Tiny CND just declared a new multi-billion barrel prospective oil resource - farm-in to drill next

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 33,040,455 CND Shares and 11,925,000 CND Options and the company’s staff own 1,538,462 CND Shares at the time of publishing this article. The Company has been engaged by CND to share our commentary on the progress of our Investment in CND over time.

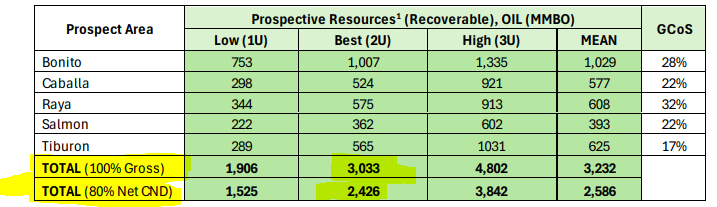

3 billion barrels of oil...

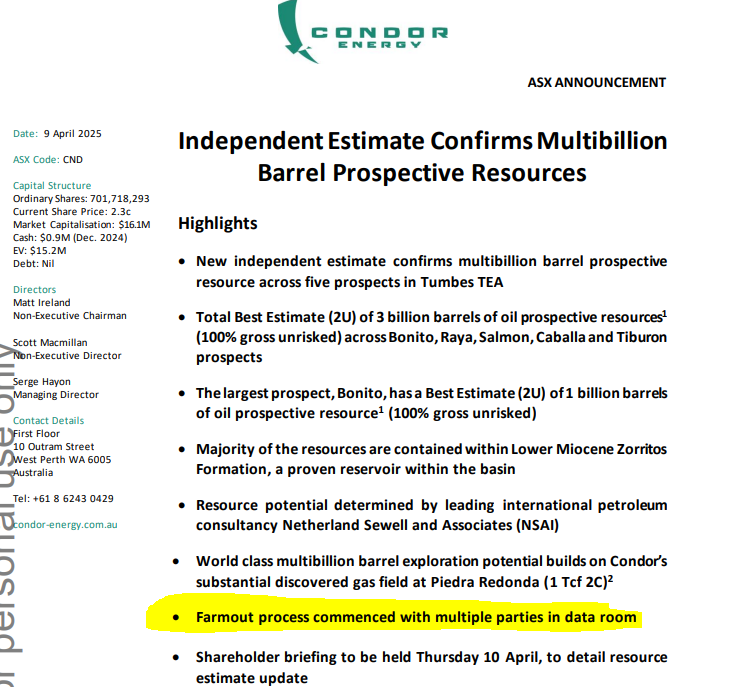

That's the size of Condor Energy (ASX:CND)’s unrisked prospective oil resource across five prospects that was released today.

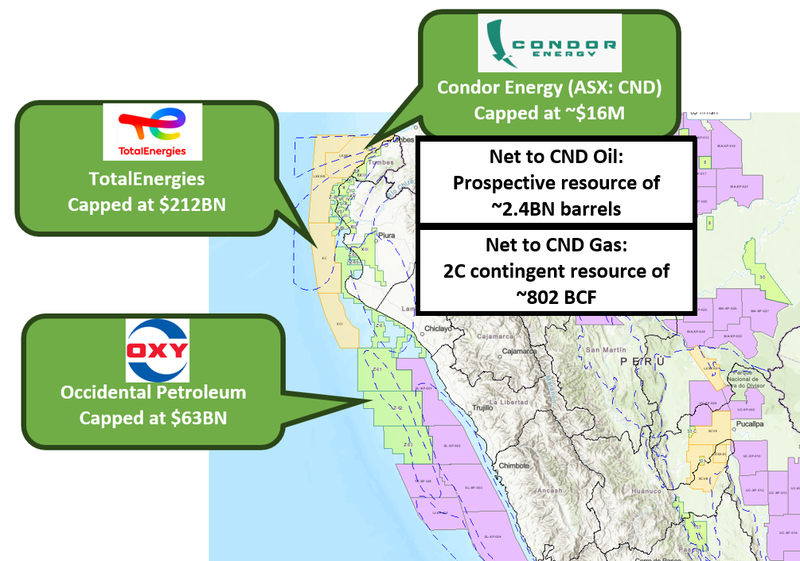

CND was capped at $16M prior to today’s news.

Is this now one of the biggest sets of offshore oil exploration prospects on the ASX?

In one of the smallest capped explorers?

We think it might be...

That “small” market cap might not be the case for long.

We think that establishing such a large, multi-billion barrel prospective resource should re-rate the stock upwards as the market prices it in.

Especially if a farm-in to drill is announced...

(Today CND said “Farmout process commenced with multiple parties in data room” - more on this later.)

Today’s oil prospects are in addition to CND’s 1 TCF discovered gas field (100% basis, contingent resource)...

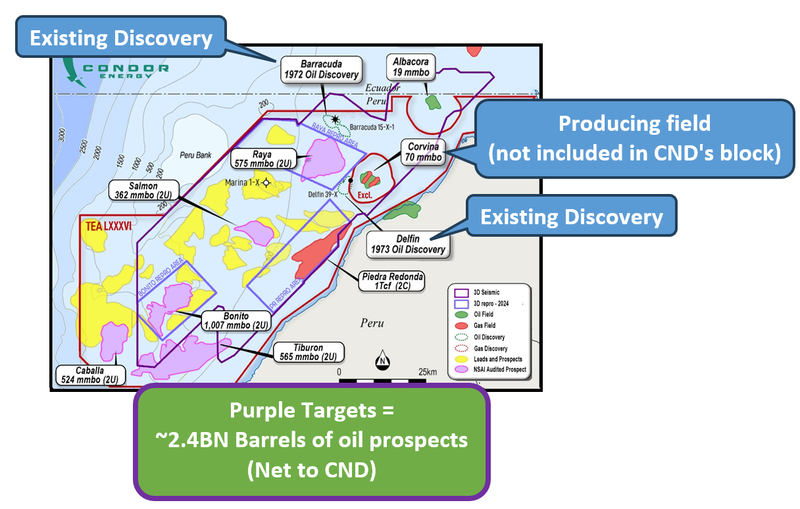

CND holds 80% of the block which means ~2.4BN of that prospective oil resource is net to CND.

The bigger goal for CND is to drill test the multi-billion barrel prospective resource to see if an oil discovery can be made.

A successful discovery with commercial flowrates should re-rate the stock many multiples of where it is today on success (which is not a guarantee - oil exploration is risky).

It all sets CND up for what could prove to be one of the most highly anticipated drilling events the ASX has seen in years.

But it's probably going to need a deeper pocketed partner to fund that drilling.

According to today’s announcement, multiple parties are in the CND dataroom, and a farm out process has commenced...

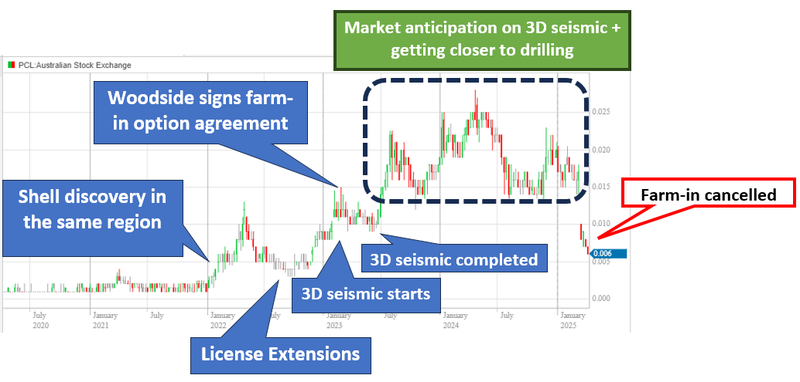

A farm-in with Woodside is what triggered another ASX listed offshore oil explorer’s (Pancontinental) share price run from ~$7M to ~$230M market cap.

(CND’s net prospective oil resources are ~2x the size of Pancontinental’s, more on this later)

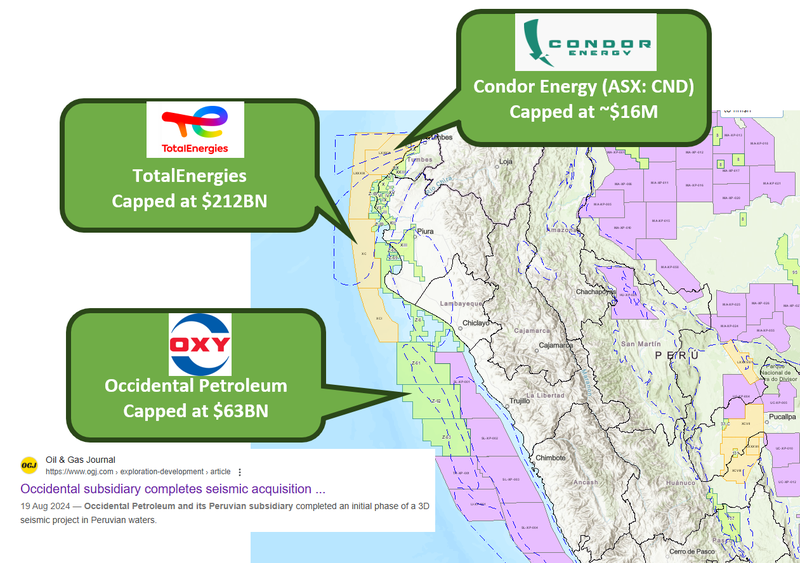

CND isn't alone in exploring this part of the world.

$212BN Total Energies - the French energy supermajor, almost completely surrounds CND’s acreage.

The $63BN Occidental Petroleum is hunting new discoveries nearby as well...

Occidental’s major shareholder is Berkshire Hathaway - who is led by Warren Buffet, one of the richest folks in the world.

Deep pockets indeed.

And now, in the same region, the $16M capped CND has multi billion barrel oil prospects to go with its existing 1 trillion cubic feet gas discovery...

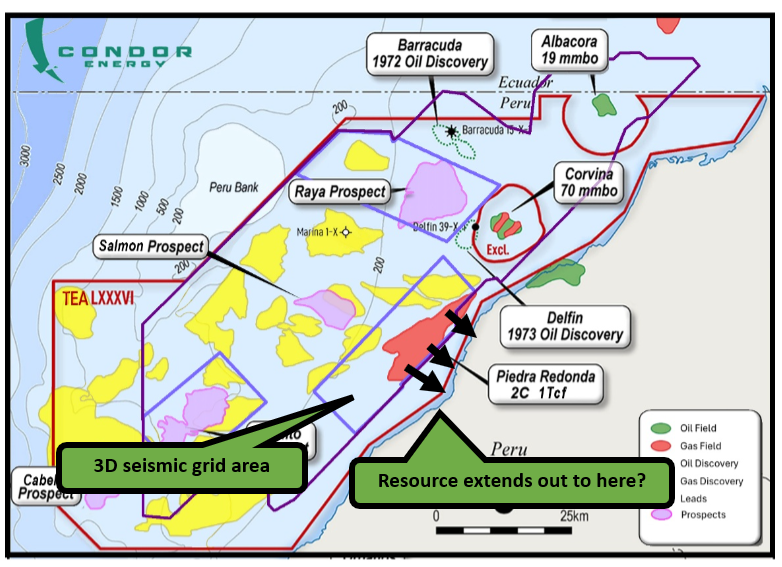

CND’s block sits in the middle of a PROVEN hydrocarbon system.

There is the Barracuda oil discovery that was made in 1972 and the Delfin oil discovery made in 1973 (both of which sit inside CND’s acreage)...

AND there is the Corvina Field (excluded from CND’s block) which is currently producing oil.

CND’s most recent reports suggested it was producing ~3,000 barrels of oil per day...

The two wider basins that CND’s block sits within have produced ~1.7BN Barrels of oil historically.

So CND’s acreage is in a part of the world where discoveries have been made and projects have been brought into production...

AND where there is still a lot of unfinished business on the exploration front.

This is why we think the likes of $212BN Total and $63BN Occidental have entered the region...

(Notably, they acquired their blocks months AFTER CND - we really like small cap first movers in emerging provinces...)

CND Managing Director Serge Hayon will be running a technical briefing tomorrow at 11:00 AM AEST (9:00 AM Perth time).

Register for the webinar here

In today’s note, we will cover:

- How CND stacks up versus another popular offshore oil explorer...

- How we think the oil prospective resources could get bigger

- Why CND’s size works in it’s favour when it comes time to negotiate a deal...

- How CND’s block could attract a farm in partner

- How far away CND is from a big drilling event

- Why we think CND is at an inflection point for it’s market cap

- AND we do a bit of a deep dive on CND’s existing 1 TCF gas discovery...

As mentioned earlier, CND already has an existing gas discovery which is one of the largest undeveloped offshore gas discoveries on the west coast of South America.

(More on the gas asset later in today’s note)

After today’s announcement CND also has one of the largest net prospective resources of any small cap oil explorer...

It’s very hard to find targets that big in an ASX explorer...

It’s even harder to find it in one capped at <$20M which is where CND was trading prior to today’s news.

The reason we think CND’s targets are especially solid is because they are all based on 3D seismic data - the highest quality datasets available for any oil and gas explorer.

Typically small cap explorers are limited to 2D seismic because 3D can cost so much to acquire.

2D seismic data is less reliable and a lot more risky to drill from.

3D seismic is as good as it gets in terms of pre-drill data to de-risk a drill target when it comes to oil exploration.

The existing 3D seismic was a big part of the reason why we Invested in CND in the first place.

We also think CND’s prospective resources could grow from where they are now...

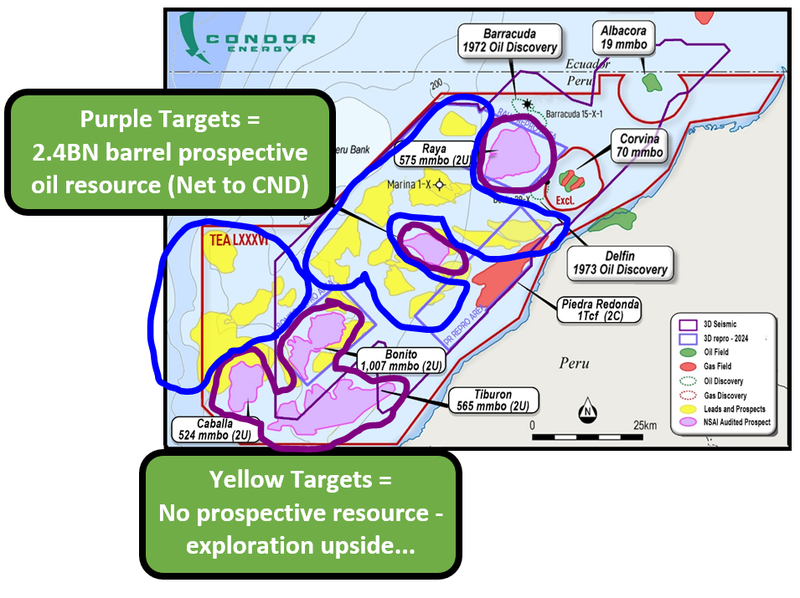

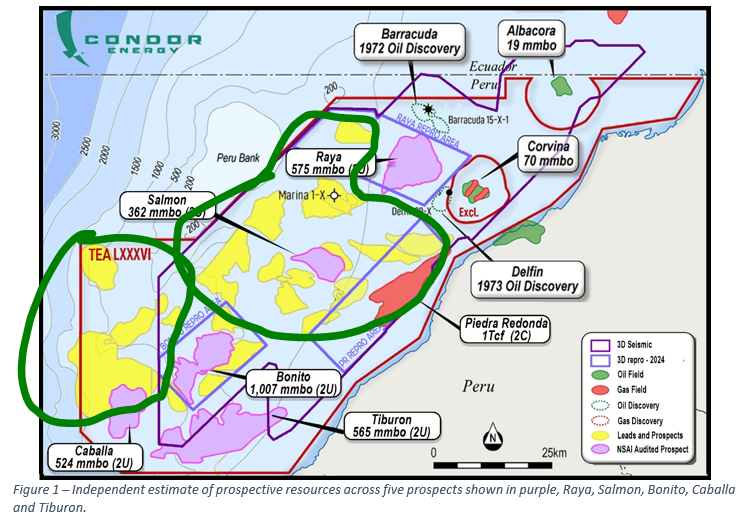

Today’s resource is based on the purple blobs alone...

The yellow leads are all potential targets too... at this stage, they haven’t been mapped enough to come into the prospective resource number published today.

As we can see those are still pretty big targets that could at some stage add to today’s numbers:

How CND stacks up versus another offshore ASX oil explorer

The ASX tends to rate offshore oil and gas explorers, just as long as they can show their targets are big enough to warrant drilling.

One example is Pancontinental Energy - a popular offshore oil & gas exploration name on the ASX.

Only ~12 months ago was capped at ~$230M off prospects mapped on 2D seismic data alone.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

After spending over US$35M on new seismic data, they announced prospective resources (2U) of ~1.2BN barrels on a net basis only a few weeks ago.

(They also have an oil in place estimate, but we are comparing the exploration prospects alone here).

Remember, CND has a net prospective resource of ~2.4 billion barrels.

Pancontinental had its joint venture partner (Woodside) pull out of a farm-in agreement at the same time as that resource news, which sent the share price down - but still it is capped at ~$57M today...

CND with roughly twice Pancontinental’s prospective resource number is capped at $16M...

(again... this is without even factoring in the 1 TCF gas asset...)

We think that as CND gets closer to an eventual drilling event, that valuation gap could close (and hopefully flip in CND’s favour).

Pancontinentals rally to ~$230M was off the back of a farm-out announcement with Woodside.

A farm out deal is one of the catalysts we think could trigger a similar run in CND’s market cap. (more on that later)

CND says farmout discussions are underway with “multiple parties in the data room”.

It all sets CND up for what could prove to be one of the most highly anticipated drilling events the ASX has seen in years.

And we like the fact that Peru could be one of the last remaining frontiers for major oil and gas discoveries in the world.

It’s the kind of frontier that has already attracted energy super major $212Bn Total Energies and $63Bn Occidental Petroleum to the region.

Total now holds all of the ground surrounding CND’s block and Occidental are running 3D seismic surveys offshore in the south:

We are biased... but we think CND holds the best ground here.

CND’s project is closest to the Peru shoreline and is right near the Ecuador border.

Shallower water means less costly drilling as well as faster and cheaper ways to bring any new discoveries online.

This is just one of the reasons why we like CND.

Prospective oil resources could get even bigger...

One thing we noticed in today’s announcement was that the prospective resource doesn't actually cover every single target inside CND’s block.

Notice the prospective resource is based on the five purple sections of the overall project area.

Whereas the yellow blobs are additional leads/prospects that haven’t been mapped to the point of a prospective resource being able to be announced:

What that tells us is that the prospectivity inside CND’s block could be multiples the size of today’s prospective resource.

Which is already massive...

Basically, if CND finds something it could be the opening discovery to unlock the rest of these prospects.

And we think that has big implications for the value of a block like this...

Why?

Because exploration upside is exactly what majors look for when they do big M&A deals.

Majors are often looking for projects that “move the dial” for them.

If they are capped at $50-100BN a single discovery which is capped in its upside doesn't really move the needle.

Majors want to have certainty that IF they enter a region and spend $50-100-200M on drilling, and sometimes billions on development.

They can leverage all of that spend and make multiple other major discoveries that can tie into all that infrastructure.

This inherent exploration upside (even though there is no guarantee it pays off) also means they are happy to pay larger dollar values upfront to get their foot on projects...

They then come in with much bigger balance sheets, get a big rig into the basin and keep it there for a few years so they can go and drill out prospect after prospect.

In CND’s case, there are already five independent prospects, all of which are >350M barrel 2U targets and one with over 1BN barrels alone...

(Source)

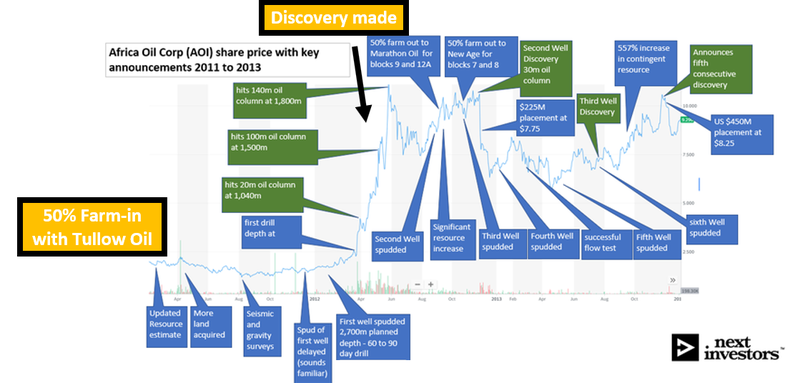

We saw this type of deal happen way back in 2011 with Africa Oil.

Africa Oil attracted Tullow as a partner then re-rated 10x off a discovery

Long time readers will remember Africa Oil was the first big oil and gas discovery we were Invested in.

Africa Oil brought in Tullow Oil as a partner back in September 2010.

A few months later Tullow and Africa Oil drilled in Kenya and made a discovery that led to a ~1,000%+ move higher in Africa Oil’s share price.

Off the back of that Africa Oil raised hundreds of millions of dollars...

The JV kept that rig in that basin for years and drilled target after target.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Ultimately, we think CND’s ground has serious size/scale which makes it a lot more attractive from a longer term perspective for someone wanting to come into a block that has many multiples upside on what is known right now.

CND in active farm-out discussions already

CND mentioned in today’s announcement that farm-out process had commenced and that “multiple parties” were in the company’s data room:

(Source)

As mentioned earlier, a farm-out or some sort of financing deal for a well is what could get CND’s share price moving.

A farmout deal provides external value of a project.

What the market is willing to pay for a speculative small cap stock is very different to what a major oil & gas company would pay for prospective ground.

As mentioned earlier, It was the Woodside deal with Pancontinental back in 2023 that started the rally to a market cap of ~$230M.

And while CND is capped at ~$16M, we think off the back of a deal alone CND’s market cap could multiply.

But CND could secure a deal that is more than just funding for a well...

This is where CND’s existing gas discovery comes into play.

CND could also do a deal on its gas asset.

The best way to think about the farm-out process is that, CND, by having both oil and gas has a much larger target audience at the top of the funnel.

Companies that are interested in high risk/high reward exploration AND companies that are looking for nearer term, lower risk development assets.

AND of course companies that are interested in oil and others that might be more interested in gas.

CND is in a strong position with both oil, gas, exploration and development stage assets that could be dealt out...

What would success look like from a deal perspective?

It’s hard to predict with so many different possibilities, but we think any of the following could be a big catalyst for CND’s share price:

- CND deals out its gas asset - maybe some of the proceeds that come from this can go toward drilling an exploration well? Maybe CND gets a free carried interest in an asset that could generate revenues in a reasonable timeframe?

- CND deals out oil exploration assets - CND gets a free carried interest in a well that would be fully funded by a farm-in partner. Means less dilution going into a big drilling event for existing shareholders...

- Maybe a combination of the two? - CND could bring someone in that is interested in both...

We have already seen $212BN Total Energies snap up ground around CND.

AND now $63BN Occidental is running 3D seismic surveys on blocks to the south...

So there is definitely interest in offshore Peru from the major players...

(Source)

There is also precedent for big deals on blocks in Peru too..

Back in 2009 KNOC (South Korean National Oil Corporation) and Ecopetrol (Colombian National Oil Company) signed a deal worth US$900M for projects to the south of CND’s block.

(Source)

What we like the most about CND’s position now is that they were first movers back into offshore Peru (picking up this block before Total’s entry).

AND the optionality from the gas/oil front.

With the current market cap hovering around ~$16M we think the risk/reward for CND is pretty good from these levels...

CND is getting closer to a big drilling event...

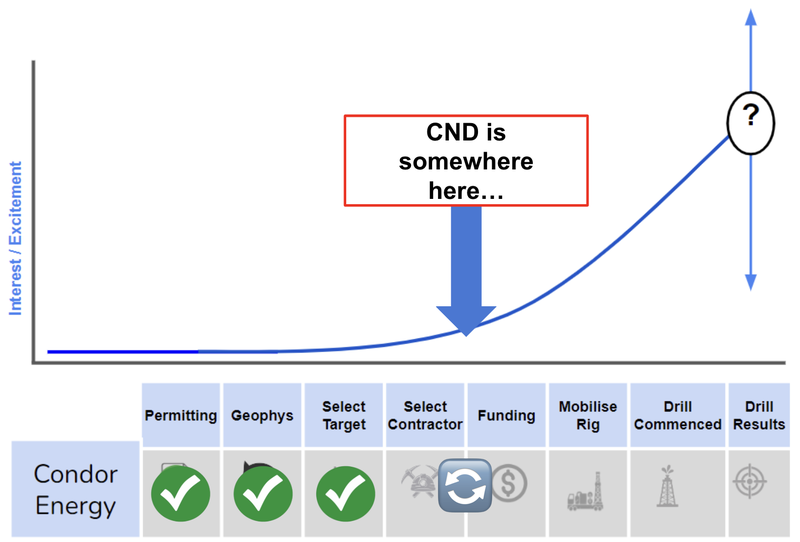

Usually, with oil and gas explorers, the valuations the market is willing to give a company depend on how far away a company is from drilling its targets and commercialising its project.

There are certain steps the explorers need to take, and as they are incrementally de-risked, the market will attribute a risk-adjusted valuation relative to the size of the prospective resources.

We think the market isn't pricing in CND’s existing gas discovery and ~2.4BN barrels of undrilled oil prospects at it’s current $16M market cap.

Here is everything we already know about CND:

- CND is operating in a proven hydrocarbon basin - CND’s block surrounds the Corvina oil discovery which is a shallow water PRODUCING oil field... So the geology that CND’s ground sits on works...

- CND has existing 2D and 3D seismic data - so CND’s prospective resources are based on a high quality dataset. To get all of this data from scratch could cost $50-100M in today’s money.

- CND already has an existing 1 TCF gas discovery - the existing discovery, being in shallow water, close to the Peru shoreline means the pathway to getting it developed and into the market is a lot quicker than other offshore discoveries.

- CND now has big blue sky exploration upside - this is where the big step-change to valuations can come from. Markets need numbers to try and quantify the potential reward that could come from drilling a target. The bigger the targets, the bigger the valuation pre-drilling.

CND is now approaching that re-rate inflection point

For those who have been following our Investments for a while with oil and gas explorers we tend to follow a five step investment plan.

Of course, before we show you our plan, we need to stress that there’s never a guarantee of success with speculative oil and gas investing.

We recommend consulting with a professional financial advisor before choosing to invest in small cap stocks like CND.

Our general plan is to Invest early, and eventually, as a drilling event draws closer over the coming years we expect to see broader investor interest increase, and with that, growth in the company’s valuation.

Our plan is usually to:

- Invest early, as the company is in the early exploration work stage.

- Increase our Investment, as the company de-risks the project through permitting, geophysics and target generation.

- Top Slice, if the share price runs in anticipation of exploration results

- Free Carry, into results while still maintaining a large position to be leveraged for a discovery

- Evaluate our position post-drilling.

Going into its maiden drill campaign one of our other oil & gas investments Invicitus Energy (ASX:IVZ) hit a peak market cap of $400M+.

(Scott MacMillan is the CEO of IVZ and chairman of CND)

Another company in our portfolio 88 Energy (ASX: 88E) hit a market cap of $1B+ when it approached its oil & gas drill campaign in the US.

The market is a little bit different to when those wells were drilled, but we still think that interest in the CND story should grow as it gets closer to a drill campaign.

Our broader thinking is that as an oil and gas explorer gets closer to a major catalyst like a drilling event, investor interest increases in the stock and the company’s valuation starts to move higher as expectations get baked into its share price.

One of the main reasons we announced CND as our 2023 Energy Pick Of The Year was because of where the company sat relative to our tried and tested Oil and Gas Investment Strategy.

We made CND our 2023 Pick Of The Year at 1.9c per share - at the time CND’s market cap was ~$7M.

Now ~24 months later, CND is capped at ~$16M and has done all of the desktop studies needed to rank high impact drill targets.

CND is now at the stage where it can make a decision on a drilling program OR market it’s assets to potential funding partners...

In terms of market interest/excitement, here is where we think CND currently sits:

It’s important to note that increased excitement/interest shown on our chart below does NOT necessarily correlate to share price increases, which depends on many other factors and broader market conditions.

Ultimately we think the big move will come when CND locks in funding, mobilizes a rig to a drill target AND starts drilling...

Between now and the eventual drill program we could see CND deal on its assets which would trigger the start of the rally...

All of this forms the basis for our CND Big Bet which is as follows:

Our CND Big Bet:

“CND defines a multi-billion barrel prospective resource and sees its market cap re-rate by 20x prior to drilling”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CND Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

CND also has an existing gas discovery...

Another reason we like CND right now is because its valuation is de-risked by its existing gas discovery.

CND has one of the largest undeveloped offshore gas discoveries on the west coast of South America.

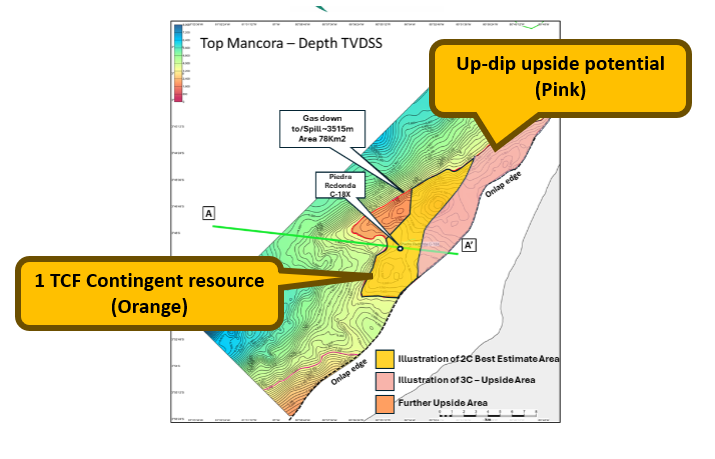

That is CND’s Piedra Redonda Gas field which has a contingent resource of ~1 trillion cubic feet of gas.

This is a CONTINGENT resource... meaning it is drawn from known gas accumulations - stuff that’s already there.

And there is still potential upside to that resource to the east of the project outside of the seismic data lines CND mapped its resource off of:

CND’s gas discovery is in shallow water and is less than 15km from the Peru shoreline...

It’s also a discovery that is technically de-risked - previous operators flowed gas to surface at a maximum 8.2mmcf per day.

AND that flow rate was from just a 32 feet section of the well that had 152 feet of total net pay...

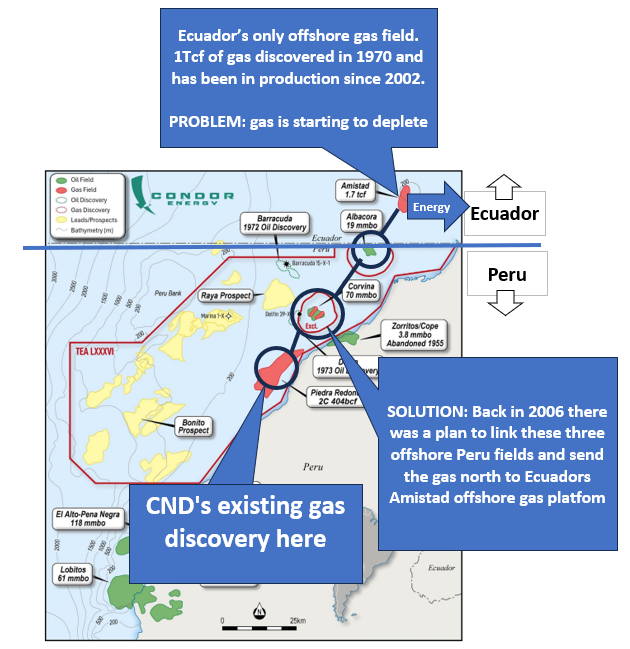

Back in 2006 the gas field was also almost developed to try solve Ecuador and Peru's energy crisis..

(which is now a much bigger problem...)

Ecuador and Peru are direct neighbors.

Ecuador only has one offshore gas field (Amistad) which has 1Tcf of gas and has been in production since 2002 - its right near the maritime border with Peru (and CND’s Peruvian acreage).

But the gas from Ecuador's field is starting to deplete and the Ecuadorian industrial sector is in need of more...

(Source)

We think energy from Peru could be a part of the solution here (not to mention the benefits to Peru itself)...

Less than three months ago the Ecuadorian Minister for Energy & Mines approved the import of 7.3 billion cubic feet of Liquefied Natural Gas (LNG) from Peru.

And the European Investment Bank said it would contribute US$125M to the construction of a power interconnector between Peru and Ecuador:

(Source)

All of that activity is happening in and around CND’s block... and where a possible development option would be tabled for its gas discovery.

Here is our rough image showing the 2006 gas to power development plan to “daisy chain” Piedra Redonda, Corvina and Albacora gas to the north via tie-in to the Amistad gas field platform just over the border in Ecuador:

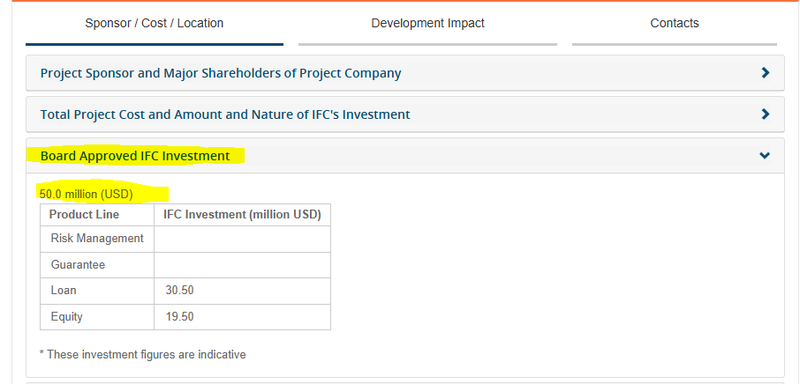

At one point the project even attracted funding from the World Bank International Finance Corporation who was going to partially fund it...

(Source)

BUT...

The previous owners at the time (a US company called BPZ) decided to focus on oil instead.

The gas market has come a long way since then. Most major mines and industrial users use gas to power their projects.

AND more and more electricity grids around the world are bringing gas flowered power generation into their energy mix.

Gas is earmarked as one of the best possible candidates for a “transitional” source of energy supply as the world moves toward more renewable energy sources....

Overall we think the likelihood of a gas project being developed nowadays is a lot higher than it was back in 2006 when the previous owners of the project flowed gas from the same asset.

AND as a result we think it really adds to the attractiveness of CND’s block overall.

What are the risks?

In the short term, the key risks for CND are 1) funding risk and 2) commodity risk.

Funding risk because CND have completed most of the desktop studies on their project.

Next will be about messaging when the company plans to drill one of its prospects.

Drilling an offshore target will cost a lot of money which CND’s current market cap wouldn't be able to support.

CND will therefore need to raise capital to fund drilling OR sign a deal with a funding partner to pay for the drill program.

A deal is never a guarantee and any delays could mean CND’s share price drifts lower as the market starts to price in a deal not being completed.

Funding risk

CND does not generate any revenues and so is reliant on raising capital to fund its exploration programs. If the markets are unwilling to finance CND’s exploration programs the company may need to go slow on its operations or offer large discounts to its share price when raising capital.

Source: “What could go wrong?” - CND Investment Memo 5 December 2023

“Commodity risk” because appetite for CND’s shares are loosely correlated to the oil price.

Over the last few day’s the oil price has come off a fair bit. Lower oil prices inevitably mean there is less incentive for companies to drill for new supply.

Usually for offshore exploration to be considered attractive we would need to see oil prices above ~US$80-90 barrel.

With oil prices now trading sub US$60 barrel, it could mean market appetite to finance a drill program OR major partners to farm-in will be diminished.

Commodity risk

CND’s project is leveraged to the price and demand for oil & gas. As the world looks to move away from fossil fuels, hydrocarbon projects may be phased out.

Source: “What could go wrong?” - CND Investment Memo 5 December 2023

To see more risks read our CND Investment Memo here.

Our CND Investment Memo

In our CND Investment Memo, you can find:

- CND’s macro thematic

- Why we Invested in CND

- Our CND “Big Bet” - what we think the upside Investment case for CND is

- The key objectives we want to see CND achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.