RML: USA critical metals, about to drill… and list on the US market

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 23,076,922 RML shares and 24,038,460 RML Options at the time of publishing this article. 4,295,863 shares and 14,647,931 options disclosed are subject to approval. The Company has been engaged by RML to share our commentary on the progress of our Investment in RML over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Over the last 48 hours, small ASX stocks with critical metals projects in the USA have been on the move up.

Why?

The sudden interest has likely been driven by what has been happening to Californian rare earths producer, USA’s MP Materials in recent days.

First the Department of Defence (the “Pentagon”) announced a US$400M equity investment into MP Materials:

(Source)

Then JP Morgan & Goldman Sachs committed US$1BN in construction financing.

Then it was Apple with a US$500M offtake agreement.

(Source)

All to secure the supply of critical rare earth minerals inside the US from California based producer MP Materials.

(The US Department of Defence even guaranteed a price floor for rare earths offtake at nearly DOUBLE that of the Chinese market)

And the Pentagon said they aren’t stopping there:

(Source)

This groundswell of interest in US-based critical minerals assets is why our exploration Investment Resolution Minerals (ASX:RML) is acquiring an antimony, gold, silver and tungsten project in Idaho, USA.

(The acquisition is set to complete at the end of July and RML plans to drill test its key targets in early August.)

RML’s US based project has already produced antimony, during both World Wars 1 and 2.

Antimony is used in various defence applications, most notably in bullets and ammunition - this is why it’s a critical metal.

The US has no domestic supply of antimony and buys most of it from China - this is why the US needs an urgent local supply

RML’s project is right next door to the biggest antimony (plus one of the biggest gold) projects in the USA - $2.3BN Perpetua Resources.

Perpetua Resources is somewhat of a market darling in North America (scroll down to check out the share price chart) - it's another company that the US Department of Defence has backed with funding over the last 18 months...

The backing was for the nationally strategic nature of its 200 million pound antimony resource estimate.

(The past performance of Perpetua is not a reliable indicator of future performance of RML. Success for RML is no guarantee.)

Two weeks ago, a senior resource geologist who spent 12 years at Perpetua joined RML - and commented on the similarity of the two projects.

(Source)

This geologist's incentive package gives him bonuses if the RML share price reaches 15c, 20c, 25c and 30c (Source)

Noting that while it’s good to see these incentives, they are not an indicator of the future price of RML.

We think the next bull run in the metals and mining space is going to come from US capital (and speculators) flowing into the USA critical metals sector.

How is RML going to gain US investor interest?

RML’s deal completion is two weeks away and its USA listing on the OTC market should be any day now based on RML’s announcements.

RML’s first drill campaign is starting in the coming weeks AND its proximity to Perpetua's national strategic antimony and gold project, PLUS the recent developments for MP Materials Pentagon funding could attract US investors to RML via the US OTC listing.

(but it also might not... we have to wait and see)

NASDAQ listed Snow Lake Resources is already buying RML and lodged a substantial holder notice on the 20th of June confirming it now holds 5.17% of RML (Source)

RML is the only ASX listed company with:

- Ground directly next to $2.3BN Perpetua

- On similar geology

- With historical production of antimony, gold and tungsten

- Drill ready antimony, gold and tungsten targets

- 6,000m of drilling planned to start in August.

So RML’s first drill program (scheduled for August) might just happen while US critical minerals stocks are running...

After the two big MP deals this week, ASX listed US critical minerals stocks are running again:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our 2024 Small Cap Pick of the Year, Sun Silver, is also running, hitting $1 yesterday - Sun Silver put out antimony news just yesterday...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

With a bit of exploration luck, RML could announce strong drill results just as the big wave of US capital starts flowing into the metals and mining space.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The ASX to USA baton pass

The “ASX to USA baton pass” is something we had written about a few months back. (Source)

Our view has for a while been that the giant pool of US capital (mostly from the tech industry) would eventually find its way into the minerals industry.

Even if it was only a small % that made the move over...

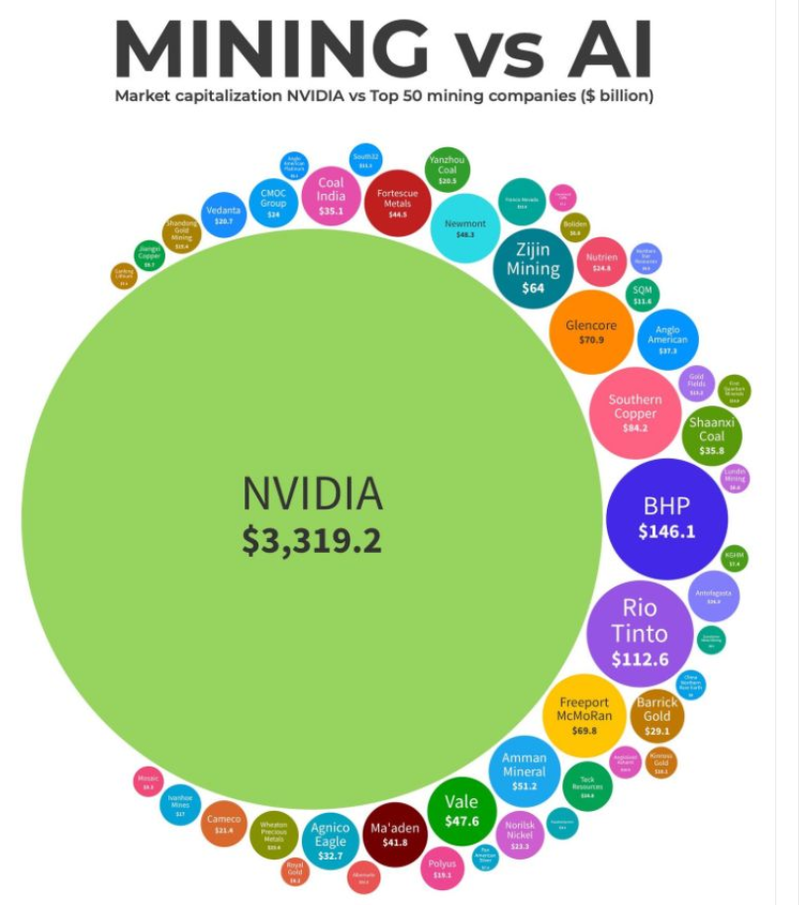

We used the NVIDIA vs the mining industry's heavyweights' market caps to illustrate the point:

(Source, Mining.com October 28, 2024)

Yes those two, small blue and purple bubbles are BHP and RIO - two of the biggest mining companies on the planet...

And yes, that giant green bubble is just one of the big tech companies, which is now capped at over US$4 trillion...

We think the deal between Apple and MP Materials wont be the last crossover between the tech giants and the minerals industry.

Especially with companies that have critical minerals inside the US...

The FIRST order effect of a deal like this is awareness.

Everyone knows Apple and will read about their US$500M offtake with a US rare earths producer.

The SECOND order effect will be capital inflows.

Particularly from the people who have made money as shareholders of successful US-based minerals companies like MP Materials and Perpetua Resources.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

RML is trying to become “Perpetua 2.0”

RML’s neighbour Perpetua, is up over ~1,000% in the last ~24 months - aiming to become USA’s first onshore source of antimony.

Again - while past performance of Perpetua is no guarantee of future performance of RML, it's worth understanding how Perpetua got to where it is today.

First and foremost the Perpetua’s project is a gold project.

But the momentum builder for its project has been its giant antimony resource estimate.

Right now, about 85% of global antimony supply comes from China, Russia and Tajikistan.

The US has no domestic source of antimony and is completely import dependent, which could explain why the US government has been so active trying to get Perpetua’s project up and running.

(Perpetua’s project, once in production, could produce ~30% of all US antimony needs).

So far the US government has given Perpetua:

- US$24.8M in funding from the Department of Defence.

- US$34.6M in 2024 under the Defence Production Act.

- US$1.8BN letter of interest for a loan from the US Export-Import bank

- Recognition as one of the first 10 minerals projects critical to the US’s national interest (in the FAST-41 program).

- Final federal permit permit before construction can begin (this last one took ~8 years to land)

These funding/permitting announcements were the major catalysts that made Perpetua the 10 bagger it is today:

With the rapid success of companies like MP Materials and Perpetua Resources over the last 18 months, we think that a lot of the investors who made money off Perpetua will eventually start looking for the “Next Perpetua”

Of course there’s no guarantee that the past performance of Perpetua is indicative of the future performance of RML.

We have seen this sort of thing play out in our Portfolio before

In the previous lithium bull market, we were Invested in Latin Resources, a lithium exploration junior looking to emulate the success of its Brazilian lithium neighbour Sigma Resources.

Sigma was up ~35x in ~4 years and at its peak was capped at nearly $6BN.

Latin was looking to make a new discovery in the same region, on similar geology.

Here is one of our old notes talking about how Latin could become Sigma 2.0:

(Source)

With some luck Latin made a lithium discovery and its share price went from ~3c pre-drilling to just over 40c at its peak.

At its peak Latin’s market cap was >$1BN.

One of the reasons that Latin Resources was able to reach the heights that it did was because of the clear and obvious market comparison in Sigma Lithium.

The same way that there is a clear and obvious market comparison for RML - Perpetua Resources.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

IF RML is able to declare a discovery and define a large enough resource estimate, the market will have a very obvious peer to which it values RML’s ground.

AND we think Perpetua’s $2.45BN market cap could only get bigger as its project is put into production.

(no guarantee of course - companies can lose value as they get closer to and enter production)

Perpetua expects to have its mine online and producing by 2028.

Growth in Perpetua’s valuation can only be good for RML and it will just mean there are investors who have made even more money off Perpetua looking for Perpetua 2.0.

Ultimately, we are hoping that the investor interest in Perpetua trickles down into RML (assuming RML can discover and define a resource of its own).

Drilling success forms the basis for our RML Big Bet which is as follows:

Our RML Big Bet:

“RML to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RML Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for RML?

Deal completion 🔄

We want to see RML complete the acquisition of its Horse Heaven project.

The shareholder meeting to approve the deal is set for Friday the 25th of July.

We expect deal completion straight after that.

Mapping and sampling 🔄

RML is currently:

- Mapping and sampling across both of its two main targets.

- Mapping and sampling across regional targets, AND

- Confirming drill sites for its August drill program

That work should mean that we could see some rock chip sampling results come to market between now and the acquisition being completed.

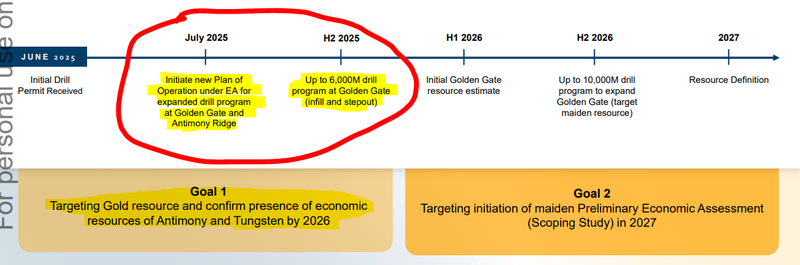

Drilling (August) 🔄

Then in “early August” we want to see RML drill its Golden Gate target.

Golden Gate is where RML has ~3.5km of known strike where old drillholes have delivered hits as good as ~71.6m at 1.37g/t gold and 36.6m at 1.51g/t gold.

None of the old drilling here was ever tested for antimony or tungsten, so there is all of that upside come drilling time.

(Source)

What are the risks?

RML hasn’t started drilling just yet so the two main risks we see to RML’s share price in the short term are “capital structure risk” and “funding/dilution risk”.

Capital Structure Risk

After RML completes its current capital raise and acquisition it will have ~1.2BN shares on issue and over 800M options exercisable at 1.8c per share.

There is a chance the outstanding options act as a weight on RML’s share prices in the short-medium term.

IF RML’s share price goes above 1.8c then the market may start to price in dilution and more supply coming onto market (through option exercises) which in turn may cause some selling in anticipation of those options coming to market.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

One thing to note though is that the options are listed, so the likelihood of them being exercised, turned into fully paid shares and sold on the market is lower.

Funding risk/dilution risk

As a pre-revenue small cap company, RML is reliant on capital markets to advance its projects.

If something negative happens at a macro or company level, RML could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

RML recently raised $1.9M at 1.3c per share. A large chunk of that cash would have gone toward finalising the acquisition of its new project in Idaho, USA.

It’s possible RML will require additional funding from capital markets to progress with its planned drilling. We should get an update on the company’s current cash balance when the June quarterly report is released at the end of the month.

For the full set of risks we have identified and accepted in making our Investment in RML, see our RML Investment Memo below.

Other Risks

Like any stock market investment, investing in RML carries a multitude of risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

Here we aim to identify a few more risks.

The company’s primary asset is a pre-discovery gold-antimony-tungsten-silver exploration project and it is possible that RML makes no economic discoveries.

RML is also highly sensitive to fluctuations in commodity prices. A sustained downturn in these prices could materially impact the project’s economic viability and the ability of RML to raise cash to finance exploration.

RML is a highly speculative investment which has already rallied significantly in recent weeks, and the current share price may already reflect the anticipated news mentioned in this article.

There is no guarantee RML will receive any government funding or support, including from the US Department of Defence, despite strategic interest in antimony.

The Company is as mentioned reliant on capital markets to fund development, and any capital raise may dilute existing shareholders.

Finally, regulatory, environmental, and permitting risks in the US jurisdiction - while generally stable - may delay or adversely affect development.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RML Investment Memo

You can read our RML Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our RML Investment Memo covers:

- What does RML do?

- The macro theme for RML

- Our RML Big Bet

- What we want to see RML achieve

- Why we are Invested in RML

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.