Beyond the noise: Tracking the global shift away from the USD, "The Debasement Trade"

Published 14-FEB-2026 17:03 P.M.

|

10 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision. Any forward-looking statements are uncertain and not a guaranteed outcome.

Another Friday breather from the ASX this week.

Almost everything on our watchlist was down for the day (but still mostly up for the week).

Then came the Friday mainstream media headlines throwing out all of the usual buzzwords - meltdown, crash, collapse...

Sometimes there are reasons to be worried in markets - Friday didn’t feel like that at all, on the contrary it felt like nothing but “noise”.

What really happened?

Locally to the ASX - it’s earnings season for the bigger companies - so naturally, some of that earnings season volatility is permeating into the rest of the ASX.

Globally? Nothing’s really changed... (apart from maybe the AI and crypto crowds being spooked)

Gold and silver are still both doing their "volatility" thing...

Big swings during the week.

But both up over 2% for the last session of the week.

....and still up a lot when zooming out of the trees to look at the forest:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The S&P 500 and Nasdaq were pretty much unchanged:

(source)

And the US government is still trying to rebuild Western critical minerals supply chains:

(source)

All good indicators for almost every macro thematic we have exposure to in our Portfolio.

(and hopefully a more positive open on Monday morning).

An update on our “everything rally” idea...

We have written about the idea of an “everything rally” - where all commodity prices go up all at the same time.

We saw brief glimpses of it early in the year when gold was up, silver was up, nickel was up, lithium was up, copper was up (you get the point).

And we laid out the case for why we could see that play out on a bigger scale over the coming years...

A few weeks ago, we said this:

(source)

Today we will break down our thinking around point #2 in the list above:

“The US dollar’s status as the world reserve currency is under pressure (this is where the debasement idea comes from”...

Basically, our take on the “debasement trade”

First, what is the debasement trade?

It’s a world in which the value of the global reserve currency (right now, the US dollar) depreciates.

Then, because everything is priced in USD, the value of those things (oil, gas, gold, silver, nickel, etc.) starts to go up in USD terms.

(Increasing US debt and more money printing reduces the USD purchasing power even more).

Once the market’s faith in the USD as a store of value is rocked, everybody starts looking for alternative places to put their “reserves”.

(Just look at the gold/silver charts to see where some of that cash is going... or even eventually into other commodities).

The image and headlines below are a pretty good summary of it all:

(source)

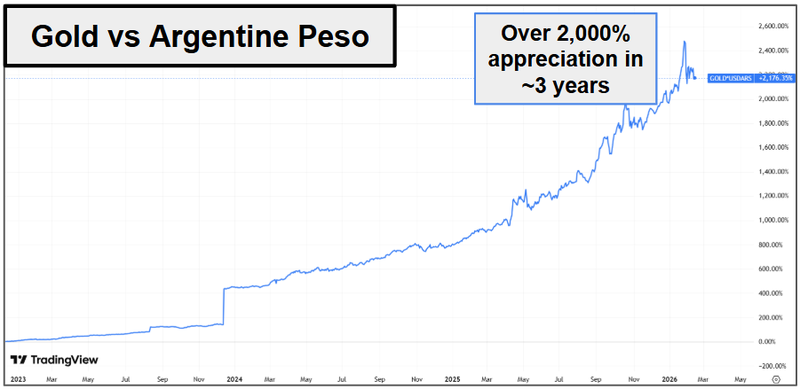

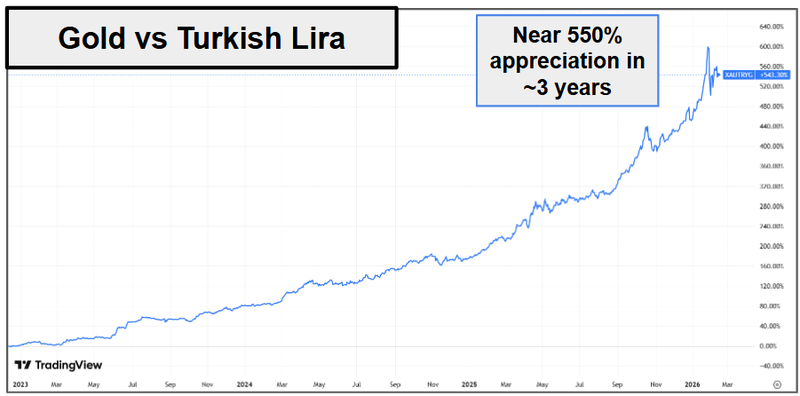

The most extreme scenarios where this type of depreciation has happened is in emerging market countries like Turkiye and Argentina:

(source)

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

No, we don’t think the same thing WILL happen to the US dollar - the USD is the global reserve currency - so an uncontrollable devaluation is unlikely.

But IF that global reserve currency status is threatened, then the probabilities of big moves in other potential reserve assets increases.

Especially when we start to see articles like the following:

(source)

This week, we saw the following news out of China - instructing its banks to reduce U.S. Treasury Holdings.

A centralised instruction from the Chinese government to move away from US dollar-denominated reserve assets.

Here’s what a few experts had to say about that move from China:

Desmond Lachman, a senior fellow at the American Enterprise Institute:

"[The US] desperately needs foreigners to keep buying US Treasuries to provide that financing, and the last thing that it needs is for foreigners to start selling their Treasurys,"

"The drying up of foreign buying of our government's bonds could set us up for a bond market and dollar crisis."

Joe Mazzola - Charles Schwab’s head trading and derivatives strategist:

"If China follows suit even as Japan's growing economy attracts more assets there, the pressure on Treasuries might advance”

The natural response from the US to these moves would normally be to increase interest rates to make the USD more attractive to hold.

Instead, the Trump administration is pushing for cuts.

And so the “debasement trade” is born, and the cycle of belief in it begins.

In summary the cycle goes like this:

- The markets think the USD’s purchasing power will decrease, so they buy another asset they think can act as a reserve (like gold),

- The purchasing power of the US dollar depreciates.

- The US cuts rates and prints more money, prioritising its domestic economy.

- US debt increases and the market gets nervous about the US’s ability to repay and fund its debt load.

- Sentiment goes back to point #1 and the cycle repeats.

We think one of the best summaries of what’s happening is from Ray Dalio - one of the most well known fund managers in the world (he writes some excellent books on market cycles too, we recommend reading them).

Here were his comments on gold and the “debasement trade”:

“When one's own currency goes down, it makes it look like the things measured in it went up."

And here are some of his comments on gold:

"In reserve currencies, gold is the second largest reserve currency...” and that monetary policymakers would still call gold 'the safest money in this kind of environment.'"

"Perhaps, central banks, or governments, or sovereign wealth funds, should say what percentage of my financial assets, what percent of my portfolio should I have in gold... and to keep a certain percentage, because it’s a very effective diversifier to other parts of the portfolio." (source)

The biggest winner from the debasement trade? Gold

IF the debasement trade plays out the way Dalio and other experts think it might, then we would think the biggest winner should be gold.

And IF gold goes on a wild run to US$6,000+ (or maybe something really outlandish above US$10,000 per ounce), then gold stocks could really run from where they are today.

That’s why we added BMG Resources (ASX:BMG) to the Portfolio last week.

And we also hold: TTM, KAU, BKB, RML, MTH, AVM, BPM, PUR, TG1, LSR, L1M.

And also why we are looking to add a few more to the Portfolio over the coming weeks.

We have looked at a few interesting stories already - but we are keen to look at any other companies we may have missed.

Send in your favourites for us to take a look at.

We are mainly looking for:

- Gold stocks that haven’t really run yet (relative to where they should be based on what they have).

- Preferably, companies past the exploration stage (unless the exploration prospects are really big swing for the fence targets, those we are always interested in), and

- Ideally, companies that are flying under the radar for whatever reason.

Some other interesting news out of the US

Two bits of news we saw this week that we had to highlight in today’s email.

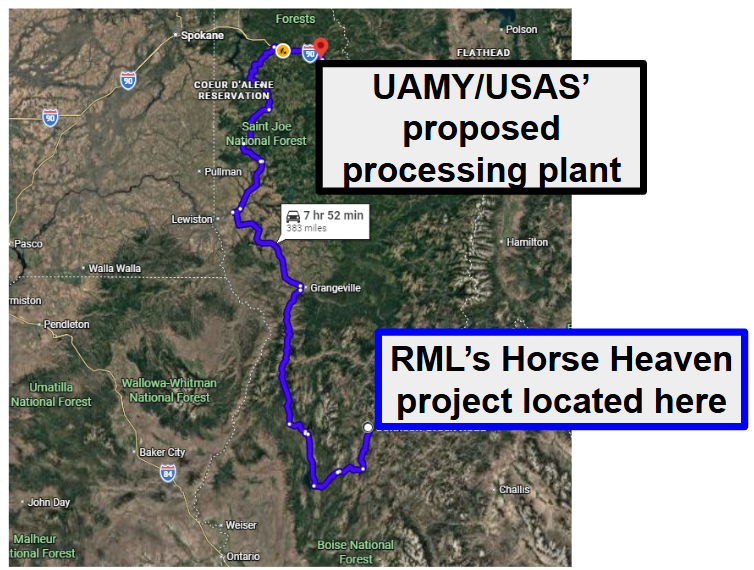

First was the United States Antimony Corporation and Americas Gold and Silver news forming a JV to build a processing plant for antimony, silver, and copper in Idaho.

Here is US Antimony Corp’s official release here.

And this is where the proposed processing plant is, in relation to our Investment RML:

US Antimony Corp aren’t the only ones either, a few months ago, the US Department Of War said it would build refineries in Idaho too:

(Source)

We think both of these could be good for our Investment in Idaho, Resolution Minerals (ASX:RML).

RML’s project has a history of producing US critical minerals antimony and tungsten (and gold): (Source)

- During World War 1: RML’s project produced antimony.

- During World War 2: Antimony was produced again

- In the 1960’s: There was even more Antimony production

- And then in the 1950’s to 1980: Tungsten was produced at RML’s project

Every time there was a kinetic conflict, historically the US turned to RML’s ground for some sort of supply.

Now with a build out of refining/processing capacity it looks like Idaho may become a base for critical minerals production in the US.

The second bit of news was out of one of the world’s biggest gold miners - $113BN Barrick Mining Corporation.

Barrick’s cornerstone U.S. asset is its majority stake in Nevada Gold Mines, a Tier One, long‐life complex in a top‐tier jurisdiction....

While a large portion of its remaining portfolio is concentrated in higher‐risk countries such as Mali, the Democratic Republic of Congo, Zambia, Saudi Arabia, Pakistan and Papua New Guinea, which elevates its geopolitical and sovereign risk profile relative to peers.

Barrick is now officially considering splitting its US assets into a separate listed entity with its own management team and a US only focus. (source)

(source)

This would take its US assets out of a global conglomerate and put it in the hands of a management team who are solely dedicated to the US.

AND more importantly, the capital war inside Barrick (where money fights to get allocated into different areas based on priorities) will disappear - meaning the US assets can finally get the love and attention they deserve.

Our view is that a focused US Barrick entity will be good for all undeveloped US precious metals assets (not just gold).

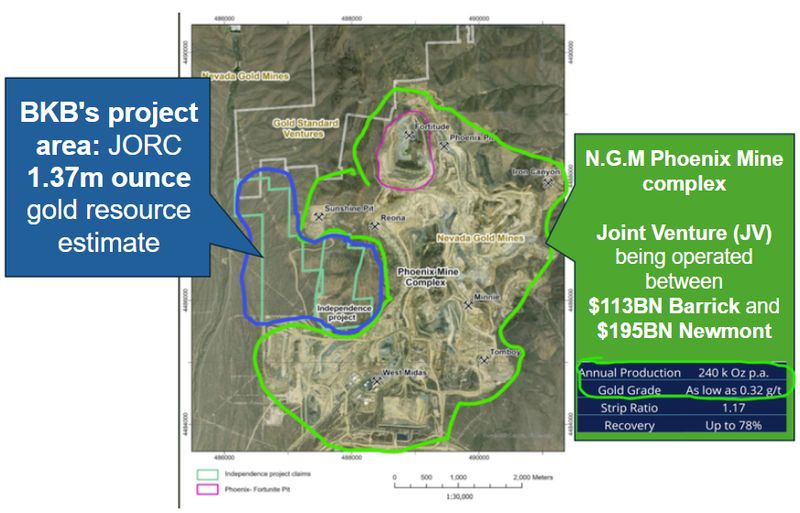

Based on this, the single biggest beneficiary in our Portfolio could be Black Bear Minerals (ASX:BKB).

BKB owns the 1.37M ounce Independence Gold Project, next door to 240k oz gold per year producer N.G.M (a Joint Venture between Barrick and Newmont).

BKB’s project is not just next door to a Barrick project - it’s literally inside the plan of operations for that N.G.M Joint Venture:

(source)

In the middle of last year, we were there ourselves, and we hiked up the hill from where BKB was drilling at the time.

After the 15 minute hike, this was our view, as you can see we were looking right at the large N.G.M operation (‘large’ probably doesn’t do it justice - it was massive):

So a giant organisation with a specific focus on local expansions and growth can only be good news for an asset that is shaping up nicely, literally next door.

See our site visit note on that project here: BKB is surrounded by one of the world’s biggest gold mines - here’s what we saw on site

(excuse the JBY ticker code in the note - BKB was called JBY back then)

See you next week, and have a great weekend

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.