Riding the Bull and Bear Cycles

Published 05-OCT-2024 16:04 P.M.

|

19 minute read

- Commentary: What we learned over the last 2 years of bear market Investing. Why is our 2024 Portfolio doing so much better than our 2023 Portfolio? Is the market about to come back?

- Quick Takes: SS1, OJC, L1M

- This week in our Portfolios: GUE, PFE

Everyone's a “genius” in a small cap bull market.

At least that is what it felt like between November of 2020 and June of 2022.

All IPO’s oversubscribed, cap raises were highly competitive and good news was being rewarded with on-market buying.

Everything was going up.

(Remember things like Afterpay? Lithium at $80,000/t? Gamestop? Shells with a $10M EV? The occasional “50 bagger”?)

Since then, it has been MUCH harder to navigate the small cap market during the “bear” winter.

It’s been the worst couple of years we have seen.

Interest rate hikes had sucked the money and appetite out of the small cap system.

A big party results in a big hangover...

In the last 2 years it has been much harder to find winners due to way less liquidity in the market and scarce attention on small cap stocks.

However, we try to see a bear market as an opportunity to pick up new Investments trading at beaten down valuations that could re-rate when the bull market cycle ultimately returns.

Many of our best Investments were made during the 2020 COVID market crash and subsequent bull market.

Naturally we have been trying to “do it again” with our new crop of Investments during the recent bear market.

Now it’s not as easy as it sounds, as we have found out...

(nothing ever is in small caps)

Just because it worked once, doesn’t mean it will work the same way again.

Timing also factors into it.

Our COVID crash Investments worked really well because the bull market quickly kicked in after the crash.

When the current bear market first kicked in during 2022, we paused making any new Investments for 6 months, to observe how things would play out and how “bad” it would get before making any new moves.

In early 2023, we decided the time was right to start adding a few “bear market bargains” that could roar back when sentiment turned.

Surely a return of sentiment was just around the corner?

Nope.

The bear market just kept on going and going... and getting worse.

And many of our 2023 positions could have been acquired at a lower entry price if we waited.

We are long term holders and give a story a few years to play out, so it doesn't affect our thesis, but getting a good entry price and timing it into a good market is always preferred.

So we have been participating in placements in our 2023 stocks to bring down our average entry price going into more positive market conditions.

In hindsight, during 2023 we also probably focused too much on early stage exploration, rather than later stage companies with more advanced assets underpinning the valuations.

Early stage explorers suffer the most when the small cap market is risk-off, so if the bear market drags on they get hit the hardest.

We also observed that companies with more advanced stage assets/projects were trading at what we consider low market caps (<$20M).

These assets/projects are developed and have had a lot of work put into them, but market conditions were such that they were being valued well below replacement values.

So for our 2024 Vintage of Investments we focused more on companies with later stage projects where we thought the market was not reflecting the intrinsic value of the assets.

(but still with a potential blue sky kicker that we love)

Our view was that if we could more objectively value the assets of later stage companies and be patient with our capital to hold these investments, then over time the market would catch on.

And in 2024 a return of positive sentiment feels more possible than it did in 2023.

Especially after a September US rate cut and China’s stimulus “Bazooka”.

So in 2024 we leaned into later stage companies rather than roll of the dice, blue sky exploration.

We did also add one exploration stock, and if the small end of the market IS in fact starting to turn back positive, we may look to add a couple more.

So lesson learned from 2023 - the window for picking up “cheap” exploration stocks needs to be when the market sentiment is just starting to turn, not when it is at rock bottom... where exploration stocks could get “even cheaper”)

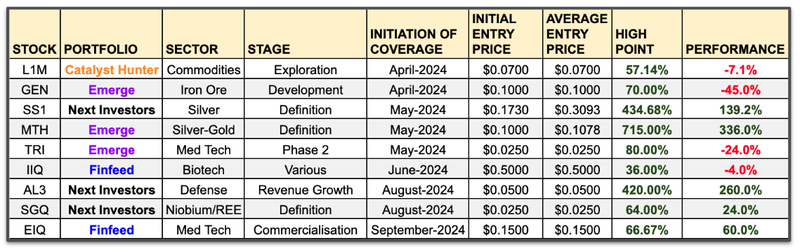

2024 has been a good year so far and the new strategy seems to be working, with a couple of sustained winners in our “later stage” companies MTH, SS1, AL3 and EIQ.

GEN has suffered a bit due to the iron ore price having a bit of a vomit over the last 6 months, but has now raised money again and the Chinese stimulus announcement has popped the iron price back up

Here is a list of the Investments we have made in 2024:

With the small end market feeling like it is finally going to turn positive soon, but not yet having “roared back”, we are considering accelerating the number of new Investments for the next few months, ahead of return in sentiment.

BUT we could also get bitten again (2023 style) if it’s another false start and the market goes back to sleep again for another 6 to 12 months.

We’ll probably just stick to our current pace and add two more new investments for the year (possibly 3 if the market is still looking good).

So on that note, here is an update on each of our 2024 Vintage so far:

Mithril Silver and Gold (ASX:MTH)

Initial Entry Price: $0.10 (increased position again at $0.20)

Return from Initial Entry: 380%

MTH was the best performing stock on the ASX in September.

Looking for more gold and silver in Mexico, MTH hit a huge intercept just as the gold price was breaking out into new all time highs and silver was running up too.

33m intercept from SURFACE at average grades of 31.8g/t gold and 274g/t silver.

MTH already has an existing JORC resource of 11 million ounces of silver and 373,000 oz gold - which is 529,000 ounces of gold equivalent.

(this is why we added it in 2024 as a “later stage” company with a genuine project + exploration upside)

MTH is currently drilling to try and double that JORC resource by Q1 2025.

Up as high as 715% from our Initial Entry Price, MTH is the best performing company from our 2024 Vintage so far.

After hitting a high of 81.5 cents MTH has since come off, but the company is still holding firm around the 50c mark which we hope is the base for another leg up in the share price.

MTH has assays pending for a drillhole ~50m away from the one that sparked the ~7x rally.

If that drill result comes in then we think MTH could go on another run.

Especially after the silver price ended this week at new 12 year highs, almost touching US$33 last night:

It really looks like the silver price wants to go on a run, especially if it can comprehensively clear that previous high point from earlier this year that it’s been knocking at for the last few weeks.

Sun Silver (ASX:SS1)

Initial Entry Price: $0.173 (increased position again at $0.625)

Return from Initial Entry: 334%

Another one of our Investments that will “ride the wave” if the silver price does go on a big run over the next 12 months.

Our 2024 Small Cap Pick Of The Year SS1 has 423 million ounce silver equivalent JORC resource at its project in Nevada, USA.

SS1 also has a potentially significant antimony resource, pending reassaying historical drill cores that were not assayed for antimony, only for silver and gold.

Since IPO, a couple of things have gone in SS1’s favour:

- SS1 is currently the largest primary silver resource on the ASX... at a time where the silver price has reached a decade high and looks to break out..

- SS1 found antimony on its project... weeks before China banned antimony and sent the US government scrambling to secure domestic supply.

- SS1’s peer Silver Mines announced permitting issues... which drove capital and attention towards SS1 as the new de facto “silver stock” on the ASX.

- Finally, SS1 managed to raise capital from an institutional investor at a PREMIUM to its market price at the time.

There is still plenty of newsflow for SS1.

SS1 is currently drilling to upgrade its giant silver resource even further.

Also, it is now well funded to further define any antimony that sits over its project - something that is of great interest to the US Department of Defence.

We look forward to the next few years following the SS1 story, as we could not have asked for a better start for our 2024 Small Cap Pick of the Year (and for the silver price).

AML3D (ASX: AL3)

Initial Entry Price: $0.064

Return from Initial Entry: 181%

AL3 was our 2024 Tech Pick of the Year.

(and they have big shoes to fill after our last Tech Pick of the Year ONE, that has been one of our most successful ever Investments)

This story is pretty unique in our Portfolio.

AL3 specialises in robotic, automated 3D metal printing of parts that are built on site and on demand.

(displacing traditional methods of casting and forging like blacksmiths did in mediaeval times)

AL3 sells custom 3D printed parts and 3D printing systems to large organisations like the US Navy and Boeing Defense and Space.

These types of parts require all sorts of certifications, which AL3 has spent years putting in place.

With rising tensions across the world, and countries ramping up defence spending, demand for systems like AL3’s is becoming more and more apparent.

While the business model isn't set up to have exploration style binary drill results, one large purchase order or contract from a major customer can be a game changer if struck on the right terms.

These lumpy revenue style tech businesses selling into giant customers are the ones that we tend to understand best, where the sales cycle is long but revenue is sticky (like with ONE).

Since our initiation note, AL3 has delivered:

- Manufacturing Licence Agreement with the US Navy through an intermediary

- Manufacturing Licence Agreement with Boeing

- $1.1M Sale of its 3D printing product to a US Navy Supplier

We are particularly interested in the MLAs as it enables the exchange of highly sensitive technical data and assistance required to 3D print a wider menu of parts for customers like the US Navy.

Think of it like UberEats, but for the US Navy to quickly and conveniently order urgently needed spare parts.

We are watching to see if these MLAs will gain traction with suppliers and if AL3 can sell more hardware (3D printing products) to customers.

Echo IQ (ASX:EIQ)

Initial Entry Price: $0.15

Return from Initial Entry: 63%

EIQ is our most recent new addition to the 2024 Portfolio and the largest market cap company at the time of our Investment.

EIQ has developed an Artificial IntelligenceI tool that helps specialised doctors detect heart related issues.

Cardiovascular diseases are the leading causes of death worldwide - it’s a big problem and a big market.

We liked EIQ because of the team behind the project, the “size of the prize” they are going after and the clinical trial results that indicate EIQ’s AI tool is incredibly effective.

Also, the team behind EIQ has been developing its AI for almost ten years, WAY before ChatGPT was a phenomenon and suddenly everyone wanted to invest in AI companies.

Any day now we should know the results of EIQ’s FDA submission on the first heart condition it is targeting - aortic stenosis.

FDA approvals will provide EIQ a clear pathway to commercialise its AI product in the US$10BN market through insurance reimbursements or licensing agreements.

This could be “company making” for EIQ.

In addition, EIQ is working towards FDA approval for a second cardiovascular condition - heart failure.

Heart failure has a bigger market (US$70BN) and commands a higher reimbursement price.

We think that the story over the next twelve months for EIQ will be working towards two key FDA approvals as well as commercialising its AI product, with a focus on the large US market.

Plenty for us to look forward to as EIQ shareholders.

Speaking of AI in disease detection...

TrivarX (ASX:TRI)

Initial Entry Price: $0.025

Return from Initial Entry: -20%

TRI has developed an AI powered algorithm to screen for mental health disorders by analysing a patient's sleep data.

The blue sky for TRI here is that if it turns out that sleep data CAN successfully be analysed by its AI to screen for depression, it is likely able to screen for OTHER mental health issues too.

(like anxiety, PTSD, bipolar, alzheimer's, etc - all huge markets on their own)

And then down the track, TRI’s AI could be refined to potentially be integrated into wearables like a Fitbit, Apple Watch or Oura Ring that all track simplified sleep data.

Since we Invested, the company has published the results of its Phase 2 clinical trial (read our take here) and the company will look to do additional clinical validation studies to get FDA approval.

Right now the company has requested a pre-submission meeting with the FDA on how to best conduct a final “pivotal trial” on its AI screening tool for Major Depressive Episodes.

We are hoping that the pivotal trial will be the final step for TRI to take its product to market.

Inoviq (ASX: IIQ)

Initial Entry Price: $0.50

Return from Initial Entry: -5%

IIQ is a biotech company developing diagnostics and therapeutics for various cancer and neurological conditions.

The company uses exosomes - nano-scale little messengers within the body (much smaller than a human cell) to identify these conditions.

Since we first invested, IIQ has published data that showed its exosome technology could potentially create a “fingerprint” for the early detection of Parkinson’s and Alshiemerz’s disease.

It is in its early stages but there is potential for a big scientific breakthrough.

We are backing EIQ because of the team behind the project, in particular David Williams (chairman of Polynovo) and the company’s cornerstone investors Merchant Group.

Polynovo is one of the great ASX biotech success stories of the last decade, having re-rated from ~4c to ~$4 in under four years (up over 10,000%).

IIQ has three directors who are all with or were previously with Polynovo, and Merchant was also an early investor in the company.

We like to back the due diligence and follow in successful investors in sectors (especially highly technical / scientific spaces like biotech), and this is a big reason we are Invested in IIQ.

Over the next few months IIQ will be advancing its exosome diagnostics platform.

At any point in time, IIQ could sign a deal with a laboratory partner to bring its breast cancer test to market.

In the background, IIQ is undergoing a clinical validation test for ovarian cancer, the results should be published by the end of the year.

St George Mining (ASX:SGQ)

Initial Entry Price: $0.025

Return from Initial Entry: 24%

SGQ is about to complete the acquisition of an advanced niobium/REE asset next door to the world’s biggest niobium mine in Brazil.

Next week, SGQ shareholders have a meeting set to approve the deal.

If/when the deal is approved, and SGQ takes control of the asset, then we expect a lot of early news flow and progress from SGQ.

One of the key reasons we liked SGQ’s new acquisition was because we think that when it comes to niobium, projects like SGQ’s are a lot more likely to be developed when compared to more greenfield discoveries.

This is because it is in the right place (next door to the largest producer with all of the infrastructure in place), at the right time (niobium is 2nd highest critical mineral for US and Europe - the world needs more niobium) to support the development of the project.

Lightning Minerals (ASX:L1M)

Initial Entry Price: $0.07

Return from Initial Entry: 0%

L1M is the one departure from our focus on later stage companies in 2024.

L1M is an early stage Brazilian lithium explorer, following in the footsteps of one of our best ever Investments, Latin Resources.

L1M has lithium exploration ground in the same “Lithium Valley” of Minas Gerais, Brazil where Latin Resources made its company making lithium discovery.

We first Invested in LRS at a sub $20M valuation. At one point LRS was valued at $1BN.

Earlier this year Latin Resources announced a deal to be acquired by Pilbara Minerals for north of $600M.

L1M has just identified a lithium trend through soil sampling, returning similar anomalies to Latin Resources did pre-discovery.

L1M is at a very early stage in its exploration - and is valued at less than $10M.

L1M is yet to drill test their project, and is going through the process to determine the best drill targets at the moment.

Lithium exploration stocks are unloved for now, but when sentiment inevitably returns we think there is scope for a material re-rates on drilling success.

Genmin (ASX:GEN)

Initial Entry Price: $0.10 (increased position again at $0.05)

Return from Initial Entry: -20%

GEN is developing an iron ore mine in Gabon.

All of the permits are in place, the DFS is published and 4 offtake MoUs are signed with Chinese companies.

Backed by Tembo Capital, GEN is fast approaching a Final Investment Decision on the project and some key funding hurdles to take it into production.

We first invested the GEN in the recap round at 10c share price back in April.

And as often happens in small cap land, the macro theme sentiment turned against us.

Ongoing concerns about an economic slowdown in China caused the iron ore price to come off over the last 6 months... and hence so did GEN’s share price.

Delays in a potential financing deal saw GEN go into halt this week, and it raised $10M at 5c.

(we participated in this placement to average down our Initial Entry Price)

Whilst these delays and macro conditions can be frustrating for longer term holders with higher entry prices than 5c - could things soon be changing for GEN?

The Chinese economic stimulus package announced over the last couple of weeks put a rocket under the iron ore price:

Enough to break out of the downtrend? We’ll see in the coming months.

We’re hoping this will add fresh impetus for offtakers and potential financiers to commit support to GEN’s iron ore project in Gabon.

Let’s not forget that the US Fed is cutting rates too now, and it’s possible a lot of the iron ore naysayers don’t factor in how much pent up demand there could be for iron ore under the covers in a world of expansionary monetary policy.

GEN has a solid project for this type of macro environment, it just needs to secure financing to build it

We’re Invested to see GEN get into production, noting that the company has 4 offtake MoUs with 4 Chinese steel producers that all fall within the top 15 of world steel production.

What we wrote about this week

Global Uranium and Enrichment (ASX:GUE)

Are there hints of another uranium spot price run starting?

Back in 2023 we took new positions in a couple of uranium stocks predicting that the uranium price would run.

...and it did.

But for the last 6 months the uranium price has gradually drifted downwards after its strong run.

So did uranium stocks.

This week we wrote detailed coverage on one of those 2023 uranium Investments - GUE.

Read: GUE delivers high grade uranium drill results - uranium price peeks higher.

Pantera Minerals (ASX:PFE)

Back in 2023, Pantera Minerals (ASX:PFE) began securing land rights over the Smackover Formation in Arkansas, USA.

Why?

PFE had cottoned onto recent activity in the historically oil producing Smackover which pointed to it potentially becoming a future lithium hotspot.

The idea was that old oil wells could be cheaply re-entered to extract lithium rich brines.

A nearby company was doing the same thing.

Meanwhile, PFE continued to quietly build its land position in the Smackover.

Turns out PFE was right about it becoming a lithium hotspot...

Read: Surrounded by big neighbours... PFE about to re-enter well for lithium

Quick Takes

SS1 announces thick silver intersection from pXRF results.

OJC - Bigger is Better as OJC merges into FMCG Behemoth

L1M working up Brazilian lithium targets

GEN completes $10M raise, we participated

BPM completes oversubscribed placement to advance gold exploration

NTI - FDA rejects orphan drug status for PANDAS/PANS

GAL set to drill PGE targets in November

GTR neighbour completes US$175M M&A deal

SLM adds to copper ground in Peru

Macro News - What we are reading & listening to

Battery Materials:

Energy Transition: China Has Broken the ‘Critical Minerals’ Market (Bloomberg)

- China's control of cobalt and lithium has caused prices to drop, but low prices don't ensure supply security.

- Dependence on China's supply chain poses a long-term risk to the energy transition.

Biotech:

Big pharma, biotech ‘won't necessarily be symbiotic’ in AI: S&P (Fierce Biotech)

- Big Pharma's investment in AI is growing rapidly, but this may position AI-focused biotechs as competitors, not partners, threatening pharma's internal R&D.

- The pharma-AI market, valued at $1 billion in 2022, is projected to reach $22 billion by 2027, creating competitive advantages for early adopters. (Hello EIQ and TRI).

Copper:

Major Copper Discoveries | S&P Global Market Intelligence (Spglobal)

- Since 1990, 239 copper deposits have been discovered, with a 4% increase in total volume this year, driven mainly by older deposits.

- A refined copper deficit is projected by 2027, with mine supply peaking in 2029, leading to a possible 2.2 MMt deficit by 2032.

How copper will shape our future (BHP Insights)

- Global copper demand may increase by 70% to over 50 million tonnes by 2050, fueled by economic growth and electrification.

- Ageing mines and declining production require 10 million tonnes of new mined copper annually in the next decade.

Gold:

Analysts warn of ‘peak gold’ by 2026, say junior miners are the answer (Kitco News)

- Central banks and retail investors have driven gold prices to record highs in 2024, but scarce new discoveries threaten future supply.

- There have only been five major gold discoveries since 2020, highlighting a trend of fewer, smaller finds and raising concerns about meeting demand.

Silver:

How the US Lost the Solar Power Race to China (Bloomberg)

- The U.S. has lost its solar industry leadership to China, with over 90% of solar polysilicon now produced there, despite once being a major player.

- Factors like corporate complacency, a lack of investment, and high energy costs contributed to the decline of U.S. solar manufacturing, creating a gap filled by China's aggressive growth in the sector.

Uranium:

Why Tribeca's Guy Keller plans to lead, not follow, on the next uranium move (Stockhead)

- Guy Keller warns of Western complacency regarding uranium supply, highlighting potential for price increases as demand grows and production struggles.

- His fund has seen a 39.15% annual return, while he views many Australian uranium stocks as undervalued amid a fundamental supply-demand mismatch.

What we are listening to:

Peter Krauth – Pro Tips On Investing In Junior Silver Stocks

$100 Silver: Solar Powered (Webinar)

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.