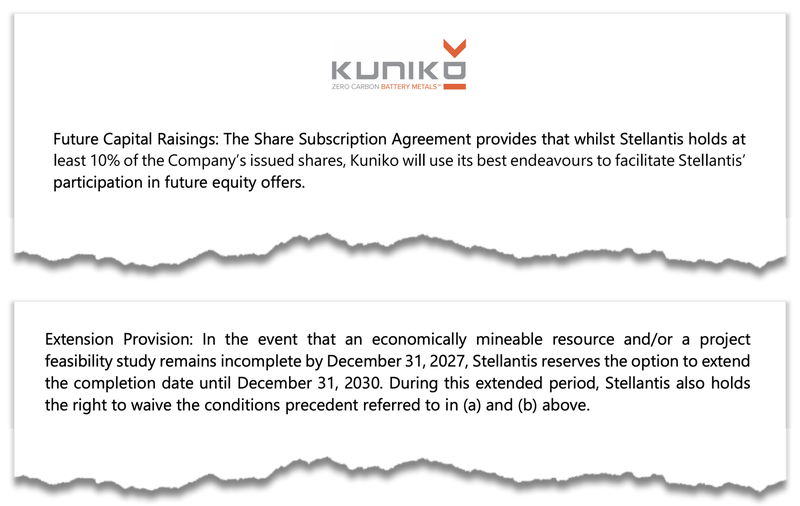

- Future participation in capital raises - As long as Stellantis holds at least 10% of KNI’s shares, KNI needs to offer Stellantis a right to maintain its ownership in the company in future capital raisings.

Our take:

We think that the terms of the direct investment are structured with intent, meaning that Stellantis has structured the deal in a way where they have a long term commitment to KNI.

Stellantis has effectively put a bet on KNI to deliver and develop an EU based battery metals project (more specifically nickel & cobalt).

The structure also tells us that if KNI are able to deliver a giant discovery hole, then Stellantis will be there to fund the company through the definition and development stages for the project.

Typically direct investments are purely financially motivated, however with this deal it seems there is a much bigger strategic angle...

Key terms of the offtake term sheet:

- Binding offtake agreement to be completed - A binding offtake agreement to be signed no later than December 31 2027 where KNI would sell ~35% of its nickel and cobalt production for a period of 9 years.

- Extension rights - Stellantis reserves the right to extend the due date for the binding offtake agreement through to December 31 2030 - IF KNI are yet to deliver an economically mineable resource and/or a project feasibility study.

- Pricing of the potential offtake - Pricing to be negotiated just before KNI kicks off a Definitive Feasibility Study (DFS) on its projects.

Before the binding offtake agreement can be signed KNI needs to have completed:

- Exploration on a project that is deemed economically mineable AND have a feasibility study completed.

- DD from Stellantis on that project.

- Binding debt and equity financing for the development of that project.

- Final Investment Decision from KNI’s board on the project.

Our take:

As above, under this agreement, Kuniko will sell 35% of the nickel sulphate and cobalt sulphate produced for a period of nine years, starting from the commencement of commercial production.

This is Stellantis thinking ahead well into the future about where and how it gets its hands on nickel and cobalt.

Offtake term sheets with companies that are pre-resource definition are almost unheard of.

We see KNI’s deal as a sign of the demand for EU based battery metals projects and how desperate the continent is to discover, define and develop projects in EU countries.

We see the deal as validation of the strong macro thematic behind our KNI Investment.

Our last KNI note was solely focused on the EU based battery metals thematic, see our note here: Norway fast tracks critical minerals push - KNI in the box seat.

Below is a high level visual overview of today’s deal:

KNI’s cobalt project

We’ve already stressed that ethically sourced cobalt from friendly jurisdictions must urgently be discovered and brought online, or eventually cobalt could be at risk of being phased out of battery chemistries.

Cobalt is an essential part of the EV supply chain and the majority (~70%) of it is sourced from the Democratic Republic of Congo (DRC) which produced 120,000 tonnes in 2021.

It is expected that almost the entire 2021 DRC production (120,000 tonnes) will be going into EVs by 2026.

Beyond that, a recent KNI presentation outlines how cobalt demand could increase by ~490% by 2050.

Read more: Our 2023 Outlook for Cobalt (Macro Theme)

Stellantis is clearly trying to get ahead of the curve here on cobalt.

KNI has completed two drill programs at its cobalt project, hitting good to excellent cobalt grades in just about every hole it has put in the ground.

The headline result from the latest drill program here was a 6.2m intercept with cobalt grades of 0.43% from a depth of just 25.2m.

For some context on that result - most of the cobalt produced around the world is done at grades of ~0.1%.

This was an unexpected near surface high grade result, so we’re looking for KNI to investigate the potential for more results like this in the near future.

We think KNI now has the funds to launch a third drilling campaign at its cobalt project.

To give a sense of the potential scope of this project, it sits near a historic cobalt mine that produced over 1 million tonnes of cobalt ore, making it the largest operational mine of its time.

KNI’s nickel project

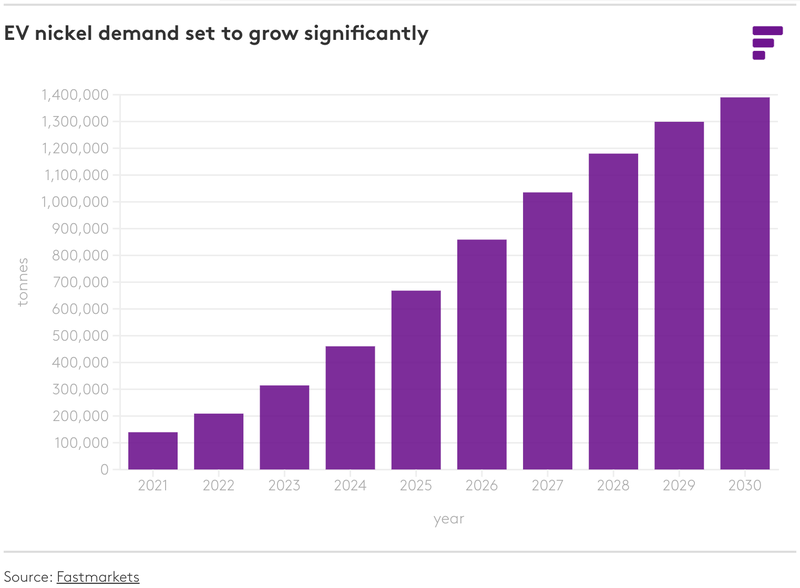

The International Energy Agency (IEA) expects nickel demand to increase by 7 to 19 times between 2020 and 2040. This will be driven by conventional demand from stainless steel as well as surging demand from batteries, mostly to supply the electric vehicle boom:

Read more: Our 2023 Outlook for Nickel (Macro Theme)

KNI’s nickel project has a fair bit of work already put into it.

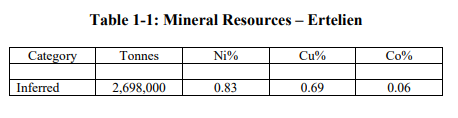

The previous owners of KNI’s nickel project compiled a mineral resource of ~2.7mt at 0.83% nickel, 0.69% copper and 0.06% cobalt - however this resource is not currently JORC compliant:

KNI’s latest round of drilling was done to verify that the resource exists and to gather more information so that a JORC compliant resource can be announced.

KNI completed a drilling program at this project with the following headline result:

25.1 m, grading 1.14 % Nickel, 1.20 % Copper, 0.07 % Cobalt, and 0.25 g/t 3E.

That’s a strong nickel grade which we think speaks to the potential for KNI to release a JORC resource at its nickel project, hopefully improving on the pre-existing numbers.

Again, KNI should have the funds to launch another drill program at this project.

What will KNI do with the Stellantis money?

With the funds from Stellantis’ equity investment and offtake agreement, KNI said that it will devote these funds to its Norwegian projects, likely with emphasis on its nickel and cobalt projects.

We expect KNI to more clearly articulate its forward works program in the coming weeks and months.

In the meantime this is what we are looking for...

Drill results from Norwegian projects 🔄

So far all of the assay results from 2 out of three of the projects drilled this year have been released.

We are now waiting for the final assay results from the company’s Undal-Nyberget copper project.

At its copper project, KNI is testing EM targets where the company has never drilled.

KNI had planned to drill eight drillholes across the two targets.

At this stage we view this drill program as a free option on a discovery and so our expectations are as follows:

- Bullish case = KNI hit copper mineralisation from one of the two geophysical conductors.

- Bearish case = Drilling returns no significant mineralisation.

Fieldwork across Norwegian projects 🔄

After the assays from the company’s copper projects, the focus for KNI will be on fieldwork to define new drill targets.

At a high level, the company will take all of the data from this year's drilling and then look to run geophysical surveys/rock chip sampling programs to define high priority drill targets.

We expect this work to start next quarter.

Rock chip sampling across Canadian lithium projects 🔄

We are conscious of the fires in Canada right now which have affected another one of our Investments exploration timelines so there is a risk KNI’s program gets delayed.

KNI did however confirm in a recent announcement that the fires wouldn’t impact its exploration timeline, see that announcement here.

Risks

These are the risks we identified in our KNI Investment Memo:

Exploration risk - despite the fact that KNI has well established mineralisation at both its nickel and cobalt projects, there is no guarantee that future results will be positive. Even if it does release a resource, there is a chance it won’t be economically viable and worthy of moving into feasibility studies.

Market risk - cobalt could be substituted or prices could be depressed further. Nickel or any of KNI’s other commodities could see reduced prices, hurting the economics of any future project.

Funding risk - as a small cap, KNI is dependent on capital markets for continued funding. Moving projects into feasibility studies costs money. This is closely tied to exploration risk.

[NEW] Big Brother risk - when a partner that is much bigger in size gets involved with a smaller company there can be a misalignment of goals between the two parties. Activity and progress can be slowed as the larger company slows down the smaller one, hindering the company’s ability to move quickly and make decisions.

Our KNI Investment Memo

Below is our KNI Investment Memo, where you can find a short, high level summary of our reasons for Investing including the following:

- Key objectives for KNI for the coming year

- Why we are Invested in KNI

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.