652 million barrel oil drilling event starts early March

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 6,610,000 88E shares. S3 Consortium Pty Ltd has been engaged by 88E to share our commentary on the progress of our investment in 88E over time.

Our oil exploration investment 88 Energy (ASX:88E) is only a few weeks away from drilling its 652 million barrel prospective resource.

88E will be drilling just down the road from US$120BN oil supermajor ConocoPhillips 400-750 million barrel Willow discovery.

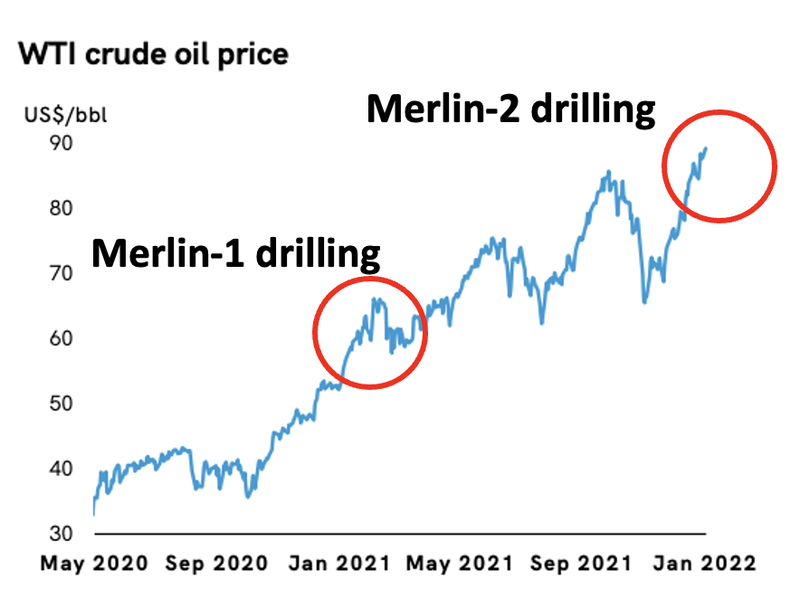

With the oil price now trading near five year highs at US$92/barrel, we think it's a pretty good time for 88E to be drilling for a potentially large oil discovery.

88E’s much anticipated Merlin-2 appraisal well is on track to be spudded early next month.

The Merlin-2 well is a follow up to last year’s successful Merlin-1 well and is targeting a massive 652 million barrels.

88E just completed a heavily oversubscribed $32M raise at 3.5c, which gives 88E a cash balance of ~ $64M.

Those placement shares were issued this morning to placement participants, so we are expecting there might be a bit of churn in the share price for a few days - until the market realises drilling is only a few days away.

The Merlin-2 well is expected to cost $39M to drill but 88E has already had a key contractor take payment in shares for a total of US$7.5M at 2.6c which should lower the cash cost to 88E.

With no farm out partner on board yet, so close to drilling, and given the recent capital raise, it would appear 88E are going to fund this well 100% themselves. This means 88E has 100% leverage to the upside (and downside) of the well and the project.

If a large scale discovery is made, then 88E will be the 100% owner of it.

We are investors in 88E because it undertakes high risk high reward drilling programs at least once a year. In oil & gas exploration, this type of drilling can deliver company making results IF drilling is successful.

As we have seen in the past with Oil & Gas drilling, there will often be a big share price run up as investors begin to speculate on the outcome of the drilling event, which creates an opportunity to de-risk for longer term investors who have been invested well before drilling starts.

Since the start of the year, the 88E share price made a big move from 2.6c up to as high as 5.3c. Now that the placement shares at 3.5c have been issued, and the drill permit has been issued, it will be interesting to see how the share price moves ahead of spudding in the coming weeks, and beyond that as the entire market waits for results.

Last Monday, 88E announced that the permit to drill the Merlin-2 appraisal well had been approved and that drilling was scheduled for early March.

So drilling is now only a few days to weeks away.

With ~$64m in cash in the bank 88E has also gone and acquired some already producing assets.

Last week 88E announced that it has acquired a ~73% interest in non operated leases and wells at a conventional onshore project in the Permian Basin, Texas, USA for a total cost of US$9.7M (split US$7.2M cash and US$2.5M in 88E shares at 3.5c).

The project has net 2P reserves of 2.1 million barrels, which equates to 88E paying ~ US$4.70 per barrel of oil equivalent.

The project is currently producing ~220 barrels of oil equivalent per day net to 88E.

This means at current oil prices around ~US$95/barrel, 88E’s share of revenues would be US$7.6M per annum.

Importantly in the acquisition presentation, 88E expects production to double after 7 workover programs in 2022. This could potentially mean over US$15M in revenues per annum if the workovers are successful.

We like that 88E will not be the operator of these new onshore assets, it will just be collecting the income, meaning it can still be fully focussed on its high risk high reward exploration projects.

Having been 100% focused on Alaska for many years, this acquisition of producing assets is a slight pivot in strategy from a pure play explorer.

What the acquisition does do, is help partially fund its “swing for the fences” exploration adventures in Alaska as opposed to relying purely on capital raises.

For now, lets turn our attention back to the imminent Merlin-2 drilling.

Drilling is now only a few weeks away.

As investors, it's always a good idea to have a think about what kind of a result you are looking for ahead of drilling.

We have had a think about what success would look like for 88E in the drilling of Merlin-2, and this is what we came up with:

- Net oil paying zones (Thickness) across the three reservoirs >41 feet (this is the reservoir thickness intercepted in the Merlin-1 well - so we want to see the same or better).

- Drilling program is successful enough to warrant production testing.

- Production tests confirm light oil and high flow rates.

One or all of the above is what we would like to see from the Merlin-2 drilling, and that would deem Merlin-2 a success.

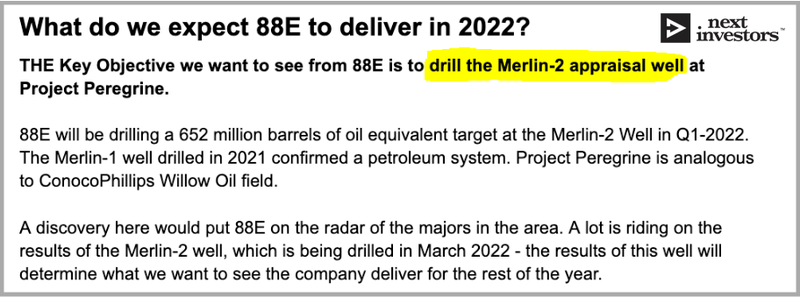

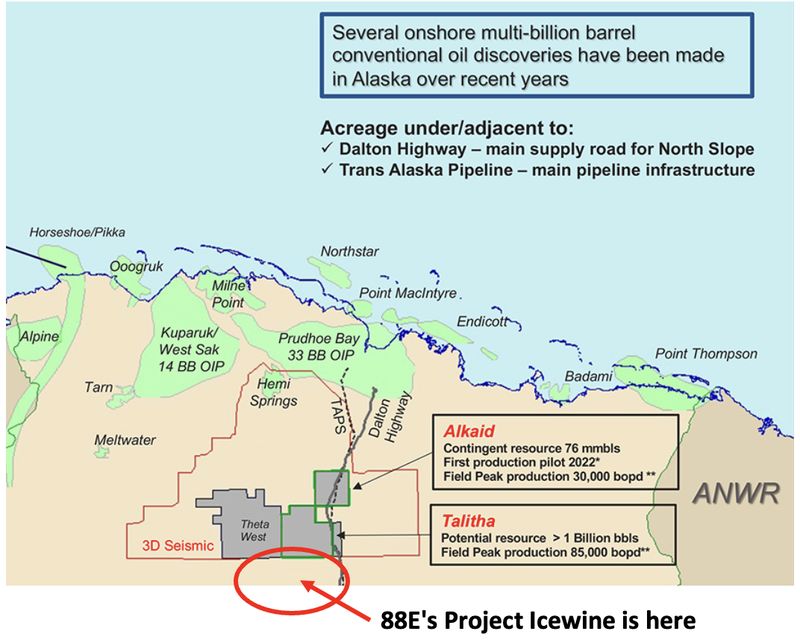

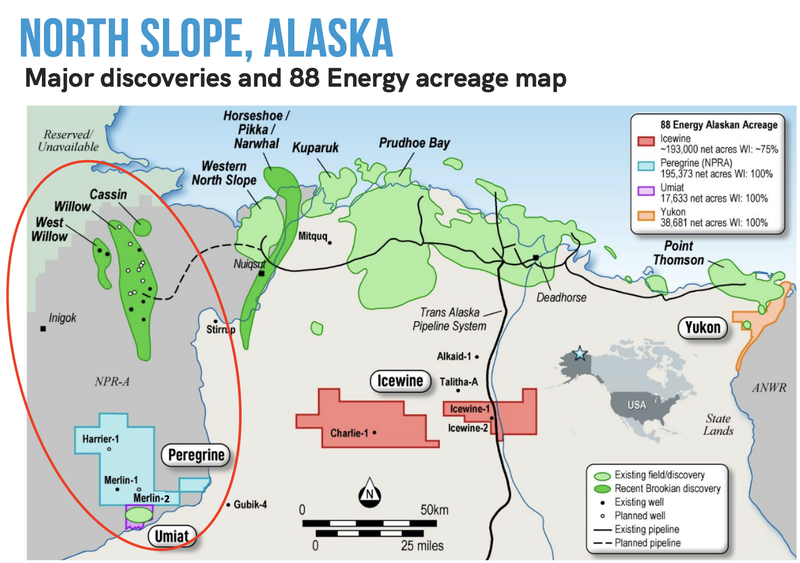

88E’s Merlin-2 well is drill testing the broader Project Peregrine. This project is located in the North Slope of Alaska, home of the largest oil discovery ever made in the USA, Prudhoe Bay - having produced over 12 billion barrels of oil since discovery.

88E’s Project Peregrine sits along trend and is considered analogous to ConocoPhilip’s 400-750 Million Barrel Willow discovery which sits ~100km to the North of the Merlin-2 well.

Merlin-2 is an “appraisal well”, which means it is being drilled into an already discovered Oil & Gas accumulation and is ultimately trying to give 88E a better understanding of the extent and size of the accumulation.

This well is a follow up on the success of Merlin-1 which detected light oil across three reservoir intervals.

To summarise, we already know there is oil, Merlin-2 will tell us how much.

88E’s Merlin-2 well is targeting 652 million barrels with a geological chance of success of 56%.

We set the drilling of Merlin-2 as our primary objective for what we wanted to see from 88E in 2022 in our 2022 investment memo.

With the permitting now approved and the commissioning of the drill rig due to commence shortly, we are looking forward to seeing if 88E can deliver a large oil discovery.

Of course - it's still high risk - a lot can go wrong in drilling speculative oil and gas wells - only invest what you can afford to lose in stocks like 88E.

While the focus right now is all on the drilling of Merlin-2, 88E still has other projects we like

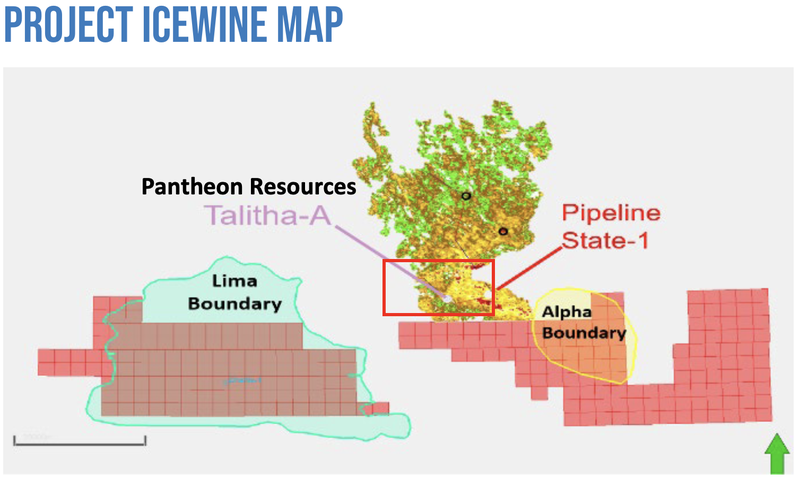

With all of the focus on Merlin-2 right now, it can be easy to forget that 88E still has its Project Icewine which we might come into focus later in the year, depending on Merlin-2 outcomes.

We have been watching 88E’s neighbour London listed Pantheon Resources (LON: PANR) who are currently drilling the Theta West #1 to the west of 88E’s Project Icewine go from a share price of GBP$0.35 to now GBP$1.40 where it trades with a market cap >GBP$1 billion.

Pantheon are also doing production testing at the Talitha-1 well, which sits over the same geological structure as found in Project Icewine. Any large scale discovery Pantheon make has a chance of extending directly into 88E’s ground.

The image below gives a better understanding of this with the small red squares representing 88E’s ground right below Pantheon’s drilling location.

Any major discovery and a confirmation of a reservoir by Pantheon could mean it's “game on” for 88E’s Project Icewine - so we will continue to monitor Pantheon’s drilling program and all of the production testing it is doing.

Drilling to start in early March

This year's big drilling event is a little bit different to that of previous years. In the past with its Charlie-1 and Merlin-1 wells, 88E was drilling trying to make an entirely NEW discovery.

Last year, the Merlin-1 well confirmed the presence of oil in the N20, N19, and N18 reservoir intervals - intersecting ~41 feet of net pay across the three reservoir intervals.

The geochemical analysis also showed the oil had an API Gravity between mid-30 and low-40 which means the oil is “light oil”.

This is important because light oil receives a higher price relative to heavy crude oil due to it producing a higher percentage of gasoline and diesel fuel when converted into products by an oil refinery.

We like to think of this as light oil means easy to process and so demands a higher price, heavy oil is harder to process so refiners are willing to pay less for it.

Now, 88E is going back in to try and define a maiden reserve figure.

We found this recent video really helped us understand exactly what Merlin-2 is all about.

https://www.youtube.com/watch?v=RpsowjZy2kY&t=1s

What happened to the 88E share price last time it drilled?

We are invested in 88E because of the high risk / high reward nature of its drilling programs.

Last year when the company announced that drilling data was indicative of “multiple potentially hydrocarbon bearing zones” the share price went from ~0.9c to a high of 9.7c - a rise of >1,000%.

Since then the share price has retraced and is now trading at ~3.7c, a very handsome return for shareholders who bought in before the drilling event at over 300%+.

In the chart below you can see the market reaction to the drilling results from Merlin-1.

Merlin-2 is drilling to test the size of the resource, which if successful could lead to 88E booking a maiden reserves figure for the project.

We think that if the market was willing to re-rate 88E to a high of 9.7c off potential oil shows at Merlin-1, then the booking of reserves could get the market a lot more interested.

Especially considering the oil price is now trading near 5-year highs at US$95/barrel, compared to US$65/barrel back in March 2021:

With Merlin-2 having the potential to unlock the region, any indication of scale could put 88E on the radar of majors like ConocoPhillips.

But once again, it's a high risk investment - lots could go wrong in the coming months - investing in 88E is not for the faint of heart - we are expecting a lot of volatility in the near term.

What’s next for 88E?

It’s pretty simple now, after many months of planning, permits and capital raising, 88E now just needs to get drilling.

Drilling of the Merlin-2 🔄

With permitting approvals now received there is very little left between now and the spudding of the Merlin-2 well.

All eyes are now on the drilling program scheduled for early March, only a few weeks away now.

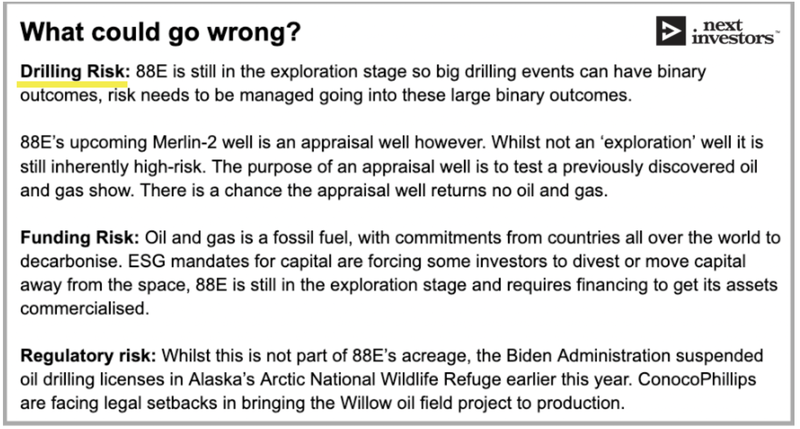

What could go wrong?

As part of our 2022 Investment Memo, we also challenged our investment thesis and put together a list of key risks to our 88E investment. Below is a screenshot from our memo.

What do we want to see from the Merlin-2 well?

With Merlin-1 intersecting 41 feet of net pay (thickness) we now want to see a much larger net pay zone across the three reservoirs at Merlin-2.

88E has also got approvals in place to conduct a production test. Should the drilling program go well, 88E expects to start production testing straight away.

A great result for us would be that the well IS suitable for production testing and 88E are able to conduct a production test, which 88E have said could run for up to 10 days.

Production testing is important because it is the precursor to understanding reservoir quality.

Understanding reservoir quality through production testing and also knowing how big it is from the net pay zones ultimately determine how large of a resource is in place. This will be used by 88E to “prove out” the prospective resource into an economic reserve number.

For context - the nearby ConocoPhillips discovery was made off the back of 2 wells that encountered 72 feet and 42 feet of net pay.

The first of those wells were production tested and over a 12-hour period produced ~3,200 barrels of 44-degree API oil per day.

This helps set a benchmark for us to compare 88E’s results with.

To summarise again, we think a great result for 88E will include the following:

- Net oil paying zones (thickness) across the three reservoirs >41 feet.

- Drilling program is successful enough to warrant production testing.

- Production tests confirm light oil and high flow rates.

Ideally we want to see at least the first two of these three, if we see all three then 88E has a solid chance at announcing a maiden reserve figure for the project.

So what's been done so far leading up to drilling?

Permitting completed ✅

Permitting and almost all of the planning works are now completed.

With the news on Friday last week confirming that the permit to drill the Merlin-2 well has been approved, 88E can now focus more on the commissioning phase of the drilling program.

Drilling is now expected to commence in early March and run for 3-4 weeks before production testing can begin.

Capital raised ✅

To go with the permit approvals, 88E also managed to raise $32M via an oversubscribed placement @ 3.5c.

Although the discount to the market price was large, the fact that the raise was significantly oversubscribed led to 88E actually increasing the number of shares offered through the raise. Since then the share price has naturally drifted down to the placement price.

The importance of the raise is that it adds to 88E’s already very healthy cash balance of $32.3M (at 31st of December 2021) and means that 88E now has enough cash to fully finance the Merlin-2 drilling program all on its own.

With oil prices trading where they are, we think 88E has put itself in a great position whereby it can take on 100% of the risk/reward of the drilling program.

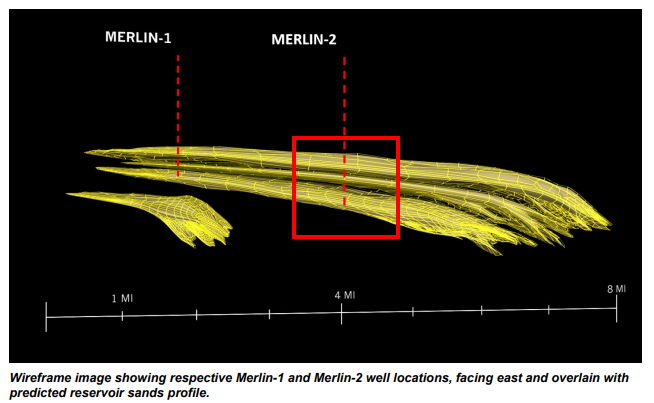

Merlin-2 Well location finalised ✅

Armed with all of the precious data gathered with the Merlin-1 well, 88E immediately went in and got permitting completed for up to three other drilling locations.

Out of these three, the final location for the Merlin-2 well has been selected to the east of Merlin-1 - in a part of the project area where the N18, N19 And N20 reservoirs are expected to be thicker.

The Merlin-2 well is being designed so that it is drilled to a total depth of ~8,000 feet, >50% lower than Merlin-1 which was drilled to a depth of ~5,267 feet.

With deeper drilling in an optimised location 88E will be looking to improve on the ~41 feet of oil paying zones that were intersected across the N18-19-20 reservoirs with the Merlin-1 Well.

The remaining two locations permitted, together with the permitted Harrier-1 well, could make up follow up drilling programs to further delineate a resource.

Of course - this is all conditional on Merlin-2 being a success - and that is no guarantee, such is the oil exploration game.

Drill Rig Commissioned ✅

In October last year 88E signed a rig contract with Doyon Drilling to use their Arctic Fox Rig.

Doyon has been around since the early 1980s and has been drilling in the Northern Alaska region ever since.

Doyon Drilling operates 8 different rigs specifically designed to drill oil wells in extreme weather climates like Northern Alaska.

Interestingly Doyon was the same contractor that drilled the Willow prospect (which is considered analogous to the Merlin prospect) for ConocoPhillips.

With experienced drilling contractors in its corner, we are hoping 88E can deliver another discovery in this part of the world.

Key Contractor support ✅

Late last year 88E also announced that it had managed to negotiate payment terms with one of its key contractors.

This contractor has been engaged to project manage the entire drilling program. That means they will be in charge of a large part of the operational and logistical aspects of the drilling program - up to and including the management of the drilling program.

Generally these type services make up the bulk of the costs incurred when drilling. 88E will be issuing 407M shares @ 2.6c to cover the US$7.5M in costs that will be incurred by the contractor.

The fact that the contractor has agreed to take the entirety of the payment in shares of 88E in our opinion is a massive vote of confidence.

It isn't often you see a contractor agree to take such a large payment in shares of the company it is doing the drilling works for.

With US$7.5M funded via share issuances, 88E’s cash position gives it even more flexibility going into the drilling program.

What’s left to do before drilling?

Farm out partner?

We mentioned earlier in the article that 88E had a very healthy amount of cash in the bank, which we think should be more than enough to finance the Merlin-2 drilling program, which was estimated to cost ~ $39M in a recent 88E announcement.

We also mentioned the fact that the key contractors were willing to take payment in shares saving 88E ~US$7.5M in cash.

With no debts outstanding, 88E are not forced to farm out the drilling program and instead can pick and choose whether or not to de-risk financing for the drilling program.

88E have flagged it would consider a farm out to a strategic partner only if the terms were suitably attractive.

We think that this flexibility is a major positive for 88E going into the drilling program.

With drilling programs that carry a ~ $39M price tag, small exploration companies are usually strapped for cash and are forced to give up large % interests in projects for financing.

In 88E’s case, there is nothing forcing them to give up a large % interest in the project BUT if a farm in partnership was on the table from an experienced operator in the region on favourable terms to 88E then we wouldn't mind seeing one get signed.

However, given drilling is due to start in early March, it would be a surprise to see a farm partner jump in so close to spudding.

What it could mean if Merlin-2 is a success?

The Merlin Prospect sits within greater Project Peregrine which covers 195,373 acres and sits on trend with the Willow prospect which was discovered by ConocoPhillips ~100km to the North of Merlin.

With a total prospective resource of ~1.6 billion barrels at Project Peregrine, any drilling success at Merlin-2 would effectively de-risk any future follow up drilling programs & bring into play the company’s other projects.

Committing to a drilling program that often costs tens of millions of dollars becomes justified if it is to delineate a prospective resource and book a bigger reserve that could be valued in the hundreds of millions of dollars.

But if Merlin-2 is unsuccessful then these drilling programs become higher risk - so future drilling programs are much more unlikely.

A success at Merlin-2 also puts 88E on the map for majors like ConocoPhillips who may be looking for bolt-on acquisition opportunities to tie in into a larger development project in the region.

Conoco is currently considering a Final Investment Decision of US$2-3 Billion development at the Willow oil field - so any bolt on acquisitions would significantly increase the attractiveness of a large investment like this.

For some context, the Willow project has an estimated resource of ~586M Barrels of oil equivalent and if it is put into production will produce >100,000 Barrels of oil per day.

These types of developments need scale to make a large capital investment worthwhile.

Instead of spending US$2-3 Billion on 400-750MBOE resource, they could double this assuming Merlin-2 can convert its prospective resource into reserves.

Success at Merlin-2 also brings into play 88E’s other projects.

The Umiat Oil Field, which recently had its well commitment extended out by 24 months to August 2023, could be incorporated into the larger Peregrine Project feasibility studies.

As part of project feasibility studies, 88E could also consider a build out of a pipeline that runs through its Icewine project and ties directly into the Trans-Alaskan Pipeline.

Direct access to the Trans-Alaskan pipeline through Project Icewine again significantly de-risk any drilling opportunities across the Icewine acreage bringing into play another ~193,000 Acres in project areas.

This video was really helpful to us in understanding the regional context of the Merlin-2 Well.

More on the new acquisition:

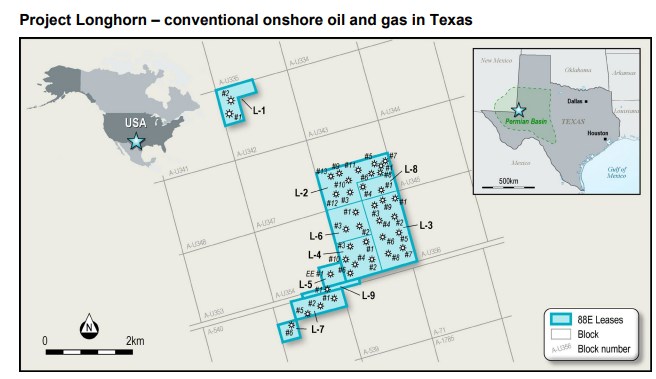

Yesterday 88E announced a slight change to the composition of its portfolio of projects. Previously, 88E was solely focused on Alaskan exploration, now it has a more diversified portfolio of projects.

With today's news 88E has added a ~73% non operated interest in conventional oil and gas production assets in the Permian Basin, Texas, USA.

“Non-operated” means that the JV partner who owns the remaining ~27% of the project will handle all of the operations, 88E will only need to contribute financially - with the associated rewards as well.

We think this works perfectly as it will mean 88E can solely focus on its Alaskan exploration assets.

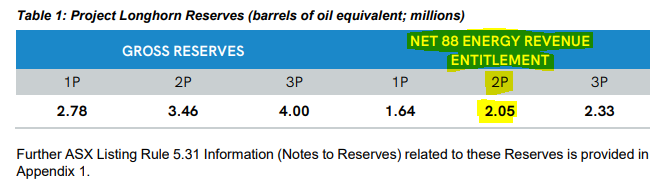

The already operational project is made up of ~32 wells that bring in ~220 barrels of oil equivalent per day net to 88E (of which ~70% is oil and the remainder gas).

The project also has a 2P reserves figure of ~2.1 million barrels of oil equivalent (net to 88E).

We see the acquisition as a good project to have in the portfolio, exploration companies like 88E spend most of its time in between large scale drilling events with no revenues to show for it.

Adding a project like this to the portfolio means 88E can benefit from the high oil prices and bring in a project that helps cover the everyday costs of running the company.

At 220 barrels of oil equivalent per day (net to 88E) at the current oil price of US$95/barrel, that means ~US$21,000 in revenue per day or US$7.6M in revenues/year.

The project acquisition cost to 88E was US$9.7M (split US$7.2M cash and US$2.5M in 88E shares at 3.5c).

In yesterday’s announcement, 88E also highlighted that seven workover programs were planned to start in March 2022 which 88E expects to ~ double output rates by the end of the year from.

If these programs are successful then the cash flow figures become significantly more interesting.

The acquisition sits outside of our 2022 Investment memo but brings some diversification and cash flow into 88E’s project portfolio.

Our 88E Investment Memo for 2022

Below is our 2022 investment memo for 88E where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations 12 months from now.

In our 88E Investment Memo you’ll find:

- Key objectives for 88E in 2022

- Why we invested in 88E

- What the key risks to our investment thesis are.

- Our investment plan

To access the 88E Investment Memo simply click on the button below:

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.