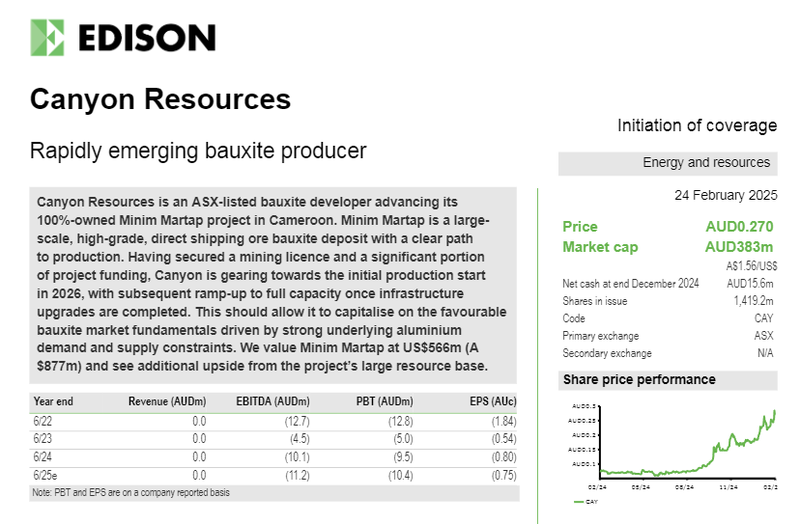

CAY research note values project at up to A$1.07BN

Our 2025 Wise Owl Pick of The Year Canyon Resources (ASX: CAY) just had a research report written for its Bauxite project in Cameroon.

The report was published by Edison Group - a London-based research house who write sponsored research for listed companies.

Small cap stocks rarely ever get research reports written about them so it’s good to see someone lay out the CAY story in this format.

The report put a valuation on CAY’s project of A$877M with an upside case of A$1.07BN which is pretty strong given CAY’s current market cap is ~$542M (undiluted).

Check out the full report here: Canyon Resources — Rapidly emerging bauxite producer

Our key takeaways from the Edison report:

On CAY’s project and its financials:

- The report reiterates how there are very few exposures to bauxite on the ASX and especially at the size/scale of CAY’s project (in the small cap end of the market).

- The report specifically mentions how CAY’s project is unique from a capital efficiency perspective - Edison mention the US$426M investment by Chinalco into a 6mtpa bauxite project with a capital intensity of US$70 per tonne. Comparing that to CAY’s project which has capital intensity closer to US$65 per tonne.

- CAY’s project once developed up to a 6.4 Mtpa capacity would still have a 20 year+ mine life based on its current reserves. The project has a 1BN tonne JORC resource so there is plenty of scope to increase mine life too.

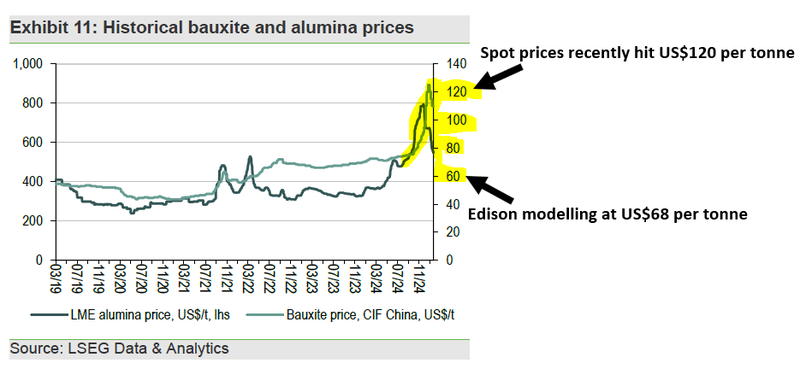

- Edison estimated an NPV for the project using a bauxite price of US$68 per tonne of A$877M. (keep in mind spot prices were almost double that recently…)

- At full capacity Edison’s modelling is estimating annual revenues of US$371M and EBITDA of US$200M.

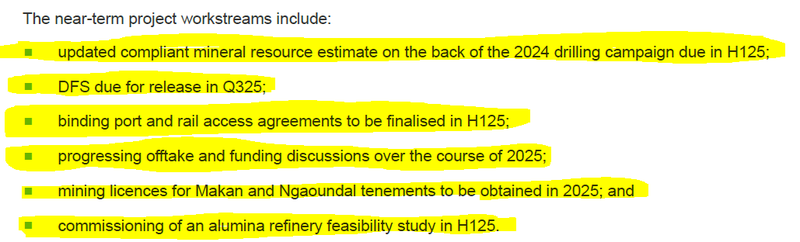

The report also highlighted near term catalysts for CAY:

On the quality of CAY’s resource:

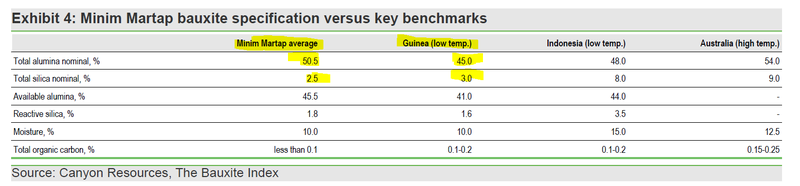

The report also touches on how CAY’s project stacks up against other bauxite from other jurisdictions (highlighting the low silica, high alumina %) which is good for showing how easily CAY’s bauxite can be processed into aluminium.

The main takeaway here is how well CAY’s resource stacks up against bauxite coming out of Guinea…

On CAY’s strategic partnership with Eagle Eye Asset Management:

The report highlights how EEA have committed to up to US$123M in debt financing for the projects CAPEX (rail stock) which de-risks the project significantly from a financial perspective - covering ~50% of the projects required CAPEX.

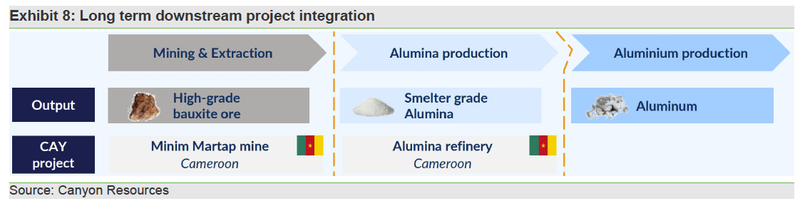

Edison also made mention of the recent media reports that EEA were in talks with the Cameroon government over a state owned aluminium producer Alucam. The report highlighted the potential for CAY’s project to be vertically integrated if EEA take a stake in that company.

On logistical infrastructure:

Edison highlighted the infrastructure upgrades that have gone on in the country since 2021:

- Since 2021 ~68 rail bridges have been upgraded.

- ~330km of the 500km rail line that runs to CAY’s project has been refurbished.

- The state owned rail operator confirmed the rail lines are rated for 20-tonne loads and can accommodate the tonnages required by CAY.

- €243m of funding which is being used to upgrade another 330km of railway lines which expects to increase rail capacity eve further by 2030.

- The port of Douala where CAY plans to ship its bauxite out of recently received €142m IN funding from the African Export-Import bank and €60m from a project company to upgrade its facilities. Those upgrades are expected to be completed within 60 months.

- There is also a push to develop an industrial zone around the port which is expected to be completed by the time CAY is ready for ramp-up.

The key takeaway’s from this is that there is scope for CAY to progressively increase the throughput from its project.

CAY’s 2022 Bankable Feasibility Study was based on production of up to 3.5mtpa.

BUT with a 1BN+ tonne JORC resource and the infrastructure upgrades being completed, by 2030 it looks like CAY will have optionality around increasing that throughput as it see’s fit.

This type of inherent upside in a project is what major players look for when considering potential takeovers. Assets they can operate efficiently and upscale/downsize as market demand changes.

On the Bauxite market/macro:

The report talked about the supply side issues in the bauxite space, and how further disruptions could impact prices even more. The report mainly mentioned:

- The mid-2023 ban on exports by Indonesia (third largest supplier of bauxite to China.

- 2024 saw bauxite export restrictions in Guinea in October, which followed supply disruptions at the end of 2023 due to an explosion at Guinea’s main oil terminal in Conakry.

- Production interruptions in Australia from Alcoa (Kwinana plant shutdown) and Rio Tinto (Yarwun and Queensland operations).

The report specifically mentioned “China’s reliance on Guinea’s bauxite” and how the risks to supply would mean the market needs new supply sources developed (like CAY’s project).

The report also makes mention of potential increases to aluminium demand from electric cars.

New cars are expected to have a lot more aluminium in them at ~81kg on a gross basis with the biggest increase coming from EV’s. Increased solar PV uptake is also expected to contribute to increased demand.

By 2030, the report suggest demand could increase by ~15-22mt in additional supply by 2030 (comparing to current production of ~70mt).