TTM’s 3.1Moz gold 22Moz silver project: Chinese strategic investment of US $10M and 90 day exclusivity to get a deal done.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,161,943 TTM Shares. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The gold price just isn’t stopping.

Gold hit new all-time highs today of US ~$4,380 per ounce.

Titan Minerals (ASX:TTM) has a 3.1 million ounce gold resource

(plus 22M ounces of silver which also hit all time highs today US $54.6 per ounce )

TTM also has a copper project where Gina Rinehart’s Hanrine is earning in up to a 80% stake in the project in exchange for US$2M cash plus US$120M in exploration spend.

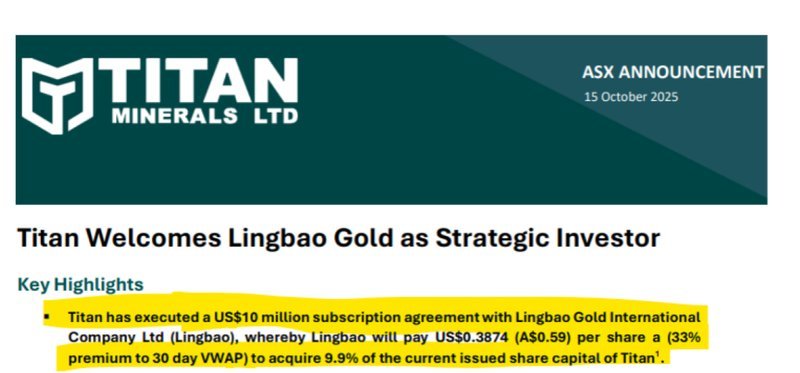

Earlier in the week received a US$10M strategic investment from US$3.5BN Lingbao Gold International Company...

Lingbao came in for a 9.9% equity stake in TTM in exchange for US$10m.

Including a 90 day “exclusivity period” to negotiate on TTM’s gold and silver asset (and a right of first refusal on the earlier stage projects too)...

(Source)

TTM’s assets are in Ecuador, a region that has recently seen a lot of deal making activity:

(especially by the Chinese, who love a bit of gold and critical metals like copper)

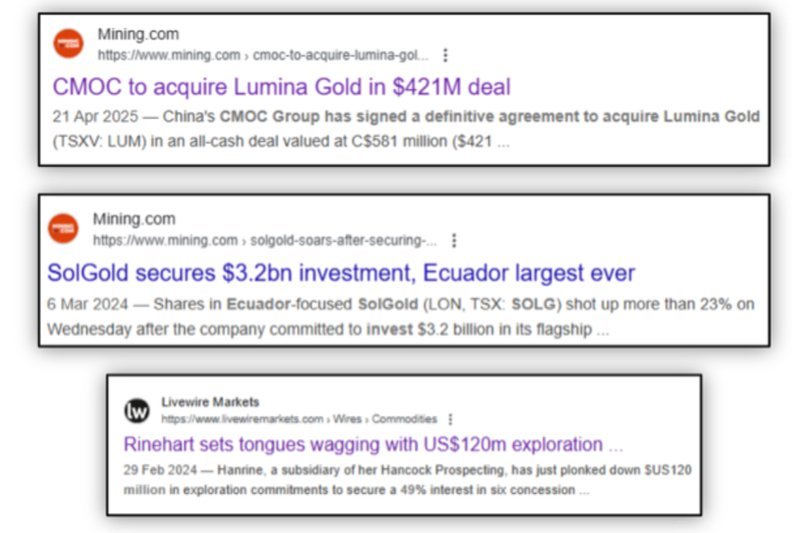

- In June Hong Kong listed CMOC bought Lumina Gold for US$421M, and (source)

- Earlier in the year Hong Kong listed JiangXi Copper upped their stake in SolGold at a premium to the market price at the time and SolGold’s share price has re-rated by over 300% since then. (source)

A lot has changed since both those deals got done... gold prices are up by over 30% and the silver price by more than 50%.

(Source)

So activity appears to be increasing and now with gold and silver prices rallying maybe urgency is too?

TTM has four assets in southern Ecuador including:

- The Dynasty Gold Project which is TTM’s most advanced asset and hosts 3.1M ounces of gold and 22M ounces of silver.

- The Linderos copper project, where Gina Rinehart’s Hancock is earning in up to a 80% stake in the project in exchange for US$2M cash plus US$120M in exploration spend. And

- Two earlier stage copper assets where we think TTM could do similar to the deal done with Gina.

TTM is actively drilling at Dynasty right now where a resource upgrade for the project was planned for late Q3, so shouldn’t be far away. (source)

At Linderos, the JV with Gina is also actively drilling. (source)

So it looks like Chinese money has its sights set on gold, silver and copper assets in Ecuador.

And TTM has a large scale gold and silver project AND a large scale copper project...

in Ecuador.

With gold and silver prices trading at all time highs it's no surprise TTM has managed to attract corporate interest in the company.

Especially with that advanced resource at the Dynasty project (3.1Moz of gold and 22Moz of silver).

Lingbao actually made specific mention of TTM’s Dynasty asset in the commentary section of that announcement earlier in the week:

(Source)

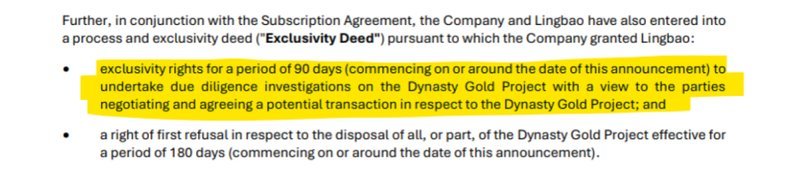

We also noticed on page 2 of the announcement that Lingbao and TTM signed an “Exclusivity Deed” which would give Lingbao exclusivity rights for 90 days to get an outright deal done on Dynasty alone...

Clearly Lingbao really like that project and while gold and silver are running hard want to be the only ones who are able to negotiate with TTM directly on a potential deal (for 90 days):

(Source)

(they also got that right of first refusal clause in for 180 days - meaning they can match or beat any competing offers too)

We are not lawyers, but we have seen these exclusivity deeds get done on different assets several times over the last couple of decades.

These deeds are ways for interested parties to be the sole negotiators on an asset while they do their due diligence on the project.

Basically, they sit down with TTM over the next 90 days and try to agree a deal on that single asset.

IF a deal isn't done and someone else comes in and puts an offer in they have a “right of first refusal” to beat or match whatever is offered to TTM for the next 180 days.

Interestingly, they also put in place a similar arrangement for TTM’s two other earlier stage copper assets:

(Source)

So inside the next 90-180 days, we COULD see more corporate news from TTM... just as M&A activity in Ecuador is becoming more and more common.

(ofcourse there is no guarantee of this, M&A deals can always drag out much longer than anyone expects and nothing is a guarantee)

M&A activity in Ecuador has been heating up...

Earlier in the year Hong Kong listed Jiangxi copper put cash into SolGold at a premium to the market price at the time. SolGold’s share price has almost doubled since that deal was done.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Over the last ~12 months we have seen:

- China’s CMOC acquired Lumina in a deal worth US$421M.

- SolGold signed a US$3.2BN deal with the Ecuador government for its Cascabel copper-gold project.

- A Gina Rinehart backed subsidiary of Hancock Prospecting invested US$120 million for a 49% stake in six different projects, partnering with Ecuador’s national mining company, ENAMI (51%) and did the US$120M deal with TTM.

That Lumina deal was particularly interesting to us.

Lumina is a single asset company with a giant copper-gold porphyry project (one of the top 30 biggest in the world).

It is the type of project that Gina Rinehart would likely have been looking for when her subsidiary group Hanrine signed that US$120M Joint Venture deal with TTM.

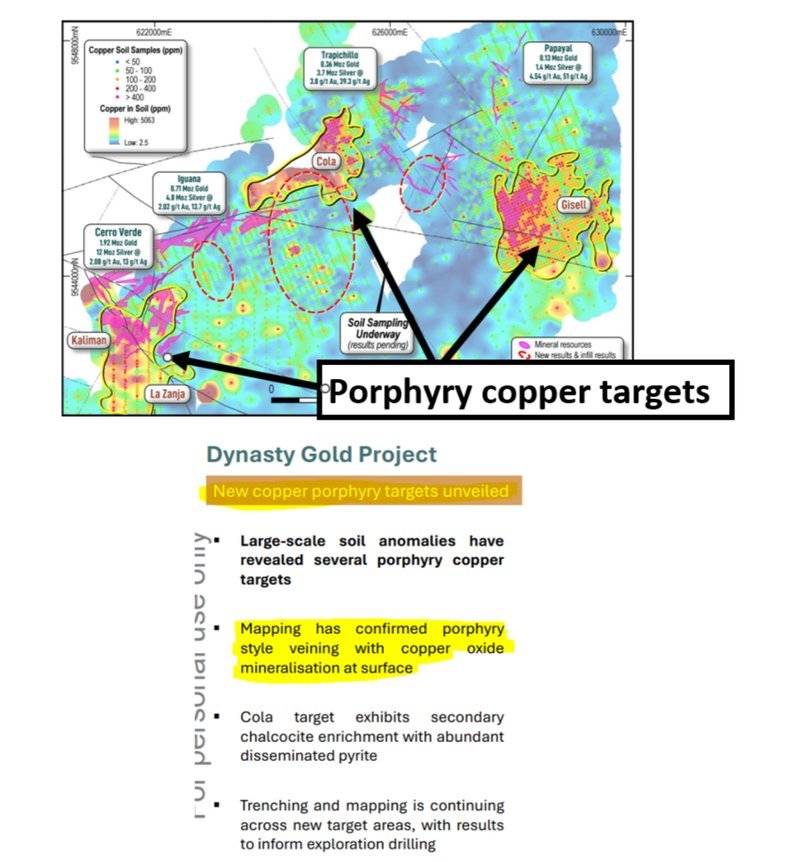

It could also be the type of asset that Dynasty could become if the porphyry exploration upside of the project comes in when TTM eventually drill those deeper targets.

TTM only started talking about the porphyry potential of Dynasty in presentations earlier this year. (Source)

Most of the drilling to date on TTM’s Dynasty asset has been shallow high grade gold and silver (down to 200m depths) - with 82% of the current resource estimate above 200m depths.(Source)

So far no drilling has been done at depth to test for the source of the high grade silver and gold near surface...

(Source)

Earlier in the year TTM ran ~920-line km geophysical survey across ~9km of strike to see if geophysics work can validate that theory.

Results from that geophysical survey could come any day now - they were due during the september quarter:

(Source)

So we could soon see if there is a big blue sky porphyry exploration target on Dynasty which is already a big gold-silver project as it sits right now.

We think that untapped exploration upside could be a really nice carrot that gets dangled infront of potential acquirers of the asset (in this case Lingbao who have exclusivity on the project for at least the next 90 days).

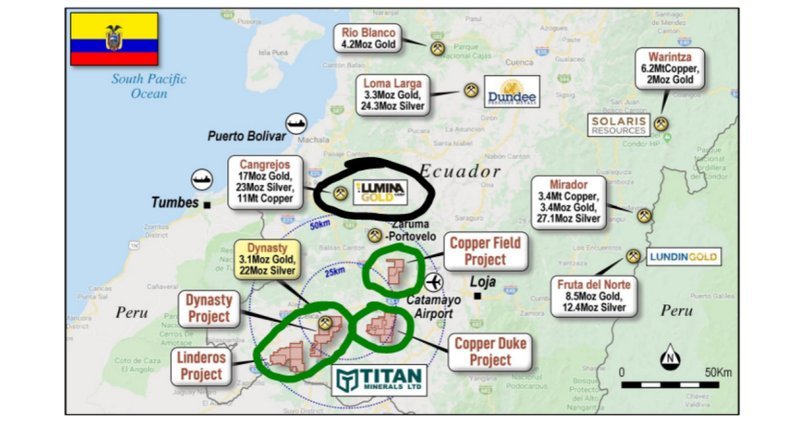

Here is where that Lumina asset sits relative to TTM’s portfolio of projects:

(Source)

Ecuador copper & gold in favour amongst the major miners...

One of the highest grade gold mines in the world is operating in Ecuador right now.

The project is owned by ~A$27BN capped Lundin Gold - it's actually their cornerstone asset.

Lundin was built off the back of Fruta Del Norte’s success - back in 2016, when the project was in the feasibility study stage Lundin’s share price was less than CAD$5 per share.

Since then, Lundin has raised billions of dollars, built its project and is producing almost half a million ounces of gold per annum.

Now Lundin Gold’s share price is ~CAD$101.97 per share and it has a market cap of ~A$27BN.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

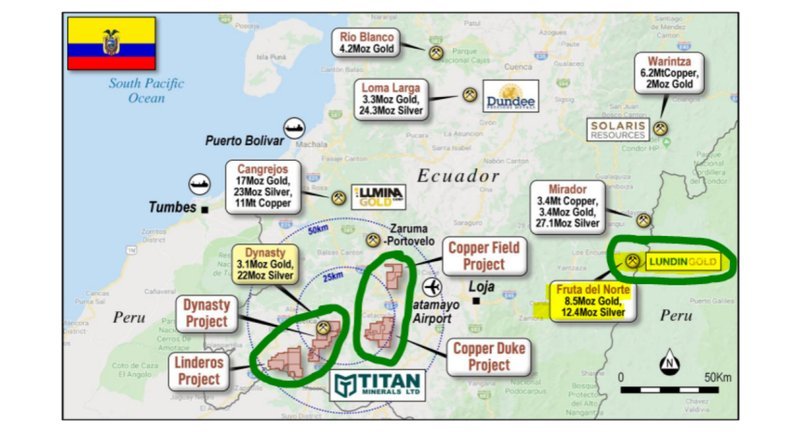

Here is where Lundin's Fruta Del Norte sits relative to TTM’s assets:

(Source)

More recently, Ecuador has also started attracting interest from major miners for copper.

Last year SolGold signed a US$3.2BN deal with the Ecuador government for its Cascabel copper-gold project.

That SolGold deal was the biggest ever mining investment commitment in Ecuador’s history AND it was completely separate to the ~US$311M SolGold had committed to previously.

(Source)

Gina Rinehart, who controls one of the world’s biggest private mining groups (& TTM’s joint venture partner at Linderos) is also pushing itself into Ecuador.

Before the deal with TTM, Gina invested US$120 million for a 49% stake in six different projects, partnering with Ecuador’s national mining company, ENAMI (51%).

Overall, we think the moves by the bigger miners into Ecuador can only be good for the country.

Once they go in and work with the government to develop the industry, it makes juniors like TTM more attractive for the mid-tier miners AND for the majors looking to increase in-country presence.

What’s next for TTM?

More drilling at Dynasty gold project 🔄

TTM is currently at Dynasty with a view of upgrading the projects resource estimate.

We expect the company to this drilling over the coming months and set itself up for a resource upgrade.

Resource upgrade/update at Dynasty 🔲

TTM is working towards a resource upgrade on its project. A presentation from earlier in the year set a +5M ounce gold target for its Dynasty asset:

(Source)

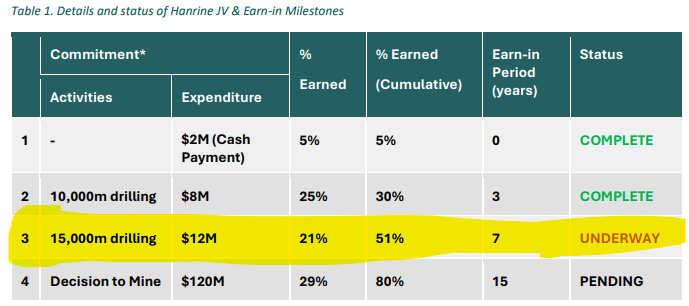

More drilling at the Linderos Copper project (Gina JV) 🔄

The JV with Gina recently completed the second stage of the earn-in agreement AND kicked off exploration under the third phase of the deal:

We are looking forward to results from this stage of works:

(Source)

What are the risks?

With TTM actively drilling right now, and with the exclusivity deed signed with Lingbao the two keys risks in the short term to TTM’s share price are “Exploration Risk” and “Deal Risk”.

If TTM is unable to discover more gold over its Dynasty project and publishes a resource upgrade lower than market expectations, it could have a negative impact on the share price.

Poor drill results from the Hanrine JV could also be negative for TTM’s share price, especially if Hanrine chooses not to proceed with the remainder of the JV earn-in stages.

TTM also kicked off geophysical surveys on its projects. there is always a chance those surveys find nothing of interest which would again be below market expectations and could impact TTM’s share price negatively.

Exploration / Drilling risk

There is no guarantee that TTM’s extensional drilling programs will be successful and TTM may fail to uncover enough economic mineralisation to justify the expense.

Source: “What could go wrong” - TTM Investment Memo 29 May 2024

There is also an element of deal risk now given the exclusivity deed signed with Lingbao.

IF the market starts re-rating TTM higher expecting a new deal to get done on the companies assets there could be an expectation in the market for M&A.

M&A deals can take a lot longer than anyone expects and there is never any guarantee that discussions conclude in a binding deal.

IF no deals are done inside the next 90-180 days and TTM’s share price runs expecting a deal to get done, the TTM share price could re-rate lower as expectations unwind.

Other risks

Like any stock market investment, investing in TTM carries a range of risks which may affect the value of the company, some of which cannot be predicted (this is the nature of risks). Here we aim to identify a few more risks.

TTM’s Dynasty Gold Project and Linderos Copper Project are pre-development and exploration-stage assets. There is a risk that the projects do not progress as planned, that resource upgrades do not meet market expectations, or that development takes longer and costs more than anticipated.

TTM’s share price is highly leveraged to the price of gold, silver, and copper. Sustained declines in any of these commodity prices could materially impact project economics, investor sentiment, and the company’s market valuation.

While the strategic investment from Lingbao provides funding and exclusivity for the Dynasty project, there is no guarantee that this will result in a final transaction or that the terms will be favourable. Market expectations around M&A could result in share price volatility if deals do not materialise. Additionally, ongoing M&A activity in Ecuador may create competition for TTM’s assets, potentially impacting valuations or deal terms.

Exploration results are inherently uncertain. Drilling or geophysical surveys may not yield significant or economic mineralisation, which could negatively impact the company’s growth prospects and share price.

TTM’s projects are located in Ecuador, which, while increasingly attractive for mining, may still carry jurisdictional, regulatory, and permitting risks. Local environmental approvals, changes in legislation, or political instability could delay or impact operations.

The company remains reliant on the capital markets and strategic partners to fund exploration and development. Any future equity or debt funding may dilute existing shareholders or be subject to less favourable terms.

Finally, TTM’s valuation could already reflect some of the anticipated upside from gold, silver, and copper price strength, as well as potential corporate transactions. Expectations may not be realised, and investors should consider the possibility of share price volatility.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our TTM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our TTM Investment Memo where you will find:

- What does TTM do?

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.