JBY kicks off scoping study for project next door to $56BN Barrick and $100BN Newmont

Our US gold Investment James Bay Minerals (ASX: JBY) has just started a scoping study for its project in Nevada.

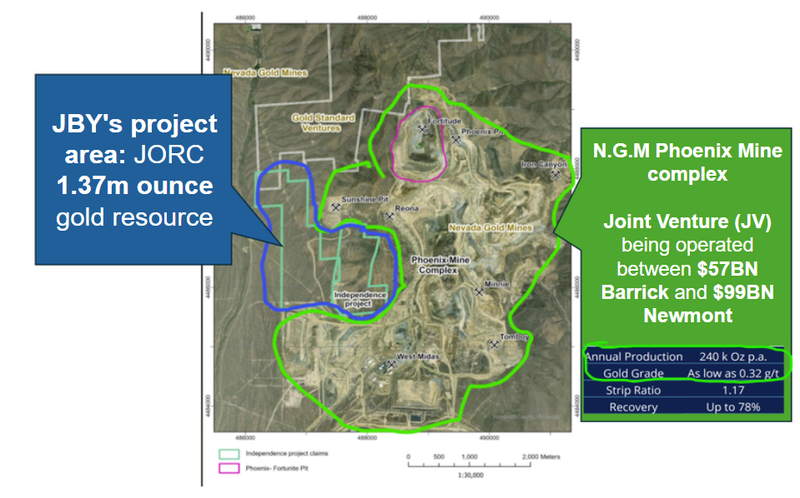

JBY’s project sits in and amongst N.G.M (Barrick and Newmont JV) Phoenix Mine which produces ~240k ounces of gold per annum.

JBY’s project has a ~1.37M ounce gold resource split across two structures:

- Shallow oxide resource - 385k ounce JORC gold resource, sitting in similar rocks to the stuff N.G.M is heap leaching nearby.

- Deeper skarn resource - 980k ounces at 6.67g/t gold sitting in similar rocks to the stuff N.G.M has produced over 2.4M ounces from next door.

The focus of the upcoming scoping study will be the shallow oxide resource.

Keep reading to see our take on what the financials might look like.

First, here is a link to our JBY site visit note (which we just got back from): JBY is surrounded by the one of the world’s biggest gold mines - here’s what we saw on site

(Here is a snap from us standing on top of JBY’s shallow resource, looking into N.G.M’s pit)

What can we expect from JBY’s scoping study?

JBY’s shallow resource has previously gone through the feasibility study stage.

Bakc in 2022 Preliminary Economic Assessment (PEA) was completed on the resource which showed it could produce 32,050 ounces of gold per year for 6 years for US$1,078 per ounce.

That study was completed when the gold price was ~US$1,800 per ounce and it returned an after tax Net Present Value of ~US$45M.

(Source)

Back then using the US$1,800 gold price, the project would have produced gold worth ~US$57M per annum.

Now with the gold price at US$3,450 per ounce, that same amount of production would generate ~US$110M in revenues…

To get a sense of how leveraged the shallow resource is to gold prices we only have to look at the sensitivity tables from that study.

For example, a 25% increase in the price of gold (assuming US$2,210) would have meant NPV around ~US$80M.

(an increase of ~US$45M for every 25% increase in the gold price)

(Source)

The gold price is up almost 105% from the base case assumption in that PEA…

IF we assumed NPV increases by that same amount for every 25% increase in the gold price it would mean at today’s prices the projects NPV could land somewhere in the US$200-250M range…

Which is multiples of JBY’s current market cap around ~A$66M AND it is only on the shallow portion of JBY’s resources.

It's also worth noting that the 2022 study does NOT include any of the deeper higher grade skarn mineralisation (980k ounces at 6.67g/t gold).

The deeper stuff can also make money - which N.G.M has shown by producing ~2.3M ounces of gold from the same host rocks.

These are all speculative calculations that don’t take into account increases in mining costs etc, so the final NPV numbers using today’s prices are hard to predict without an updated study.

We are just trying to get a sense of how the economics of that shallow resource are a lot stronger now than they were only a few years ago.

JBY resources are also likely to grow…

Whatever the numbers from the study, we think JBY can improve its project economics significantly with more drilling.

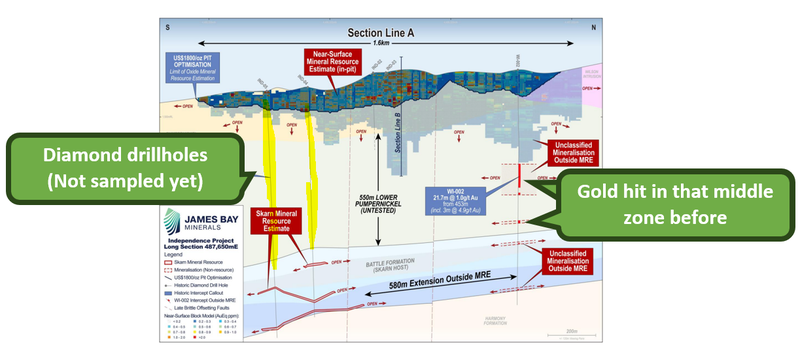

We have already seen JBY prove mineralisation outside of its current resource (FROM SURFACE) with its most recent set of assay results.

Here are the extension to the north (in red) - the image on the left is before the drill results, the image on the right is AFTER the drill results and the black outline is where the current resource sits:

With the next round of drilling we are hoping to see the following:

Ultimately, we are hoping that translates into a bigger shallow resource that JBY can add to its scoping study…

What else are we watching out for from JBY?

We expect the scoping study to be a catalyst for JBY because it will give the market a first look at the economics of one portion of JBY’s resource.

Beyond the scoping study and drilling results mentioned earlier we are looking forward to:

Assays pending on deeper skarn + Metwork 🔄

JBY has also flagged it would do some metwork testing on its deeper skarn resource which is ~984k ounces of gold at 6.64g/t.

From that work we are hoping to see recoveries that somewhat resemble the ones from N.G.M’s Fortitude pit which has mined ~2.3M ounces of gold from similar geology.

If the metwork is similar, the look through for us will be that JBY’s resource might also be feasible to mine.

Well understood recoveries could also pique the interest of N.G.M who are likely keeping a close eye on everything JBY is doing given the proximity of its ground to N.G.M’s operations.

Re-assaying old cores 🔄

We are also watching out for re-assaying results from the old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between JBY’s shallow and deep resources: