Surprise, LCL’s Colombian Gold project might be coming back…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 9,755,814 LCL shares and staff own 14,285 LCL shares at the time of publishing this article. The Company has been engaged by LCL to share our commentary on the progress of our Investment in LCL over time.

The gold price looks like it’s about to break its all time record (in AUD).

...it’s now sitting at around ~$3,050 /oz.

And LCL just surprised us this morning with news that its giant Colombian gold project (that saw the LCL share price go from 3c to above 15c a few years ago) could be making a comeback...

A project everyone thought was paused after the 2022 change in the Colombian government.

In the meantime, our Investment LCL Resources (ASX:LCL) has been getting some excellent gold hits on their new gold project in Papua New Guinea.

Notably hitting a “spectacular” 52m @ 3.65 g/t gold in May, earlier this year.

So now we could have progress from LCL on both its “blue sky” PNG gold projects AND its original Colombian gold project.

We had originally invested in LCL for its gold project in Colombia back in 2020

So what happened?

LCL went from ~3c in 2020 to trade consistently above 15c for nearly two years on progressing its Colombian gold project.

The market loved it.

This gold project was rapidly moving towards development and across its Quinchia portfolio, LCL had 88Mt, grading 1.02g/t gold for a total of 2.6 million ounces of gold.

During this time the market valued LCL at ~$100M (it’s currently around $22M)

This ~$100M valuation was made possible by LCL’s discovery hole at Tesorito (porphyry) in September 2020, which saw the LCL share price tack on ~250% in a short space of time:

Unfortunately... in 2022, LCL’s giant Colombian gold project was effectively paused when a new Colombian government was voted in and introduced some uncertainty around mining projects...

The LCL price came back to ~3c.

BUT...

Today we got a big surprise.

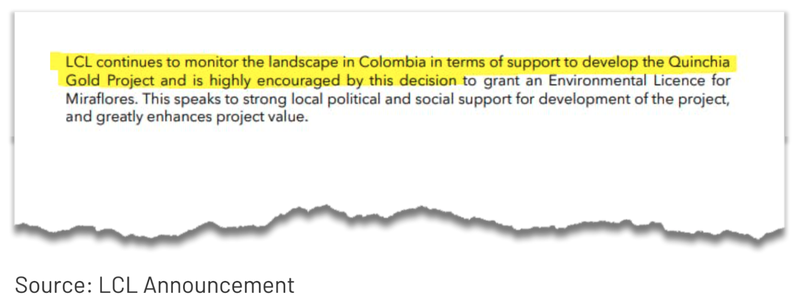

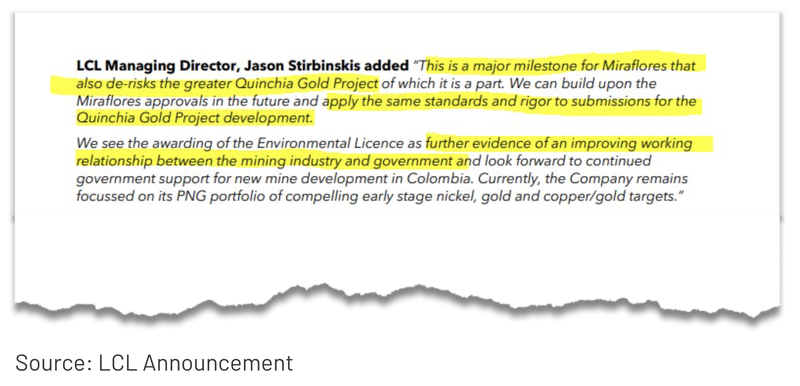

LCL’s environmental licence was APPROVED at its Colombia gold project which is the last major step before production is allowed.

(Source)

So could things be thawing in Colombia earlier than expected?

A few weeks ago another gold company in Colombia forked out ~US$60M for the remaining 50% stake of its project 260kms north east of LCL’s project

And another Colombian gold company, Aris Mining had its Environmental Management Plan for the underground portion of its project approved, which sits just 45kms northeast of LCL’s project.

We hope these are the first big signs that the new Colombian government has settled on its approach to mining in the country.

So we hope we can now expect more updates from BOTH the LCL’s Colombia gold project and LCL’s new gold and nickel projects in PNG.

(Source)

Now, the environmental licence granted today was over part of LCL’s larger deposit, Miraflores which sits within the larger Quinchia resource.

All was going well for LCL until there was a change of government in Columbia, which we think, is why LCL put the project on ice.

We thought that it would be years before the government figured out what it wanted to do with mining projects.

Obviously the market didn’t like this at the time...

Well, it now appears that the environment for advanced gold projects in Columbia is starting to thaw out a bit..

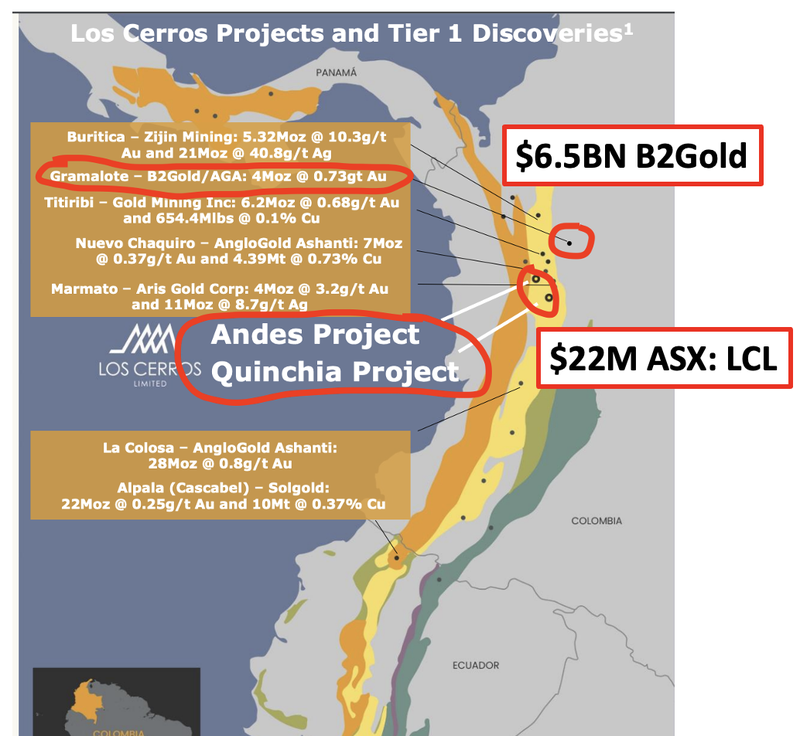

We also noticed that $6.5BN Canadian listed B2Gold just consolidated its ownership of the Gramalote gold project in Colombia which sits ~260km north-east of LCL’s project.

B2 paid ~US$60M for the remaining 50% stake in the project (US$20M upfront and US$40M in milestone payments).

(Source)

For some context - Gramalote has a ~4M ounce gold resource with gold grades of ~0.73g/t, LCL’s project has 2.6M ounce gold resource with grades averaging ~1.02g/t.

LCL’s resource is smaller but we think that with a bit of time and money invested into its project LCL could continue drilling out a resource that is comparable to some of the monster deposits in the region.

Once the project is big enough it wouldn’t surprise us to see majors start to take notice of it, just like Anglogold Ashanti had done back in April 2020 when it took a ~4.3% stake in LCL.

(Source)

Here is where B2’s project sits relative to LCL and some of the other major discoveries across Colombia:

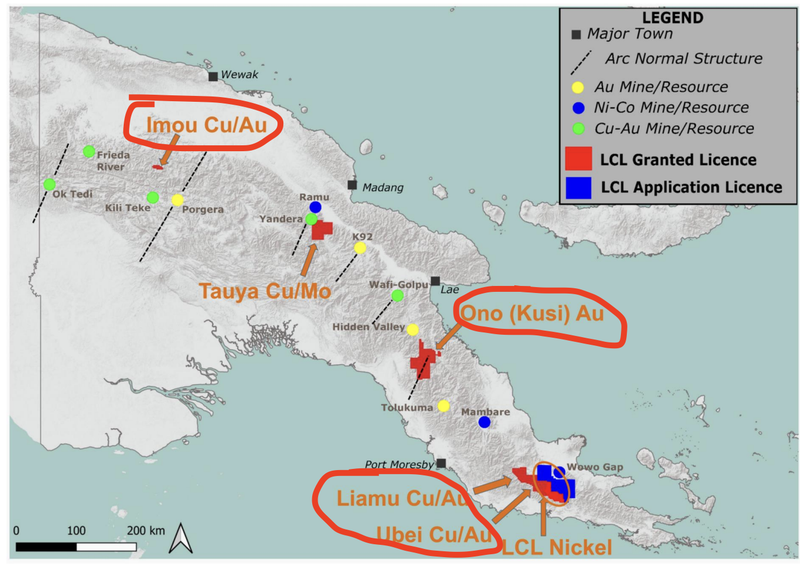

LCL’s PNG nickel projects (Blue sky exploration):

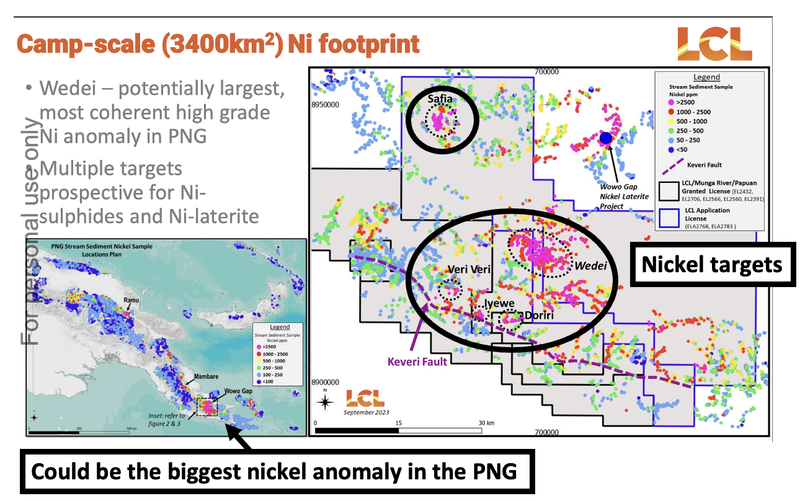

LCL has ~3,400km^2 of ground with multiple nickel exploration targets - one of which could be the biggest nickel prospect in the PNG.

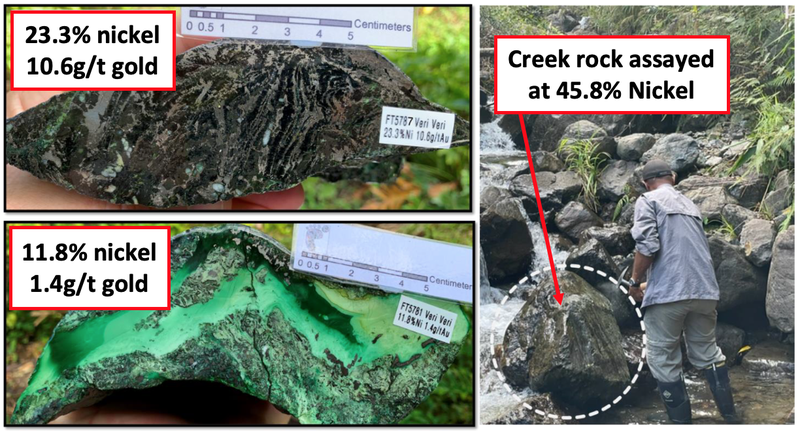

The focus for LCL so far has been its Veri Veri nickel target where LCL has been picking up nickel grades as high as ~45.8% in nickel sulphide boulders.

Initially the boulders were being found floating in a nearby creek but a few months back LCL found what could be the source for the nickel boulders picking up “in-situ” outcropping nickel sulphides grading as high as 13.4%.

We covered that news in a previous LCL which you can read here: Has LCL found the source rock of its nickel boulders at surface?

Now the focus is on doing some more field work including some airborne EM surveys, before drilling to see if LCL can make a new nickel discovery.

LCL’s PNG gold-copper projects (Blue sky exploration):

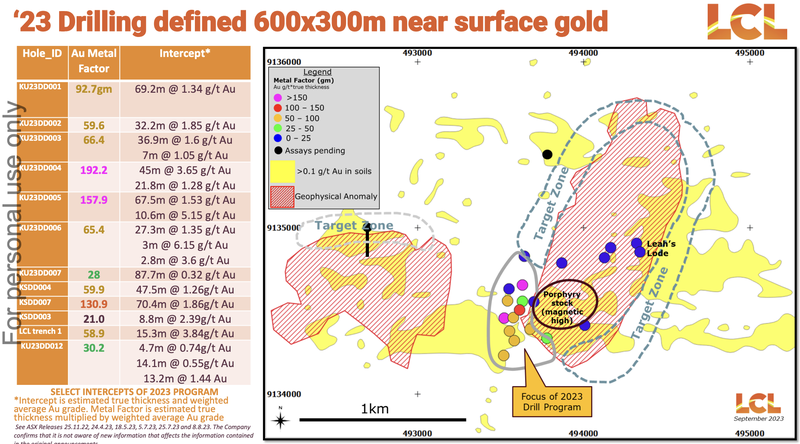

So far across its PNG projects, LCL’s focus has been its Kusi gold-copper project where LCL has done ~3,000m of drilling and hit a 52m intercept with gold grades of 3.65g/t.

At Kusi LCL now has a discovery sitting on a ~300m x 600m footprint with plenty of exploration upside.

At the same time, LCL still has a bunch of other copper-gold targets across its portfolio, which we think could become of interest in the future.

Of particular interest to us is the ~60km channel between its Liamou and Ubei targets.

Across those targets, LCL has undrilled EM and IP geophysical anomalies which could lead to the discoveries of entirely new copper-gold porphyry systems.

We are looking forward to LCL drilling these at some stage in the future.

So LCL has a portfolio of projects which include:

- Blue sky exploration potential - PNG projects where LCL could deliver company making nickel-gold-copper discoveries.

- Development stage with in ground resource - A development ready gold project in Colombia with a JORC resource of over 2.6m ounces of gold.

We think the depth in its project portfolio is what differentiates LCL from other companies in the market right now.

It also means LCL has two pathways to achieving our Big Bet, which is as follows:

Our LCL Big Bet

“LCL to deliver a 1,000% return off exploration success on its PNG gold, copper, nickel projects OR from developing its advanced gold project in Colombia”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LCL Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for LCL?

Field programs at nickel project in the PNG 🔄

Airborne electromagnetic (EM) geophysical surveys and get on ground for some sampling/mapping - these will help work out the best places LCL should focus its future drill programs.

Field programs across copper-gold targets in the PNG 🔄

LCL is also running field programs across its copper-gold targets in the PNG.

Most of this will be sampling/mapping work to work out the highest priority areas for future drill programs.

Joint Venture discussions 🔄

Potential farm-out/Joint ventures across LCL’s project portfolio both in PNG and Colombia.

What are the risks?

At present the three key risks relevant to LCL are, exploration risk, sovereign risk and funding risk.

Exploration risk at its earlier stage gold-copper-nickel projects in the PNG. Here LCL’s projects are all pre-resource and so there is always a chance LCL drills its prospects and makes no discoveries.

Sovereign risk at its far more advanced Colombian gold project. Here, there is a risk that project development is slowed due to government pushback/environmental permitting.

In terms of funding risk we are also conscious of LCL needing to raise capital OR bring in a farm-in partner to continue to explore its projects. Given LCL has no revenues to fall back on there is always a chance LCL decides to tap the market for additional funding.

See the key risks we listed in our LCL Investment Memo here.

LCL takes ESG seriously, which may have helped with today’s news

LCL has made ESG a big part of its wider program of works in Colombia which we think may have helped with today’s news.

We note that LCL has received the Colombian Gold Symposium’s ESG award in November 2022:

(Source)

This is important work, because every mine needs a social licence to operate and LCL’s ESG initiatives contribute to the company having a beneficial presence in the community.

In turn, reinforcing local communities' desire to have LCL operate in the area.

Learn more about LCL’s ESG initiatives here

Our LCL Investment Memo

Click here for our latest LCL Investment Memo, where you can find a short, high level summary of our reasons for Investing, including the following:

- Key objectives for LCL

- Why we are Invested in LCL

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.