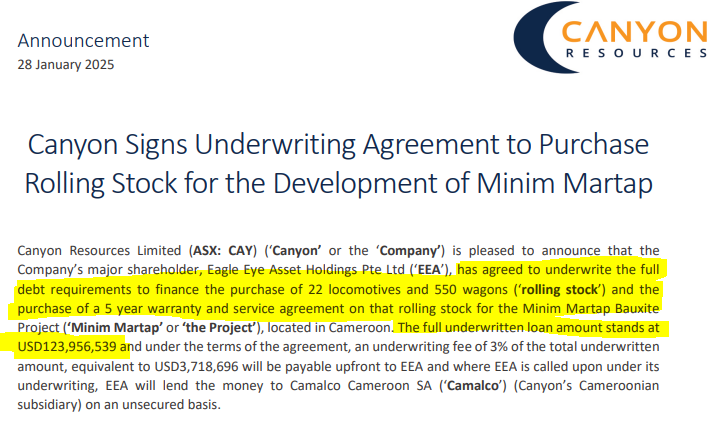

US$124M in financing now underwritten - CAY can buy trains to get its bauxite to market - 50% of CAPEX

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time.

This mine needs some trains.

22 locomotives and 550 wagons to be precise.

Today, our Investment got the US$124M of financing support it needed to get those trains rolling.

Last week we announced our 2025 Wise-Owl Pick of the Year, Canyon Resources (ASX:CAY).

CAY is developing a Tier One bauxite asset in Cameroon, Africa.

Bauxite is the key ingredient to make aluminium.

Aluminum is a critical metal for the energy transition and the defence industry.

The bauxite price has been looking very strong lately...

Bauxite is a “bulk commodity” - like iron ore - meaning it's fairly simple to mine and process.

The challenges of building a profitable bulk commodity mine are more around transporting that heavy (but valuable) load to whoever wants to buy it.

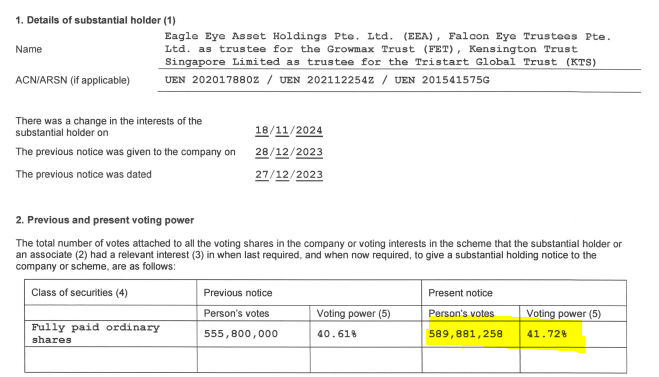

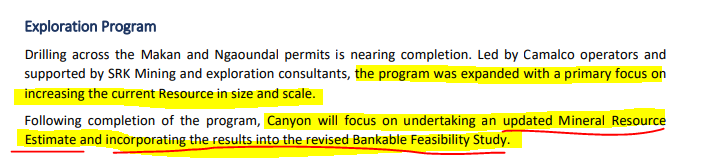

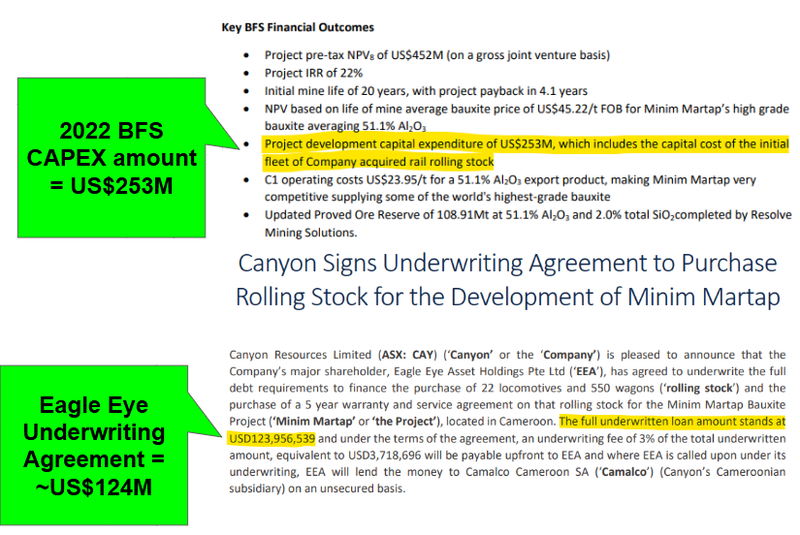

Today, CAY made a big step forward in the development of its bauxite mine - its largest shareholder, Eagle Eye Asset Management, has agreed to fully underwrite a loan for ~US$124M.

The US$124M underwritten amount is circa 50% of the CAPEX from CAY’s 2022 Bankable Feasibility Study.

Eagle Eye holds ~ 41.72% of CAY shares - a lot of skin in this game - and we will cover more on those guys, and the other ASX stock it was involved in, later on in this note.

The underwriting is to finance the purchase of 22 locomotives and 550 wagons - this is called ‘rolling stock’ in the train game.

As well as the actual locomotives and wagons, the underwritten amount provides funding for a five year warranty and service agreement.

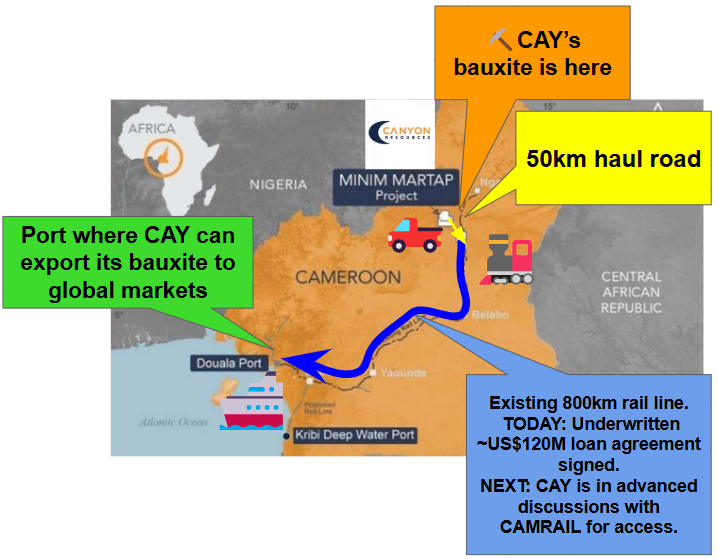

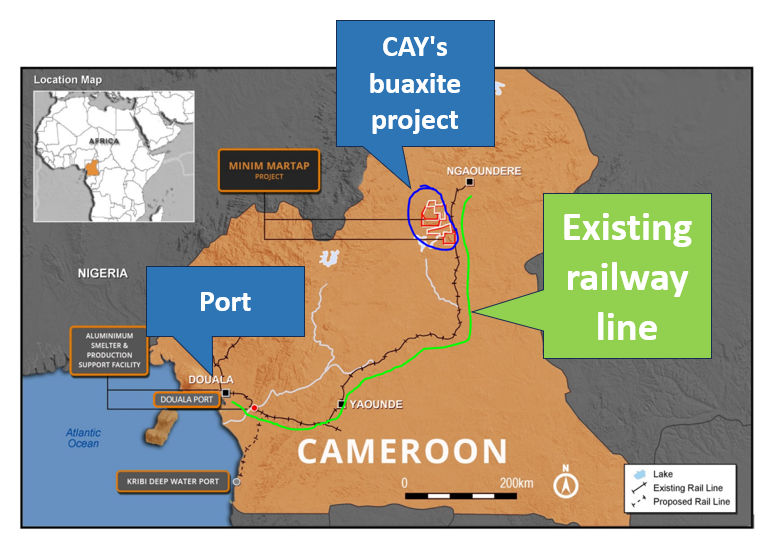

The plan is for CAY’s rolling stock to transport its bauxite along a 800km existing rail line to the existing port.

Having its own rolling stock will ensure CAY is in control of logistics, cost efficiency and reliability.

Securing CAPEX funding is often the biggest hurdle to getting a mine developed, so having a pathway to getting half of it locked away is a big step forward for CAY.

CAY’s cornerstone shareholder, Eagle Eye Asset Management, and now its new loan underwriter, has long term development and mining experience in Africa (again, more on these guys later).

We think a cornerstone investor like Eagle Eye with deep pockets and regional experience is exactly what CAY was missing for a long time.

(We first Invested in CAY back in 2022)

A big part of why we made CAY a Pick of the Year last week was because we are backing Eagle Eye to unlock milestones like today - which would have taken a company without a cornerstone backer potentially years to try and secure.

Before we dive deeper into today's news, you can check out last week’s Pick of the Year initiation note here - it provides a good overall summary of the company, why we Invested, and what we are looking out for over the coming years from our Investment:

Canyon Resources (ASX: CAY) - 2025 Pick of the Year

Big chunk of CAY’s CAPEX is now underwritten

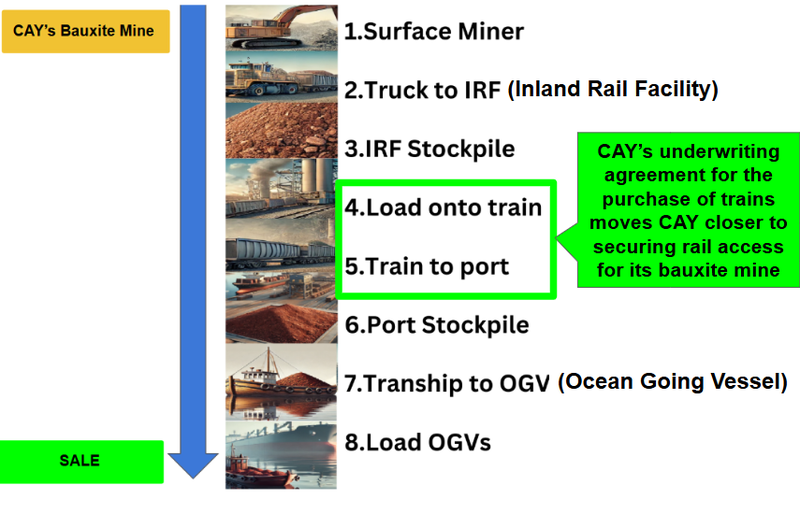

CAY’s project is relatively simple to mine - it's a “Direct Shipping Ore” (DSO) project (similar to iron ore projects).

Below are the steps it takes from mine to sale:

Most of the CAPEX is for transport infrastructure.

Once the infrastructure is sorted - from both a practical and financial perspective, we think it should be fairly easy to get the rest of the project financed and into construction.

We’ve outlined the key road, rail and port infrastructure involved in getting CAY’s bauxite to global markets in a map of Cameroon below:

That blue arrow on the map indicates the 800km railway track from mine to port.

Today’s news on underwriting of the purchase of locomotives and wagons really firms up the rail side of the infrastructure for CAY.

Underwriting is when an individual or institution (Eagle Eye in this case) takes on financial risk for a fee - think of it like a financial backstop for CAY.

For CAY to be in a position of strength in regards to funding its rolling stock is important for negotiations with Cameroon’s railway operator, a company called CAMRAIL.

(CAY is in advanced discussions to secure rail access).

And it gives other potential financiers of CAY’s project greater confidence when funding.

Which again, is why we think today’s news is so important for CAY.

And in terms of funding, the picture is now much more clear given how much of the total CAPEX in the 2022 Bankable Feasibility Study (BFS) was attributable to the purchase of rail rolling stock (trains).

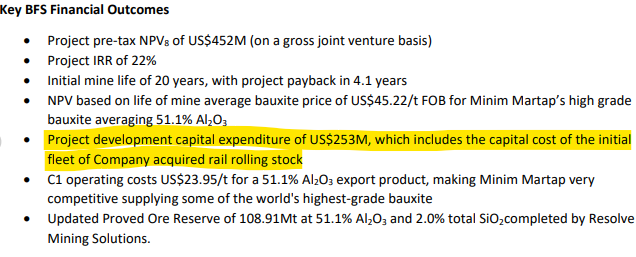

For CAY the 2022 BFS showed that the total CAPEX for the project was US$253M.

That US$253M included the “initial fleet of company acquired rail rolling stock”.

(Source)

CAY’s biggest shareholder Eagle Eye has committed to underwriting ~US$124M - almost 50% of the 2022 BFS CAPEX required to get its project into production.

It’s also further proof that major CAY shareholder, Eagle Eye is firmly in CAY’s corner and can help in tangible ways to get the bauxite project developed.

Eagle Eye has been there and done it before...

Eagle Eye has long term development and mining experience in Africa, having successfully built companies through the various life cycle stages.

ASX investors may be familiar with the Eagle Eye name in relation to another small cap stock, Prospect Resources.

Eagle Eye were the single biggest shareholders in Prospect Resources leading up to the sale of its Arcadia Lithium project in Zimbabwe back in 2022.

Prospect sold that asset for ~$530M and then went on to return most of that money to shareholders.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. These products, like all other financial products, are subject to market forces and unpredictable events that may adversely affect future performance.

Eagle Eye holds ~41.72% of CAY and is therefore very interested in making sure CAY is a success.

(and they have been buying on-market pretty aggressively over the last few months)

(Source)

Given Eagle Eye’s deep pockets, and development experience in Africa, a big part of why we made CAY our Pick Of The Year in 2025 was its cornerstone backing.

But there are other reasons too...

Reasons we made CAY our Wise-Owl 2025 Pick Of The Year:

You can read our full 2025 deep dive note on CAY here:

Canyon Resources (ASX: CAY) - 2025 Pick of the Year

Below are the reasons we are Invested in CAY from this note:

1. One of the biggest undeveloped bauxite projects in the world

CAY owns one of the largest undeveloped, high grade bauxite deposits globally.

(Source)

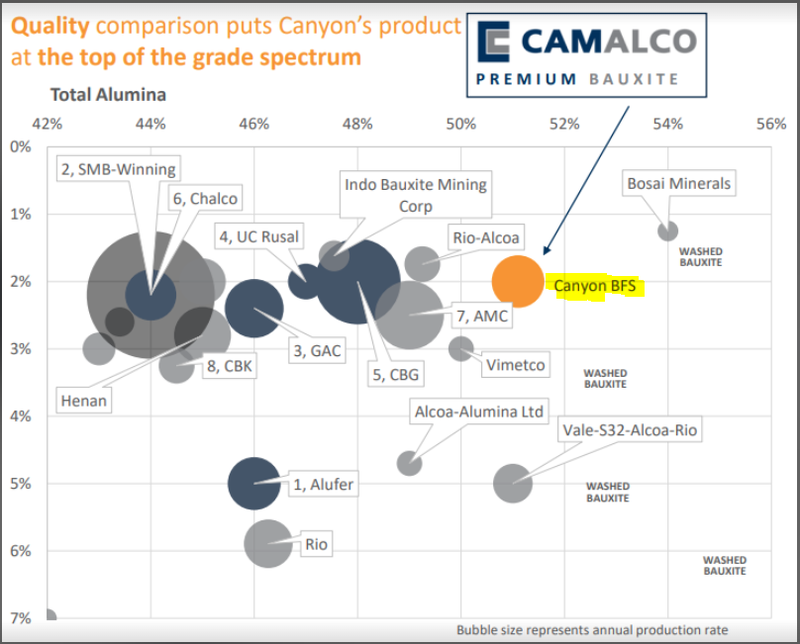

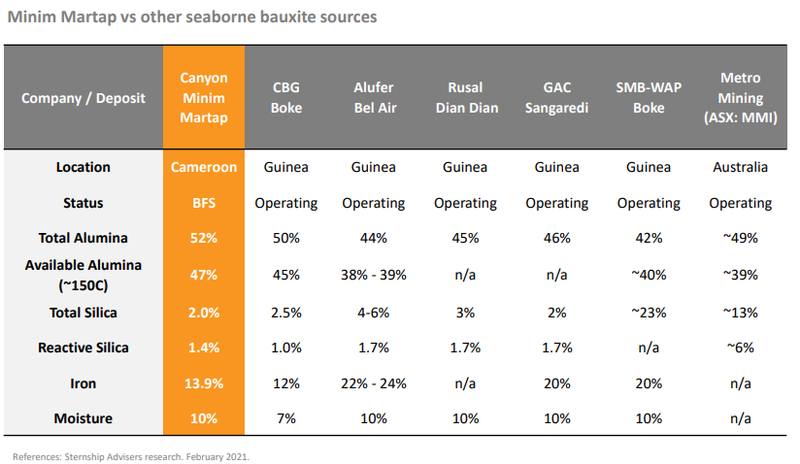

2. A “tier 1” asset with a giant resource and premium quality product:

When looking for “tier 1” assets there are two key factors: size and quality.

CAY’s project has a JORC resource of 1 billion tonnes at 45.2% Alumina

with a low silica content of 2.7% (less Silica % the better when it comes to bauxite)

It also has a reserve of 108Mt at 51.1% and 2% silica.

(Source)

3. Impending structural changes to the bauxite market

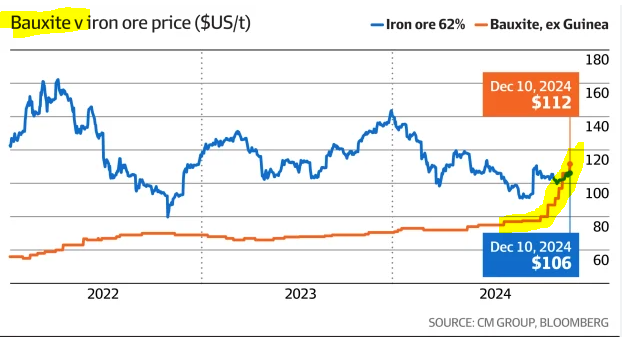

The bauxite market is extremely tight, which has pushed up bauxite prices significantly over the last two years. Global bauxite supply is concentrated with ~80% of production coming from Guinea and Australia.

Any disruptions to supply out of either of those countries could impact the market massively.

Guinea is the primary bauxite supplier in West Africa and the 2nd biggest producer globally... but they recently blocked an export out of the country.

Aluminium producers got spooked and are now looking to diversify their bauxite supply.

The blocked export sparked a rally in the bauxite price from ~US$60/tonne to where it trades now at ~US$110 per tonne.

(Source)

4. Permitting complete which paves the way to production -

Despite its rich natural resources Cameroon has had very few operating mines.

So, for CAY to secure a Mining Convention and 20 year Mining License, which took about 4 years of work, has significantly de-risked the project and provides a pathway to production.

5. The new major shareholders of CAY have had success in Africa

Eagle Eye Asset Holdings are the now biggest shareholders of CAY (owns 41.27%).

They were the biggest shareholders in Prospect Resources before the ~$530M sale of its lithium project in Zimbabwe back in 2021. We are backing the team to achieve similar success with CAY.

Eagle Eye Asset Holdings has purchased ~$4.1M of CAY shares on market between August and November 2024 (source).

6. Compelling project economics, improved by a strong bauxite price

CAY published a Bankable Feasibility Study (BFS) in 2022 showing an NPV of US$452M and CAPEX of US$253M over a 20-year mine line.

However, the price of bauxite has more than doubled since this BFS was published so we think these numbers could improve when CAY puts out its updated study.

In addition CAY’s BFS is only from its reserves, which is only about ~10% of the total current bauxite resource.

In the 2024 Annual Report CAY said it is working on a “revised BFS”, with all the extra drilling and rising bauxite price we assume the numbers are only going to get better.

(Source)

7. Project close to existing Infrastructure

The key to bauxite mining is always its proximity to rail to get to a port from where it can be shipped to export markets OR its proximity to smelting facilities where it can be refined into aluminium.

CAY’s project is in trucking distance (~50km) to a rail line that goes to a port.

In December 2020, Cameroon received a EUR$120M commitment from the European Investment Bank to upgrade one third of the railway line that CAY plans to use.

We are Invested in CAY for the long term, and we are hoping that a combination of the above reasons help the company achieve our Big Bet which is as follows:

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CAY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

How does this impact our CAY Investment Memo?

One of the key risks from our CAY Investment Memo was “development risk”.

This was a key risk because like other bulk commodities (think iron ore) the key to getting a project developed is to have modern transport infrastructure that is capable of moving tonnes and tonnes of material.

Today’s news means CAY has a clear line of sight to getting its infrastructure CAPEX funded.

~US$124M of the project’s total ~US$253M CAPEX requirements means CAY now has commitments for ~50% of the project’s financing.

(Source - June 2022 CAY 4C, Source - 28/01/2025 CAY Announcement)

We see today’s news mitigating development risk overall for CAY.

Development risk

The challenge with bauxite mines that sit in-land like CAY’s is that they need to have well-built out infrastructure for the projects to be considered economically viable.

Cameroon has recently made some upgrades to its rail infrastructure but to support a project like CAY’s will need to make more investment. There is a risk this is delayed or does not materialise and the project is deemed stranded.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

What are the risks?

While bauxite prices remain very strong, we are keeping our eyes peeled for any changes to the bauxite price - if the bauxite price falls this could hurt CAY’s share price.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

We are also paying attention to West African politics, in particular Guinea. Guinea may be considering a bauxite export ban, which it also may reverse away from. As Guinea is a major exporter of bauxite any change to the status quo here could alter the desirability of CAY’s project in the eyes of potential financiers.

Geopolitical risk

While we believe Cameroon’s current political climate is stable, there have been four coups in the last 4 years in the West Africa region. CAY’s project is subject to the volatility of doing business in this part of the world. Geopolitical risks form a significant part of CAY’s overall risk profile.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

We list more risks to our CAY Investment Thesis in our Investment Memo here.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.