BKB: Now 2.2 million ounces of gold equivalent in Nevada, USA - plus a silver mine in Texas too?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,815,118 BKB Shares and the company’s staff own 30,000 BKB Shares at the time of publishing this article. The Company has been engaged by BKB to share our commentary on the progress of our Investment in BKB over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Legendary “gold royalty” pioneer Pierre Lassonde reckons gold is going to US$17,500 per ounce.

Veteran momentum analyst Michael Oliver reckons silver is going to US$300 to $500 per ounce.

Look they could be wrong - these are just two analysts’ price predictions that may not eventuate.

However our view is that many things are pointing to gold and silver having suddenly become nationally strategic metals.

Just look at the price rises on both over just the last 2 years... gold up over 100%, silver up nearly 200% - somebody's buying them?

(The past performance is not an indicator of future performance)

US national debt is spiralling past US$36 trillion. Foreign central banks are quietly dumping US Treasuries in favour of gold at a record pace.

Which is why Trump's Executive Order last year on US domestic mineral production explicitly named gold.

Washington suddenly needs a lot more of it coming out of the ground at home, fast.

Like gold, silver is also a defence against financial system uncertainty and inflation...

PLUS silver has industrial uses in the three key global buildouts of the next decade:

AI, robotics and advanced weapons.

(a three pronged global buildout we think will be bigger than 1800s railroads, 1900s industrialisation and the 2000s China urbanisation buildouts combined)

We think the USA will want to build domestic gold and silver supply as quickly as possible...

After decades of underinvestment and relying on imports from overseas.

We also believe the current geopolitical and financial system landscape will see gold and silver prices keep rising...

Which is why we made Black Bear Minerals (ASX:BKB | OTCQX: BKBMF) our 2025 Small Cap Pick of the Year.

BKB has a gold project in Nevada, USA... AND a silver project in Texas, USA.

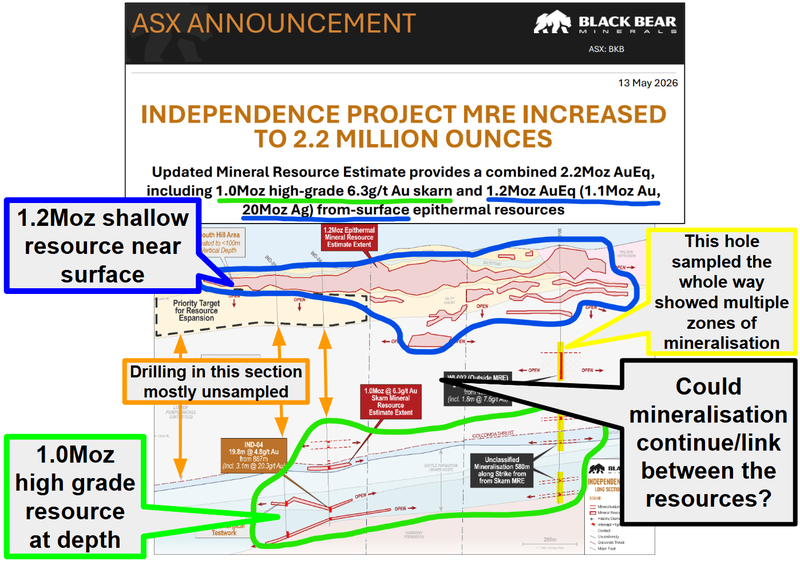

BKB just upgraded the JORC resource on its US gold project in Nevada.

That resource estimate is now 2.2M ounces of gold equivalent.

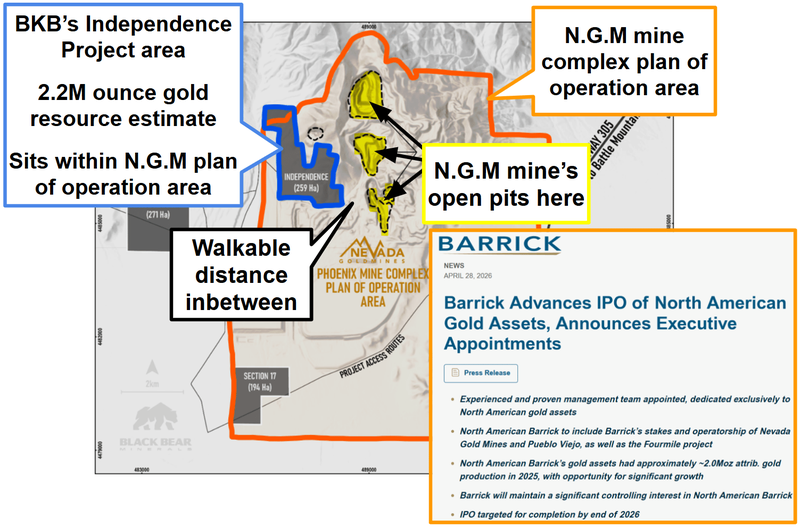

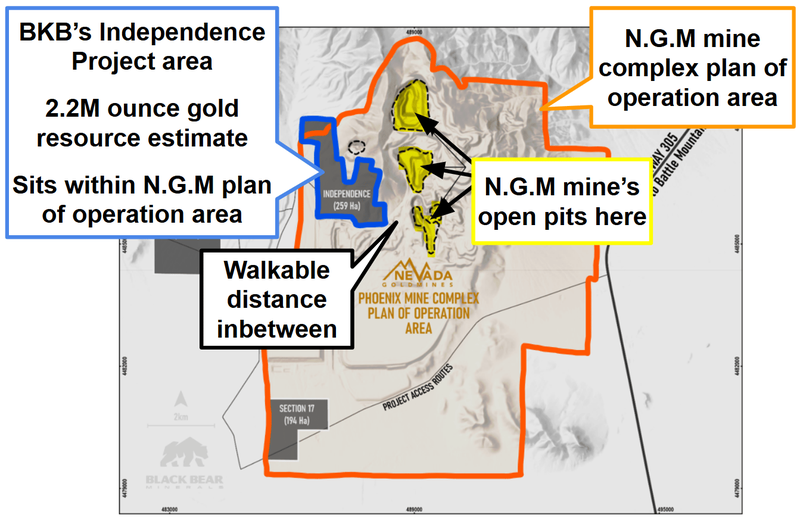

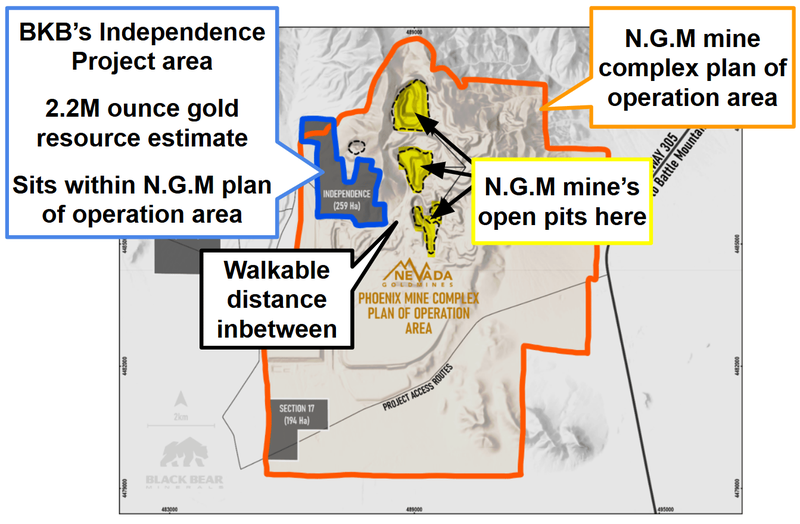

BKB’s project is right next door to $107BN Barrick and $177BN Newmont's Nevada Gold Mines Phoenix Complex.

(In fact BKB’s project is practically surrounded on all sides but one by the giant Phoenix gold complex. Check out the image coming in a sec)

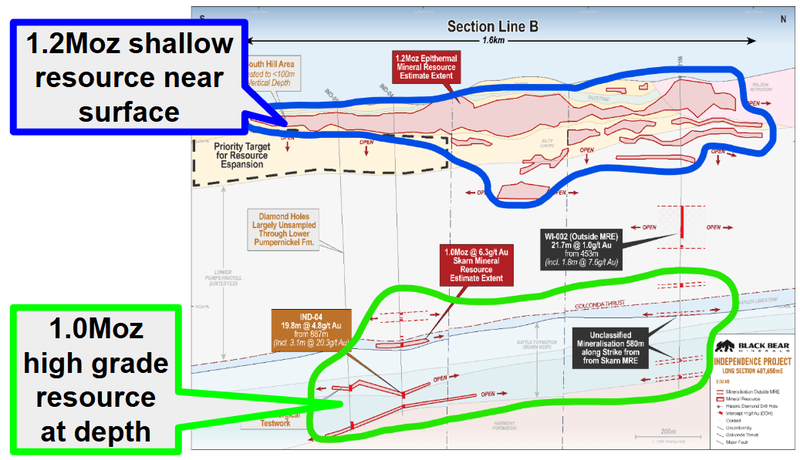

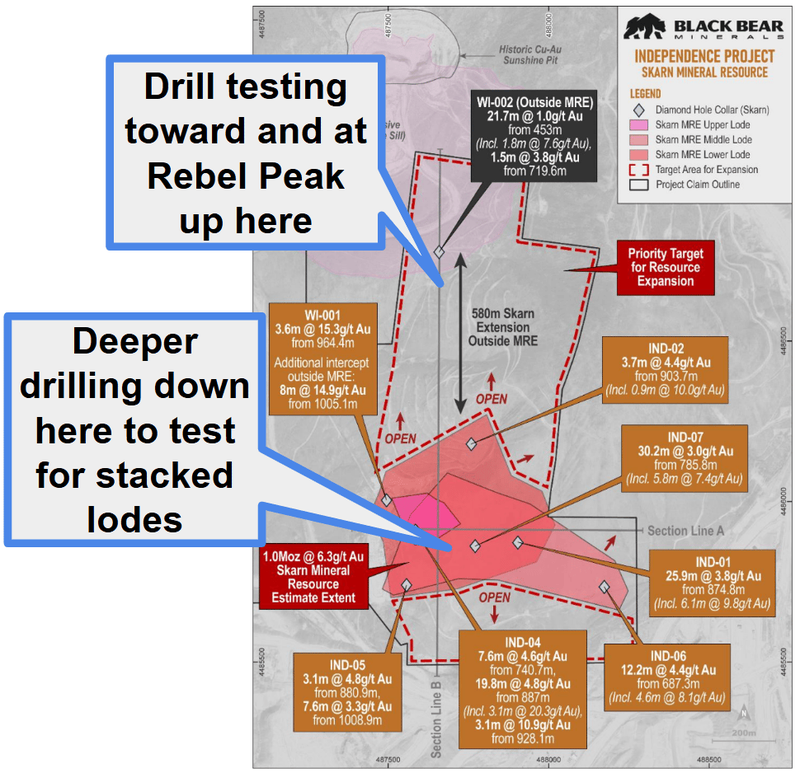

BKB’s updated JORC resource estimate has 1M ounces near-surface AND 1.2M ounces at depth with an average grade of 6.29g/t gold.

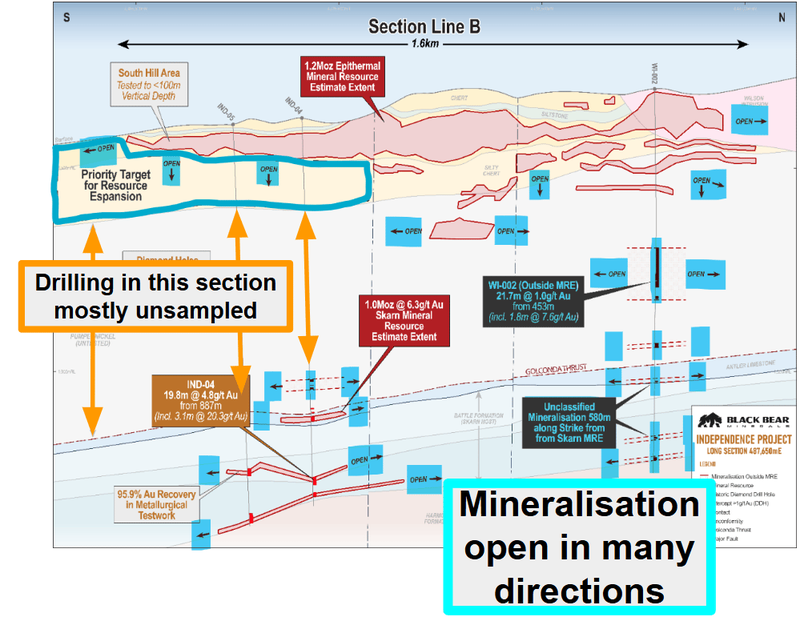

All open along strike AND at depth (and maybe even connected)?

(source)

We think this asset alone more than justifies BKB’s current ~$101M market cap.

Especially now, with $107BN Barrick about to spin off its US assets into a single gold supermajor whose only focus is US gold assets (mainly in Nevada).

That IPO is targeted for completion by the end of the year.

So a new listed gold supermajor, focused on US gold assets, who just so happens to be right next door to BKB...

That spin out is a big talking point right now:

(source)

Gold is currently trading at record highs of US$4,700.

Pierre Lassonde reckons gold is going to US$17,500 per ounce in the next couple of years - he explains why here. (Remember: he could be wrong)

(Pierre Lassonde is the guy who invested the “Lassonde curve” model, used by us and many mining analysts who to track mine development)

The main reason we made BKB our 2025 Small Cap Pick of the Year is because BKB has another asset that we really like...

BKB also owns a very high grade silver project in Texas.

With A$150M of existing on-site processing infrastructure and a 17.6 million ounce silver foreign resource estimate at 289g/t silver.

(source)

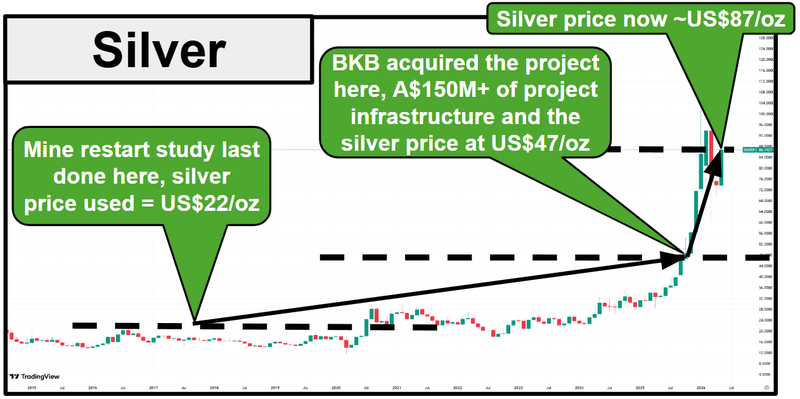

This plant was last operated 2012–2013 when silver was at US$18 per ounce.

BKB announced they were acquiring the project when silver was US$47.

Today the silver price is US$87.

We think the silver price is going higher.

(no guarantees of course, commodities prices can go down as well as up)

And BKB has already commenced a study for a “rapid restart” of this silver mine and processing plant.

What will the silver price be when BKB restarts it?

(we hope up a lot - but it could also be down, we can’t control the silver price)

Silver has started quite the run over the last 3 days.

After a well earned 3 month rest, post being the best performing commodity in 2025:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our favourite momentum technical analyst Michael Oliver reckons silver is going to US$300 to US$500 per ounce - here his reasoning here. (Remember: he could be wrong)

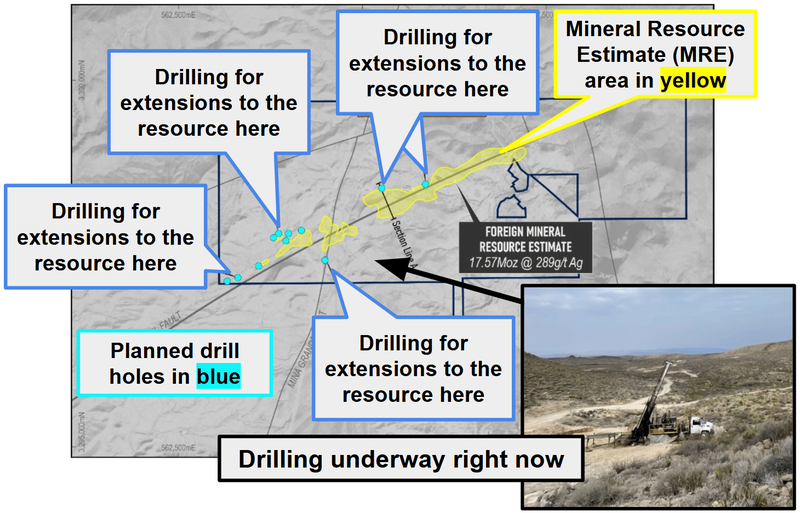

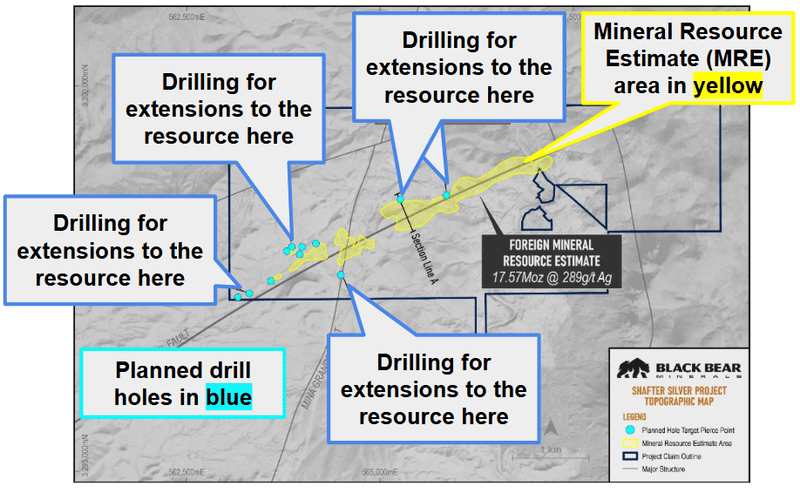

BKB is drilling this silver project right now.

(source)

So inside the ~$101M capped BKB we get exposure to two potential company making assets.

A 2.2M ounce gold equivalent JORC resource estimate - surrounded by two of the biggest gold miners in the world (Barrick and Newmont).

And a high grade silver asset with all of the processing infrastructure in place to go mining while the silver price is hot...

We think both of BKB’s assets are potential company makers

BKB current market cap sits at ~A$101M.

We think the market is only valuing one of BKB’s two assets and two scenarios:

Scenario A: Assuming the US gold project is the main story in which case BKB has:

- A 2.2Moz gold equivalent JORC Mineral Resource estimate

- Exploration upside (open along strike and at depth in every direction)

- Adjacent to the N.G.M Phoenix mine complex ($107BN Barrick and $177BN Newmont)

- Inside N.G.M's Plan of Operations Area

IF the market thinks of BKB like this then we are getting a “free option” on the silver asset (with its estimated A$150M of infrastructure and 17.6Moz at 289g/t).

Scenario B: Assuming the US silver project is the main story, in which case BKB has:

- A 17.6Moz silver foreign resource estimate at 289g/t

- A$150M of existing processing infrastructure (built in 2011-2012)

- Silver on the US Critical Minerals List

- A 2018 restart study with a Net Present Value of US$42M at US$22/oz silver (way below the current ~US$87 silver price).

- A rapid restart study underway right now

- Drilling underway right now

And in this scenario, we get a “free option” on the gold asset (with its 2.2Moz AuEq next door to NGM).

We are bullish on BOTH gold AND silver.

So we're more than happy to hold the majority of our BKB position and let either story play out (or both).

More on both assets in the rest of today’s note.

But first here is why we think the timing is very good for today’s announcement from BKB.

The macro setup for BKB’s gold asset is about to fire up

First there is the gold price, which we are bullish on (in case you hadn't already figured that out). If it continues to run, then the strategic value of BKB’s resource goes up with it.

We saw this video yesterday of mining royalty Pierre Lassonde calling for a run to US$17,250 per ounce:

“I Could Not Be More Bullish”: Pierre Lassonde’s $17,250 Gold Target

Of course this is just one person’s opinion, its very hard to predict future commodity prices, so don't invest based on one commentator’s opinion alone, do your own research.

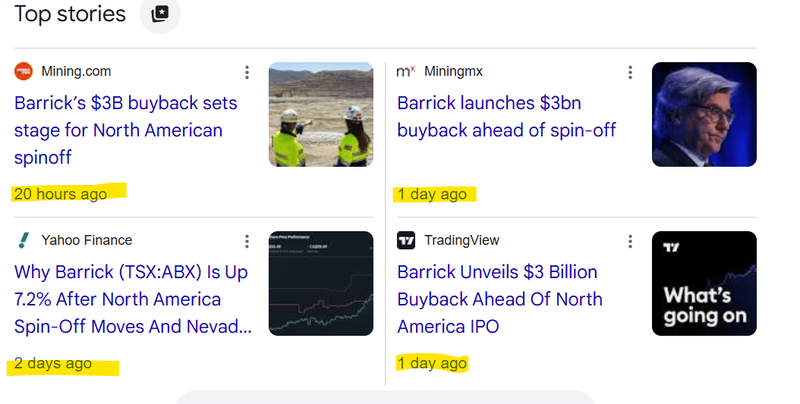

Then the second macro catalyst (and possibly more important) - $107BN Barrick is officially spinning out its US assets into a separately listed entity.

(source)

The new entity, which is expected to complete an IPO in late 2026 at a ~US$42BN valuation would hold:

- 61.5% stake in Nevada Gold Mines (the JV with Newmont - includes Phoenix, Cortez, Carlin, Goldstrike, Turquoise Ridge)

- 100% Fourmile (Barrick's wholly-owned Nevada discovery), AND

- Barrick’s 60% stake in Pueblo Viejo (Dominican Republic)

For the first time in decades, Nevada will be home to a pure-play, listed US gold producer whose management can focus 100% of its time and capital on the US.

No more competing inside Barrick for capital that gets allocated to copper projects in Pakistan, gold in Mali, or African expansion.

Which we think means more capital flowing into its US based assets for growth.

IF only there was an asset that had a 2.2M ounce gold equivalent JORC resource...

Sat right next door to one of NewCo’s assets..

AND actually sat inside one of NewCo’s existing mine plans:

(source)

We think the Barrick spin-out will be good for all gold assets in Nevada.

But especially good for BKB’s asset.

Today’s resource upgrade makes BKB’s project more interesting to a US-focused gold major

We think now, with a 2.2M ounce gold equivalent resource estimate, BKB has demonstrated that its project is big enough to warrant attention from the operators of a massive mine next door.

Especially given BKB’s project still has plenty of exploration upside too.

Here is where the current JORC resource estimate sits:

- 1.2M ounces near-surface across ~1.5km of strike, and

- 1.0M ounces at depth with an average grade of 6.29g/t gold

(source)

And here is all that exploration upside (something that a major looking at the asset would care a lot about):

Open along strike, down dip, north, south.

(source)

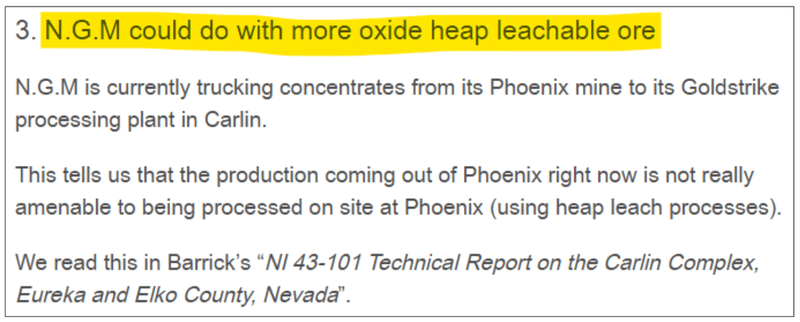

We already know that the at surface mineralisation is similar to the stuff that N.G.M’s been mining at its Phoenix pit for years - and the right type of ore to go straight into their processing plants.

Here is what we said in our BKB site visit note from last year:

(source - our site visit article)

And here is that reference to the Carlin plants processing “third-party ores” from Phoenix.

(source)

We also know that BKB’s deeper resource is the same type of material that was mined at N.G.M’s Phoenix operation at the Fortitude pit between 1984-1993.

That pit produced ~2.1Moz of gold at ~6.68g/t Au at over 90% recoveries.

Almost identical grades to BKB’s current resource (BKB's deeper resource is 6.29g/t Au) and Interestingly the metallurgy looks similar...

BKB’s shown that it could have 95.9% gold recovery (per BKB metallurgical testwork).

BKB's project literally sits inside Nevada Gold Mines' Plan of Operations Area

That means it’s inside all of the permitting frameworks N.G.M have put in place for their operation.

It could also mean faster integration of the project into whatever N.G.M wants to do with its assets.

(source)

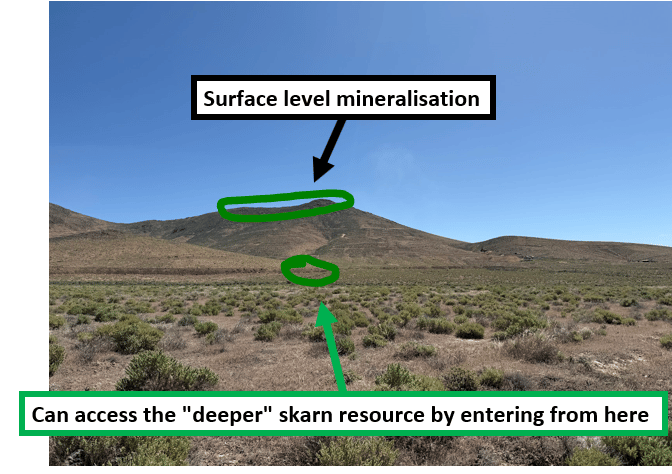

We have actually been on site and hiked up to the border of BKB’s ground and the giant pit N.G.M is operating.

When you stand on top of that hill and look in one direction, you see BKB's project and on the other side the massive pit being mined by N.G.M:

Check out our site visit note here: JBY is surrounded by the one of the world’s biggest gold mines - here’s what we saw on site

We are not mining engineers - but it feels like BKB’s near surface resource could be mined using conventional heap leach processing and an open-pit, then once that’s exhausted an underground decline to access that deeper resource:

How about BKB’s silver project in Texas

This is the asset that made BKB our 2025 Small Cap Pick of the Year back in November.

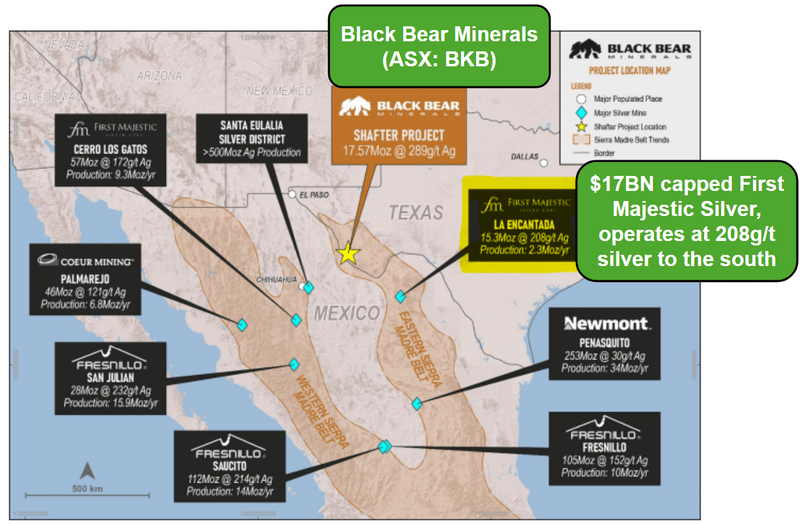

BKB owns 100% of a 17.6Moz silver foreign resource at 289g/t silver.

Those are seriously high grades especially when compared to other primary silver mines operating globally.

For example ~$17BN First Majestic Silver’s assets ~300km to the southeast on the same belt operates with grades below ~289g/t silver:

(source)

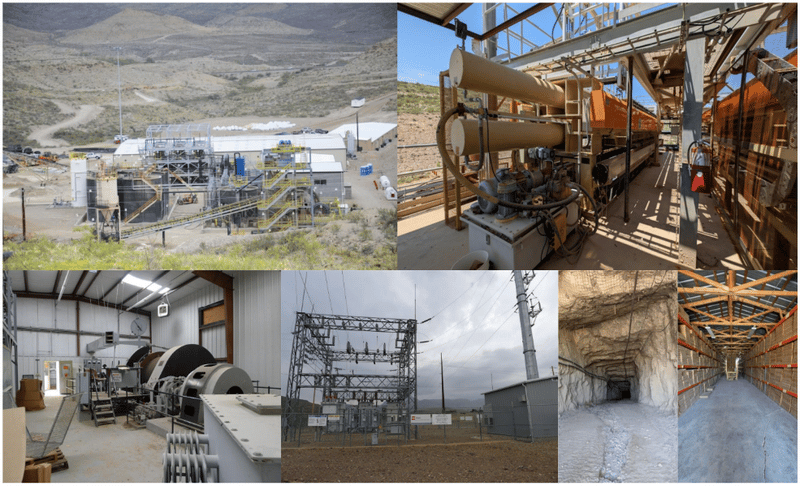

The reason we like the project is because it already has A$150M of existing on-site infrastructure, including:

- modern Merrill-Crowe plant + refinery (built 2011-2012) A

- A 24,000 sq. ft. warehouse

- An assay lab

- A 69 kV power line + on-site substation

- Full unencumbered water rights

- 160km of existing underground workings

- Four production shafts

The project also produced ~35 million ounces of silver between 1883 and 1942 at an average grade of 521 g/t Ag.

And then more silver when it was last in production in 2012–2013 - until silver prices below US$18 per ounce forced the asset into care and maintenance.

We think that this is the type of asset that can get back into production quickly (because of all that infrastructure on site) in a higher silver price environment.

Then, because of those grades they operate with strong margins...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

BKB has engaged Ausenco (one of the world's leading mining engineering firms) to deliver a rapid restart study for the project.

AND drilling is currently underway for 11 diamond holes across three target zones, including the historic Mine area.

So over the next 6 months we could see drilling results from the asset and the outcome of that restart study.

We think both pieces of newsflow dropping into a market where silver prices are running again could bring with it a lot more interest into BKB’s silver asset.

Our BKB Big Bet:

“We want to see BKB drill, extend and grow the resources on both its gold and silver projects to the point of the projects being development ready (or to the point of a major buying out the assets). At that point, we hope to see BKB’s market cap trade at $750M+”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, market risk and commodity price risk - just some of which we list in our BKB Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's next for BKB?

🔄BKB’s 2.2M ounce gold equivalent Nevada gold project

At the moment BKB isn't drilling this asset and has instead moved into the study/mine planning stages.

Next we want to see BKB deliver:

- UNDERWAY: Mining study phases on a heap-leach development 🔄

- DUE NEXT: Metallurgical testwork across all epithermal oxidation states 🔲

- DUE LATER: Mining study / scoping study 🔲

Eventually when drilling is back on the cards we want to see BKB test for the following:

- UNDERWAY: Planning for follow-up drilling north of skarn (the 580m gap to WI-002) 🔄

- DUE NEXT: Drill testing the Rebel Trend (1km of untested strike) 🔲

- DUE NEXT: Deeper drilling at South Hill (untested stacked lodes) 🔲

(source)

🔄 BKB’s high grade silver project (Texas)

BKB is drilling this project right now, with the initial results recently reported on the project. (source)

We want to see results from the rest of the drill program - especially given BKB will be assaying for minerals outside of just silver.

Surprise high grade hits or multi-element assays could be a catalyst for BKB’s share price.

We are also looking forward to seeing BKB release the results of its restart study on the project.

Here are the milestones we are tracking:

- UNDERWAY: Ausenco rapid restart study (dilapidation study + CAPEX estimate)

🔄 UNDERWAY: Drill results from 11 hole diamond drilling program. 🔄 - DUE NEXT: Drill results (including multi-element assays) 🔲

- DUE NEXT: JORC conversion of the 17.6Moz foreign resource 🔲

(source)

What could go wrong?

The single biggest risk for BKB right now is “Exploration risk”.

BKB is drilling its silver resource which has an existing foreign resource estimate.

IF the results fail to confirm that resource then it could mean BKB delivers results well below market expectations and lead to a re-rate in BKB’s share price.

The second risk is “commodity price risk”.

BKB’s share price moves in line with gold and silver prices.

Both gold and silver are at or near all-time highs. A meaningful pullback in either would hurt BKB regardless of operational progress.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold or silver prices fall, this could hurt BKB’s share price. We have already seen this happen with the lithium price and what it meant for BKB’s Canadian lithium assets in the past.

Source: “What could go wrong” - BKB Investment Memo 02 October 2025

Other risks

Like any early-stage exploration and development company, BKB carries significant risk, here we aim to identify a few more risks.

The Texas silver project currently relies on a foreign resource estimate. There is a risk that modern JORC-compliant drilling and modeling could result in a smaller or lower-grade resource than what is currently reported.

The A$150M of existing infrastructure has been in care and maintenance since 2013. The upcoming rapid restart study might reveal that the costs to refurbish and modernise this equipment are significantly higher than the market expects.

While metallurgical tests for the Nevada gold project have been positive, processing the deeper, high-grade ore can be technically complex. Any unforeseen issues with gold recoveries could negatively impact the eventual project economics.

Running two major work programs across Nevada and Texas is capital intensive. BKB will likely need to raise additional funds to move these projects toward production, which often leads to shareholder dilution.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our BKB Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

In our BKB Investment Memo, you can find the following:

- What does BKB do?

- The macro theme for BKB

- Our BKB Big Bet

- What we want to see BKB achieve

- Why we are Invested in BKB

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.