CAY Goes Again after BFS, New CEO and a Surging Bauxite Price

Disclosure: The authors of this article and owners of Wise-Owl, S3 Consortium Pty Ltd, and associated entities, own 3,000,000 CAY shares at the time of writing this article. S3 Consortium Pty Ltd has been engaged by CAY to share our commentary on the progress of our investment in CAY over time.

Our Investment Canyon Resources (ASX:CAY) released a Bankable Feasibility Study (BFS) for its 100% owned bauxite project in Cameroon, Africa. Today we breakdown the study, recent share price movements, and specific risks to our Investment.

As shareholders, we’re acutely aware that the stock is down 40% since it entered (and since emerged from) its trading halt on 21 June to release its BFS.

However, we think that fall doesn’t truly reflect the findings from the BFS and the massive potential of this project — one of the largest undeveloped, high grade direct shipping bauxite deposits globally.

We also think that the share price decline can be attributed to a couple of things...

First, during the seven weeks that the company was in suspension, the stock market took a beating with the ASX dropping 15% and small caps faring even worse.

News of a $5M cap raise at 4.5c, announced alongside the BFS, was not well received by existing shareholders who missed out on the heavily discounted shares but had to accept the financing solution (including us).

We think that the discounted raise happened because CAY needed the cash, but the market conditions had deteriorated to the point where investors were reluctant to finance small cap companies if not at large discounts to share prices.

In poor market conditions, companies raising funds are 'price takers', meaning they take the price given to them by the financing institution.

It’s been a rough ride for us with CAY so far. After watching on the sidelines for almost 18 months, we Invested in CAY back in February at 10c.

Shortly after, the company went into suspension to clear up licensing issues, then was suspended AGAIN due to delays with its BFS... all while the market was crashing in the background.

CAY is now trading at 4.5c (the same price the Placement was completed at) compared to our Initial Entry Price of 10c.

Since our Investment in CAY, we have seen three key risks play out including "geographic risk", "funding risk" and "permitting risk" - more on these risks later in this note.

That said, we think the BFS was overwhelmingly positive, confirming that CAY’s Minim Martap Project has the quality and scale to help meet the massive long-term global bauxite demand that’s coming in the years ahead.

Now we just need to wait for 4.5c placement shares to be digested and hopefully we’ll see CAY re-rate as it progresses against our milestones.

With a JORC resource of more than 1 billion tonnes, we already knew Minim Martap as one the largest undeveloped, high-grade direct shipping bauxite deposits globally.

Bauxite is a key ingredient in aluminium, a material that’s critical to a low-carbon future including wind power, solar and energy storage.

The BFS has now confirmed the project as a robust long-term project, producing some of the highest grade bauxite in the world for an initial 20 years of mining.

Further, the BFS pointed to project operating costs being considerably lower than was indicated in the PFS phase, resulting in improved project economics.

Completion of the BFS was a key objective that we wanted to see CAY achieve "in the first half of 2022", as listed in our Investment Memo:

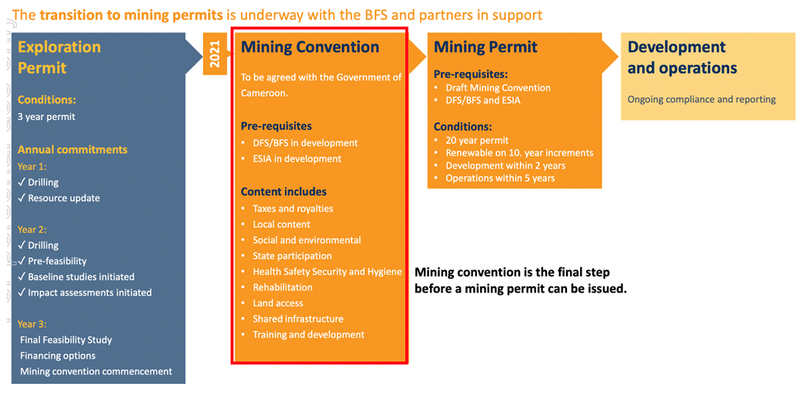

Its completion and delivery pave the way for the execution of the Mining Convention and the grant of the Mining Permit - which seems all but a formality now that the window for objections has closed.

The BFS is also a key milestone towards securing strategic financing, offtake and government agreements and CAY notes that strategic offtake and funding discussions are advancing.

CAY has also recently appointed a new CEO, Jean-Sebastien Boutet, who has more than 16 years in the bauxite and aluminium industry.

What we like is that Boutet has significant experience in securing key partnerships, and we view this as a well timed appointment as CAY looks to shift its focus to financing and project development, with key offtake and other commercial partnerships progressing.

Bauxite supply, and the broader aluminium industry, is facing persistent supply shocks due to geopolitical events, which underlines the importance of new bauxite projects such as CAY’s Minim Martap Project.

With strong project economics indicated by the BFS and despite recent share price woes, we think CAY is in the right place at the right time to capitalise on this opportunity.

What to take from the BFS

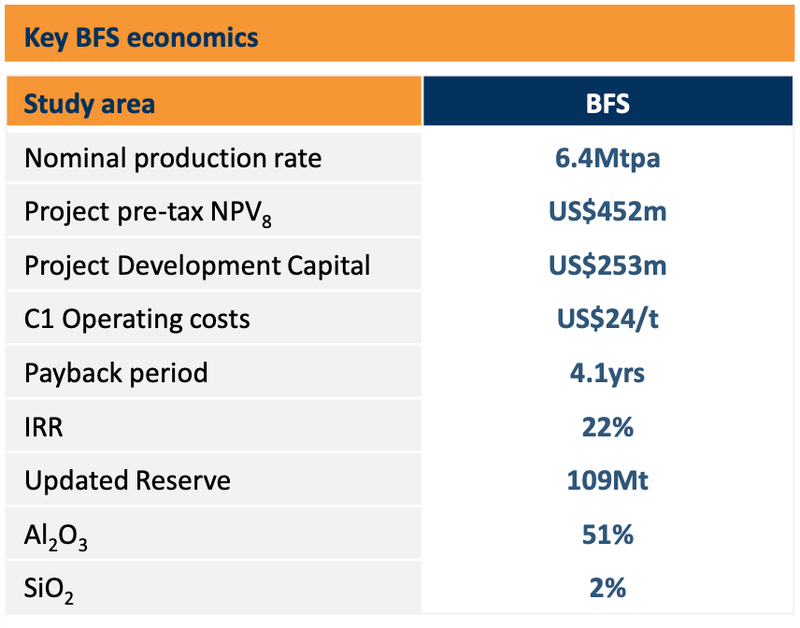

At 107-pages long the BFS is a lot to digest, so here’s a snapshot of the project economics:

And a summary of what we took away from the study...

Increased production projections

As per the BFS, the project is expected to produce up to 6.4Mt of high-grade bauxite per year for 20 years — a 28% increase from the earlier PFS.

The project has a total JORC Mineral Resource estimate of 1,027Mt, at 45.3% total Al2O3 and 2.7% total SiO2.

Yet this 20-year mining schedule represents just one-tenth of the total current 1 billion tonne Minim Martap resource. CAY notes that technical studies have identified potential to further increase the export tonnage from the project.

Furthermore, this billion tonne total resource only represents 17 out of 62 bauxite plateaux on the total Minim Martap project area.

High grade bauxite, with low silica content

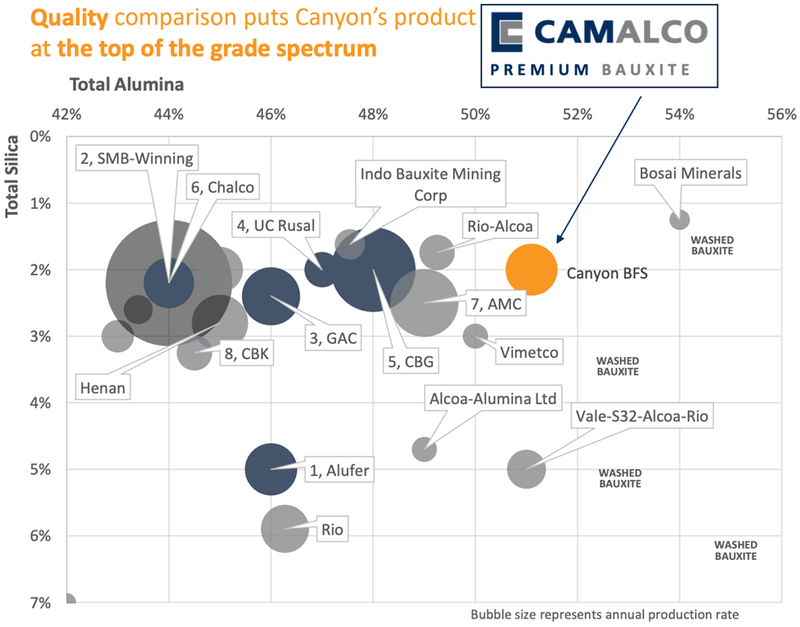

The Minim Martap resource is of considerable significance due to its relatively high alumina grades combined with its low silica grades.

The high-grade bauxite is anticipated to average 51.1% total alumina, and total silica to average 2.0% for the first 20 years of operation.

(While wanting high-grade bauxite is self explanatory, low silica concentrations are important too as the silica reacts with comparable amounts of alumina to form insoluble sodium aluminium silicate, which is then lost as refinery plant residue.)

Based on its high available alumina content and low reactive silica, the bauxite product has a high in-situ value compared with other bauxite projects globally. And over the initially modelled 20 years of mining, CAY expects to produce some of the highest grade bauxite in the world.

Here’s a product quality comparison between Camalco (CAY’s wholly owned subsidiary in Cameroon) and its peers:

(Camalco SA is the local Cameroon subsidiary of Canyon Resources that has 100% ownership of the Minim Martap Project)

A low cost operation

The BFS estimated considerably lower operating expenses than in the PFS phase, resulting in improved forecast project economics.

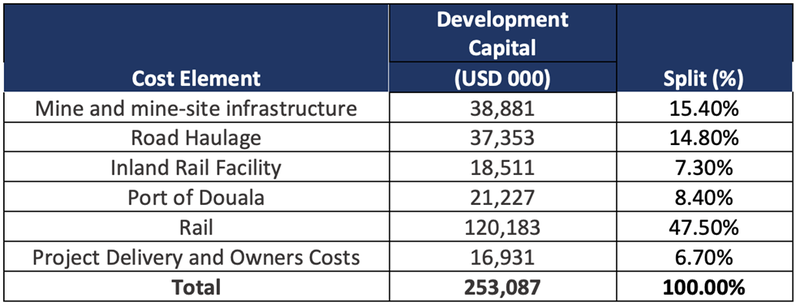

Upfront project development costs of US$253 million are anticipated, including the capital cost of the initial fleet of the acquired rail rolling stock:

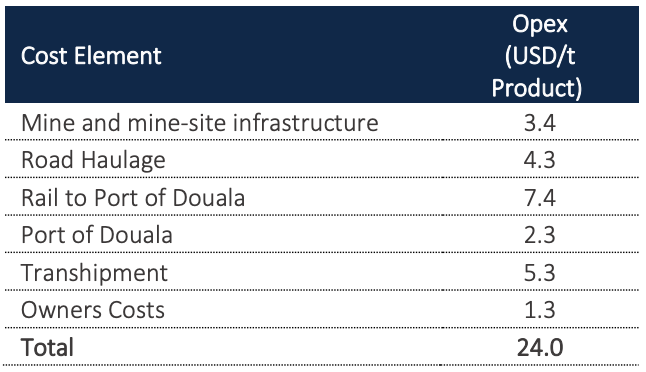

Here’s a summary of the operating costs (OPEX) that support the Ore Reserve estimate, for the economic modelling period of 20 years:

Total C1 operating costs, or 'direct' production costs, come to US$24/t for a 51.1% Al2O3 export product. This makes Minim Martap bauxite very competitive, supplying some of the world's highest grade bauxite.

The reasons for the substantially reduced operating expenses and improved project economics from the PFS stage can be attributed to optimised rolling stock configuration and scheduling which has increased rail capacity.

Project valuation

The BFS determined a pre-tax project NPV of US$452M, (on a joint venture basis with the Government of Cameroon, on granting of the Mining Licence in which CAY will own 90% of the project).

Given the strong project economics and globally competitive operating costs, CAY expects to produce some of the highest grade bauxite in the world for an initial 20 years of mining.

This reflects a 22% project IRR and a payback period of just 4.1 years.

Bauxite pricing as a critical metal

Considered a critical raw material by the EU, bauxite is the ore needed to make the "green metal" aluminium. Aluminium has infinite recycling capacity, and is a critical metal in the technologies behind wind power, solar, and electric car batteries.

To make a single ton of aluminium four tons of bauxite are needed, and according to Volkswagen, 126 kg of aluminium is used in a typical 400 kg electric car battery — far more than any other metal.

With the anticipated growth in this sector, aluminium’s use in batteries and other electric vehicle components will see automakers double their aluminium consumption by 2050.

With this in mind, the high price of bauxite should come as no surprise.

Short term factors are also supporting a higher bauxite price.

In addition to the growing use of aluminium in new technologies and growing Chinese bauxite demand , Russian producers’ Guinean bauxite exports face a clouded future due to the Ukraine conflict .

While there is uncertainty around the impact of an upcoming ban on Indonesian bauxite exports expected in 2H 2022, we think that the previously mentioned supply side factors could play into the economics behind CAY’s proposed project.

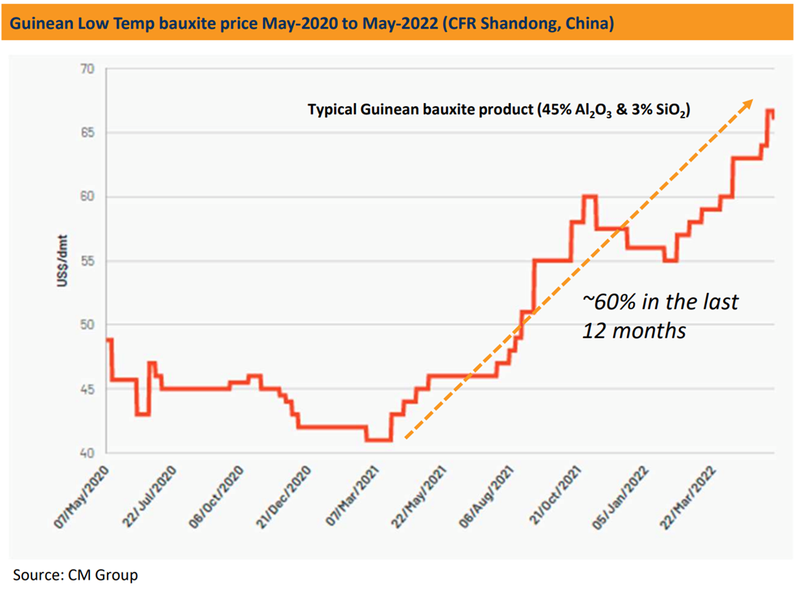

Here you can see the recent price rise of typical Guinean bauxite product to China in the two years to May 2022:

While that was a fast and sharp rise, we suspect this is more than just a short term trend higher in prices.

The surging bauxite price isn’t just about short term issues though (inflation, Ukraine, supply) — global demand for primary aluminium is expected to increase by 50% in the next thirty years.

The project NPV, as per the BFS, was based on an average bauxite price of just US$45.22/t FOB over the mine life for Minim Martap’s high grade bauxite averaging 51.1% Al2O3.

However, as above, bauxite exports to China have been much higher during the first quarter of 2022 with imports up 15.4% from a year earlier and setting new highs.

The Chinese import price is the most relevant for CAY as this is a likely destination for much of the company’s bauxite.

This is owing to the strong relationships with potential Chinese offtake partners that the company’s new CEO Jean-Sebastien Boutet has established over his career and continues to build for CAY.

Alongside China, CAY also expects to export its bauxite to India and to the Middle East:

Bauxite market challenges

Indonesia is banning the export of unprocessed minerals, including bauxite, by the end of 2022.

China imports around 30% of its bauxite supply from Indonesia, but is even more heavily reliant on Guinea bauxite supply — around half of its bauxite imports coming from Guinea. So while China believes that the gap created by an Indonesian export ban could be further filled by Guinea, new legislation by the African nation may change that.

As Africa's biggest producer of the aluminium ore, Guinea also wants to channel its mineral wealth into economic development. It has pressured companies operating in the country to build local facilities to refine bauxite into higher value alumina.

The country’s junta (government military) has set deadlines on bauxite mining companies to present a timeline for the construction of alumina refineries. And while these deadlines appear to have so far been largely ignored, the political risk of non-compliance exists for downstream users.

Bauxite exports from Guinea made up nearly all (95%) of the total bauxite exported out of Africa in 2019. So clearly a crackdown that forces local bauxite miners to refine bauxite into alumina adds a real layer of political risk to producers sourcing bauxite from Guinea.

Therefore, we think a new African bauxite source (maybe from Cameroon) would be timely to help fill the cut in exports out of Indonesia and potentially reduce exports of the bauxite raw material out of Guinea.

CAY boosts management team

With the successful completion of the capital raise and the release of the BFS, Phillip Gallagher has stepped down as Managing Director with Mr Jean-Sebastien Boutet assuming the role as of 1 July 2022.

Boutet is an experienced metals and mining executive with more than 16 years in the bauxite and aluminium industry.

He has more than six years experience in West Africa, including at Alufer Mining, an independent bauxite mining company that discovered and developed the now operational Bel Air bauxite deposit.

Previously, he was on the board of Compagnie des Bauxite de Guinée (CBG) while working as Commercial and Market Development Director for Alcoa Corporation.

What we like is that Boutet has significant experience in securing key partnerships, and we view this as a well timed appointment as CAY looks to shift its focus to financing and project development, with key offtake and other commercial partnerships progressing.

What’s next?

Execution of the Mining Convention agreement with the government 🔄

With the BFS out of the way, and the existing port and rail infrastructure determined to be suitable for CAY’s project (MoU in place with the Port of Douala to finalise commercial terms), we can look ahead to the execution of the Mining Convention with the Government of Cameroon.

CAY confirmed that the required documentation has been forwarded by the Minister of Mines to the Prime Minister of Cameroon for approval before signing.

The Mining Convention is the precursor for a Mining Permit application and is expected in the coming quarter.

It should really just be a formality at this stage as the period for objecting to the Mining Permit application has now passed.

Converting the Mining Convention to a Mining Permit was the #1 Objective that we wanted to see CAY achieve this year so we look forward to soon ticking it off the list.

We think that a signed Mining Convention agreement will ultimately open the door to CAY securing binding financing and offtake agreements with interested parties, and as a result see it as the major catalyst for the company in the coming months.

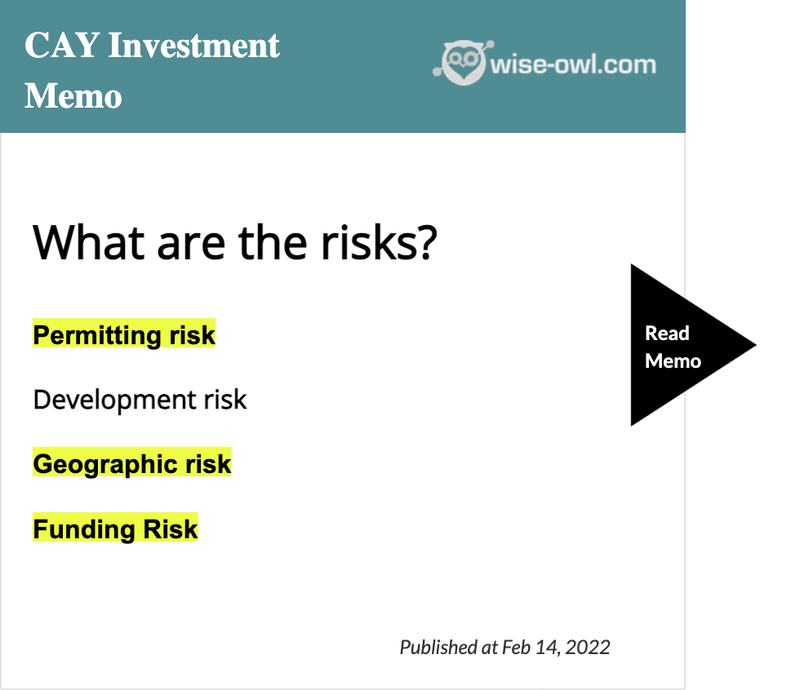

What are the risks?

So far we have only been Invested in CAY for ~5 months.

In that time we’ve had to contend with company developments that have touched on three specific risks that we set out in our 2022 CAY Investment Memo.

We would prefer that our Portfolio companies manage these risks so that they are non-issues, but the lifecycle of a small cap company means that sometimes these risks can materialise.

Importantly, by detailing the risks in our CAY Investment Memo, we were not blindsided by these developments and knew how to react to them objectively as opposed to emotionally.

The risks that materialised are as follows:

Permitting risk:

Only a week or so after our initial Investment in CAY, the company was put into a trading halt pending licensing issues with respect to two of its exploration prospects.

The two prospects sat outside of CAY’s JORC resource area, but the confusion with respect to permitting still needed to be resolved.

It didn't take CAY long to have this issue resolved but it was still unsettling for investors.

To see our coverage of what went on and how CAY managed the risk check out our last CAY note here: 15 Ministries now signed off on CAY’s Mining Convention – Final Sign off by Government Next

Geographic risk:

The geographic risk in some ways ties itself back to the permitting risk that materialised.

The confusion around the permitting issues came after what appeared to be miscommunication between different stakeholders in Cameroon.

Although the issue was resolved quickly, it highlights the fact that CAY’s project is subject to the volatility of doing business in this part of the world.

As investors, we are aware of the material geopolitical risks inherent in our CAY Investment.

Funding Risk:

In our 2022 Investment Memo we mentioned that given CAY’s project location in Cameroon - a developing mining jurisdiction, financial institutions and capital markets would view CAY as a high-risk investment when it came to providing funding.

We also specifically flagged in our Investment Memo that "in the short term, CAY [would be] reliant on tapping the market for funds as it moves toward bigger financing rounds".

When both of these factors combined with a broader market sell off, it made securing financing difficult without providing a large discount to institutional investors.

In poor market conditions, companies raising funds are 'price takers' and take the price given to them by the financing institution.

The discounted capital raise appears to be a result of the negative market sentiment and the company’s NEED to raise capital at that time.

Generally we would point out the potential impacts of broader market sell offs with a "market risk" factor, which definitely became an issue for CAY ahead of the BFS release and capital raise.

Our 2022 CAY Investment Memo

Below is our 2022 Investment Memo for CAY where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company’s performance against our expectations 12 months from now.

In our CAY Investment Memo you’ll find:

- Key objectives for CAY in 2022

- Why we continue to hold CAY in 2022

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.