KNI share price moving up over the last two weeks…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,879,550 KNI at the time of publishing this article. The Company has been engaged by KNI to share our commentary on the progress of our Investment in KNI over time.

The Kuniko (ASX:KNI) share price has had a nice little run over the last two weeks.

Joining a few other small caps that seem to be bouncing off their 12 months lows.

The European Union (EU) has made securing local, clean battery metal supply a key strategic priority.

Which is great - but the local resources need to be successfully discovered and developed - which is what KNI is aiming to do.

KNI holds a portfolio of battery metals exploration assets (copper, nickel, cobalt and lithium) in the EU (Norway and Sweden).

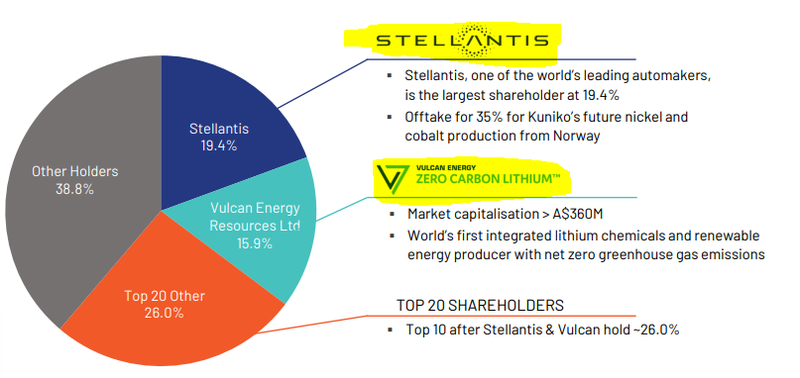

KNI is a $22M capped EU metals explorer, owned 19.4% by Stellantis - one of the EU’s biggest electric vehicle makers.

Stellantis’ investment was done at 46.7c per share - well above KNI’s current share price of ~26c.

Yesterday, KNI announced that it would conduct an EM survey - on the hunt for more nickel in the EU, with a chance of copper.

With results from the surveys due in Q2 of this year, we’re hoping it reveals some large targets worthy of drilling.

KNI has a JORC resource coming from the same project in April - the geophysics and another round of drilling will be to try and increase that resource by the end of the year.

The resource upgrades are targeted for Q4-2024.

The KNI strategy is to find EU based critical minerals deposits that can eventually be sold to EU buyers.

KNI is aiming to fill this demand by developing one of its EU based battery metals projects.

...or acquiring a new EU battery metal project to develop.

KNI is cashed up with $6.7M (as at the December quarterly) for a company of its size, following the investment from major car maker Stellantis.

A small company like KNI having a cash pile and a deep pocketed major shareholder while battery metal sentiment is low is a strong position to be in.

KNI can acquire a high quality, new battery metals project on the cheap as other explorers run out of money and become distressed sellers.

OR private project owners become more realistic on project valuations compared to bull market conditions.

We are watching to see what KNI might do here, they certainly have the cash to do it.

KNI had a massive run up after its IPO back in 2021, and has since pulled back.

And we’ve been Invested since day one.

(KNI was spawned as a spin-out from our best ever Investment, Vulcan Energy Resources).

We think that the future looks bright for this company, as the EU gets serious about its critical minerals supply chain.

By February 2027 all EV and industrial batteries sold in the EU market will need to have a battery passport. (Source)

The battery passport will mean all batteries will have strict rules on sustainability and traceability.

In effect, the EU will be policing where and how the critical raw materials inside batteries are made.

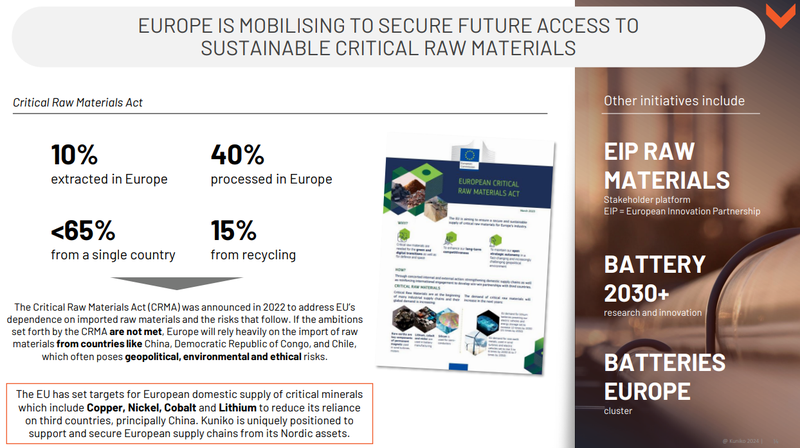

AND by 2030 EU Critical Raw Materials Act dictates that the following percentages come from within the EU:

- at least 10% of the EU's annual consumption for extraction

- at least 40% of the EU’s annual consumption for processing

- at least 15% of the EU’s annual consumption for recycling

- AND no more than 65% of the EU’s annual consumption from a single third country

At the same time, the EU has virtually no critical minerals mining industry - it consumes about a quarter of the world's raw materials but produces only three percent.

Which makes KNI exploration efforts in Norway all the more important

This company’s work over the last couple years was enough for the world’s fourth largest carmaker, Stellantis, to directly invest in it with a view to securing offtake of battery materials like nickel and copper.

KNI is in an enviable position for an explorer.

$139BN Stellantis holds 19.4% of KNI, and Vulcan Energy Resources owns another ~15%.

(source)

Stellantis made the investment and at the same time signed a nickel/cobalt offtake deal - which we think means they see KNI as the right company to deliver it.

KNI has a tight cap structure, a board full of heavy hitters in the critical metals space, great relationships with politicians and industry in Europe’s North from their work with Vulcan - and a slew of projects to work on.

With a bit of discipline, a lucky drill bit (good results) and market factors - KNI could be a sleeper hit after flying under the radar the last few months.

(or using its cash pile to acquire a new project while critical metals sentiment is having a breather - cash is king when markets are soft)

After an unsustainable initial spike up (then pull back) on the charts when it listed in August 2021, KNI shares needed to go through some consolidation and churn time, which sets things up for the next move upwards.

The consolidation period was made more difficult by weakness in the battery materials market - something which we will ultimately reverse amid the big macro trends of electrification and decarbonisation.

KNI has spent that time deciding how best to spend its money from the Stellantis investment, which we think is wise in a period where even the best results were sold into.

Post the Stellantis investment in KNI, KNI had $6.7M (at 31 December 2023) and in a soft market for exploration, cash is king.

We think KNI has a strong hand to play here - particularly as the small cap market starts to improve.

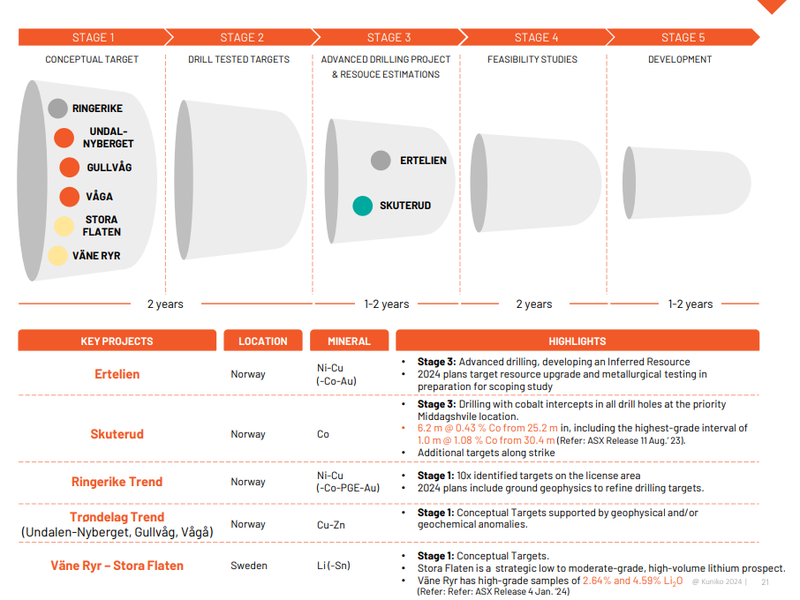

In terms of projects, KNI has the following under its belt after two and half years of work:

- A nickel-copper project with a JORC resource estimate on the way (April 2024) - KNI announced yesterday that it will conduct an EM survey on the larger project area that the JORC mineral resource will sit on. Hopefully it throws up some big targets with the potential for a “district scale” discovery.

- A cobalt project potentially worthy of development - KNI’s project sits in and around a historic cobalt mine that produced over 1 million tonnes of cobalt ore, making it the largest operational mine of its time.

- Early stage lithium projects in Sweden - in January, KNI acquired 70% interest in two lithium projects in Sweden. Historical sampling has turned up rock chips grading as high as 4.59% lithium. We see this as a cheap “free hit”.

- Large swathes of exploration territory Norway - a country that is positioning itself has the hub for the EU’s battery materials push, surrounded by gigafactories that will pump out the necessary batteries.

The focus for much of this year will be on KNI’s nickel-copper project in Norway.

We’re long term holders of KNI - and we expect it to deliver plenty of newsflow this year.

KNI has spent its time positioning itself as the go-to EU critical minerals explorer, and is backed by a macro theme that has delivered some of our most out-sized returns.

This macro theme forms the basis of our KNI Big Bet:

Our KNI ‘Big Bet’

“To develop a sustainable battery metals mine within European borders that is of strategic importance - and hence highly valuable as an acquisition target.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our KNI Investment Memo.

More on KNI’s nickel-copper-cobalt project - JORC resource due in April -

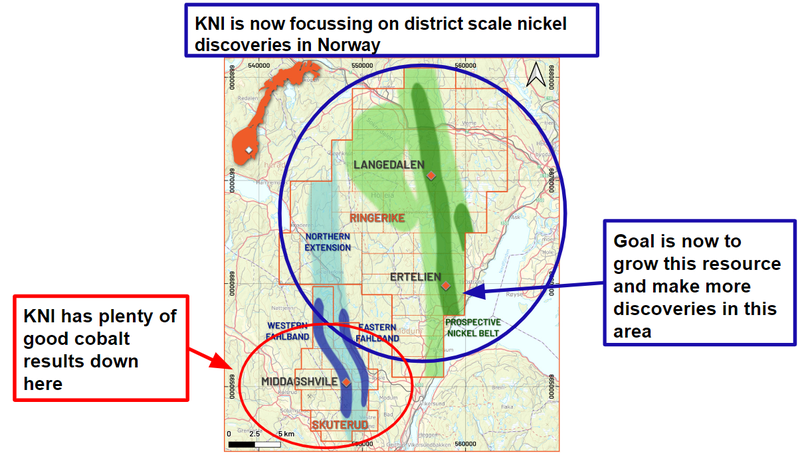

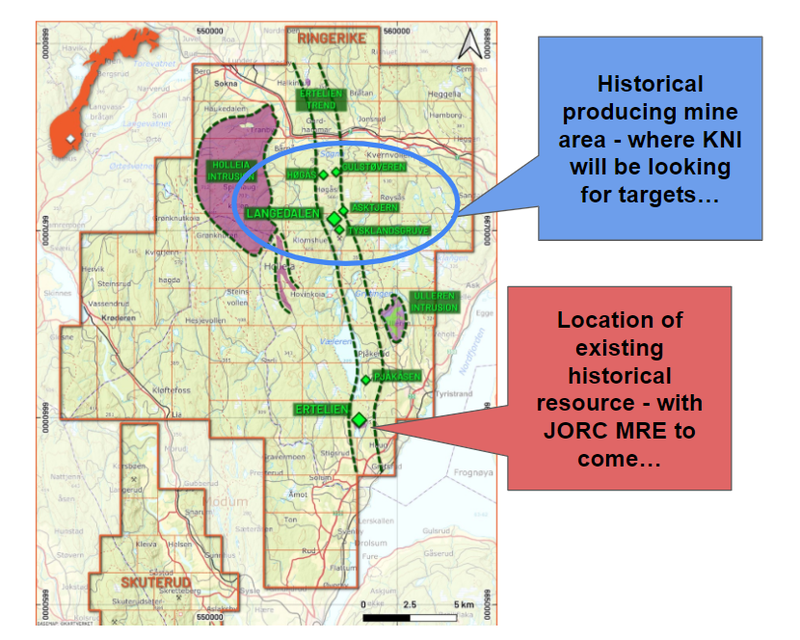

Most of KNI’s work over the last ~6-9 months has been on the Ertelien nickel-copper-cobalt project within the wider Ringerike region in which KNI has a package of land:

(Source)

KNI first built a 3D model of the existing non-JORC resource at Ertelien and is now looking to convert that into a maiden JORC compliant resource estimate.

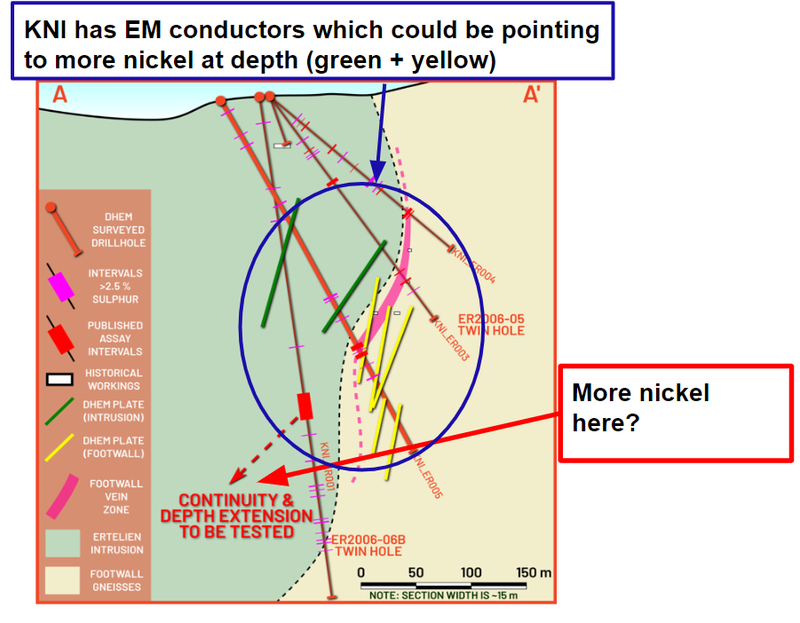

The interesting thing about Ertelien is that mineralisation remains open at depth, meaning that there could be more good nickel hits to be found down there.

KNI’s latest round of drilling at the project was done to verify that the resource exists and to gather more information so that a JORC compliant resource can be announced.

KNI completed a drilling program at this project with the following headline result:

25.1 m, grading 1.14 % Nickel, 1.20 % Copper, 0.07 % Cobalt, and 0.25 g/t 3E.

KNI is armed with conductors from down hole electromagnetic surveys which could be pointing towards more nickel mineralisation in a certain direction:

In addition to that data - KNI announced yesterday that it will be conducting ground electromagnetic surveys (TEM) targeting high-priority areas across the larger project area:

KNI’s plan is to get a JORC resource out on the Ertelien project in April and then follow that news up with drilling to try and increase the resource for the project overall.

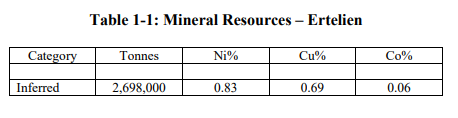

The good news here is that KNI already has a mineral resource estimate - however this resource is not currently JORC compliant.

The previous owners of KNI’s nickel project compiled a mineral resource of ~2.7mt at 0.83% nickel, 0.69% copper and 0.06% cobalt:

While we previously referred to this as a nickel project - that .69% copper grade is not to be ignored.

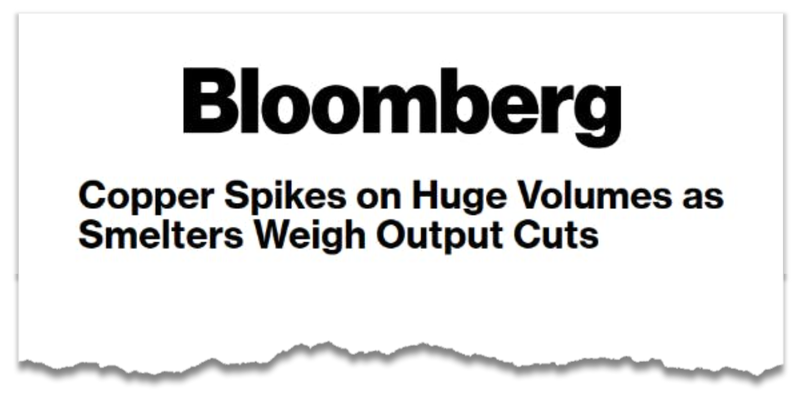

We’ve been bullish on copper for a while and it appears the copper market is heating up:

(Source)

Key takeaways:

- Chinese copper smelters are discussing potential production cuts due to plunging processing fees

- This sparked a spike in copper prices to 11-month highs amid supply fears

- However, large-scale smelter cuts remain uncertain given copper demand concerns

And a long term copper supply deficit forecasted :

(Source)

So we think the copper at KNI’s project can contribute to its viability in a meaningful way, even when nickel prices are depressed.

Why the EU and why Norway?

The answer - because the EU has given itself only a few years to sort out its battery metals supply chain.

By February 2027 all EV and industrial batteries sold in the EU market will need to have a battery passport. (Source)

The battery passport will mean all batteries will have strict rules on sustainability and traceability.

In effect, the EU will be policing where and how the critical raw materials inside batteries are made.

AND by 2030 EU Critical Raw Materials Act dictates that the following percentages come from within the EU:

- at least 10% of the EU's annual consumption for extraction

- at least 40% of the EU’s annual consumption for processing

- at least 15% of the EU’s annual consumption for recycling

- AND no more than 65% of the EU’s annual consumption from a single third country

At the same time, the EU has virtually no critical minerals mining industry - it consumes about a quarter of the world's raw materials but produces only three percent.

The EU has an ambitious agenda for building gigafactories which we think means the downstream demand will be there in a few years time, but no upstream to feed those factories.

The ideal scenario here is a producing mine inside the EU and sourced using ESG friendly mining methods.

Both things KNI is looking to do.

KNI’s most advanced projects are in Norway - a country where 98% of all power generation in Norway comes from renewable sources - meaning a mining company can produce minerals with a very low carbon footprint.

Two of those Norwegian projects are relatively well advanced at the JORC resource estimation stage.

As for why Norway is the perfect place to be in the EU...

Norway built its riches off North Sea oil.

The country set up a sovereign wealth fund and has been operating its oil industry as efficiently as possible for 50 years ever since they first found oil in 1971.

The key takeaway - Norwegians are always one step ahead of the game when it comes to recognising what the world needs and incentivising industry to produce it.

And they are doing the same thing with critical raw materials.

The big problem in Europe is the lengthy permitting processes for mines - we’ve seen this happen to some of our other Portfolio companies.

However, Norway’s critical minerals strategy is focussed on streamlining licensing - a big problem across the rest of the EU to incentivise private capital to invest in country.

KNI is clearly a favoured partner for spearheading Norway’s critical minerals push - in mid-January KNI presented before Norway’s parliament.

It’s not often that an exploration company gets this type of access to decision makers - below is a picture of KNI Chief Operating Officer Mona Schanche and KNI’s new Stellantis nominated board member Bruno Piranda:

(Click here to read the full KNI announcement)

The company presented to an array of representatives from the Norwegian parliament as well as key industry leaders.

It will be a busy year for KNI - with plenty of focus to be placed on big nickel discoveries.

KNI’s goal now is to make “district scale” nickel discoveries in Norway to feed a nickel hungry European EV market.

Nickel has been labelled a critical raw material by the EU and European nickel production has been in decline over the past two decades.

And yet, by one estimate, €1.2 billion of nickel was imported into Europe from Russia in the first half of 2023, with Russia making up to 90% of Europe’s nickel imports. (Source)

Despite a decline in the nickel price of roughly 50% over the last year on an Indonesia supply glut, we don’t see this as impacting KNI too much in the long-term for the following reasons:

- Commodity prices change quickly - and KNI isn’t mining right now (prices may improve by the time that happens). There are talks of a bottom being in on nickel prices too (Source).

- Europe has designated nickel a critical raw material - which means it will be subject to the domestic production quotas and other rules found in the Critical Raw Materials Act.

So things could be very different in the next few years.

What’s next for KNI?

- 🔃 JORC resource at Ertelien nickel-copper project (due in April 2024)

- 🔃 Geophysical surveys across its nickel-copper project (results in Q2 2024)

- 🔃 New drilling in (starting in Q2 2024)

- 🔲 Upgrade nickel-copper resource (expected by Q4-2024)

Risks

In the short term the key risk for our KNI Investment is “market risk”.

KNI is looking to put out a JORC resource estimate on its predominantly nickel focused, nickel-copper-cobalt project in Norway.

There is a risk that KNI puts out its resource estimate and the market just doesnt show much of a reaction.

Current market appetite for nickel projects is relatively low so the market may not re-rate KNI’s share price immediately after any news from its Ertelian project.

We are long term investors and more interested in KNI progressing the asset then we are the market reaction - in the long run we expect sentiment for nickel to turn and the market to start reward progress like KNI’s.

See our KNI Investment Memo for more risks we listed as part of our KNI Investment Thesis.

Our KNI Investment Memo

Below is our KNI Investment Memo, where you can find a short, high level summary of our reasons for Investing including the following:

- Key objectives for KNI for the coming year

- Our KNI Big Bet

- Why we are Invested in KNI

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.