An analyst deep dive into battery metals markets

Published 03-FEB-2024 12:18 P.M.

|

12 minute read

Two of our team have just landed in Cape Town.

We’re here for the annual Mining Indaba conference - one of the largest mining conferences in the world.

If you’re here too - reply to this email, we’re keen to meet up.

Speaking of conferences - we attended the Benchmark Minerals conference in Melbourne.

All eyes are on the slump in battery materials right now.

Lithium and nickel are stealing all the headlines...

For all the wrong reasons.

It appears to be all doom and gloom in the battery metals space, with broad based selling in vogue.

It was in this environment we headed along to Benchmark Minerals’ World Tour - “Financing the Energy Transition” in Melbourne this week.

Ironically... the front cover of the day’s program was a giant bull:

Benchmark is one of the top pricing analysts for lithium, nickel and other battery metals, so we were keen to hear what they had to say.

Our key takeaways was that the current breather in battery metal prices was part of a smaller cycle of supply and demand, but as we step further back the larger electrification thematic cycle is still intact.

We heard from several speakers who discussed key commodities, including nickel, lithium, and iron ore, as well as from battery maker BASF.

Keep reading for our key takeaways from the event.

The question everyone wants to know the answer to is “is this the bottom”?

And, when does the negative sentiment translate to a buying opportunity?

Well, no one really knows.

Not even analysts with piles and piles of data who are busy revising their models based on current events.

It is hard to time the peaks and the troughs of the smaller trends.

But, if we can identify the bigger overarching trends, then hopefully our Portfolios will be in good shape.

So on that basis, we continue to be big believers in the global “electrification thematic”.

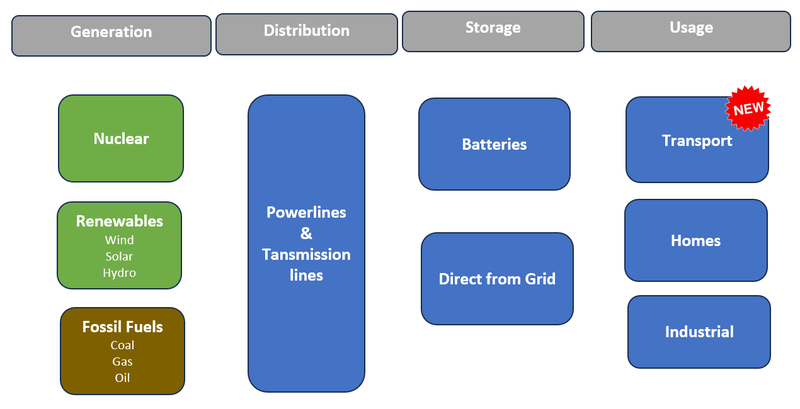

Our investment thesis is that as the world moves away from fossil fuels and towards an electric future we are going to need A LOT more commodities that power the electrification of energy.

The four key pillars this “electrification thematic” are as follows, with each pillar having its own supply and demand outlook that affects the pricing of the underlying commodities.

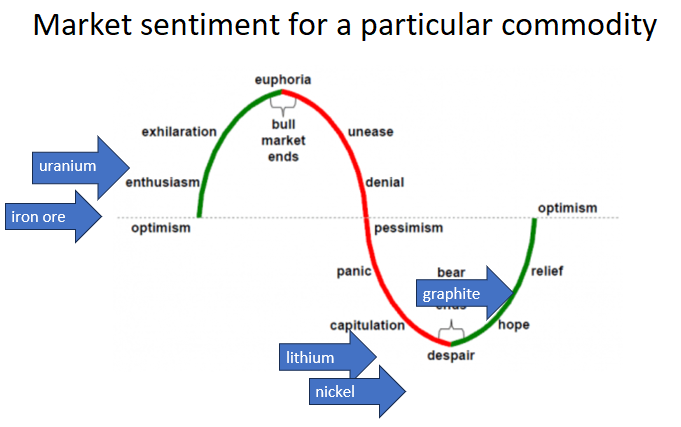

The short term cycle looks something like this...

Commodities at the start of the cycle are in a period of “excitement” - projects with this are being funded and investors are rewarding results by buying on the market.

Commodities at the end of the cycle are entering a period of “panic” - share prices are depressed and investor sentiment is low.

For us, it is about holding strong through the cycles that dictate commodity prices based on supply and demand and continue to make investments that are leveraged to the bigger cycle that is driven by the electrification thematic.

Here are some of the key takeaways we got from attending the Benchmark Minerals event.

Key Trends in the Battery Supply Chain

Commodity prices work in cycles.

Both in small cycles and big cycles.

And although the price of many battery metals have come down over the last six to twelve months, the long term outlook remains strong.

Benchmark analysts underestimated the short-term demand picture for battery metals - due to underestimating a slower than predicted EV uptake despite EV inventories continuing to build out.

However, the longer term demand picture still remains strong.

This long term demand picture is driven by policy and a desire to get to net zero emissions.

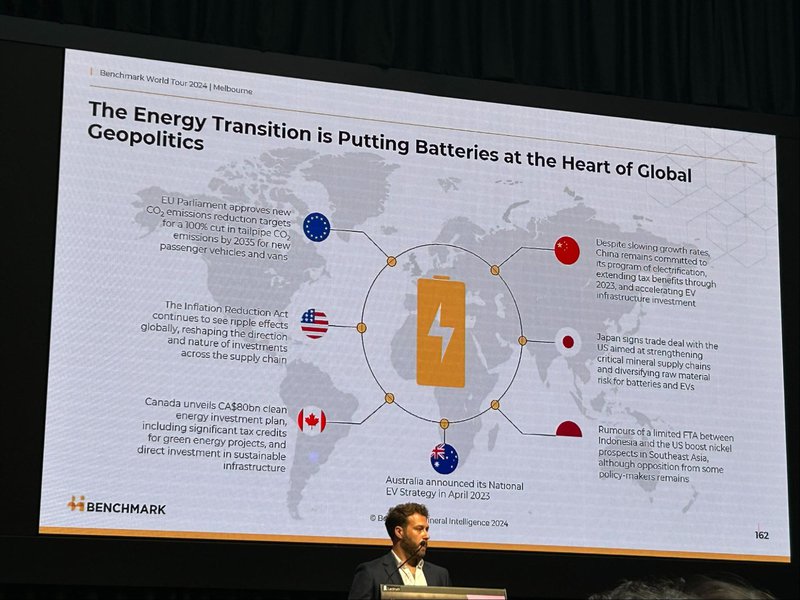

The US, through the Inflation Reduction Act, has lit a fire under the supply chain build outs for many of these battery metals.

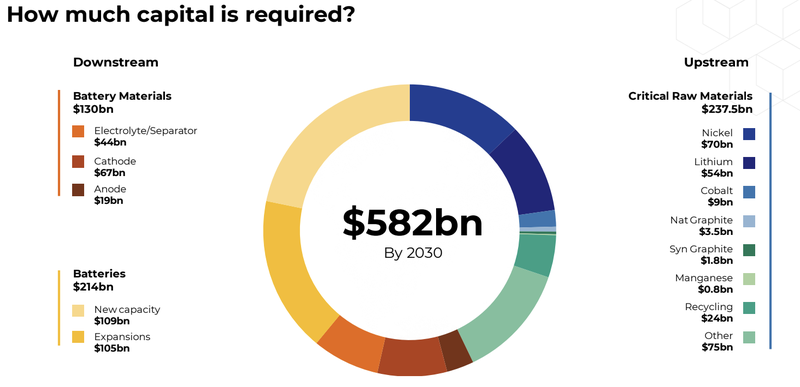

If the world is moving away from fossil fuels and towards a diversified energy future, we cannot ignore the enormous amount of materials that will go into the transition.

The total capital required to meet ambitious net zero targets is forecast to be $582BN in the next 6 years.

Policies like the Inflation Reduction Act and other similar incentives in Europe and around the world are designed with national security in mind and to secure supply chains for critical minerals.

The US in particular does not want to be at the behest of China for key materials needed for its energy transition.

Even though the short term outlook is relatively muted for now the long term prospects for materials remains strong.

This is due to a genuine desire to get to net zero emissions, the vast amount of commodities needed to get there and a national security interest that underpins robust supply chain policy.

China’s grip on the battery metal supply chain

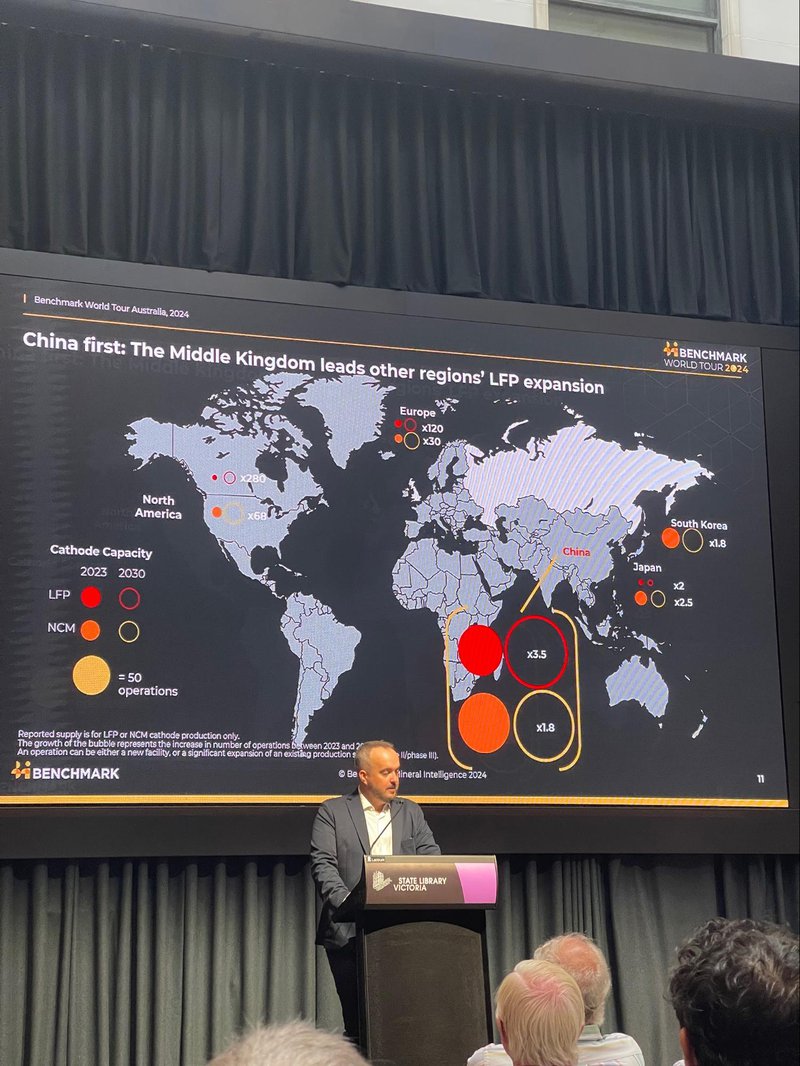

What was clear from the presentations was that China still has a strong grip on the battery metals supply chains.

In particular the country’s buying power for raw materials and vertically integrated processing capacity.

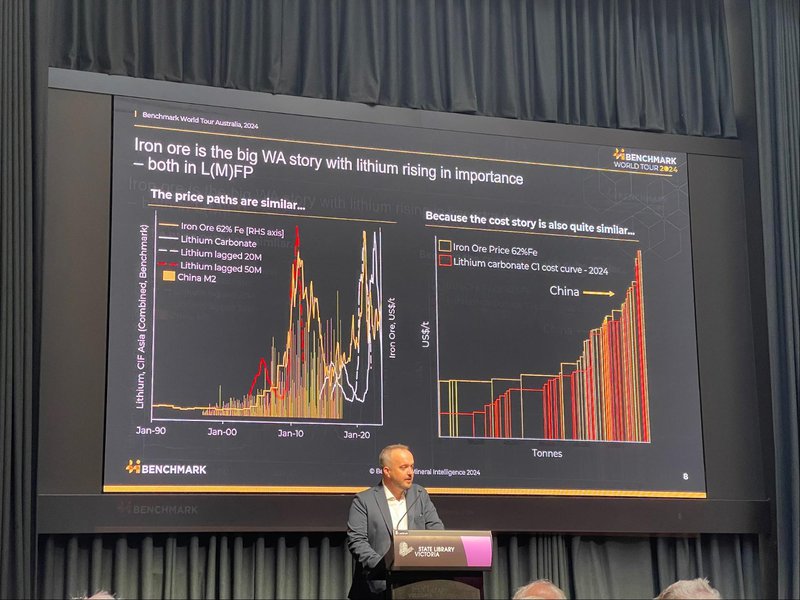

Have a look at this chart that shows how interrelated China’ money supply (M2) is with the prices of raw materials (in this case iron ore and lithium).

The correlation between the price of commodities and the Chinese money supply (M2) shouldn't come as a surprise to anyone especially considering they are the biggest buyers of lithium and iron ore.

But, what is M2 and why is it important in this context?

Our armchair economist's explanation is that M2 is a broad measure of the total amount of “money” or cash in the system at any given time.

If M2 goes up, it means that the economy is flush with cash and business activity is high.

If M2 goes down, it means that there is less money in the economy causing a retraction in economic and business activity.

At a very high level, if China is having domestic economic problems then that is bad news for the price of raw materials demand.

For raw materials in particular there is no bigger buyer than China.

In a healthy market, the economic power of ONE buyer shouldn’t be able to affect the entire supply chain - particularly with something as important as commodities.

However, given China’s grip on the supply chain - it has enormous sway when it comes to commodity pricing and demand.

When the Chinese wallets are closed - the industry feels it...

Anyone following the Chinese domestic economy will know that the country is going through one of the biggest debt restructures in its history.

Just this week one of the country's biggest property developers Evergrande was ordered into liquidation.

That is how the two seemingly unrelated events - the fall of the Chinese property market and the drop in commodity prices for battery materials - are inherently linked.

So how does this help to predict the outlook for battery materials going forward?

Well, any improvement in domestic economic conditions in China could be a strong signal that battery metals come roaring back.

ALSO, the West will likely look to wrest back control over the market through policy, propping up their own commodity supply chains and incentivising EV demand.

This is all in a bid to alleviate China’s almighty grip over the commodities market.

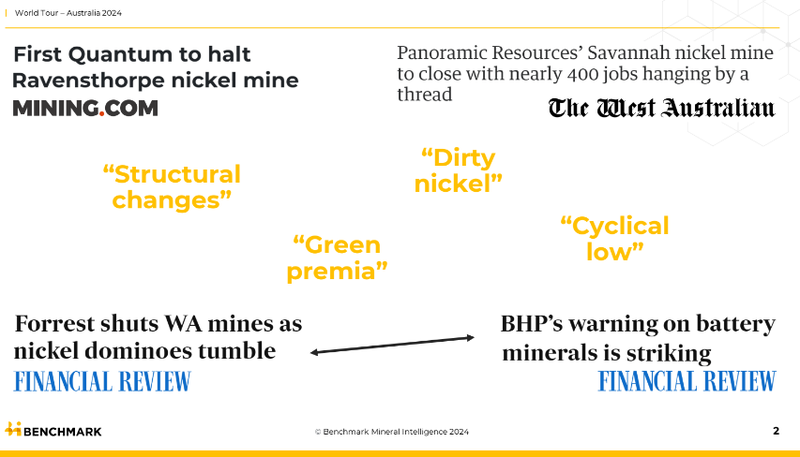

Looking past “Dirty Nickel”...

Nickel... sigh...

One of the most beat up battery metal sectors right now.

A number of mines have been shut down, major players in the space are writing down nickel assets and the prospects for the commodity are looking grim.

The growth in the nickel market was leveraged to battery metals macro thematic because of its use in high range, high performance EV batteries.

Remember back in 2020 when Elon Musk said at the infamous Tesla Battery Day - “We Need More Nickel”?

(Source)

From there, the nickel price soared, but has since cooled significantly with relatively cheaper supply coming out of Indonesia flooding the market.

It led to most of the industry participants calling for the end of the nickel boom.

BUT, as Benchmark analysts argued, nickel as a battery metal hasn't had time to mature yet...

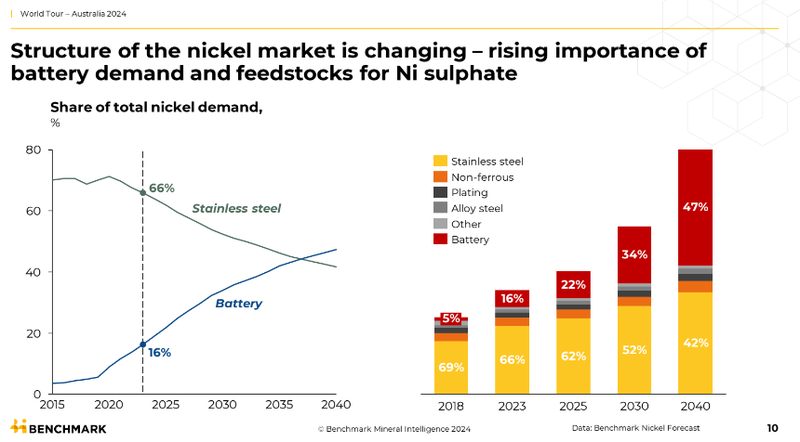

Only 16% of nickel supply is used in batteries right now with most nickel going into producing stainless steel.

It isn't until ~2035 when nickel demand from the battery sector is expected to surpass the steel market.

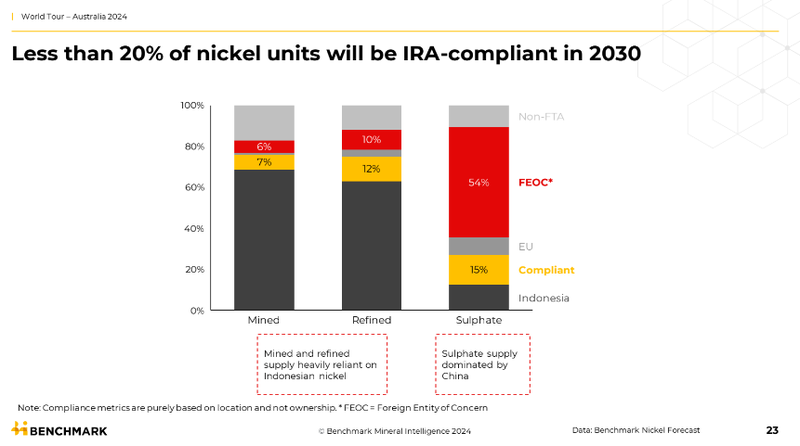

Adding to that momentum will be the IRA incentives that will force nickel to come from ESG friendly sources, from inside countries that have free trade agreements in place with the US.

Like most other battery metals, the short term outlook for nickel looks poor.

However, if the long term demand picture for battery metals plays out as expected, then the cycle will turn in the long run.

And, when it does, all of the projects that were taken offline during the cycle lows will exacerbate the supply deficit leading to much higher prices than the market expects.

Last weekend we wrote about how companies that pick up projects at cycle lows often end up performing the best when the cycle turns.

We gave the example of Champion Iron, who bought an iron ore mine in Canada at cycle lows and then had it back operating when the iron ore price started moving back up to <US$100 per tonne.

Champion’s share price went from ~9c at the bottom of the cycle to a peak of $8.50 per share this year.

We are Investors in the nickel space in the long run and hope that we can pick the best companies during the downturn so that they can deliver us performance in the up cycle...

The Lithium Outlook

While the supply side of the lithium equation was in line with expectations the demand side was not.

This led to prices falling.

What many of the analysts recently got wrong was the declining year on year growth figures for EVs.

Right now, we are in an interesting position - where demand has not lived up to expectations.

This has triggered the downcycle in lithium price.

Generally, demand changes quickly, but supply does not.

With prices for lithium expected to be subdued, capital may not flow as much into new lithium supply.

However, when new demand comes online, as we expect driven by policy, prices for lithium will return.

And so the cycle will continue.

How quick the price cycle returns depends on how quickly the demand picture returns for EVs.

We think that the geopolitical interests in achieving net zero as well as nation security concerns over supply chains will drive policy that drives EV demand in the long term.

BASF - How Battery Chemistry is Changing

If you were born before 1990, you may best remember BASF as the blank video cassette maker.

Turns out this giant German firm does a lot more than just producing archaic media items...

As a chemical maker, BASF plays a key role in the EV battery supply chain, as it buys plenty of raw materials.

Dr Bill McPhee, a Regional Business Development Manager from BASF presented at the Benchmark event to provide a downstream perspective.

BASF is aiming to not only become a leading global battery producer but also a leading battery recycler.

As a German company, Dr Bill was able to present how BASF is ensuring its products comply with EU regulations for battery passports and source ESG friendly raw materials.

Battery recycling will also start to emerge as a bigger part of the supply chain, however it's very early days for that business model.

Dr Bill also ran through how battery chemistry is changing.

The key takeaways was that there will be a lot of different battery metal chemistries including NMC (Nickel-Manganese-Cobalt) and LFP (Lithium-Ferro-Phosphate).

With the latter presenting an attractive opportunity, particularly in China.

Final thoughts on the Benchmark World Tour

It is an interesting time to be an investor leveraged to the battery metals thematic.

The prices of many of these commodities have fallen, but the long term outlook hasn’t changed.

The insights presented by the Benchmark analysts supported our battery metals investment thesis that the “electrification thematic” will drive commodity prices higher over the long run.

However, in the short term, a reduction in money supply particularly in China has led to lower demand and a cooling in the commodity market.

Long term, the West will need to introduce policy that drives back this demand - IF it want’s to decouple itself from China and achieve its net zero goals.

Next week some of the team will be reporting in from Cape Town, South Africa for Mining Indaba and the 121 Mining Conference.

We have a number of resources Investments based in Africa, and given this week in Cape Town attract a lot of global interest in the mining industry, we find it important to gather the sentiment on the ground over there.

So keep an eye out for that write up next week.

Maverick Minerals IPO is Open

Latin Resources (ASX:LRS) is spinning out some of its projects into a new ASX IPO - Maverick Minerals (MVM).

We are participating in the Maverick Minerals IPO.

LRS will be 16.2% shareholder in MVM.

MVM plans to list on the ASX on March 6th (indicative date).

For full details see the MVM IPO prospectus.

To bid into the MVM IPO click here

(make sure to read the prospectus in full before you bid)

What we wrote about this week 🧬 🦉 🏹

Pantera Minerals (ASX:PFE)

This week PFE announced an exploration target for its lithium brine project next door to Exxon Mobil in the Smackover formation in the US.

Read: 🎯 PFE announces exploration target... and we are going to Arkansas to see it.

Arovella Therapeutics (ASX:ALA)

Our best performing stock of 2023, ALA, announced that it has licensed a technology that “boosts” its cancer killing treatment. It also presented new data from mice studies that showed this new technology improving the product.

Read: 🧬 ALA Bolts on New Technology in Cancer Fighting Cell Therapy Platform

BPM Minerals (ASX:BPM)

Our gold microcap explorer BPM commenced a 10,000m AC/RC drilling campaign this week for gold. 7 days ago, BPM’s big neighbour $1.6BN Capricorn Metals announced a number of drill results including a 10m hit @ 17.16g/t from 32m. BPM’s drilling is 500m away from these hits.

Read: ⛏️ $5.2M microcap BPM is now drilling it’s Claw gold project - 500m from $1.6BN capped gold miner

Quick Takes 🗣️

MNB pushes ahead with fertiliser project

LYN to drill in the West Arunta in early 2024

BPM Commences Drilling at Claw

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.