LCL Unveils Mineral Resource Estimate as Gold Brushes up Against US$2000/oz

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 3,210,000 LCL shares at the time of writing this article. S3 Consortium Pty Ltd has been engaged by LCL to share our commentary on the progress of our investment in LCL over time.

It's been almost two years since we first suspected that our gold investment Los Cerros (ASX:LCL) may have a monster gold system on its hands.

Gold pierced the US$2,000 mark in the last three weeks as the crisis in Ukraine kicked off. Across the market we're noticing gold stocks like LCL have not been following the gold price higher.

BUT we don't think this lag will last long - especially for gold stocks that have a Mineral Resource Estimate like LCL now has.

We first recognised the potential of LCL at its Colombian gold project in April 2020, joining the share registry ahead of a discovery of a gold rich porphyry later that year at the project’s Tesorito Gold Porphyry.

Since then we’ve watched with anticipation — and completed multiple rounds of further investment — as LCL undertook an extensive exploration program, working towards Maiden Resource Estimate at Tesorito.

In this note you’ll find:

- Our take on the Maiden Resource

- Comparison of LCL’s Colombian projects and economics to its peers

- A review of how progress is tracking against the four objectives we set for LCL in 2022

- Sprott’s take on the resource announcement and its new 37c price target on LCL

- What is the optimised pit shell (the profitable way of mining the deposit)

- A deep dive into the Resource estimate and potential paths to production

A “Maiden Resource Estimate” is a widely accepted measurement of a gold resource - and now LCL has one, the market can evaluate how LCL’s resources stack up against other gold peers with defined resources.

The delivery of this maiden resource was the #1 Objective that we wanted to see LCL deliver this year, as per our Investment Memo here.

Having reported over a dozen spectacular gold intercepts over the past 18 months, yesterday LCL lifted the veil, revealing just how big its Maiden Resource is at Tesorito.

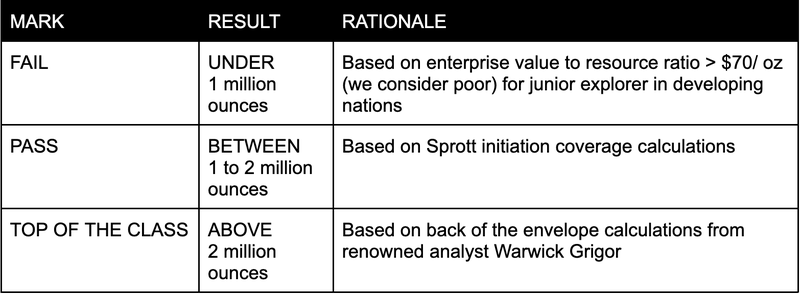

In our last note on LCL we set three sets of scenarios for the size of the JORC Resource. This was to gauge whether the Resource size came in above or below our expectations.

A Resource of 1-2 million ounces would be classed as a Pass, anything below 1Moz was a Fail and above 2Moz would be Top of the Class.

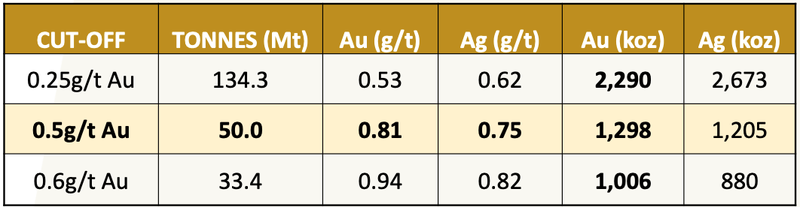

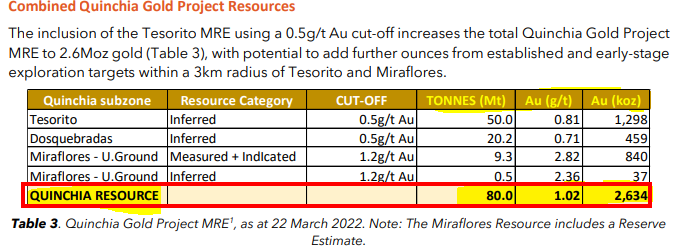

Yesterday we received the Maiden Mineral JORC Resource at 50mt grading 0.81g/t gold for a total of ~1.3 million ounces of gold.

That’s a decent sized resource and at first glance, it sits almost in the middle of the range, earning a very respectable Pass (*with a Distinction) from us.

But we think there’s more to the story here...

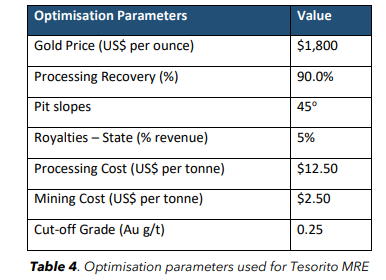

LCL confirmed that after running pit optimisations as part of the Resource estimation process, using a US$1,800/ounce gold price, the appropriate cut-off determined was 0.25g/t gold.

Using a 0.25g/t cut-off grade lifts the Resource to 134.3mt grading 0.53g/t gold for a total of 2.3 million ounces of gold.

This sits well above our “TOP OF THE CLASS” mark.

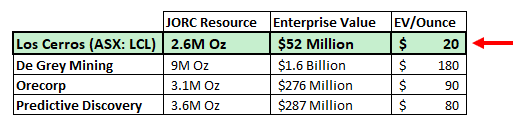

Comparing LCL to its ASX gold peers, we think the stock is looking extremely cheap with an Enterprise Value / Resource ounce of just $20 — keep reading for more on that.

Following the announcement, LCL released a presentation and a video in which Managing Director Jason Stirbinskis provides a good overview of the project and walks listeners through the result:

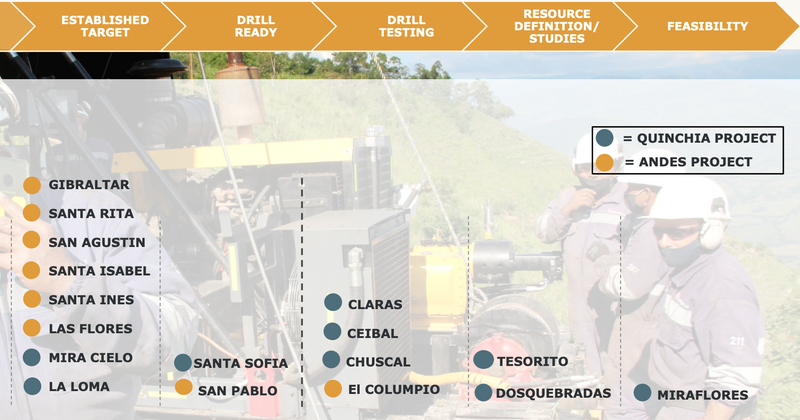

LCL is confident the Quinchia Project will evolve into a cluster of economic gold deposits, with multi-million ounce gold potential.

There are still lots of areas of interest for follow up and LCL sees potential for all of its gold resources to be developed as a “mining” hub with a central processing facility.

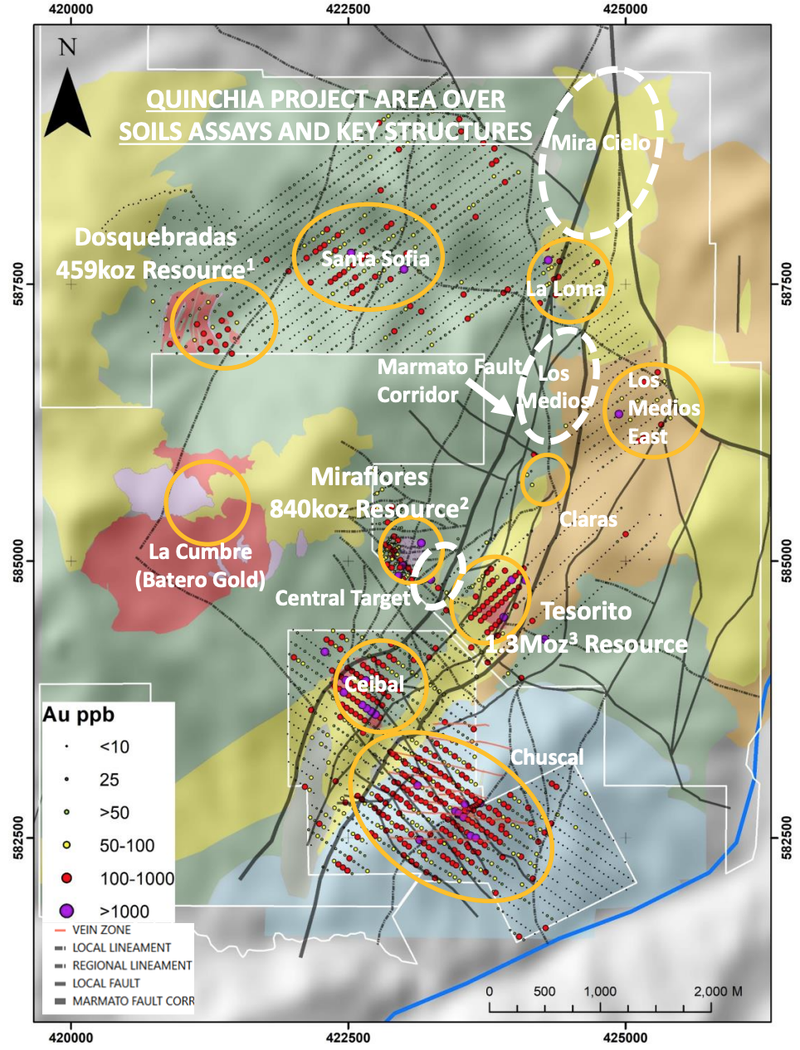

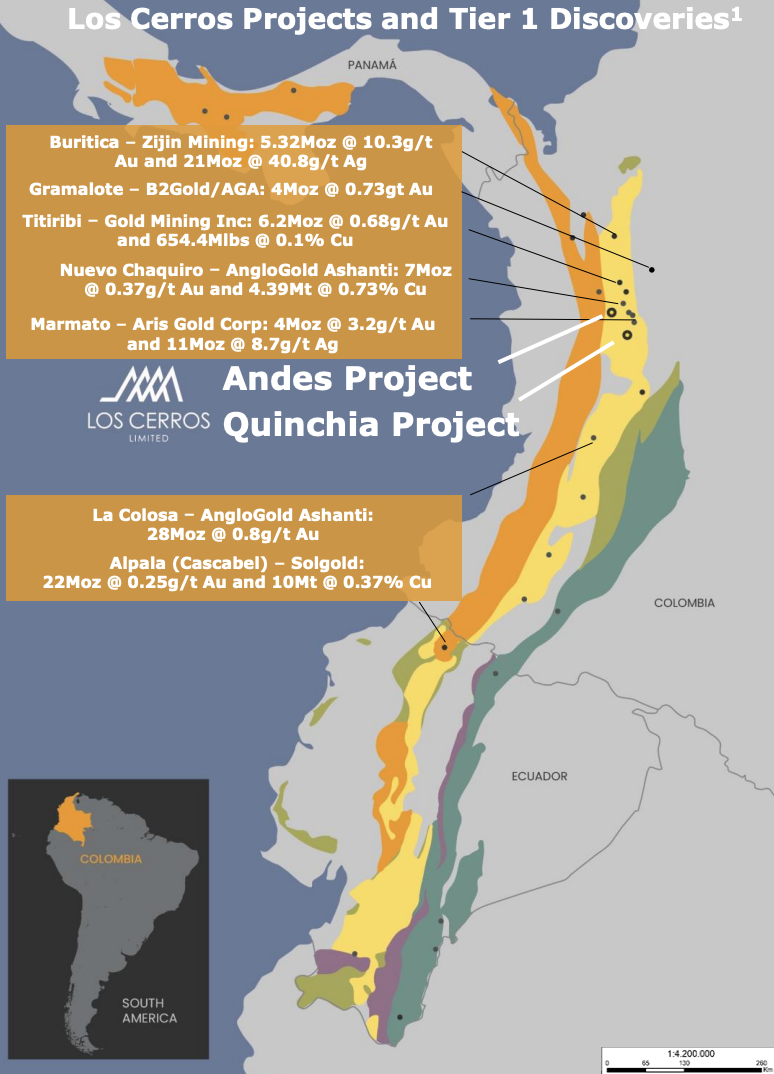

A quick look at the map below provides a visual of the potential to add further ounces from established and early-stage exploration targets within a 3km radius of Tesorito and the Miraflores deposit.

Tesorito is just one target of LCL’s at its advanced Quinchia Project in the mid-Cauca gold porphyry belt of Colombia — host to many multi-million ounce gold deposits

LCL has identified immediate growth opportunities at Quinchia through its large number of advanced and early-stage targets. Note the newly identified Claras target which will now undergo drill testing.

Meanwhile, ~90% of targets at LCL’s second project, the Andes Project, are yet to be mapped or systematically explored.

And with no fewer than five drill rigs now spinning all within a 3km radius of Tesorito-Miraflores (two with deep drilling capacity of more than 1km), a significant amount of cash in the bank ($17.4M), and a first class technical and operational team we can see why it is confident.

Of the five drill rigs now at Tesorito/Miraflores:

- 3 rigs are testing magnetic targets at Ceibal

- 1 rig is testing Claras — a new magnetic geophysical target 1km north of Tesorito within the Marmato Fault Corridor

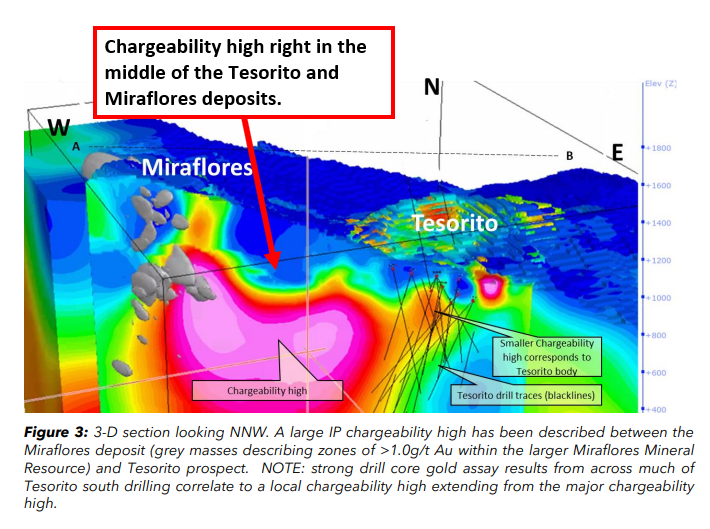

- 1 rig is testing the Central Target — a coincident magnetic and chargeability/conductivity high between Tesorito and Miraflores

Being located on the highly prospective mid-Cauca gold porphyry belt of Colombia, there are plenty of successful peer examples.

Colombian peer backed by majors

At first glance the Tesorito Resource grade of 0.81g/t may not excite “old school” gold experts, as historically 1g/t has long been viewed as the marker between being profitable or unprofitable.

Now that may have made sense historically — when gold was priced in the US$1,200/oz to US$1,300/oz range.

But now, with gold back around the US$2000/oz mark, lower grades are all the more economical.

Simply consider that if a project was profitable at 1g/t, when gold was at US$1,200, surely if the gold price doubles, for example, 0.5g/t should be the new cut off.

And it’s not just us thinking this way.

A 150km trek from Tesorito is the Gramalote open pit gold project (see map above). This project provides a good example of what development of the larger project at Quinchia may look like.

Gramalote is an advanced development project, currently at the feasibility stage and it makes for an excellent comparison for economic investigation of Quinchia.

Gramalote has a 4Moz resource grading 0.73g/t (at cut-off grades ranging from 0.15 to 0.18g/t) gold.

Gramalote’s 0.73g/t Au is clearly below the often touted 1g/t mark, yet the project is being developed by highly respected gold investors Anglogold Ashanti Ltd and B2Gold in a 50/50 JV.

Clearly grade is not a stumbling block for these two gold heavyweights.

By way of comparison, LCL’s total current Quinchia resource has a grade of 1.02g/t. The Tesorito 1.3Moz MRE is 0.81g/t, while LCL’s unconstrained Mineral Resource Estimate — capturing material beyond the current pit optimisation — generates an Inferred Resource of 1.7Moz at 0.71g/t, using a 0.45g/t cut-off grade.

In addition, much of the gold, and especially the high-grade gold zone, is quite shallow - which will help the project economics when it comes to the potential profitability of an operation.

This points to potential for large project development and Quinchia’s attractiveness to major partners or suitors.

How does LCL stack up against its ASX gold peers?

We have had about one and a half trading days since the announcement, so we expect that the markets have had time to assess the increase in LCL’s JORC resource.

Together with the Tesorito JORC resource, LCL’s total resource across its Quinchia portfolio is now 88mt grading 1.02g/t gold for a total of 2.6 million ounces of gold.

With a market cap of $70M, $17.8M in cash as at the 22nd February, LCL has an enterprise value (EV) of $52.2M.

This means, today, LCL sits at an EV/ounce of gold JORC resource sits at ~$20.

This is effectively a measure of how the market values a company's in-ground JORC Resource.

It provides investors a way to compare companies at similar stages (say explorers with other explorers) and discern value.

Mind you, other factors ought to be considered too, including the quality of management, the in-country risk, and whether the gold is near surface or deep underground.

In our last note on LCL, we mentioned the ASX listed Ramelius Resources takeover of Apollo Consolidated. In that deal, Ramelius valued Apollo’s 1.1M ounce JORC Resource at ~$148M. That gave the transaction an EV/gold resource ounce of ~$134 per ounce.

Hypothetically, if a company is spending $20 in exploration costs to discover an ounce of gold resource, it may be cheaper for them to simply acquire a company that is trading on a EV/Resource basis of just $10 per ounce.

Effectively, the lower this multiple is, the more attractive a company looks as a potential takeover target.

To put some context behind this we put together the table below, comparing LCL to other gold explorer’s with similar size deposits.

We also saw Sprott come out with a research note on LCL right after the JORC announcement - maintaining its BUY rating on LCL and lifting its previous A$0.36/sh target price to A$0.37.

At Sprott’s price target, LCL would have a $236M market cap (vs the current $70M MC) and an enterprise value of ~$218M. That translates to an EV/ounce of gold resource of ~$83 and puts LCL in line with its peers.

The full Sprott report can be found here.

Of course analyst predictions cannot be relied upon alone, they are based on a number of assumptions that may not happen. Always seek professional financial advice and make your own investment decisions.

What we want to see next

Now that Objective #1 from our 2022 LCL Investment Memo has been met, let’s check how the company is progressing on our other objectives.

[READ THE INVESTMENT MEMO HERE]

Objective #2: Test if LCL’s two gold systems are connected by drilling in-between them

One of the reasons that we continue to hold LCL into 2022 is the potential that its two discovered gold systems are connected.

Late last year, geophysical surveys confirmed a huge, deep, metallic anomaly (that we affectionately labelled “Jabba the blob” for its size and now known as “the Central Target”) between LCL’s two most advanced prospects (Tesorito and Miraflores).

LCL has started drilling Jabba to determine if it hosts a deeper, possible source porphyry deposit that links other known prospects and could indicate a much larger goldfield. This first hole was the first serious hole drilled by the company of greater than 1 kilometre depth.

LCL have now reported that drilling was terminated at 1,205m downhole due to the rig reaching its depth capability.

We asked LCL Managing Director Jason Stirbinskis if he could give us any insight around what to expect but he was very tight lipped, suggesting we wait for assay results next month.

That’s a bit later than was expected but with the drill bit encountering hard rock at surface that slowed progress and Christmas getting in the way, results have been pushed back some.

But surely news that a second drill hole has commenced at that same site has got to be a good sign.

Objective #3: Commence Scoping Studies

We had anticipated LCL to commence Scoping Studies following the just released Resource estimate. However, it appears that LCL is already well on its way to compiling a Quinchia-wide Preliminary Economic Assessment (PEA).

LCL will commission a PEA of Quinchia incorporating Tesorito, Miraflores and Dosquebradas resources, once the first round of Tesorito metallurgical testwork is complete.

A PEA is essentially a more stringent or more detailed version of a Scoping Study - spelling out the business case and potential profitability of the project.

Overseen by Ausenco Ltd, a metallurgical testwork program is now underway with sample selection already begun. This will lead into the PEA that we expect to be completed in an estimated 4-6 months.

Objective #4: Get some big gold funds on the register

While LCL is yet to grab the attention of the local market in any real way, it hasn’t gone unnoticed abroad.

Last year’s share placement saw the addition of two high profile North American gold funds including Franklin Templeton’s resource fund, one of the top resources-centric funds globally.

Institutions now comprise ~10% of the LCL register.

The $10BN multinational gold major Anglogold Ashanti is also a shareholder.

The team here heard Anglogold CEO Alberto Calderon present to the Melbourne Mining Club yesterday, who (maybe unsurprisingly) had a very upbeat take on the future for gold miners, praising in particular their ESG benefits (who would have thought).

Even so, and considering the potential scope of LCL’s Colombian assets, we would like to see a strategic raise to bring in a couple more major gold funds, preferable at a much higher share price than current levels. Bringing on more major gold funds (or increased investment from the two gold funds already on the cap table) will help underpin the valuation.

Deep dive on the Tesorito JORC Resource

Now the natural first question after reading the Resource announcement is:

What is an optimised pit shell?

This is reference to an exercise that all exploration companies do after discovering and delineating a JORC resource. Click here to read more about the stages of delineating a JORC resource).

A junior explorer will finish enough drilling to the point they are satisfied that no large mineralised parts of a project have been missed. That drilling data is then fed into resource estimation software that builds a 3D model of a Resource.

Knowing where all of the gold mineralisation is, the software runs 1000s of pit shapes options considering all variables including the gold price, cost of labour, etc then spits out the most profitable way of mining that deposit. So, basically, the optimised pit shell is just another term for referring to the most economic way to mine a deposit.

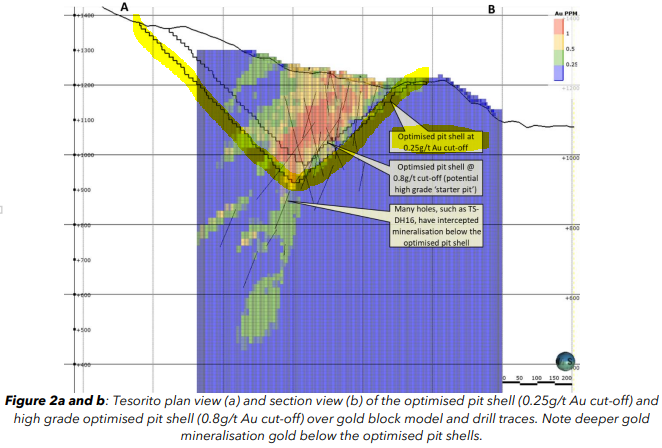

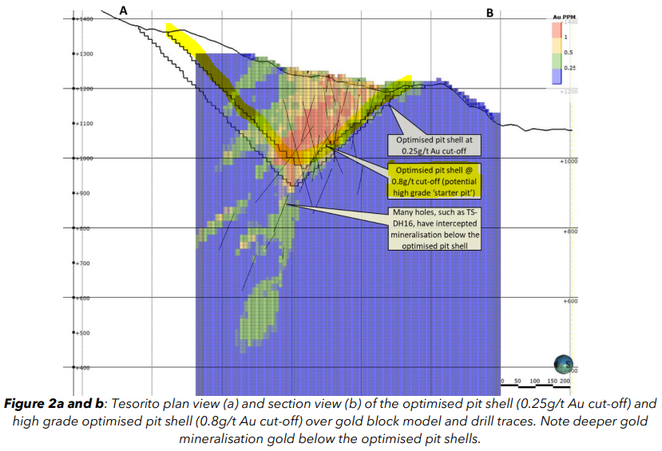

Below is the highlighted image of that optimised pit shell.

The significance of all of this is that the cut-off grade used is 0.25g/t where the JORC Resource becomes ~2.3M ounces of gold, and this was all modelled using a gold price of US$1,800/ounce.

The gold price is currently trading well above that at US$1,937/ounce.

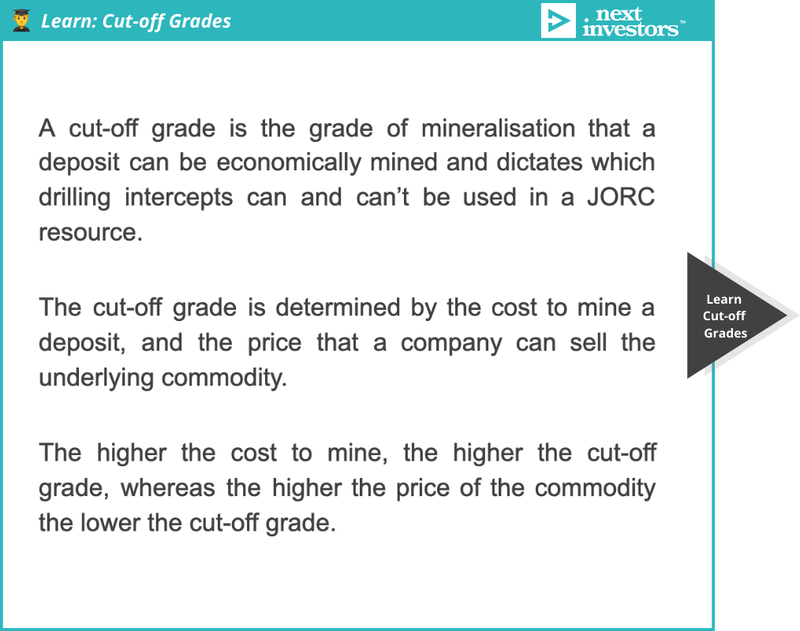

All of this flows directly to the next question: what is a cut-off grade and why does it matter?

🎓 Educational Content

Before reading on, you can check out our educational note which details what a cut-off grade is and how they are determined.

A cut-off grade is a set parameter in the resource estimation process. It determines the grade of mineralisation that a deposit can be economically mined and dictates which drilling intercepts can be used in a JORC resource.

In the case of LCL’s optimised pit shell, the JORC Resource is approximately 1,100m length, 675m width and a depth of 375m, making it amenable to low cost open pit mining.

Plugging in the following high level assumptions including a US$1,800 per ounce gold price LCL’s software has put together an optimised pit shell. This is based on a 0.25g/t cut-off which seems to be the lowest possible grade for an economic mine (at US$1,800/ounce).

Given the Tesorito deposit is just one part of the larger Quinchia portfolio of gold deposits, should LCL manage to increase the size of the overall global resource across all of its deposits we suspect the lower grades will become more profitable as economies of scale take hold.

With the optimised pit shell indicating a potentially profitable 2.3M ounce operation at a head grade of 0.53g/t gold LCL is proving out the potential for a long mine life gold project.

LCL’s project gives the company optionality to operate a larger and longer life of mine project with lower grades profitably in a high gold price environment.

Paths to development

LCL says that Tesorito has “all the hallmarks of a major discovery” and with the Quinchia Project now demonstrating significant scale, it has a number of options in seeing the project through to development.

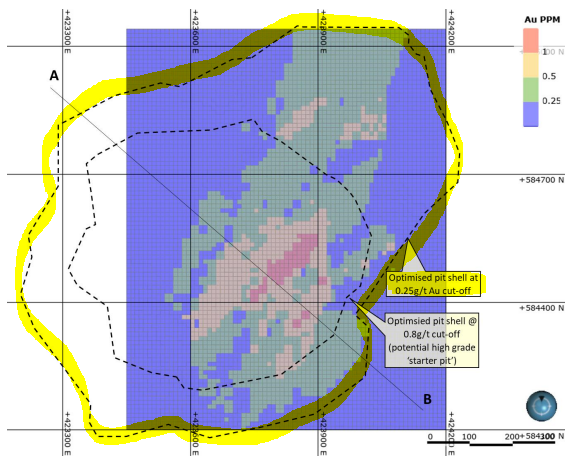

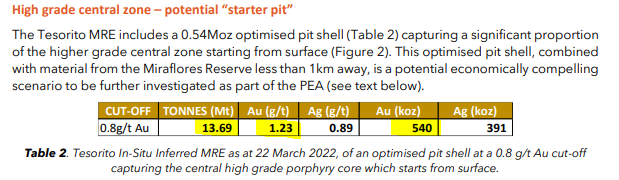

It highlighted the potential for a higher grade, starter pit based on a 0.8g/t cut-off grade.

This gives LCL optionality if there is volatility in the gold price. If the gold price stays high or even trades higher, we suspect that LCL would want to establish an even larger project that is focused less on grades.

As will be investigated in the preliminary economic assessment (PEA), there are benefits of starting out small with a potential “starter pit” are:

- A junior can afford to build it alone

- Higher grade so there’s a killing to be made on margins

- Can be achieved in a short time frame

Having this higher grade optimised pit shell gives LCL the option to put its project into production early, via this higher grade section. This would see a fast payback for the initial CAPEX spent to develop the project.

After this, LCL can still transition to a longer term development project by bringing in the rest of the Tesorito JORC Resource and processing the lower grade materials.

With a resource of ~540k ounce gold, this would just mean that the cash flows are weighted to the beginning of mining when LCL will need it most.

This potentially high margin but low scale plant could help fund the construction of the big plant, of which Gramalote is a fair comparison.

With greater scale, contributions from the larger pit configurations capturing the significant volumes of lower grade material in the Tesorito resource could be considered.

Below is an image of the higher grade pit (using a 0.8g/t cut-off grade) sitting inside the larger pit (0.25g/t cut-off).

We think that the market is missing this optionality which gives LCL’s project resilience , no matter the gold price, and weights cash flows so that the project payback is quicker.

CAPEX payback is often the biggest hurdle when a gold explorer goes to secure development financing which makes all of this that much more important.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.