Introducing our Next Investors Small Cap Pick of the Year for 2022

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,802,500 SGA shares and 1,466,250 SGA options, the Company’s staff own 50,000 SGA shares and 12,500 options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

Today we announce our Next Investors Small Cap Pick Of The Year for 2022.

This is a label we reserve only for our highest potential Investments.

As with our previous Picks of the Year, we see the potential for this company to re-rate 1,000%+ over the coming 3+ year holding period.

Our last two Next Investors Small Cap Picks of the Year were:

- Vulcan Energy Resources (ASX:VUL) in 2020 - Up 3,555% since initial entry; highest point up 8,225%

- Province Resources (ASX:PRL) in 2021 - Up 164% since initial entry; highest point up 900%

As always, just because these last two picks performed well does NOT mean today’s pick will perform this way - small cap investing is risky and all sorts of things can go wrong.

For 2022, our Small Cap Pick of the Year isn’t an entirely new name to the Next Investors Portfolio — we first Initiated Coverage back in June when it listed on the ASX.

Early on we recognised the potential of this Investment — first investing in its seed round and every round since, including pre-IPO and IPO. We also visited the project to check it out for ourselves.

Yet there had been one question mark hanging over the company that held it back from reaching our Pick of the Year status.

Today, these concerns have been allayed with an announcement from the company giving us the extra confidence needed to name it our 2022 Small Cap Pick of the Year:

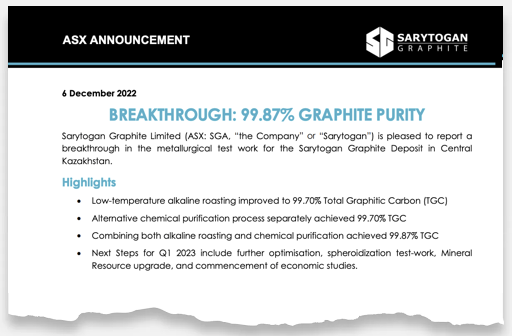

Sarytogan Graphite (ASX:SGA) has just announced a breakthrough 99.87% metwork purification result — the trigger for us to name it as our 2022 Small Cap Pick of the Year.

Today we will:

- Cover the significance of today’s “breakthrough” 99.87% graphite purity result,

- Share photos and observations from our visit to the project site in Kazakhstan, and

- Share the 3D model we created of SGA’s project.

Graphite demand for battery anodes is expected to surge over the next decade, with Benchmark Minerals Intelligence forecasting the need for 93 new graphite mines globally as the world transitions away from fossil fuels.

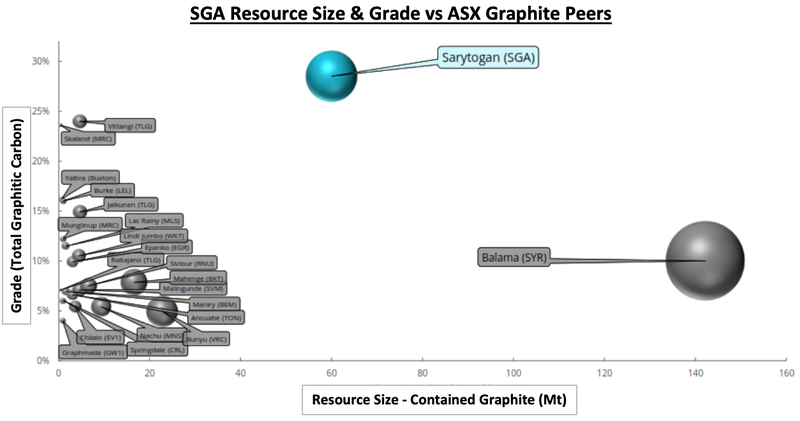

Before today, we already knew that SGA’s project in Kazakhstan had:

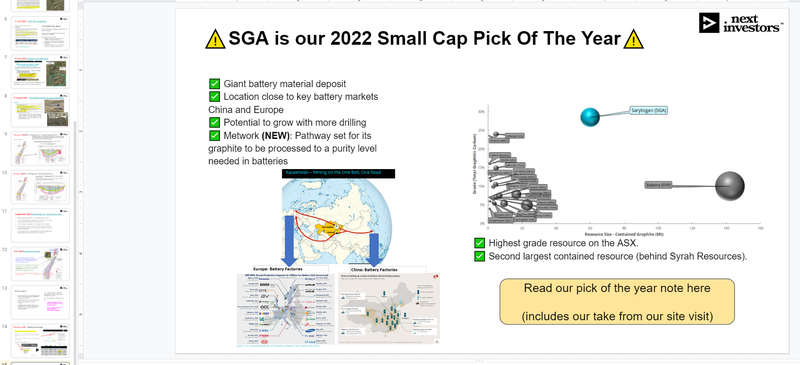

- The highest grade graphite resource on the ASX; and

- The second largest graphite resource on the ASX (second only to $1.7BN-capped Syrah Resources)

Here is SGA (blue bubble) compared to its ASX graphite peers - note Syrah’s Balama Project (largest grey bubble), whose resource is larger but of lower grade than SGA’s:

Before today, what we didn’t know was whether SGA was able to get close to achieving the graphite purity needed for use in battery anodes.

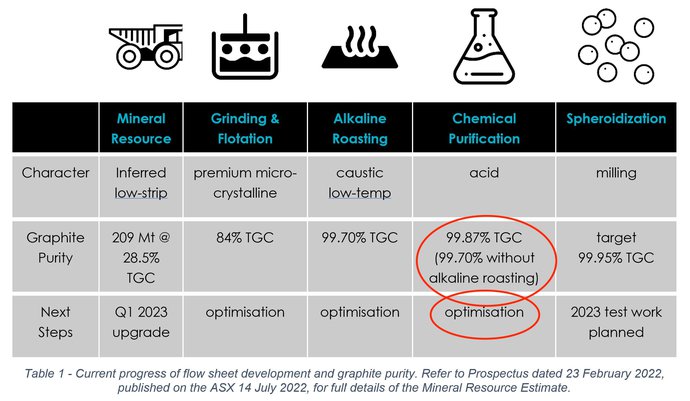

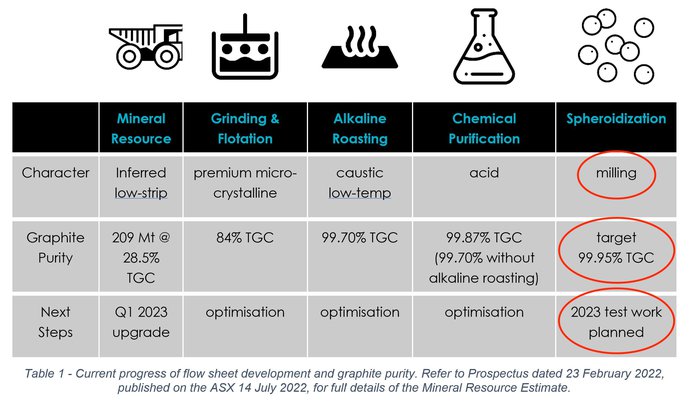

This morning a major breakthrough was reported when SGA announced that metallurgical test work (metwork) achieved 99.87% Total Graphic Carbon (TGC) — a significant step towards battery anode specification.

These metwork results (with further refinements still to come) mean that SGA is fast approaching the requirements for the battery anode suitable “Uncoated Spherical Graphite (USpG)” which requires:

- Graphite purity levels of 99.95%; and

- Spherical graphite balls of 5-20 micron in size.

Uncoated Spherical Graphite is a graphite product that can be sold into the lithium ion battery anode market at a price that’s three times higher than that of traditional flake graphite products.

A quick scan of the announcement tells us that grinding, flotation and low temperature alkaline roasting SGA achieved purity levels of 99.7%. Chemical purification also achieved 99.7%.

Combining the methods (roasting then chemical purification) achieved the 99.87% - with further refinement tests to come.

By introducing a milling process as the final step, SGA expects to bring its product up to the required battery anode specification. We expect this to be a big focus for SGA in 2023.

The samples that were purified were a composite mixed from 6 holes across the project. After today's excellent result, one of the key things for SGA to do next is to identify specific sections of its graphite deposit that are easier (hence cheapest) to purify. Honing in on these valuable sections of the deposit could deliver future share price catalysts.

Now, with some major breakthroughs in the metwork, we look ahead to more drilling results and to the resource upgrade that SGA has targeted for the March 2023 quarter.

While the resource is already of a giant size, another future potential share price catalyst we want to see is a significant amount upgraded to the JORC Indicated category, from its current inferred category.

All up, SGA’s project is ideally suited to serve the battery anode market which is facing a critical supply shortage over the decade ahead.

✅ Giant battery material deposit

✅ Location between key battery markets in China and Europe (see below)

✅ Potential to grow its high-grade graphite resource with more drilling

✅ Metwork [6 Dec 2022]: Graphite can be processed to the near the purity needed in batteries

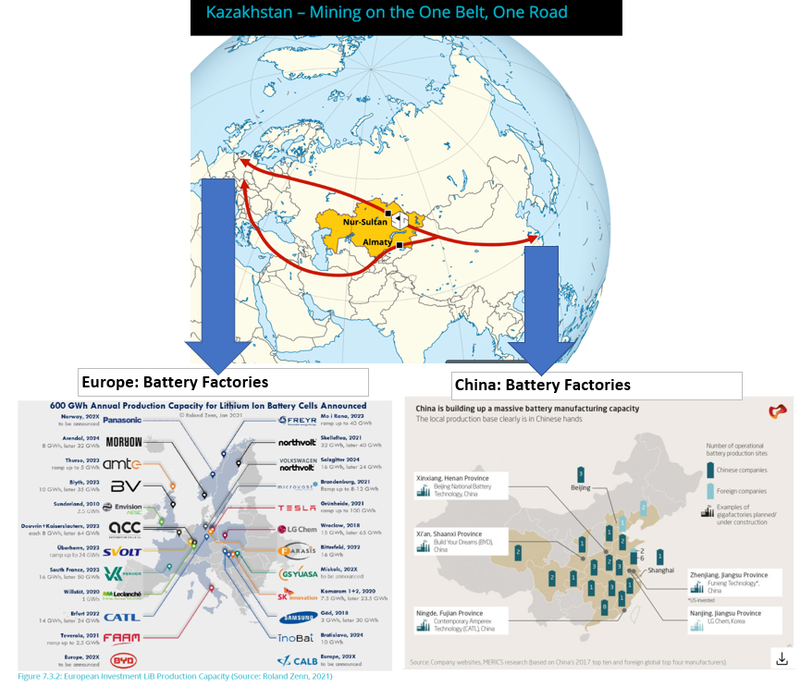

SGA’s giant graphite resource is located in central Kazakhstan, right between two battery hungry markets - Europe and China.

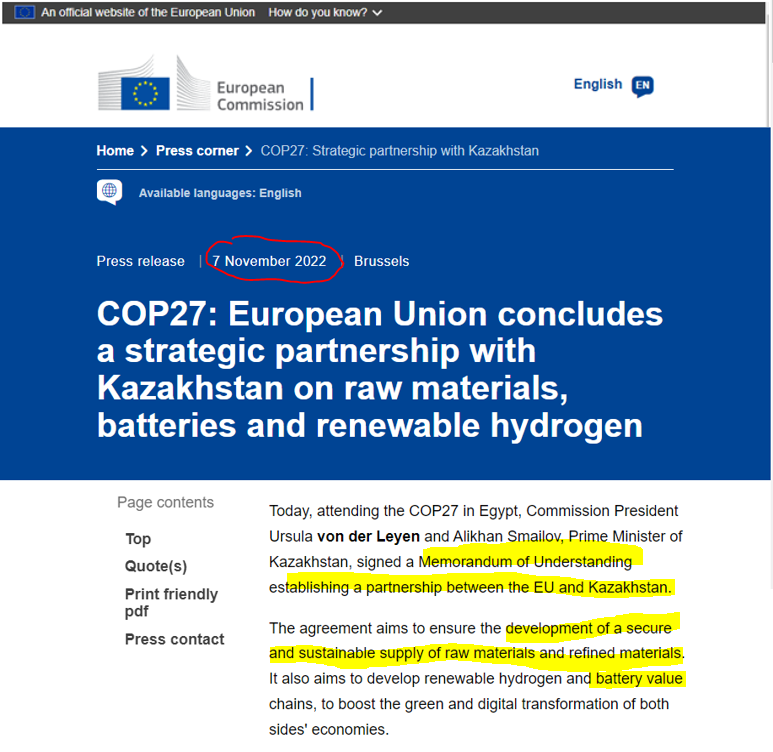

The European Union likes the potential of building closer ties to Kazakhstan, recently signing an MoU with the nation to establish a partnership on battery materials supply.

With that in mind, we think major European automakers could start to take an interest in SGA’s graphite, similar to when Ford signed a graphite supply deal with Syrah earlier this year.

Graphite makes up ~50% of the raw materials in every lithium-ion battery and over 95% of every battery anode, and graphite demand is expected to increase by over 700% by 2030.

That is expected to put the graphite market in a sustained period of structural supply/demand imbalance, meaning we are likely to see a lot more graphite offtakes signed by European automakers who want to lock in supply.

We visited SGA’s project in Kazakhstan earlier this year (more on our trip later in today’s note, including more on-site photos and some of our observations).

Here we are at the drill rig working to extend SGA’s already huge deposit:

We could see graphite outcroppings at surface — the graphite is literally sticking out of the ground all over the place. The black tinge on the hill is graphite:

With such shallow deposits, the graphite can be dug up straight from the surface through a process called trenching:

BUT...

It’s all well and good to have a giant graphite deposit, at surface, that is getting bigger with more drilling - but that means nothing unless the graphite can be extracted and economically processed to the right level of purity for the battery anode market...

And progress here is what we had been waiting to see...

SGA has now successfully delivered near battery grade metwork results, which it announced today, leading to us naming SGA as the Next Investors’ 2022 Small Cap Pick of the Year.

“Breakthrough” 99.87% graphite purity

When we launched our SGA Investment Memo in July and visited the site, we already knew SGA had the highest grade graphite project on the ASX, however it was still unknown whether SGA could produce marketable graphite, specifically for the battery anode market.

That question remained up until this morning, when SGA announced a “breakthrough metallurgical result” and an ability to produce high purity graphite.

SGA reported that metallurgical testwork by its German lab partners have officially produced a premium micro-crystalline high-purity product with purity levels of 99.87%.

Today’s news is a major improvement from the preliminary 92.1% purity that SGA announced in October and all of the historic data available which suggested achievable purity levels of ~98.6%.

The 92.1% prelim result back in October by an Australian lab spooked the market a little bit and saw SGA come back to around the IPO price of 20c.

We covered the initial metwork results in our last note in October: Initial metwork results are in - SGA targeting battery market.

So far, SGA’s flowsheet includes grinding and flotation, roasting and chemical purification. Next, SGA will be introducing a milling process.

While the aim is to improve purity further, we also want to see SGA prove that the flowsheet can be scaled up economically and are conscious of this still being a key metwork risk.

SGA’s goal is to produce “Uncoated Spherical Graphite (USpG)” to be sold into the market for lithium ion battery anodes.

This type of graphite product currently sells for >US$3,000 per tonne, which is around 3x higher than flake graphite products.

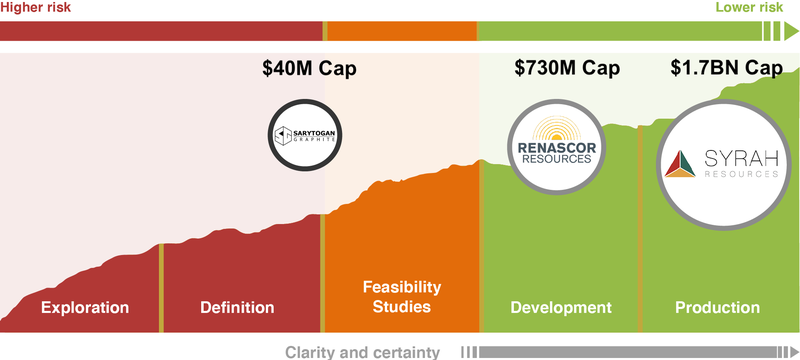

This is the same type of graphite product that the now $735M-capped Australian graphite player Renascor Resources is looking to produce.

Note that SGA’s current market cap is only $40M - 18x smaller than Renascor’s and ~42.5x smaller than Syrah.

We hope that as SGA’s project advances we hope that the company will grow to the size of some of its peers.

To produce graphite for the battery market, SGA now needs to show it can produce tiny, spherical graphite balls of 5-20 micron in size with purification levels of 99.95%. The company expects to be able to achieve this by milling its product.

This will be the target of SGA’s planned testwork optimisation in 2023.

Once completed, SGA can add a “modelled output product” into future feasibility studies and therefore a price for the graphite it expects to produce and sell.

It’s worth noting that metallurgical testwork is an ongoing process where a company works on a “flowsheet” to figure out the best way to process its graphite.

Already, in the 4.5 months since listing on the ASX, SGA has been able to lift its graphite purity to 99.9%.

These types of improvements can typically take years to make.

SGA is now working on refining its processing method so that its graphite meets the micron size and purification requirements to produce USpG.

And it still has plenty of time to do so while it completes drilling and permitting to bring its project closer to development.

If SGA achieves this it can start work on offtake agreements and economic studies - which will be the next set of share price catalysts - like we saw with Vulcan Energy.

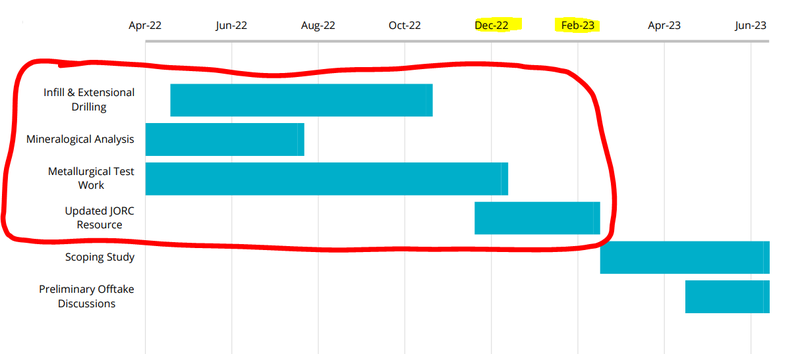

Drilling continues

While continuing to refine and optimise its processing methods, SGA continues drilling to make its already giant graphite deposit bigger, find pockets of easier to process graphite and generally get a better understanding of what SGA is sitting on.

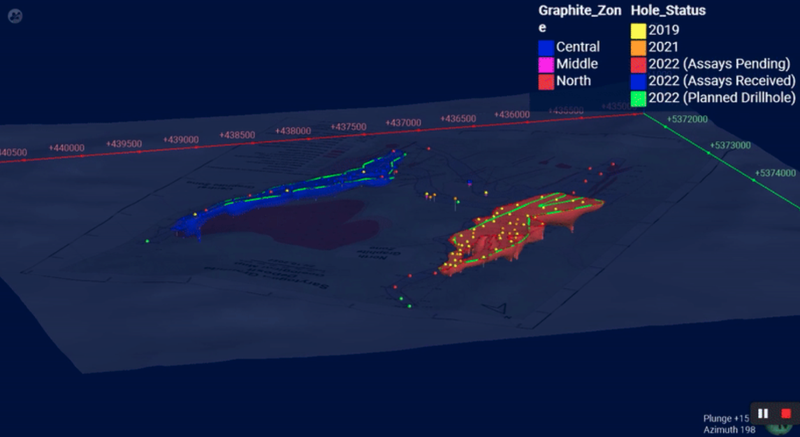

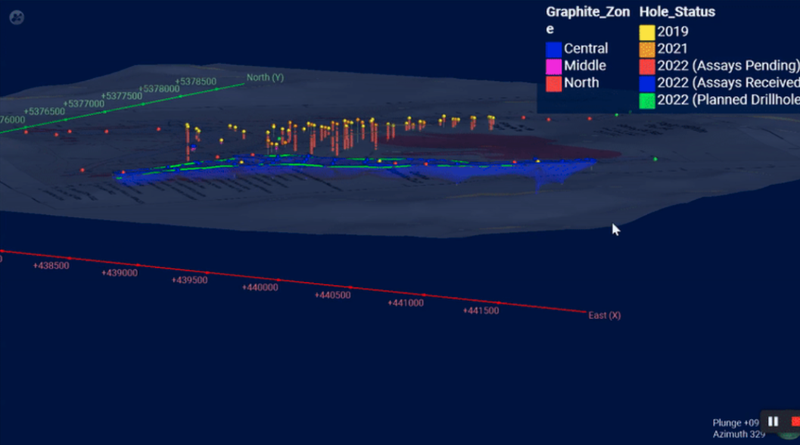

Below is our 3D model of the drilling program overlaid on SGA’s project area.

Disclaimer: these 3D models are just an interpretation of the publicly released results and several assumptions have been made. The models are for illustrative purposes only and to help explain the upcoming drilling. Investors should not rely on these illustrative models in making any investment decisions.

The yellow and orange dots are historical drill holes from 2019 and 2021, the blue, red and green dots are drillholes in the current drilling program across the Central, Middle, and North graphite zones.

SGA already has a giant Inferred Mineral Resource of 209Mt @ 28.5% TGC for 60Mt contained graphite.

So the primary objective of this drilling is to convert the resource into a higher confidence interval (from inferred to indicated JORC category) so that SGA can move into the feasibility study stage of the project’s lifecycle.

Our expectations for the upgraded JORC resource are as follows:

- Bull case = Total contained graphite >20mt in the “indicated” resource classification.

- Base case = Total contained graphite 15-20mt in the “indicated” resource classification.

- Bear case = Total contained graphite <15mt in the “indicated” resource classification.

This brings us to our “Big Bet” for SGA:

Our ‘Big Bet’

“Given this graphite project’s strategic location in between China and Europe, we hope that if SGA proves out the size and economic extractability of the resource, it will generate interest from major mining companies, leading to a takeover of SGA for $1 billion+.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor the progress SGA has made since we first Invested and how the company is doing relative to our “Big Bet”, we maintain the following SGA “Progress Tracker”.

See our SGA Progress Tracker here:

Our site visit to Kazakhstan

In July, SGA hosted several investors, equity analysts and the board of directors at its graphite deposit in Kazakhstan to see the drilling site, meet the local team and check out the drill core processing facility.

This is known in the industry as a “site visit” — an opportunity to get a better understanding of the project by seeing the operation up close.

This is especially important in a location like Kazakhstan that many Australian investors may be unfamiliar with.

Here’s what we saw on the site visit and our key takeaways:

Kazakhstan is not like you may first think

Despite the Kazakhstan portrayed by Borat, it is a modern country with amazing cities – we travelled via Almaty, then went to the project site and headed home via Astana:

Almaty:

Astana (formerly known as Nur Sultan):

The country is an established mining jurisdiction. It is the world’s largest uranium producer from mines (source), and recent reforms have created an attractive environment for investment in new exploration and extraction (more on existing major Kazak mining projects below).

Kazakhstan boasts the largest economy in central Asia — growing by double digits since 2002, the World Bank ranks Kazakhstan 25th for doing business, just behind Germany, Canada and Ireland, but ahead of Italy and Brazil (source).

It’s an environment that favours investment, including that from foreign junior mining companies.

Great roads and infrastructure en route to SGA’s graphite deposit

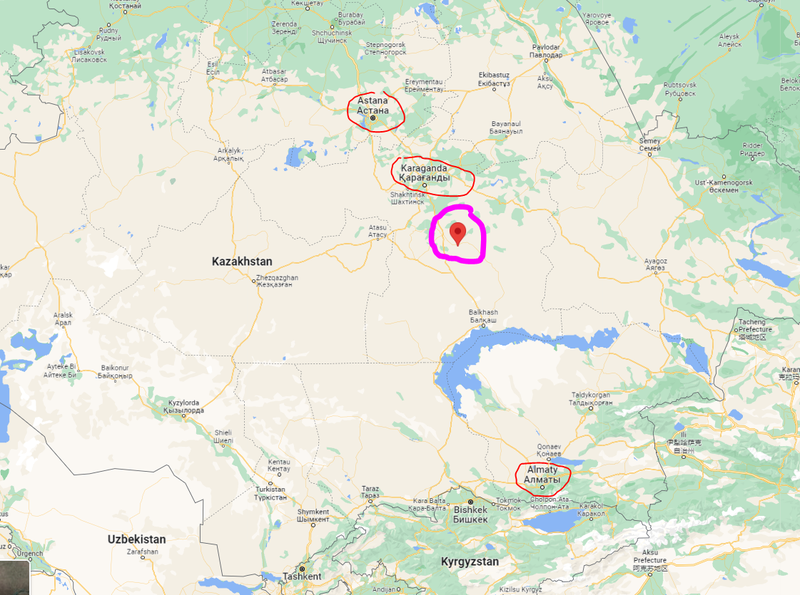

After landing in Astana, the nation’s capital, we drove to the industrial city Karaganda, then on to the SGA’s graphite deposit and project site (circled in purple) which was ~170km away by highway then some rougher road:

We observed well developed roads, rail and power infrastructure, confirming what SGA says about the project in its investor presentation.

Good infrastructure close to a project is important when planning and developing a mine. There needs to be roads to truck out the product, electricity supply to power the mine, and rail to reach export markets.

Here you can see good working power lines close to project site:

Here you can see rail access close to project site (sorry for the blurry image, it was taken while driving on Kazakhstan's fast and efficient highways):

We also noted significant road upgrades underway on the way to the project site:

So seeing all this infrastructure first hand means we don’t have concerns about getting the product out from the project location to future customers.

Graphite at surface

On site at the graphite deposit we walked across the two graphite zones, found some historical drill holes and observed the graphite outcropping at surface (the black/dark areas on the ground are graphite).

When a mineral deposit is close to surface, it is easier and cheaper to mine than one that is deep underground:

You can below see the dark tinge under the shrubs on the hill and on the ground in the front of the photo - this is graphite at surface:

There are no homes at or near the project location, which will make the building of a mine a lot easier:

Here’s an old drill hole from the 1980s:

We visited both the “North Graphite Zone” and “Central Graphite Zone”.

We have modelled both zones in 3D.

North Zone:

Central Zone:

Drill rig in action

We saw the drill rig in action, working through the drilling program to extend the Central Graphite Zone (which was successful), and met and had lunch with the drilling team (who were also great cooks).

Here’s our convoy at the Central Graphite Zone where the drill was happening:

Interesting fact, the drill rig is housed in a shipping container so that it can operate during the Kazakhstan winter when temperatures can reach minus 45 degrees Celsius.

It wasn’t exactly the newest rig we have ever seen, but this rig has successfully worked through many Kazakhstan winters. And at the end of the day, a drill core is a drill core.

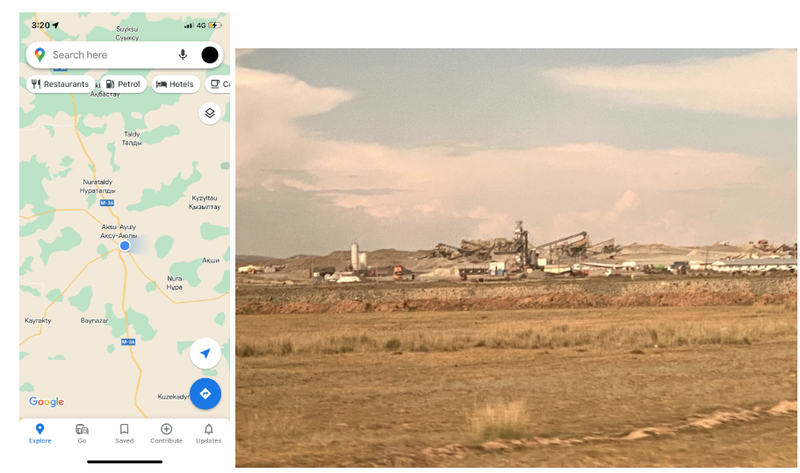

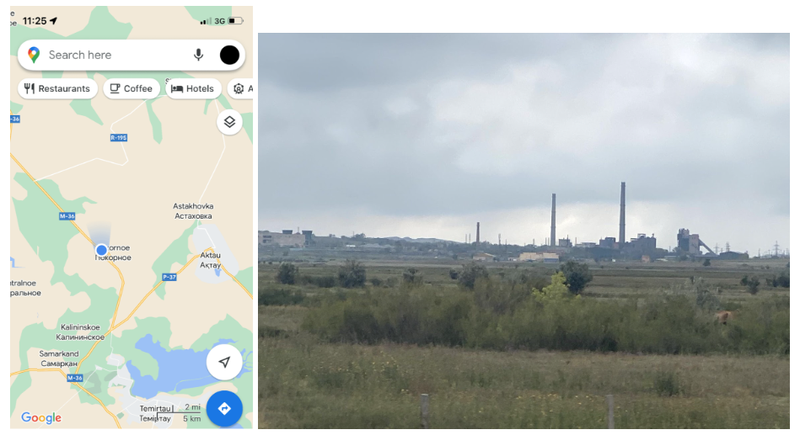

Other operating mines and plants nearby

On the way back to Karaganda we drove past two large plants (pretty sure it was a steel mill and a cement plant), which shows that it is possible to build complex industrial projects in areas near SGA’s site.

Cement plant near SGA site:

Steel mill near SGA site:

Karaganda is the closest city to SGA’s graphite deposit, an industrial city near Kazakhstan’s many coal mines that is the country’s fourth largest city.

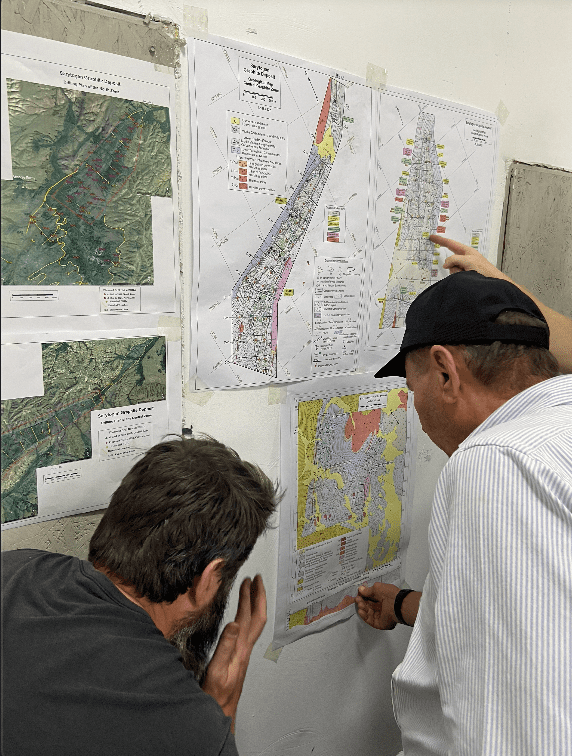

Drill Core processing facility

Back in Karaganda we visited SGA’s drill core processing facility and saw how the drill cores are stored and processed prior to being sent to the assay lab to test the grades. We also met the local SGA geology team.

Learning about the SGA project:

Drill Core storage shed:

Graphite samples:

Museum of Kazakhstan’s major mineral discoveries and mines

Kazakhstan has a long history of successful resource development projects, most famously in oil and uranium – it is the biggest uranium supplier in the world.

A strong history of successful projects increases the likelihood that a future project will also be a success - to name a few:

- Kazatomprom - Kazakhstan’s biggest uranium producer accounting for ~24% of global uranium production.

- Bogatyr Coal - one of the world's largest open-pit coal miners operating two mines inside Kazakhstan and produces 40% of the country’s coal.

- Kazakhmys - The largest copper producer in Kazakhstan and the world's 20th largest producer of copper concentrates (271 thousand tons).

Kazakhstan is an established mining jurisdiction, and has brought its mining legislation into line with Western Australia’s Mining Code (Standard Subsoil-Use Code in 2018) — one that is well understood by the global investment community.

One point of difference is that the country has a lower corporate tax rate than Australia, at 20%; mineral royalty of 3.5%; and other taxes of 1.5%, leading to stronger incentive to develop new projects.

The museum we visited is owned by the drilling contractor that SGA is using, and showcases 13 key past discoveries and mines in Kazakhstan, along with rock samples from each one.

Kazakhstan mining museum:

Each featured project includes project maps, description and rock samples from the project:

SGA’s project is already featured as an exhibit, with graphite samples from site:

Again, many thanks to SGA and their team for hosting everyone.

More on Metwork - progress toward de-risking the project

Let’s now consider what today’s metwork announcement means for SGA and its effort in de-risking the project.

Having a giant resource in the ground is one thing, getting it out of the ground and turning it into a product buyers want is another altogether.

When looking at new commodity discoveries, the latter is often ignored, but it’s the processing of a resource that makes or breaks a project. Without an effective processing solution a project could be stranded, no matter how big the resource is. This is why companies start metallurgical testing programs early on in a project’s lifecycle.

Before a company commits more capital to a project, the testwork programs are used to determine whether the in-ground resource can be extracted economically. When it comes to graphite projects, it’s the metallurgical testwork that is especially important.

There is plenty of graphite in the earth's crust, so much so that junior explorers looking for copper and nickel junior often walk aways from projects when they hit graphite.

What’s critical is being able to process and produce a type of graphite product that buyers want AND need.

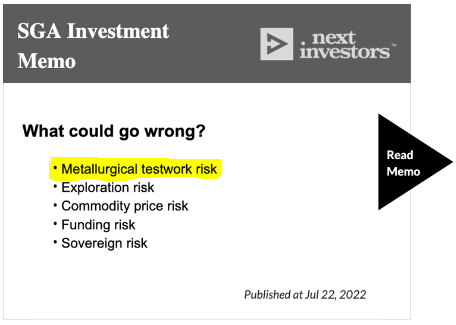

For that reason we listed metallurgical testwork as a key risk in our SGA Investment Memo.

Without positive metwork results a company can’t specify what it will produce and the price it can sell its graphite for once in production.

The obvious caveat here is that SGA needs to prove that it can replicate its metwork at scale in a processing plant big enough for its resource.

Today's news is a huge step in the right direction, but SGA still has some work to do before its project is development ready.

For that reason we have not yet marked the ‘metwork risk’ in our SGA Investment Memo as having been mitigated.

“Purification chemicals” and ESG

Purification chemicals used in SGA’s metwork were hydrofluoric (HF) acid.

At this point it is worth noting the ESG perceptions regarding the use of HF at an industrial scale.

All acids are hazardous substances that need to be carefully managed. HF is commonly used in Australia for industrial cleaning products at low concentrations and mineral laboratories at high concentrations.

It is used more extensively at an industrial scale in the chemical industry worldwide. The vast majority of natural graphite for battery use is treated by HF with the alternative being synthetic graphite which is produced by energy intensive (and CO2 intensive) high temperature thermal purification.

HF can be effectively controlled to protect the environment as it is readily diluted with water and neutralised with limestone. Due to this high solubility, off-gases from chemical processes can be scrubbed by passing through water curtains to capture and recycle the HF to be used again in the process.

HF is derived from fluorspar, which is mined in commercial quantities in north-east Kazakhstan for the Uranium industry and is readily available for industrial use. In any event, SGA has achieved 99.70% TGC with and without the use of HF.

HF can be safely administered and we will be monitoring SGA’s proposed use of and waste treatment of HF and how the process will be handled from an ESG perspective.

What’s next for SGA?

Assays from drilling program 🔄

Assays are pending from SGA’s infill and extensional drilling programs.

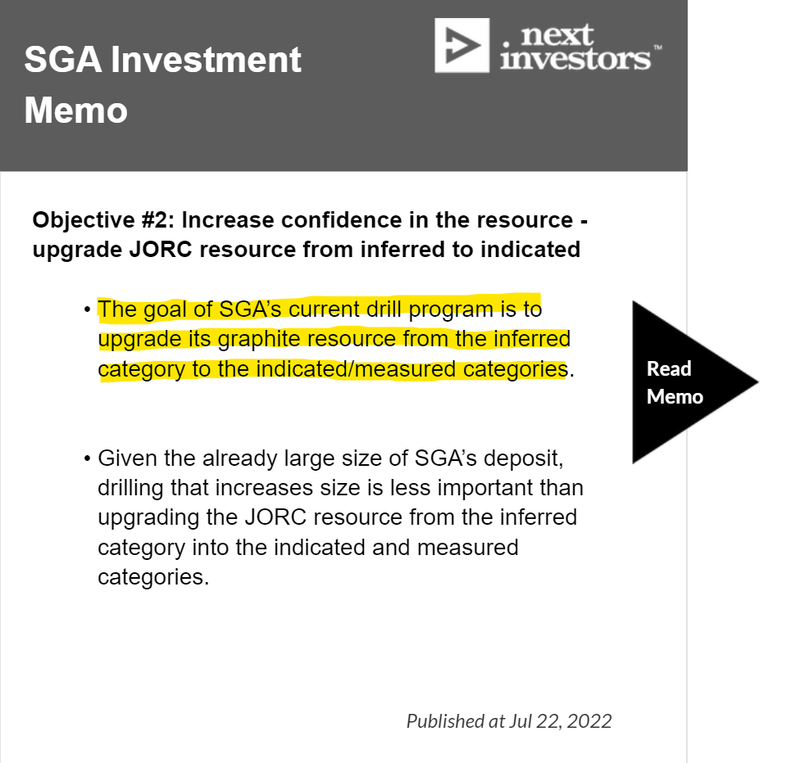

We are particularly interested in the infill drilling results as they will inform whether SGA can upgrade its JORC resource from the “inferred” category into the “indicated” category.

The market values indicated and measured resources above inferred resources as it points to the company being more confident in the accuracy of its resource estimate.

Results so far have been positive — the last batch of assays returned graphite grades of ~35.5%, up from previous intercepts in the same area of the resource that graded as low as 19% TGC.

See our coverage of the last assays here: Were the grades SGA released today good?

As for its extensional drilling, SGA is targeting NEW high grade, shallow extensions to its already giant JORC resource.

These are less important to us given the already giant size of SGA’s resource. But if SGA finds shallower and more valuable materials it could improve on the project's overall economics.

Therefore, we are also monitoring the results from these drillholes.

Updated JORC resource 🔄

The goal of SGA’s drilling program is to upgrade the classification of its JORC resource from inferred to the Indicated category, and move its project into the feasibility study stage.

The resource upgrade is targeted for Q1-2023.

Our expectations for the upgraded JORC resource are as follows:

- Bull case = Total contained graphite >20mt in the “indicated” resource classification.

- Base case = Total contained graphite 15-20mt in the “indicated” resource classification.

- Bear case = Total contained graphite <15mt in the “indicated” resource classification.

This is key objective #2 of our SGA Investment Memo.

Ongoing metwork 🔄

SGA will be building on today’s results, continuing to work with its processing partners to optimise processing methods. The ultimate aim is designing the most economic method to generate products at similar purities to that already achieved.

The next stage of work will focus on achieving the required specifications of “Uncoated Spherical Graphite (USpG)” which requires spherical graphite balls of 5-20 micron in size with purification levels of 99.95%.

Of course we are still conscious that SGA may not be able to achieve these required specifications and/or it may not be able to scale the processing solution to a size/scale that is required for its project.

This is why we think metwork is still a key part of the SGA story.

Our 2022 SGA Investment Memo

Click here for our SGA Investment Memo, where you can find the following:

- Key objectives we want to see SGA achieve

- Why we are Invested in SGA

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.