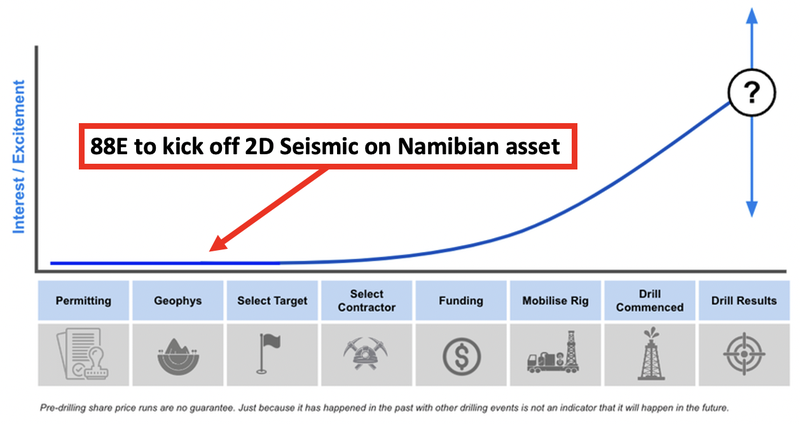

88E starts on “swing for the fence” Namibia oil exploration.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 68,888,890 88E shares and 6,296,297 options at the time of publishing this article. The Company has been engaged by 88E to share our commentary on the progress of our Investment in 88E over time.

We love a big “swing for the fences” oil and gas drilling event.

The anticipation of the wait, then the excitement of the drilling...

and the glory or despair of the drilling result.

88 Energy (ASX:88E) is kicking off work on its new Namibian oil exploration project.

(Fresh off the back of two successful flow tests on its projects in Alaska)

The work onshore in Namibia follows some giant offshore discoveries by oil supermajors like Exxon and Total.

We don't think the market is placing much value on 88E’s African asset at the moment.

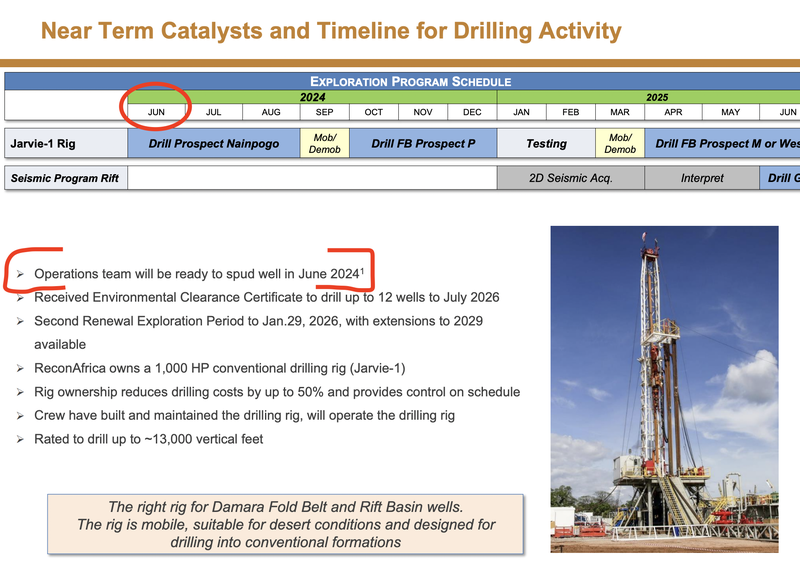

But this may start to change as a regional peer (Recon Africa) moves closer to drilling in a few months time.

88E recently raised $9.9M, adding to the $17.5M cash on hand at the March 31st quarterly report.

This cash should see the company through work programs across both its US and Namibian assets.

There are a few low-cost catalysts in the works for 88E over the coming months:

- In Alaska, USA - booking contingent resources & potential farm-out deals.

- In Namibia - wells being drilled by its regional peer which could increase investor interest in 88E’s ground and an already paid for 2D seismic program.

88E’s Alaskan assets have been de-risked with two successful flow tests completed last quarter.

On it’s Namibian asset, 88E has just locked in 2D seismic contractors.

The seismic is expected to be processed and analysed by the end of Q4-2024, targeting a maiden drill program on 88E’s ground in H2-2025.

Namibia is being talked about as an emerging oil and gas province.

Oil supermajors Shell, Tota and Chevron have made some of the biggest deepwater offshore discoveries in recent decades - estimated at ~11 billion barrels of oil and ~8.7 TCF Gas.

Onshore in Namibia, 88E’s regional peer has also traded at a market cap of over $1BN (in 2021)

...without even making a discovery.

AND this year, Recon is planning multiple wells starting in June, targeting the same play type found on 88E’s ground.

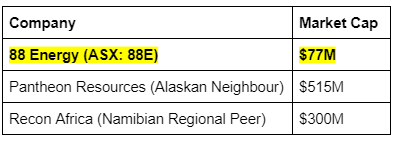

Right now, at a 0.3c share price 88E is trading at a fraction of the market cap of both it’s regional peers in both Alaska and in Namibia:

We are Invested in 88E to see it close the valuation gap to its peers over the coming months/years.

(and hopefully deliver a discovery on its new “swing for the fences” project in Namibia)

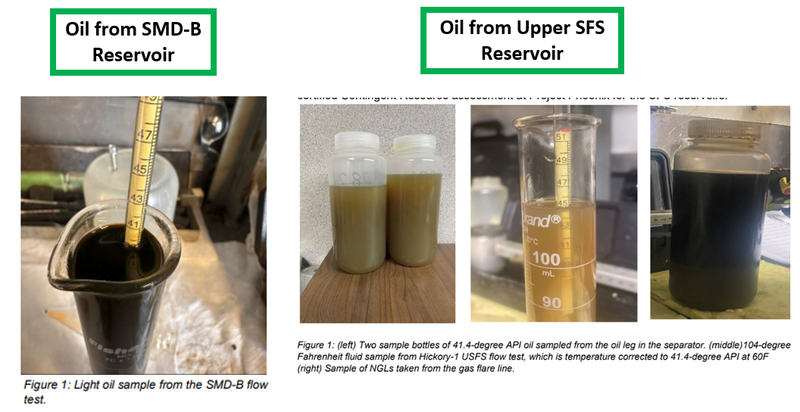

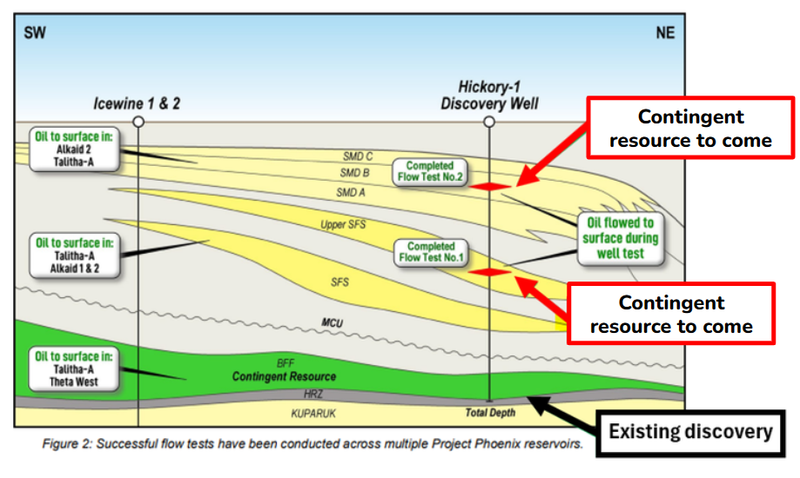

In early 2023 88E drilled its most successful well at one of its projects on the North Slope of Alaska, USA.

At the time 88E made two separate discoveries.

A few months ago, 88E flowed oil to the surface from those discoveries—both news catalysts that most explorers dream of releasing.

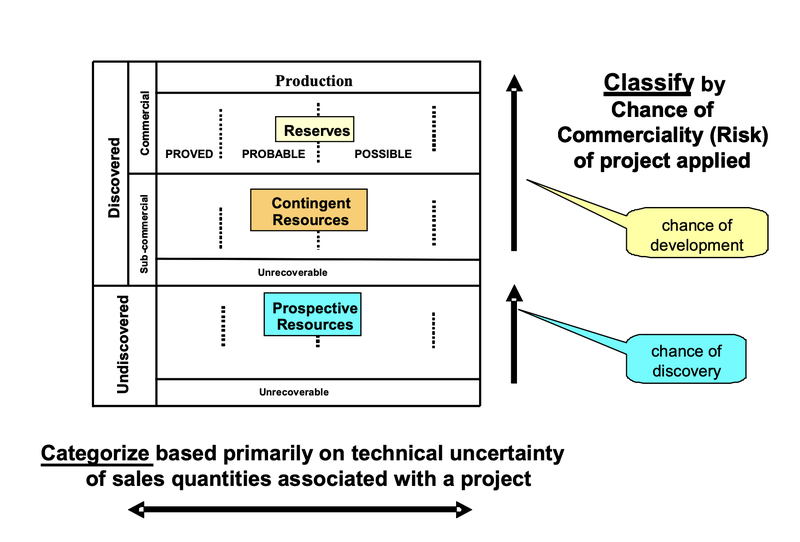

88E has already declared one contingent resource and has two more on the way.

Contingent would mean 88E can officially book discovered oil and gas quantities that have a chance of being developed.

🎓To learn more about oil & gas resources check out our educational article here: How to Read Oil & Gas Resources

We expect both to be catalysts for 88E’s share price, especially considering the market reaction to similar newsflow from 88E’s Alaskan neighbour Pantheon Resources.

Over the last few months Pantheon’s put out resource updates and has seen its share price almost 4x.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think that over time the market may start to close the gap between 88E and Pantheon’s valuations - especially as 88E books its contingent resources over the second half of this year.

Along with the US assets, we think the market is also underappreciating the value of 88E’s onshore Namibian assets.

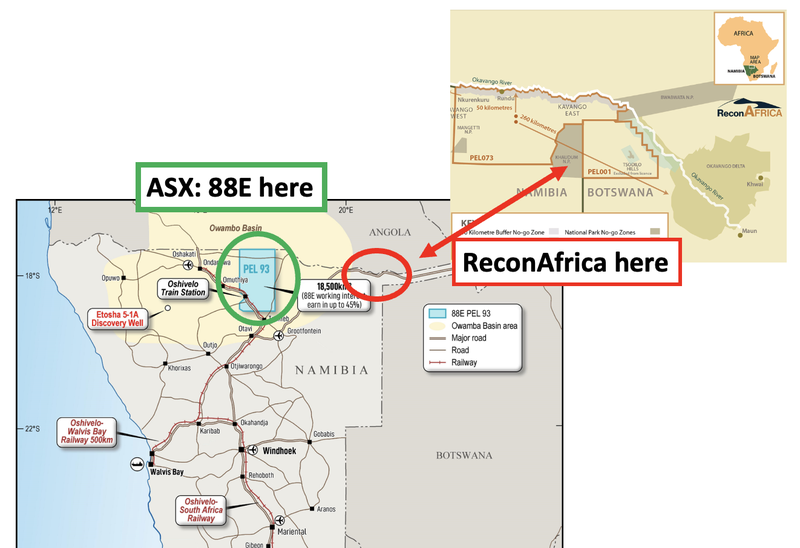

88E is also farming into 45% of a giant onshore Namibian block next door to ReconAfrica.

A few years ago, after the company drilled its first well, Recon’s market cap was >$1BN.

Recon is now planning multiple wells starting in June running through to the end of this year.

Right now Recon’s market cap is $267M.

88E is farming into its project at a similar stage to where Recon was before its big share price run back in 2020-2021.

88E’s licenses recently got renewed, and 2D seismic contractors have just been appointed.

88E is looking to have the seismic done in Q3 and the results in by Q4 this year.

The target for the project is for the first exploration well to be drilled in H2-2025.

While 88E does its work, it will be keeping a close eye on Recon Africa.

Our view is that before 88E’s first well, there is a good chance Recon’s activity will increase the look-through valuation of 88E’s project.

Over the next 6-12 months we have 4x potential major catalysts to look forward to from 88E’s - which don't require large cash expenditures:

- Two contingent resources from 88E’s recent discoveries in Alaska, USA - expected before the end of this quarter. Resource newsflow is what re-rated Pantheon Resources by starting last year.

- Potential commercialisation deals on 88E’s US assets - farm-out/JV deals on either its Phoenix/Leonis projects.

- 2D seismic results from 88E’s Namibian asset - which 88E has already paid for and will be completed in Q3-4 2024.

- Recon Africa’s drill programs in Namibia - any success from these could increase the look through valuation of 88E’s assets.

Following a recent placement that raised $9.9M (adding to the $17.5M cash in the bank at 31 March) we think 88E should be able to see through most of the above catalysts without having to tap capital markets again.

Especially considering the potential cashflows from the company’s Texan producing assets.

Following the successful flow tests and a forward work plan for Namibia, it's time we re-visited our 88E Investment Memo.

Today, we are publishing our new 88E Investment Memo detailing:

- Why we are Invested in 88E

- Our long term Big Bet - what we think the upside Investment case for 88E is.

- The key objectives we want to see 88E achieve

- The key risks to our Investment thesis

- Our Investment Plan

We remain Invested in 88E and hope the company can deliver our Big Bet over the medium term which is as follows.

Our Big Bet for 88E is as follows:

“88E re-rates to a $500M market cap after commercialising its Alaskan assets (through a takeover or farm-out deal) OR by making a discovery at its Namibian asset”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our 88E Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Re-rate from Namibian asset?

Our view is that over the next 18 months, 88E’s Namibian asset will become a big part of the company’s story.

At the moment, we think the market is paying close to zero attention to this assets.

88E is farming into up to 45% of a huge onshore block in Namibia, in the same region as TSX listed ReconAfrica.

ReconAfrica holds ground to the east of 88E and only a few years ago was capped at >$1BN.

From 2019 through to 2021 Recon went from licence renewals to its first drill program.

During that period Recon rallied from a COVID low of ~CAD$0.30 to a share price >CAD$12.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So the big run up in Recon’s share price started when its licence was renewed in early 2020 through to its first well in April 2021.

We think 88E is exactly where Recon was back in early 2020.

88E recently got its licence renewed and is about to kick off a 2D seismic program.

By the end of 2024, the seismic is expected to be done.

In the 2nd half of 2025, 88E expects to drill its first well.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

As mentioned earlier Recon briefly hit a market cap >$1BN.

We are hoping that in the lead up to 88E’s first well (and hopefully into good results) 88E’s share price can go on a similar run.

Especially considering 88E’s current market cap at $86M.

Between now and then we think there is also potential for the look through valuation of 88E’s asset to increase.

Recon is planning to drill multiple wells this year, starting in June.

In the lead up to Recons wells (and off the back of strong results) we would expect the market to automatically start bidding up ground in this part of Namibia.

(Source)

For now we want to see 88E run its seismic program, refine its portfolio of 10 leads and firm up its best drill target.

Here is why we rate 88E’s Namibian assets:

1. Huge ground position - ~70x the size of 88E’s Project Phoenix in the North Slope of Alaska, USA. The project is large enough to host a large resource base.

2. Namibia’s fast developing oil and gas industry - recent giant discoveries offshore by TotalEnergies and Shell have put Namibia on the map. Namibia being touted as the next Guyana where US supermajors Exxon and Hess are making discovery after discovery.

3. Namibian onshore peer re-rated by over 40x - ReconAfrica drilled its first well at its onshore Namibian project back in 2021. Between 2020 and 2021 Recon’s share price went from CAD$0.30 to CAD$12.50+.

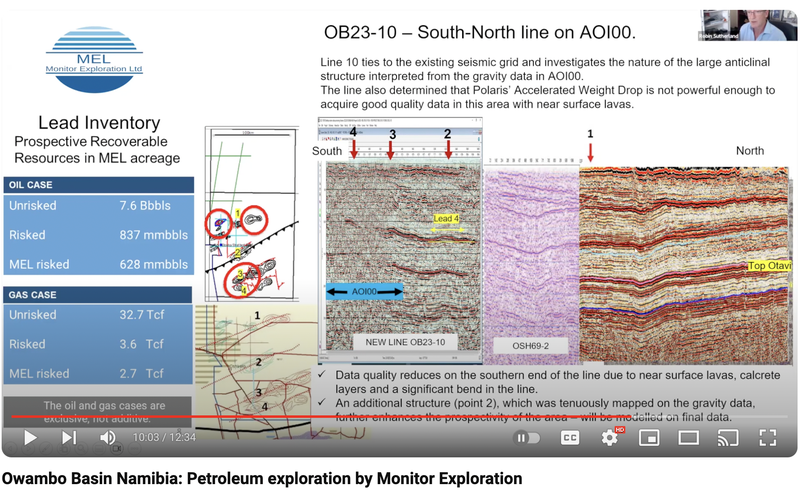

4. Project vendors linked to Invictus Energy (ASX: IVZ) - IVZ director Robin Sutherland is a part of the team doing the deal with 88E. Robin was also involved in EnergyAfrica, which sold to Tullow Oil for $500M in 2004 and then again with Tullow Oil as it went onto make discoveries across East Africa.

See the Monitor guys run through a pretty detailed presentation on the assets that 88E is farming into here:

(Source)

5. Early stage with plenty of upside - 88E is getting in on the project at a very early stage. There is scope for 88E to run seismic surveys, define a large prospective resource and drill target, then drill over the next 12-24 months.

6. Strategically located - 88E’s Namibia asset sits next to one of Africa’s largest economies, South Africa, which is looking to replace its retiring coal-fired energy generation fleet.

A re-rate from the US assets?

As for 88E's US assets...

So far we think the Hickory-1 well has ended up being 88E’s most successful drill program.

While the share price hasn't really reflected the progress at a fundamental level, 88E has managed to:

- Make discoveries across two reservoirs

- Flow oil to surface from both reservoirs

- AND has already put out 88E one contingent resource...

The next major catalyst for the US assets will be the booking of two contingent resources for its new discoveries.

That's where we think 88E could deliver major catalysts that could help move 88E’s share price.

Resource newsflow from 88E’s neighbour Pantheon Resources kicked off the rally in its share price.

Pantheon has re-rated by ~400% off the back of resource newsflow over the last ~12 months:

88E expects the two contingent resources to be delivered in the second half of this year - we think these could impact 88E's share price.

After the resource newsflow, 88E will start examining the best options for commercialising the assets — either through farm-outs/JVs or through a capital-light development option.

88E is also working up its Leonis asset, and it has confirmed it is pursuing a “targeted farm-out.”

In a recent presentation, 88E mentioned that “multiple parties” were “engaged in data room review” for the asset - so this could be a surprise catalyst to drop at any time.

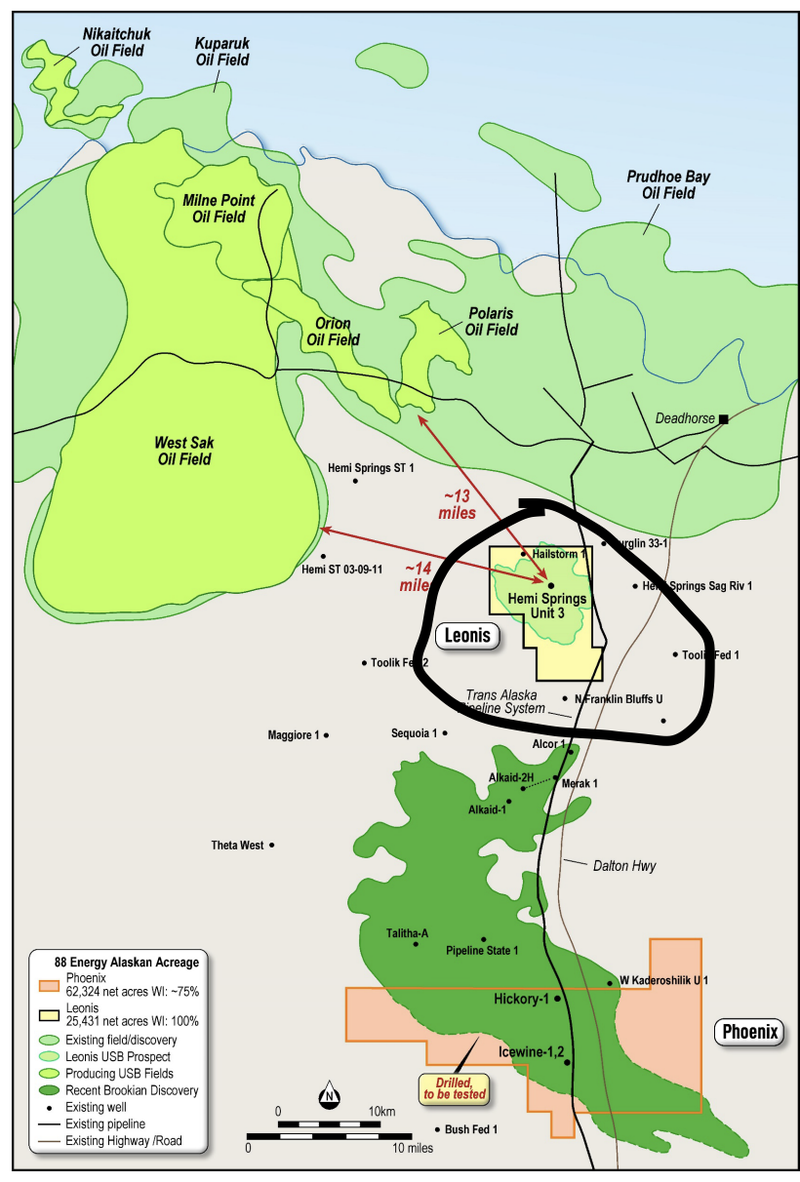

88E’s Leonis asset sits on ~25,600 contiguous acres immediately south of Prudhoe Bay - the USA’s biggest-ever oil discovery.

88E picked up Project Leonis in April last year and has spent most of the last 12 months reprocessing existing seismic data AND reanalysing data from a historic well inside the acreage.

88E already has old well data showing ~200 feet of pay from the project's main reservoir target so there is a good chance the numbers will be relatively strong.

Right now the focus for that asset is to get a maiden prospective resource estimate done inside H1 2024 followed by some sort of farm-out deal.

See our latest deep dive on 88E’s Project Leonis here: Will 88E drill Project Leonis next? Watch for a farm-out

Over the next 6-12 months, we want to see 88E show the market the commercialisation pathway for its US assets looks like, either through JV/farm-out deals or studies on a capital-light development option.

To follow the story over the coming 12-24 months, below is our new 88E Investment Memo.

Our new 88E Investment Memo

With 88E now finished drilling and flow testing its Project Phoenix asset on the North Slope we think now is a good time to reset our Investment Memo.

Check out how 88E performed relative to our previous memo here.

Today we will be launching our new 88E investment Memo where you can find:

- Why we are Invested in 88E

- Our long term Big Bet - what we think the upside Investment case for 88E is.

- The key objectives we want to see 88E achieve

- The key risks to our Investment thesis

- Our Investment Plan

88 Energy (ASX:88E) Investment Memo #3

Memo Opened: 20 May 2024

Shares Held at Open: 68,888,890

What does 88E do?

88 Energy Ltd (ASX:88E | OTC: EEENF) is an oil and gas exploration company with projects on the North Slope of Alaska and onshore Namibia.

What is the macro theme?

The last decade has seen massive underinvestment in new oil and gas projects in favour of renewable energy.

We think the sector is headed toward a medium-term supply/demand imbalance and expect oil and gas prices to remain elevated over the next 5-10 year period.

88E’s assets sit in the salem region as the USA’s biggest oilfield and in a part of the world that is emerging as one of the world’s most exciting oil and gas provinces.

Our 88E Big Bet -

“88E re-rates to a $500M market cap after commercialising its Alaskan assets (through a takeover or farm-out deal) OR by making a discovery at its Namibian asset”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our 88E Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

8 reasons why we are Invested in 88E -

- Projects in the North Slope, Alaska in the USA - 88E holds ground in one of the oiliest places in the USA. The North Slope is home to the USA’s biggest ever onshore discovery (Prudhoe Bay) which has produced the equivalent of ~12 billion barrels of oil since discovery.

- 88E has confirmed discoveries - 88E made two discoveries with its 2023 drill program on the North Slope of Alaska, It has proven flowing oil from two reservoirs

- Nearology to Pantheon Resources - One of 88E’s projects in the US is bordering Pantheon Resources which is working up the same reservoir systems 88E has on its ground. 88E is trading at a fraction of Pantheon’s market cap.

- Namibia’s fast developing oil and gas industry - recent giant discoveries offshore by TotalEnergies and Shell have put Namibia on the map when it comes to new oil discoveries. Namibia is being touted as the next Guyana where US supermajors Exxon and Hess are making discovery after discovery.

- 88E is farming into an onshore Namibian asset next door to Recon Africa - 88E is farming into a 45% interest in ground in the same region as Recon Africa. The ground was picked up in 2018, well before any of the major discoveries made in offshore Namibia.

- Namibian onshore peer re-rated by over 40x - ReconAfrica drilled its first well at its onshore Namibian project back in 2021. Between 2020 and 2021 Recon’s share price went from CAD$0.30 to CAD$12.50+.

- JV partners on the Namibian assets are linked to Invictus Energy (ASX: IVZ) - IVZ director Robin Sutherland is a part of the team that are JV’ed with 88E in Namibia. Robin was also involved in EnergyAfrica, which sold to Tullow Oil for $500M in 2004 and then again with Tullow Oil as it went on to make discoveries across East Africa.

- Underinvestment in global oil and gas exploration - The transition to green energy technologies has meant investment capital has shunned fossil fuel investment opportunities. In the short to medium term, the world still needs a well balanced supply of fossil fuels to ensure an abundance of energy sources for countries all around the world.

What we want to see 88E deliver

Objective #1: Contingent resource estimates at Project Phoenix, USA

- We want to see 88E put out contingent resource estimates for its two recent discoveries.

Milestones

🔲 Contingent resource estimate #1 (SFS Reservoir)

🔲 Contingent resource estimate #2 (SMD Reservoir)

Objective #2: Farm-out/development studies for Project Phoenix, USA

- We want to see 88E layout the commercial pathway for Project Phoenix either through a farm-out/JV deal or via economic studies

Milestones

🔲 Farm-out/JV MOU

🔲 Binding farm-out/JV deal

🔲 Capital light development studies

Objective #3: Farm-out Project Leonis, USA

- We want to see 88E announce a maiden prospective resource number and sign a farm-out deal which sees a partner fund a well for the project.

Milestones

🔲 Maiden prospective resource estimate

🔲 Farm-out/JV MOU

🔲 Binding farm-out/JV deal

Objective #4: Firm up drill target at the Namibian asset

- We want to see 88E run the 2D seismic data acquisition program on its Namibian JV. Once completed we want to see 88E lock in a primary drill target for the project.

Milestones

🔲 2D seismic program starts

🔲 2D seismic program completed

🔲 2D seismic results & interpretation

🔲 Maiden prospective resource estimate

🔲 Primary drill target selected

What could go wrong?

Exploration risk

A large part of 88E’s project portfolio is still full of pre-discovery assets. There is always a risk that 88E fails to make a discovery on those projects which would in turn negatively impact 88E’s share price.

Commercialisation risk

88E has now flagged to the market that it is pursuing multiple farm-out deals across several of its US assets. If 88E is not able to lock in a farm-in agreement it may be forced to self-fund the development of these assets. If 88E isnt able to deliver successfull farm-out deals its projects could stay stranded until a capital partner is found for them.

Funding risk

88E will at some point need to raise capital to fund the drilling at its Namibian asset as part of its earn-in agreement. Depending on the markets interest in oil and gas drilling events, 88E may be forced to raise capital before the major drilling event at a discount to its market price. Funding requirements could put downard pressure on 88E’s share price.

Market risk

88E is still predominantly focused on running high risk exploration programs on a recurring basis. There is always a risk that a market wide sell off will hurt 88E’s share price the most, given investors will look to withdraw capital from the high risk high reward investments in their portfolios first.

Geopolitical risk

The Namibian oil & gas sector is still fairly new in terms of maturity, there is always a risk geopolitical instability puts projects in country on hold. 88E’s US assets are also susceptible to geopolitical risk from an environmental perspective. If the US government were to put a moratorium on oil & gas exploration/development this could impact the value of 88E’s assets significantly.

Capital Structure

88E has almost 29 billion shares on issue at the moment. The bigger the share count, the higher the volatility in market cap and the harder it becomes to raise cash. At some point 88E may need to consider a consolidation which may put pressure on the company’s share price momentarily.

Our Investment Strategy

With our 88E Investment, we will follow our typical oil and gas Investment Strategy, where we Invest ahead of a drilling event and de-risk our position as the event approaches.

Our plan is to invest early, months before drilling, and hold as momentum increases in the story. We will look to increase our position in 88E over the coming months while the share price is depressed after the last result.

We then seek to free carry and take some profit at drilling. Generally we always look to hold a material portion of our position going into drilling results.

This suits our Investment strategy but may not suit yours.

Always seek professional advice when investing in speculative stocks like this one.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.