LCL finally hits the edge of its giant gold system - JORC resource estimate coming.

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 3,210,000 LCL shares at the time of writing this article. S3 Consortium Pty Ltd has been engaged by LCL to share our commentary on the progress of our investment in LCL over time.

Our gold investment Los Cerros (ASX:LCL) has its hands on what appears to be a monster gold system at their main project, Tesorito in Colombia - and it just kept on getting bigger.

They found a gold rich porphyry at Tesorito in September 2020, leading to the share price tripling, and for the last 18 months have been drilling and drilling and drilling, trying to find the edges of the gold system.

But they kept on turning up more and more gold.

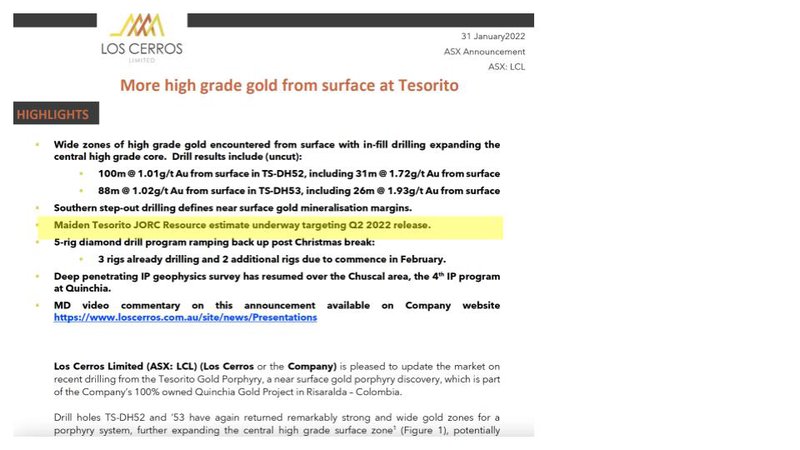

A few days ago LCL announced their latest batch of drill results (including one that ranked top 10 for the week for any ASX company)...

But more importantly they announced that they have FINALLY found the southern edge of their seemingly never-ending gold system.

Now that we are getting closer to finally understanding just how big this gold system could be - we want to see two key things next from LCL:

- Drill in between their two gold systems to see if they are connected as one giant gold system.

- Release a “JORC estimate” - a size and grade (how much gold) and level of confidence (inferred, indicated...) for LCL’s main project. “JORC” refers to the mining industry's official code for reporting mineral resources and reserves, and is trusted by investors and markets.

The key question on everyone’s minds remains - just how big is their main gold system? And when can we expect that JORC resource to be delivered?

Today we’ll deep dive into both.

We’ll also explain why we believe we are entering a period of Mergers and Acquisitions activity in the gold sector, where large, cashed up gold companies are going to start buying up smaller companies with proven gold deposits.

We are expecting big things from LCL - here is our LCL investment memo for 2022 covering:

- Key objectives we want to see LCL deliver in 2022

- Why we continue to hold LCL

- The key risks

- Our investment plan

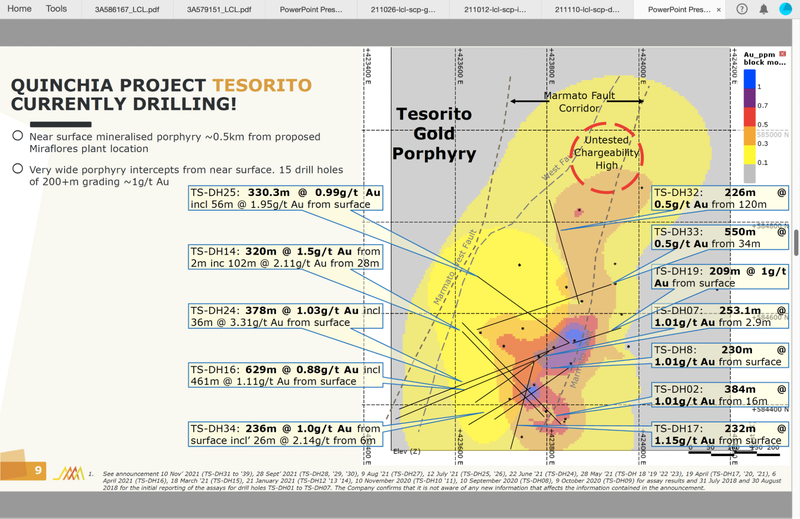

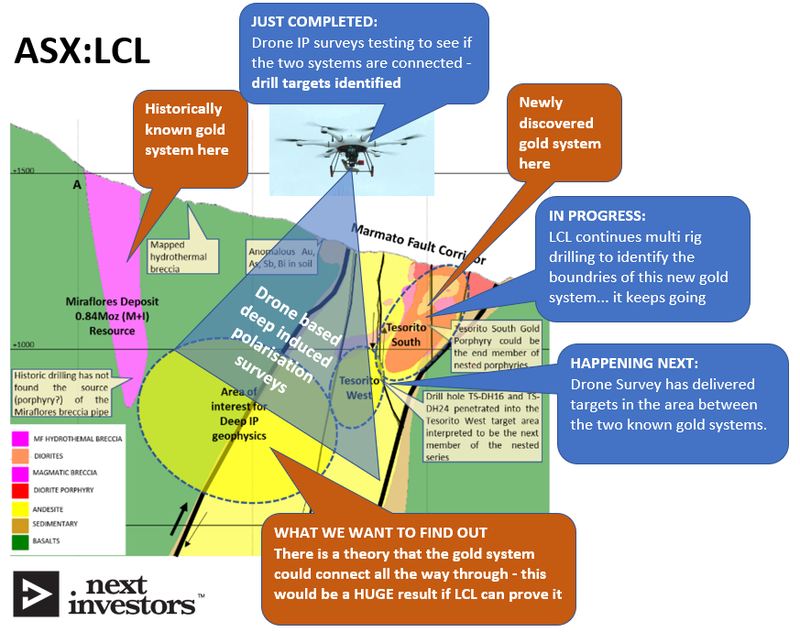

We’ve been very keen to see just how big LCL’s main gold system would become, ever since LCL’s spectacular discovery in September 2020 returning 230m at 1.0 g/t gold from surface.

You might recall that this particular drill hole led to LCL’s share price tripling within the space of a couple of weeks.

LCL calls that particular project Tesorito or “little treasure” and it's turning out to be more of a ‘big treasure’ given the amount of successful drilling there.

Drilling is only all well and good up to a point though, now we really want to see the JORC resource at Tesorito, which is the number one thing we’d like to see this year from LCL.

Ever since this discovery, we’ve had to be patient while LCL kept drilling... and finding more gold... and drilling... and finding more gold... consistently for the better part of the last 18 months, attempting to find the edges of this gold system.

LCL increased the number of drill rigs on site from two to five to speed up this delineation process.

On Monday, LCL announced the latest batch of drill results, which included their customary spectacular hits (2 holes exceeding 88 metres and grades over 1 g/t Au, which is considered high-grade for porphyry systems).

For a useful commentary of the announcement, direct from the horse’s mouth so to speak, LCL’s managing director Jason Stirbinskis hosted this recent video presentation, which includes the first 3-D modelling of the main project that we’ve seen.

What stood out to us is that LCL has now defined the southern and northern edges of their main project. What this means is that the company is now comfortable that they have not missed any massive areas of interest along those edges.

Translation - we’re now ready to move into the JORC resource estimation stage.

Finally!

This is important because “size matters” for gold juniors - the easiest, first pass way that pre-production companies are typically measured and compared against each other is by the size and grade of their resource base.

Of course, other factors are to be considered, like depth, metallurgy, jurisdiction, topography...etc - but these are the realm of scoping and feasibility studies, whereby the financial returns of commercialisation are considered.

We’ve been invested in LCL since early 2020, just prior to the company devising its maiden drilling program for Tesorito. We increased our holdings at 16 cents per share during LCL’s previous capital raising in August 2021, which raised some $20m and attracted two of the world’s biggest gold funds to the register.

We believe that those big funds are interested in seeing whether LCL has a tier-1 gold asset on their hands, the first step of which is figuring out how big the main project is.

So just how big could Tesorito be?

AND when can we expect that JORC resource to be delivered?

So, what to expect from LCL’s star gold project?

We are excited about the forthcoming JORC resource at Tesorito, given just how extensive the gold mineralisation revealed by drill results has been to date.

Tesorito has now delivered 14 intercepts extending over 200 metres and grading ~1 g/t Au or better - indeed, just one such drill result would typically be considered ‘company making’ for a junior gold explorer, so to have so many clearly points to Tesorito’s upside potential.

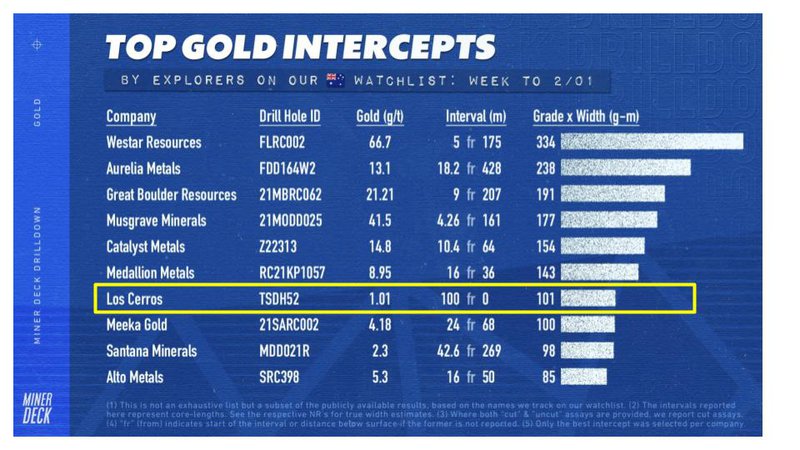

In Monday’s announcement, LCL delivered yet another “top 10 best drill intercept of the week”, as tracked by Miner Deck.

LCL also has no issues to fund its activities for the year ahead and beyond, with ~$19.4M cash in the bank to start 2022.

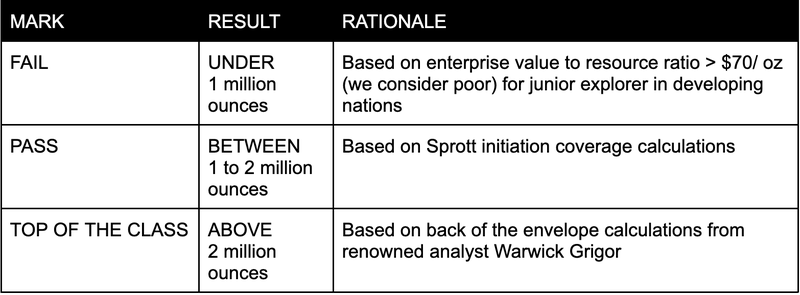

So, just how big will it be? - here’s our ranking system

We’re not geologists, but we do read what the experts say, and so have devised our own “ranking system” as to our expectations for the total size of the JORC estimate at Tesorito.

Here are our expectations for the JORC resource estimate, in ounces of gold:

As announced on Monday, LCL has commissioned a JORC Resource estimate for release in Q2 2022 - i.e. sometime between April and June this year.

Besides providing us our first official indication of how big their main project is, LCL will also progress with metallurgical and mining scoping studies, which will also consider synergies between Tesorito and the advanced Miraflores project such as shared mineral processing and infrastructure.

Pullback in gold stocks? Time for mergers and acquisitions by cashed up majors.

An overall theme for 2021 was that commodity prices went parabolic one after the other.

These parabolic moves resulted in commodity prices re-basing at a much higher level from where it was for most of the previous decade. The market then responded by pouring capital into exploration as well as the bigger producers.

One of the commodities that didn't join in on these parabolic moves has been gold, with poor investor sentiment plaguing the sector last year (gold equities broadly stagnated in 2021, from producers through to explorers).

Whilst sentiment may have been gloomy for the precious metal, the actual commodity price traded at around the US$1,800 per ounce mark for much of the year - to put that into perspective, that is only ~10% off all-time highs of ~US$2,100 per ounce.

We think that that healthy pullback and consolidation from all-time highs is being well reflected broadly in the market valuation of gold companies, which seem to have been overly punished.

Let’s look at Northern Star Resources, among Australia's biggest gold success stories of the past 2 decades, which moved to an all-time high share price of ~$17 per share coinciding with the commodity highs. However, it is now trading at $8.42 per share - that is down almost 50% from it's all time high, despite the commodity price dropping only ~10%.

Another example is Newcrest Mining which was trading at ~$37 per share during the big move in gold in mid-2020 and is now trading at $22 per share - i.e. down almost ~40% from its all time high.

Is this being reflected internationally too?

Taking a look at Barrick Gold, which in mid-2020 was trading at ~$30 per share, yet is now trading at $19 per share. That is down almost 37% on-market.

We think the market valuations of these gold producers have decoupled from fundamentals. Whilst several of these producers are experiencing some operational cost-inflation (e.g. staffing issues related to COVID and supply chain disruptions), most are still enjoying very healthy margins and producing record free-cash flows

Returning to Northern Star, the company stated in their most recent quarterly report that their all-in sustaining costs of production was US$1,200 per ounce, leaving them with a very solid US$600 per ounce margin on every ounce of gold produced.

What is interesting is that despite somewhat tepid gold market investor sentiment, many of the producers continue to deliver very strong profits. With margins remaining strong, yet reserves depleting, one quick and easy way for these companies to increase their resource base is through mergers and acquisitions.

So how does this relate to LCL?

This inordinance between the miners and the explorers is even worse.

Looking at LCL, trading peaked at ~21 cents in late 2020 following its Tesorito discovery. Yet, despite more than a dozen excellent assay results delivered since, as well as the additions of several renowned institutional funds to the register, trading has returned to near 10 cents of late, not far off the levels of pre-discovery LCL.

Some of the explorers that have been overly punished in the market last year are likely now becoming the targets as value propositions of M&A activity by bigger companies that are sitting on record cash-piles and continuing to produce record free-cash flows.

Producers face the age-old issue of ever depleting gold resource/reserve bases and they need to replace this either through mergers, acquisitions or through higher-risk exploration.

The bigger gold companies have historically shunned greenfields exploration work and tend to leave the discoveries for the juniors - preferring to pay up at a premium once a potential large discovery is already made (ie de-risked).

Take for instance ASX-listed Ramelius, which took over its Kalgoorlie neighbour Apollo Consolidated last year, so as to integrate the 1.1Moz Lake Rebecca project into its own asset base.

Apollo was in the middle of an extensive drilling program and the results were looking very promising - enough to warrant a resource upgrade. As the potential became obvious and the project's scale was de-risked, Ramelius swooped in. They weren't the only ones interested either, as WA miner Gold Road Resources also put in an offer - ultimately Ramelius won the takeover menage de trois.

So, in the end, Ramelius took-over Apollo for ~62 cents per share (split cash and equity in Ramelius), or an enterprise value of ~$148M. Giving the transaction an EV/ Oz of gold resource of $134 per ounce.

Before the takeover Apollo was trading at ~35c, so the takeover came at an almost 80% premium to its share price pre-takeover.

The play-book for Apollo was:

- Prove out a JORC resource - (Putting themselves on the radar of bigger producers)

- Show scale and resource growth potential - (Drawing more appeal for those watching)

- Commit to an aggressive drilling strategy to identify that resource - (Further grow the asset without need to commit to project financing, further appealing to those watching).

If we look at LCL in terms of the above playbook, we’d regard the company as progressing towards the end of this process.

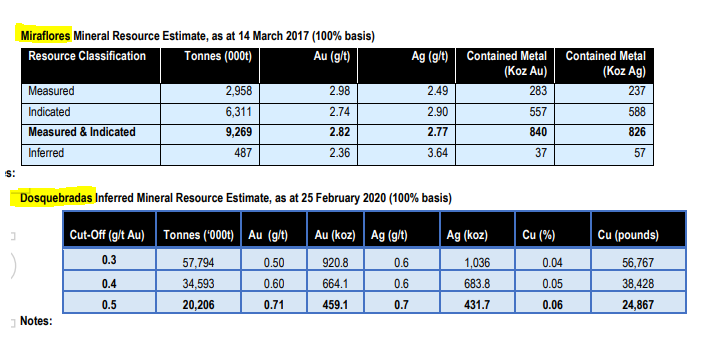

LCL already has a JORC resource at its Miraflores deposit down the road from Tesorito - this contains ~877k ounces with a reserve of 457k ounces. It also has a JORC resource at the Dosquebradas deposit totaling some 459k ounces.

So, at present, combined LCL’s projects have a current JORC gold resource of ~1.34M ounces.

In a few months, LCL will add Tesorito to the mix, and that’s when the real excitement should begin.

This is the first part of the equation we mentioned above - “proving out a JORC resource”.

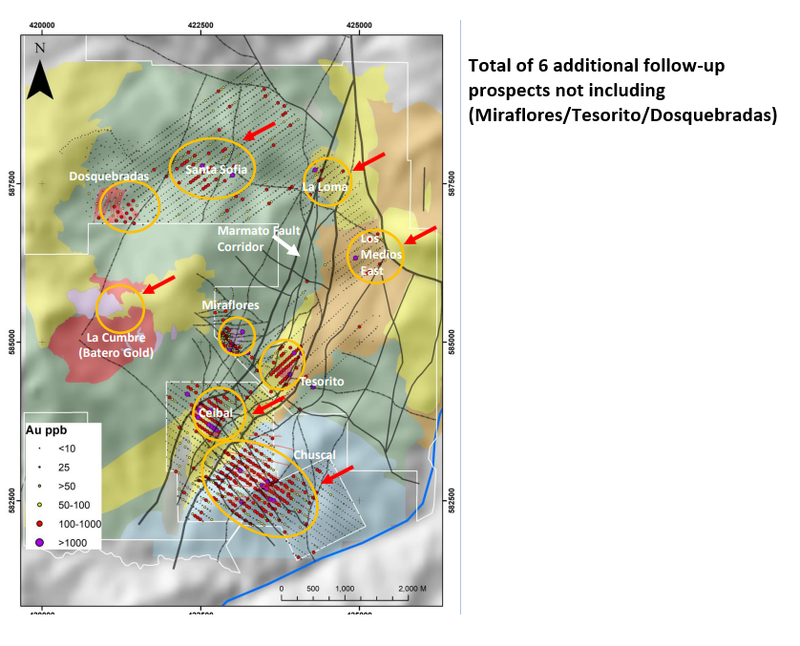

Step 2 of this process is “showing scale and resource growth potential”. Our belief is that the Tesorito drilling and subsequent move into resource estimation is enough to fulfil this criteria - however, when you start to incorporate LCL’s recent drilling at its other regional prospects like the newly confirmed Ceibal Porphyry discovery, this further cements the scale opportunity of LCL’s prospects.

AND we have written recently of our interest at seeing how LCL’s nested porphyry thesis plays out, with drilling in between LCL’s two existing gold systems happening right now:

So we think that LCL is already “showing scale and resource growth potential” of its assets, and is at this stage of its lifecycle.

Hence, our view is that LCL is now at the last of the three stages - Committing to aggressive exploration and creating that urgency that forces larger players to consider acquiring/ partnering with LCL before the project becomes too big for the majors to battle it out over.

An example would be Solgold’s Cascabel project in Ecuador, with both BHP and Newcrest declaring interest, yet having to accept participation as shareholders rather than partners.

Of note, LCL was an early mover in building its portfolio of Colombian Mid-Cauca belt assets - of late, the region has become a hotspot with several majors moving into the neighborhood including Anglogold, Zinjin and Newmont - to the point that it is very difficult to acquire any new prospective ground - this makes sense, given there is now over 60Moz gold discovered in the region to date.

With the macroeconomic background being supportive of M&A in the gold sector, the gold price elevated and yet to break-out into a parabolic move, the majors sitting on massive cash-balances producing record free cash flow and with all-time low interest rates making financing capital so cheap, we believe the ingredients are all here for widespread gold sector consolidation.

We suspect that companies like LCL, which have their hands on projects that are demonstrating size and scale and with the potential for further growth - especially in regions that are highly prospective - will be high on the radars of acquisitive majors in the year ahead.

What’s ahead for LCL?

- Maiden resource at Tesorito: We anticipate a first indicated and inferred resource by the end of June.

- Commence metallurgical studies: This kind of work is crucial to seeing the steps required to process ore once out of the ground, which points to costs of production.

- Scoping study at Tesorito: Incorporating the maiden resource estimate, we expect LCL will soon begin a Scoping Study, with likely release in 2H22.

- Drilling of ‘Jabba the Blob’ anomaly - deep drilling is continuing at the anomaly located between Tesorito and Miraflores, with three holes planned to be drilled in 1H22.

- Continue to progress exploration of other earlier stage prospects within its project, especially at Ceibal.

Our LCL Investment Memo for 2022

We’ve been rolling out Investment Memos across our portfolio in order to better track companies execution over time.

These “investment memos” are short and sharp high-level summaries of why we continue to hold LCL and what we expect the company to deliver in 2022.

The purpose is to record our current thinking as a benchmark to assess the company's performance against our expectations 12 months from now.

In our LCL Investment Memo you’ll find:

- Key objectives for LCL in 2022

- Why we continue to hold LCL

- The key risks

- Our investment plan

To access the LCL Investment Memo simply click on the button below:

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 3,210,000 LCL shares at the time of writing this article. S3 Consortium Pty Ltd has been engaged by LCL to share our commentary on the progress of our investment in LCL over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.