LCL hits high grade gold on first hole - 17 more to come

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 9,755,814 LCL shares and staff own 263,250 LCL shares at the time of publishing this article. The Company has been engaged by LCL to share our commentary on the progress of our Investment in LCL over time.

The gold price continues to hover around near all time highs of ~US$2,000/oz.

A couple of weeks ago we said if the gold price can hold or continue its recent run that small cap gold explorer’s share prices should start to run off their recent lows.

We haven't seen that happen yet - but it could only be a matter of time.

With gold explorers potentially about to swing back into favour in a big way, it could be a case of excellent timing for our gold Investment Los Cerros (ASX:LCL) who is drilling right now.

LCL is drilling a 18 hole, 3,000m campaign to determine the extent of the gold mineralisation already encountered on its project in Papua New Guinea.

Earlier this week LCL reported high grade results from its first drill hole - so far, so good.

LCL’s first diamond drill hole returned a 15.2m intersection grading 4.45g/t gold (from 138.2m deep), which sat within a broader interval of 76.4m grading 1.34g/t gold (from 106.9m).

The first drill hole confirms LCL’s theory that its gold mineralisation is continuous... and it could well be widespread.

PNG is one of the few regions on the planet that can still deliver new, big, high grade gold discoveries.

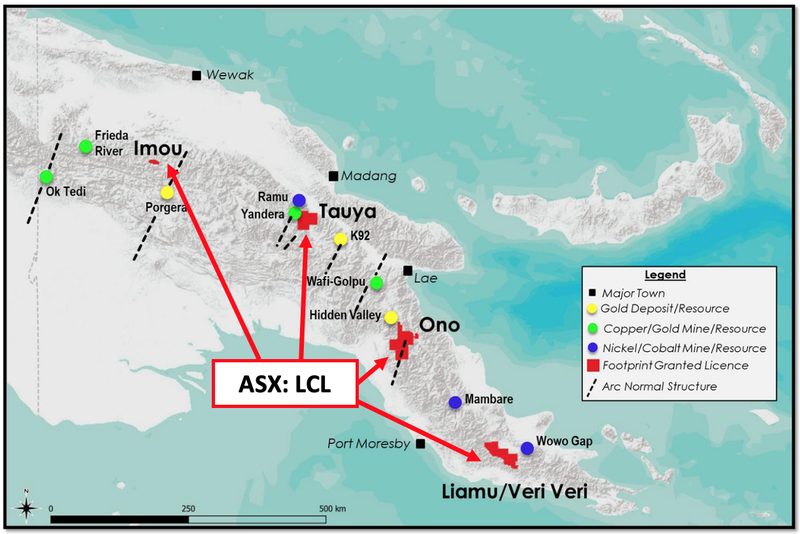

This gold project, one of LCL’s 5 new gold projects in PNG, is in the same structural belt as Harmony Gold’s producing Hidden Valley gold mine and the in development Wafi-Golpu copper/gold project owned by Newcrest and Harmony in a 50:50 JV.

This is LCL’s first assay result, and it has another 17 to go over the next few months. The next batch of assay results is due in mid-May.

Now all we need is more great LCL assay results AND the gold price to keep moving up.

Los Cerros

ASX:LCL

We have been Invested in LCL for a few years now, and after participating in the recent rights issue, we put together an Investment Memo on LCL. This Investment Memo is a high level overview of LCL, and includes why we Invested, and what we want to see the company deliver over the coming period - you can check out our LCL Investment Memo here.

LCL acquired its PNG projects late last year, which came with the vendor team who are experienced in country geologists, who now have ~10% of LCL shares, so are incentivised to deliver a big result for LCL shareholders.

This week LCL released its first assay result at the high-priority Kusi target as part of its 3,000m drilling program.

But LCL already had a pretty good idea of the types of high grades that it had on its hands.

The new intersection sits between two historical drill intersections of 20m at 2.89g/t gold and 35m at 3.04g/t gold.

The new result has come in above the 2.5-3.0g/t that would be expected given this hole was infill drilling.

Here you can see LCL’s current drilling as black lines, and the blue lines are historical drill hits:

What’s really important from this result is that LCL has now confirmed continued high grade mineralisation.

...and this is just from the first hole of 18 planned drill holes in the current drilling program.

Together, this first drill hole and the historical results provide proof of concept that the gold-copper oxide “skarn unit” here is continuous, potentially widespread, and could be capable of delivering large tonnage and grade.

A “skarn” is a type of rock that is typically found at the contact zone between intrusive rock and carbonate sedimentary rock. Skarns can be economically significant as they can host gold - as LCL is finding out.

LCL has identified two areas of interest for the current drill program. Rock chip samples from the second area have included grades of 61.3g/t gold, plus 18% copper, and 135g/t silver.

From Colombia to PNG - what happened?

We originally Invested in LCL a few years ago for its gold project in Colombia and were very happy with the management team’s execution to rapidly make a discovery and progress that project.

Unfortunately the political winds shifted in Colombia with a new government coming into power last year, who wanted to make some changes to exploration regulations.

In response to this (which we agree was the right thing to do) LCL reduced greenfield exploration activities until the new government’s updated exploration regulations are clear and in place, and has instead transitioned to focus on investigating potential development scenarios on its Colombian gold project.

While we wait for clarity on exploration in Colombia - LCL acquired these new PNG assets.

LCL adds the PNG vendors as shareholders & in-country team

The PNG projects were acquired from a team of highly experienced in-country geologists late last year.

The two vendors have a combined 60 years exploration experience, both having most recently served 8 years at Barrick Gold in PNG.

Now the vendors have circa 10% of LCL shares. We see this as a big alignment with other LCL holders.

That in-country experience and relationships will be invaluable for LCL moving forward.

We are backing the now expanded management team to deliver on this new project in PNG.

We like that LCL is not afraid to venture into frontier geographies, which fits our risk-reward profile very well.

LCL’s management team and our confidence that they can deliver in PNG is why we participated in the recent rights issue at 3 cents per share.

The LCL share price has been trading at multi-year lows while the market digested the project refocus, combined with a general negative sentiment in gold stocks - which also encouraged us to participate in the 3c capital raise because we believe gold will have a run in 2023.

LCL raised $2.2M in this rights issue, adding to its December quarter cash balance of $8.4M - so cash is no problem for LCL for the foreseeable future.

LCL has more than enough to complete its current 3,000m drilling program and other exploration at any one of its PNG projects that follow.

So in summary, we are backing the LCL management to deliver on their new projects in PNG and they have plenty of cash to do it.

Now all we need is the gold price to keep going up to new all time highs...

Gold price back to record highs

We can't talk about a small cap gold company without recognising the current disconnect between the price of gold and that of gold companies.

The gold price is currently trading at ~US$2,000/oz mark — just below its all time high.

Despite the high gold price, there has been little to no movement in share prices across the entire gold sector, from the majors already in production down to the gold juniors like LCL.

While the gold price is at new all time highs, many gold company share prices, and junior explorers in particular, are trading at or near all-time lows.

We expect this to change if the recent run in the gold price continues going higher and proves to be more than a short term gold price spike.

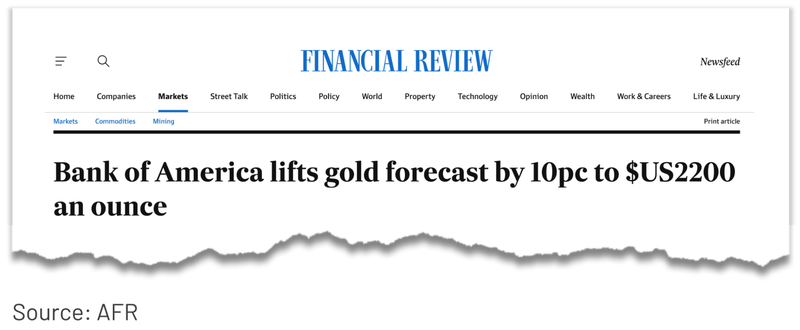

Indeed, a number of investment houses have been upping their target price for gold, the latest being Bank of America that has tipped gold to breach $2200/oz by year end.

A re-rate in favourable macro conditions has happened to LCL before.

Back in August 2020 the gold price hit all time highs - just as its first drilling campaign commenced at its Colombian gold project.

Then only a month later in September 2020, LCL confirmed a gold discovery at its Tesorito project.

Off the back of a rally in the gold price and some strong newsflow LCL’s share price rallied by ~300%.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

There’s little doubt that the then strength of the gold price helped increase market attention to LCL’s results at the time.

Now with the gold price back up around record highs, we hope to see a similar scenario play out.

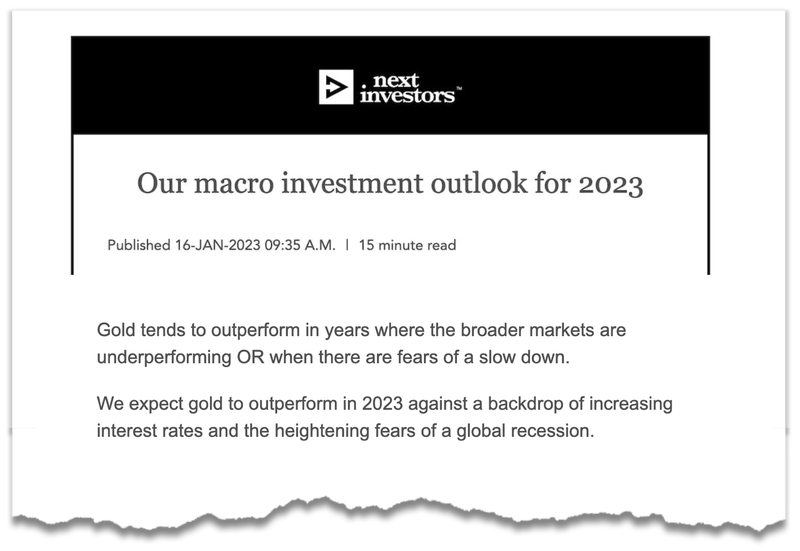

A higher gold price is also something we anticipated in our 2023 outlook back in January:

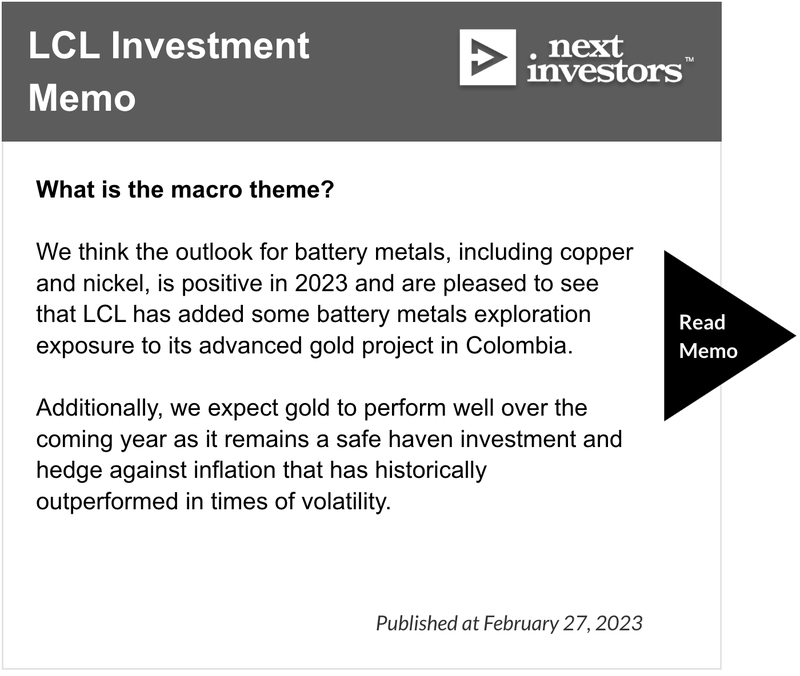

And in our LCL Investment Memo in February:

Our Big Bet:

“LCL to re-rate 1,000% off exploration success on its new PNG gold, copper, nickel projects or from developing its advanced gold project in Colombia.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LCL Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Gold in PNG - a quick overview

Focussing on PNG, whilst considered a somewhat risky jurisdiction to be operating in, it is considered “elephant country” - with the potential for big, new discoveries.

There are a lot of existing discoveries, producing mines, and majors operating in the area.

The Ono/Kusi project (one of LCL’s five in PNG) is located within the same structural belt as the Hidden Valley gold mine — an operating open pit gold and silver mine owned by South Africa’s $4.2BN-capped Harmony Gold Mining that has annual salable production of 151,00o.

This structural belt also hosts the Wafi-Golpu copper/gold project — an advanced exploration project in 50/50 JV between Harmony and $25BN Newcrest Mining that has gold production capacity of 415,000oz/year.

But it’s not just the majors that have found success here.

Small cap success story in PNG - can LCL do something similar?

Canada’s K92 Mining is one example of a company with projects in this part of the world that started out as a junior explorer and eventually re-rated into a billion dollar company.

K92 entered PNG in 2014 when it had a sub-CAD$100M market cap.

After restarting production at the Kainantu gold mine and making multiple high grade gold discoveries, K92’s share price rose from CAD$0.80 cents to CAD$6.80 per share today to trade with a CAD$1.6Bn (A$1.77BN) market cap.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Given LCL’s 3,867km2 landholding, the number of gold prospects, its current market cap of ~$25M, and the gold price trading near all time highs, we think there is potential for LCL’s share price to re-rate if the company makes a large gold, copper or nickel discovery.

We note that much of the project areas have never been prospected or assessed with modern mining techniques and understanding.

So for LCL, and its current market valuation, we think these PNG projects offer potential for significant upside.

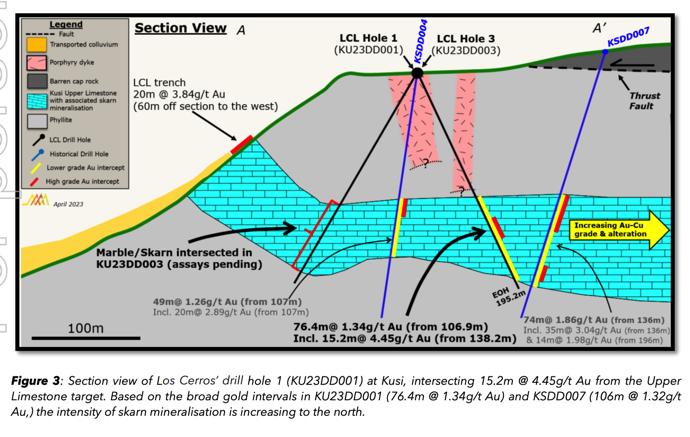

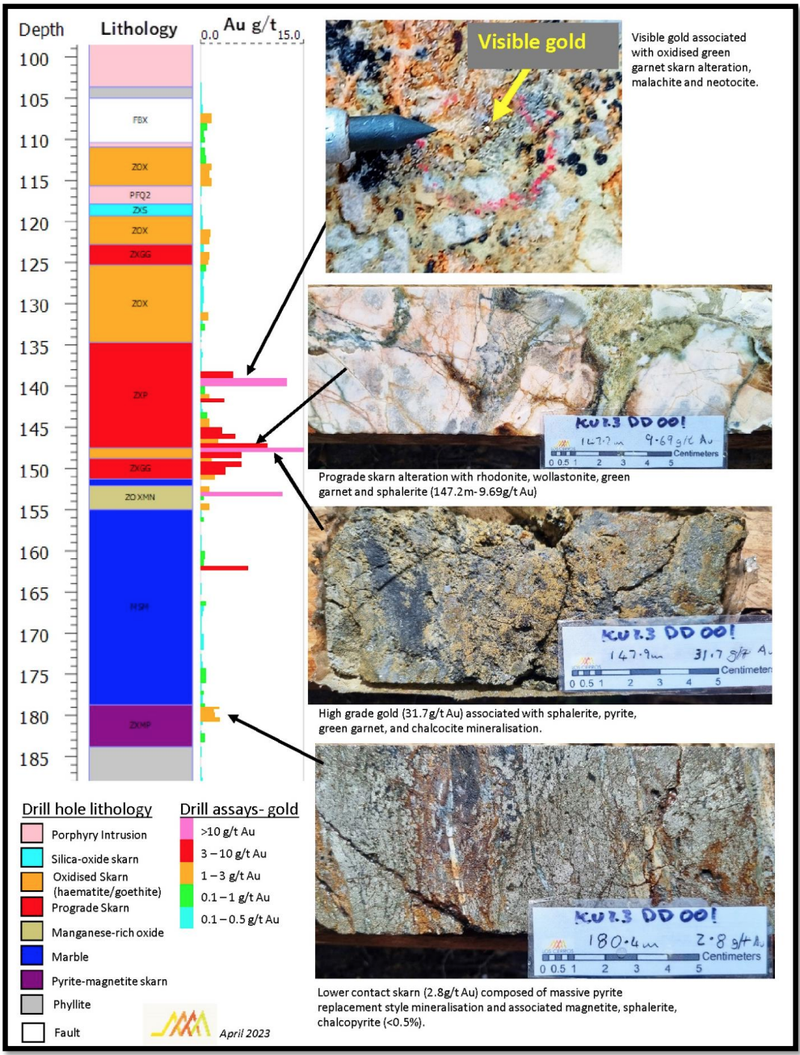

LCL’s first drill result - a deeper dive

LCL’s first diamond drill hole at its Kusi target returned a 15.2m intersection grading 4.45g/t gold (from 138.2m deep), which sat within a broader interval of 76.4m grading 1.34g/t gold (from 106.9m).

Here’s a geology strip log from the hole showing the various mineralisation types and gold grades along the depth of the drilled hole.

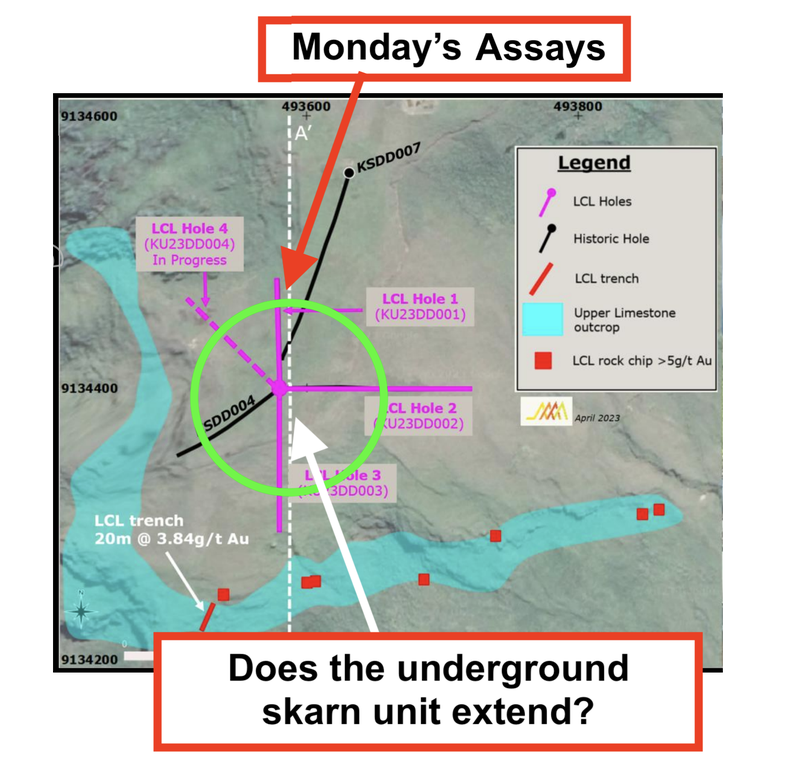

But the best way to get an understanding of what these results could mean at Kusi is to look at the results on the map.

The goal of this drilling was to see if the upper limestone skarn unit (think of this as the area that should hold high grade mineralisation) extends between the trench (which found more gold from surface) and the historical drill holes.

Here you can see the first diamond drill hole 1, for which assays are now in, located between the historical drill holes (KSDD007 & KSDD004):

LCL has also completed holes 2 and 3, so far we know that each hole intersected wide zones of upper limestone with skarn mineralisation at targeted depths (hole 4 still pending).

This was the area that holds high grade mineralisation that LCL was looking for.

Assays for drill holes 2 and 3 aren’t expected until late May, but our expectation is to see gold grades and intersections similar to those from the historical and new drill holes here.

This is also true for the rest of the holes to be drilled in this area of Kusi.

LCL now has four data points that define a ~300m zone of mineralised upper limestone skarn that reaches from its trench (20m at 3.84g/t gold) in the south to historical drill hole KSDD007 to the north.

This suggests that the upper limestone outcropping skarn unit (represented by the light blue band) has continuity of high grades and continues underground (to an extent still to be determined).

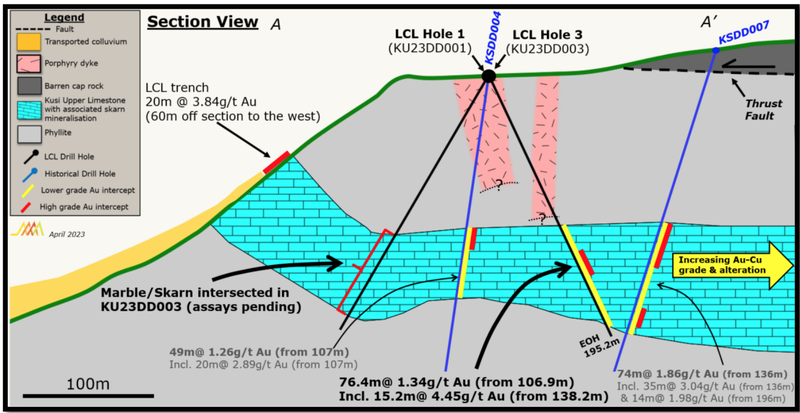

Here is a section view taken from the north-south white dotted line marked A-A’ above:

With LCL’s recent drilling, the company has confirmed that the area that high grade mineralisation (the light blue section) extends from where the outcropping starts at the trench to the historical drill holes.

LCL’s exploration continues

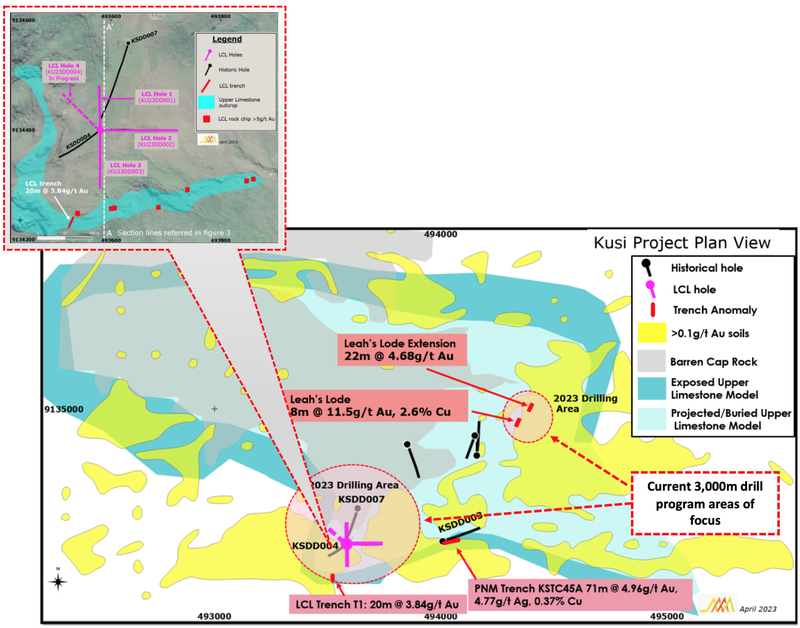

By zooming out we can see the area of recent drilling in a broader context - located amid all of the suspected mineralisation across a larger area at the Kusi Project:

Here you can see the current drill holes (pink lines) and gold in soils geochemical anomaly (yellow) with the modelled exposed “upper limestone” skarn unit (darker blue band) as well as the projected deeper Lower Limestone unit (light blue).

The outcropping upper limestone skarn unit appears to be quite extensive at Kusi. Initial drilling has confirmed that it continues under the surface - the extent of which remains unknown but could be very widespread.

With its ongoing 3,000m diamond drilling LCL will continue to test the oxidised skarn mineralisation within the upper limestone unit that was established from past drilling, trenching, and surface sampling.

LCL expects to drill 18 holes each spaced around 150-200m apart, across the two circled target areas above.

Alongside the current drilling program in those two areas, trenching and regional mapping is also ongoing at Kusi to see what can be found further afield.

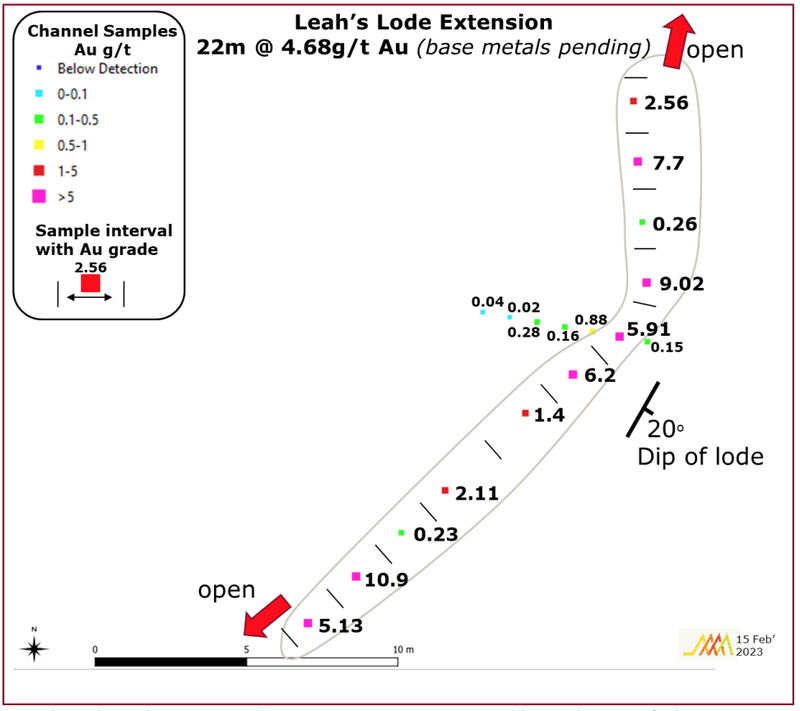

LCL’s second target area - Leah’s Lode

After drilling is complete at the current target area, later in the drilling program LCL will move to the second target area at Kusi - the Leah’s Lode Extension.

Rock chip samples from outcroppings here have included a massive grade of 61.3g/t gold, plus 18% copper, and 135g/t silver.

LCL also has two really good intercepts at this target.

Recent trench sampling along strike at Leah’s Lode averaged 22m grading 4.68g/t gold (base metals pending). While previous trench sampling returned 8m grading 11.5g/t gold, 2.6% copper, and 24g/t silver.

Here are channel sample gold assays from Leah’s Lode:

(Note trench orientation is along strike and therefore not an indication of width of the mineralised unit.)

Exactly where the holes will be drilled at Leah’s Lode has not been specified yet, but we would hope to see continuity of the grade and style of intercept those from the area currently being drilled.

Here is an idea of our pre-drill expectations at Leah’s Lode:

- Bull case: >2.5 g/t gold

- Base case: 1g/t - 2.5g/t gold

- Bear case: <1g/t gold

Given the extremely high grade rock chip sampling results here and samples from trenching, we are optimistic as to what drilling might uncover, and most importantly we want to see just how big the Kusi target actually is.

The current drilling program at Kusi, which includes Leah’s Lode, was the first objective in our LCL Investment Memo that we wanted to see LCL achieve this year.

What’s Next?

Kusi target

With the first four holes now drilled, LCL’s current 18 hole / 3,000m drilling program remains on schedule and on budget.

The next assay results from drilling are expected in around one month’s time, in the second half of May.

In addition to following up on historical drilling and trenching work to confirm the continuity of mineralisation, there are two more broad objectives of the wider exploration program at the Kusi target. 1. Regional scale potential

The first is to gauge the potential regional scale and gain an understanding of just how big the upper skarn unit is.

Running in parallel to the drilling program, trenching and regional mapping over a total area of approximately 3km x 1.5km is ongoing. This supports the concept that upper limestone skarn mineralisation extends well beyond the limits being tested by the planned 2023 drill program.2. Central copper porphyry

Secondly, LCL wants to gain a better understanding of the central copper porphyry because while porphyry deposits tend to be lower grade, they are one of the most attractive exploration targets due to their high tonnage and relatively easy open pit mining.

Continued drilling and surface work will be instrumental in locating the porphyry source.

Beyond Kusi...

We should keep in mind that the Kusi Target is only one section of the broader Ono Project. And that LCL has a multitude of prospects across its 3,867km2 of exploration claims across its five projects in PNG — Ono, Imou, Tauya, Liamu and Veri Veri.

Other PNG project areas

While LCL’s primary near term focus is on drill testing the high-grade gold-copper Kusi oxide skarn and then commencing fieldwork at Veri Veri, which LCL intends to drill test during the first half of this year after it finishes up at Kusi. Veri Veri is prospective for high grade nickel sulphide.

Outside of these two targets, the company has many others that it wants to advance concurrently. In order to do so while its own capital is largely being directed to Kusi, LCL is seeking joint venture partners.

The #3 Objective in our LCL Investment Memo was to see LCL secure JV partners to advance exploration works at its other PNG targets.

We look forward to news on this front.

Our LCL Investment Memo

Click here for our latest LCL Investment Memo where you can find a short, high level summary of our reasons for Investing including the following:

- Key objectives for LCL

- Why we are Invested in LCL

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.