Why we invest in IPOs and our investment approach

Published 11-APR-2022 12:44 P.M.

|

14 minute read

Yesterday we launched the newest addition to our Next Investors portfolio, Noble Helium (ASX:NHE) which is a pure play helium explorer looking to make a helium discovery of global significance in Tanzania.

The company listed on the ASX yesterday via an Initial Public Offering (IPO).

We have been invested in and have been following the story for almost a year, participating in the seed funding round when the company was being operated privately.

Here is our investment memo on why we invested in NHE and what we want to see the company achieve in 2022.

This hasn't been the only new IPO we have made an investment in this year though.

In a previous weekend update, we announced we would also be participating in the Sarytogan Graphite (ASX:SGA) IPO, which will be listing later this month.

The world is rapidly changing and the need for “new commodities” for the green energy transition and electric vehicle batteries has only come about in recent years, meaning that many of the best “new commodities” projects are not yet publicly listed, because there wasn’t significant investor appetite for them until recently.

Given some of our more recent investments are being made off market via IPOs, seed rounds or pre-IPO funding rounds, we thought it would be good to detail our approach to IPO/private market investing.

First of all, what does it mean to be “off market” or in the “private markets”?

We are all used to logging into our online brokerage accounts, waiting for the markets to open at 10am and looking at the bids and the offers to see at what price we can buy or sell shares.

That is the beauty of being a listed company, the investors capital is considered “liquid”.

That means if a shareholder of a public company is invested because they like its future prospects, but one day they need an extra $10,000 for a deposit on an apartment, wedding or holiday, they can go ahead and immediately sell $10,000 worth of their shareholding.

The private markets operate completely differently.

Investors are offered shares in private unlisted companies that are most of the time working with extremely small budgets and are trying to build projects from the ground up.

These opportunities carry higher levels of risk, as a future liquidity event is not guaranteed, and there is potential to quickly lose all of the investment, especially if the company runs out of money and can't find any new private investors.

This is part of the reason these rounds are only available to s708 sophisticated investors only.

Some of the more common offerings are done via the following:

Seed raise 1:

This is often the riskiest stage, where the company is raising funds to start building or executing on its business plan. At this stage, a company has very little outside of a new idea and a dream to build it.

Seed raise 2:

This is just as risky as the first stage, but the idea has usually formed to a certain extent and the company has something it can show for the capital it has spent doing so. There can be several seed rounds but we will cap it at two for now.

Pre-IPO raise:

This comes after the company has delivered enough progress to soon need more capital to grow.

For an aspiring exploration company it might be some rock chip samples or EM targets. The company will look to raise funds which it will primarily use to try and get the company listed on a stock exchange.

The listing process can take 6 months and cost upwards of $500k depending on the size of the company - there is a lot that can go wrong to delay or cancel the IPO.

This stage is considered slightly less risky versus the seed stage given the company is now showing visibility towards getting itself listed and accessing larger amounts of capital at what the early stage investors hope is a higher valuation.

IPO raise:

This is the final stage of a company’s private life.

A company would have invested all of its pre-IPO funds formulating a concise business plan, future work programs, getting all its bookkeeping and compliance in order preparing for the listing.

At this stage, the company should be looking to raise a much larger amount of capital and detailing in its prospectus why it needs that capital (more on this later).

This is often seen as the least risky stage of a company's life from a capital raising and liquidity perspective, where investors hope that should the IPO conditions in the prospectus be met, the company will have access to the public capital markets to satisfy future needs for cash AND most investors will be able to freely trade their shares on market once a listing is achieved.

Investors in the seed and pre-IPO rounds will likely have full or partial escrows on their holdings, meaning they are prohibited from selling their pre-IPO or seed stock for a period of time after the IPO - this information can be found in the IPO prospectus.

In summary, there is a different risk/reward ratio in off-market investing.

To attract investors to the higher level of risk, pre-IPO and seed shares are offered at a discounted valuation that would be on offer had the company been listed and already trading on the ASX.

In return for the discounted valuation, investors accept the higher risk that the companies have nowhere near the level of transparency of a listed company, and there is no way to sell any of the shares issued, and the company may never get to the IPO stage at all.

This means there is always a risk of an indefinite lock up on the cash an investor hands over to the company in the event a company never manages to get listed, and the cash evaporates - and yes this does happen... often.

This makes sense though, as investors always make decisions based on risk/reward.

The risk of having capital locked up indefinitely in a private company with no prospects of securing further funding needs to be compensated via a raise at a lower valuation and vice versa when a company gets a listing done.

Sometimes we will be following and investing in a private project that we really like for a long time, hoping that one day it will IPO and raise enough cash to execute on their long term business plan, for example:

- NHE

- SGA

- TEE

Other times we discover and like a company that is already at IPO stage and participate at the IPO level only:

- KNI

- PFE

- EV1

Having established what the off-market investing landscape looks like, we can detail our investment approach when considering these off market opportunities.

First let's start with the “Seed” stage:

At this stage in a company’s lifecycle, we tend to focus on the people behind the idea and the macro tailwinds behind that particular idea, focussing mainly on the following questions.

- What is the macro thematic?

- Have the people behind the project built an idea from scratch before?

- Are the people passionate about the idea?

- Do the people have a clear vision and see something that others in the market/industry are missing?

- What is the capital structure like - are the operator founders incentivized enough to work for many years on this company, and does the valuation leave enough room for an attractive valuation in later rounds?

Given this is the riskiest stage of investing, with no line of sight to a public listing where an investor can get any capital back - this is by far the easiest round to lose 100% of an investment, and yes it happens often.

At this stage, we generally like to see the company tick all of the above boxes and we tend to pass on opportunities that don't.

The next step comes in the “Pre-IPO” stage:

At this stage we are generally comfortable with the people and the projects/ideas being built. All of our focus is on whether we think the company can get a listing done. The main questions we ask ourselves at this stage are:

- Are the macro tailwinds strong enough to get a listing done?

- Is the project advanced enough to warrant raising more money?

- Are market conditions strong enough to raise the capital?

- Is the capital structure still set up for future success?

This stage is generally less about the company and more about whether or not we think the markets would be open to seeing this company float, if we think the conditions are strong enough then we will increase our investment at this stage.

The final step comes via the “Initial Public Offering (IPO)”:

At this stage the primary question becomes, “why is the company raising capital?”

If we haven't already taken a position in a company in the earlier funding rounds, we will consider IPOs after satisfying these two main questions:

- What does the company plan to use the capital for?

- Does the company need to be listed to achieve its plans?

For a company to pass our filtering process, it will need to have strong answers to both of those questions.

An example was our investment in our Wise-Owl portfolio’s 2021 Pick of the Year, Evolution Energy Minerals (ASX:EV1), which we discovered and invested in only at the IPO stage.

The company listed raising $22M @ 20c per share with the primary goal of developing its “shovel-ready” graphite project in Tanzania.

This asset was spun out of another listed company.

The answer to the first question is: the capital will be used to progress its project closer towards a final investment decision and eventual development, with the aim of taking the company from explorer to producer, plus clear out a debt on the project.

The answer to the second question is: a listing would mean the company is seen as more investment friendly by all financiers when it came time to look at securing funding for the project. With US$87M in capital costs required to develop its project, a listing would make the raising process a whole lot easier for the company.

You can see our investment memo for EV1 here and how they are progressing on executing their post-IPO plans 5 months after they listed.

With the IPO process, we are primarily looking for a company that is raising capital to take its business/projects to the next level that wouldn’t be otherwise be achievable.

So how does our newest portfolio company Noble Helium stack up against this criteria?

- What does the company plan to use the capital for?

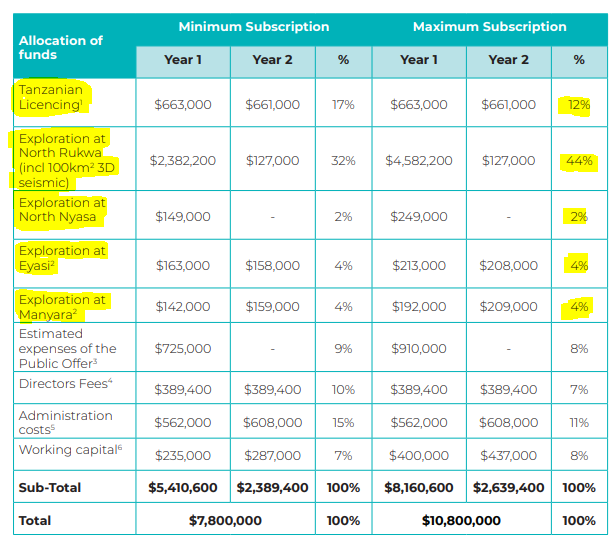

Noble Helium (ASX:NHE) listed in its prospectus that ~66% of its IPO funds would be directed towards exploration activities.

This includes the planned 2D/3D seismic data acquisition programs the company plans to run, which can be extremely expensive and hard to finance privately.

All of the target generation works will be completed leading up to the big 2023 drilling event where it plans to test its enormous mean unrisked prospective resource of 175.5 billion cubic feet (bcf) helium.

2. Does the company need to be listed to achieve its plans?

Our answer to this is yes. The reason being that Noble Helium is targeting a resource that could potentially be large enough to be globally significant.

With that enormous mean unrisked prospective resource of 175.5 billion cubic feet (bcf) helium, NHE is effectively targeting a discovery that has the potential to be the world’s third largest helium reserve behind the USA and Qatar, and the largest ever reserve held by a single company.

This sort of frontier exploration would be almost impossible to finance privately, and in the event of a successful discovery being made, would have an even smaller chance of being funded through to development.

These large scale opportunities require easy access to capital markets, which is what makes a listing a necessity.

📰 This week on Next Investors

⚠️NEW INVESTMENT ALERT⚠️

Why We’ve Invested in Noble Helium

We ended the week by launching the latest addition to the Next Investors portfolio, Noble Helium (ASX:NHE) which is aiming to discover a globally significant helium resource in Tanzania.

NHE currently has a mean unrisked prospective resource of 175.5 billion cubic feet (bcf) helium, meaning that if NHE’s resource can be proven, it has the potential to be the world’s third largest helium reserve behind the USA and Qatar, and the largest ever reserve held by a single company.

In just one of NHE’s four prospects, there could be enough helium to supply ~30 years’ annual global demand.

NHE is aiming to identify drill targets from a series of leads across similar geology in the East African Rift system - known as a “String of Pearls”.

The East African Rift System has become home to some of the largest, most consistently successful onshore African oil and gas discoveries with an impressive 80% success rate from 30 wells between 2006 and 2018.

NHE is now in a position to do all of the target generation works leading upto the big 2023 drilling event where it will test its project to see whether or not NHE can repeat the success of oil and gas explorers, but this time looking for helium in this part of Africa.

In our launch note which can be read here, we listed the top reasons why we invested in NHE. We also launched our 2022 Investment Memo which details what we want to see the company achieve this year and the risks to our investment thesis.

Click here to view our 2022 NHE Investment Memo.

📰 Read the full breakdown: Why We’ve Invested in Noble Helium

IVZ Identifies New Prospective Targets Ahead of First Well

On Thursday, our 2020 Energy Pick of the Year, Invictus Energy (ASX:IVZ) announced that it had completed 2D seismic processing — one of the final steps ahead of the upcoming maiden drilling program scheduled for June this year.

The seismic confirmed:

- prospectivity at the Mukuyu Prospect (previously named Muzarabani) including extensive seismic anomalies at multiple levels,

- a substantial new shallow target of 15km x 16km identified, and;

- an extensive array of prospects and leads along the basin margin.

IVZ is planning a two well drilling program in June and with all of the seismic data now processed, we suspect that more parties will start to show interest in the project. We expect to see a binding farm-in agreement signed before the 30th April deadline that IVZ set for its current non-binding partner Cluff Energy Africa.

With the first well expected to cost US$12M, we think that's a small price to pay given that the first well alone will hit no fewer than four primary target levels.

We like the risk reward on offer going into this drilling, given IVZ has an elephant scale target and the drilling could potentially be basin opening.

📰 Read the full breakdown: IVZ Identifies New Prospective Targets Ahead of First Well

In our other portfolios 🧬 🦉 🏹

🏹 Catalyst Hunter

GGE’s First Helium Exploration Well Now 10 Days Away

On Tuesday our 2021 Catalyst Hunter Pick of the Year, Grand Gulf Energy (ASX:GGE) confirmed that the drilling permit for its Jesse #1 well had been granted.

With mobilisation on site having started back in late March, GGE has drilling scheduled to start on 15 April 2022.

This news comes a day after GGE said it has identified three new independent helium prospects inside its project area after ~315km of 2D seismic data was reprocessed.

At the same time, GGE confirmed that given the size of its Jesse prospect (where the first well will be drilled), four step out locations had been identified which can be quickly brought up to drill ready status in time for a follow up drilling program in Q3 of this year.

More wells could potentially lead to more helium production and in turn, more revenues for GGE.

GGE is going into this drilling program with a P50 unrisked prospective helium resource of 10.9 billion cubic feet (bcf) of which 6.3 billion cubic feet (bcf) is net to GGE. With the drill permit now granted, the only thing left for GGE to do is get the Jesse #1 well spudded.

📰 Read the full breakdown: GGE’s First Helium Exploration Well Now 10 Days Away

🗣️ Quick Takes

NEW: We are now releasing our Quick Take opinions as they happen so you don't have to wait until the weekend to see them.

The link below will scroll you directly to the Quick Take related to the specific company listed.

Bookmark this page to read our Quick Takes LIVE

Below is a list of all of this week's Quick Takes:

VUL: Heat offtake - Germany's largest municipal energy supplier

VUL: Expediting geothermal energy amid German energy crisis

GGE: Commences Trading on OTCQB Market in the USA

GGE: Additional drilling locations identified

GGE: Onshoring semiconductor manufacturing a top priority for the USA

LRS: Gets new lithium tenement. Drilling to start immediately

ALA: Anagrelide patent for the United States

GAL: Galileo presents at Mines & Money

LCL: Video - recent milestones & potential economic development

MNB: Fertiliser prices up further, MNB plant design finalised

BPM: $3M cash raised ahead of Hawkins drilling

GTR: $5M raised via placement @ 2.1c and new Uranium acquisition

TMR: Private placement completed raising $762k

PFE: Aerial survey helps pinpoint targets for Hellcat campaign

88E: Icewine resource update due soon, farm-in partners show interest

AKN: AKN delivers 30% upgraded JORC resource at base metals flagship

AKN: AuKing to move to full ownership of flagship project

PUR: Share price up 100% in two days

PUR: Air core drilling commenced at its Warrior Project in WA.

TMZ: Positive metallurgy from historic intercepts, MRE coming

Next Investors: Pilbara Minerals MD on why lithium prices will remain strong

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.