RCM: Gallium and Germanium? Permits in, drilling commencing in a few weeks... while we wait for moonshot silver drill results

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,213,572 RCM Shares at the time of publishing this article. The Company has been engaged by RCM to share our commentary on the progress of our Investment in RCM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The global markets are back.

A US-Iran deal is nearly done, SpaceX IPO is up 35% in its first two sessions, mood has switched back to positive, NASDAQ is up 3% last night.

The global AI and AI datacentres buildout rolls on, hyperscalers raising hundreds of billions to build.

Silver is up ~14% in the last few trading sessions.

(but remember, markets can go up AND down. We'll take this positive sentiment swing for now)

Rapid Critical Metals (ASX:RCM) is currently drilling into the guts of a potential new parallel silver lode they clipped the edge of in previous drilling.

(to add to its 67 million ounce silver equivalent resource estimate across three projects)

We are waiting on early news or visuals, possibly any day now.

BUT...

Prior to acquiring its silver project a year ago... RCM was working towards acquiring and drilling another project for two critical AI semi-conductor and military minerals in Canada:

Gallium and germanium.

RCM hasn’t really talked about this critical minerals project since it acquired its silver assets and focused on silver a year ago.

But this morning, RCM announced that it finally got the permits to drill it - seems like they have been quietly busy in the background while banging the drum on the silver.

And RCM says the gallium and germanium drilling is set to begin in a few weeks time, with first results shortly after.

(meaning no long waits and long lead up to drilling, RCM just got the drill permits - plus now we will have silver AND gallium and germanium drilling going on at the same time)

What we do know heading into drilling is that RCM’s project has some of "the highest germanium grades globally” - all from surface samples - 22.69% zinc, 40 g/t gallium and 1,500 ppm (0.15%) germanium.

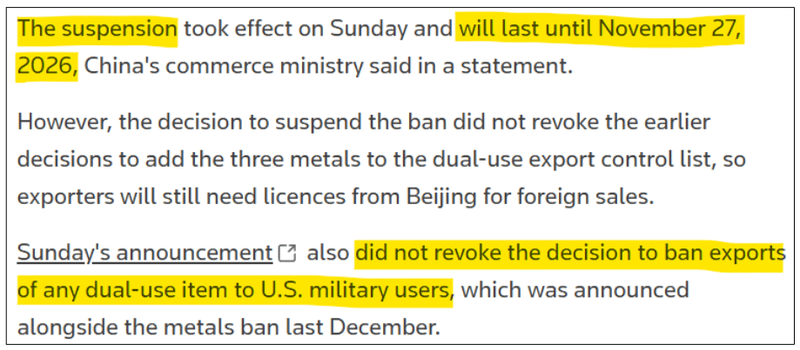

In 2024 China put export restrictions on critical minerals.

These restrictions kicked off the entire “US critical minerals” macro theme on the ASX and turned a few micro cap explorers into billion dollar companies (check out Dateline and Larvotto).

Two critical minerals that China banned exports of back in 2024 were:

- gallium - used in military semiconductors for higher power/frequencies, and;

- germanium - used in fibre optic cables and infrared military systems.

China has since softened the broader critical minerals export bans while negotiating a trade deal with the US...

(The export bans were turned into a licensing regime running to late November 2026)

... BUT one thing that stayed was the ban on selling gallium and germanium to "military end-users".

(source)

China controls roughly 98% of the world's gallium production and around 60% of its germanium.

So the US gallium/germanium supply problem is nowhere near solved - for the most critical of uses - national defence.

Which probably explains why the US Department of War is stockpiling gallium & germanium (source).

The DoW has some existing germanium stores with a small program recycling from army equipment to top it up.

Plus no gallium stockpiled as of at least 2024 (it isn’t exactly the sort of thing you would communicate and let your adversary know about). (source)

As we mentioned up top, RCM plans to drill its gallium and germanium project in less than 6 weeks (the announcement said ‘late July’).

Again, RCM’s project has some of "the highest germanium grades globally” - all from surface - 22.69% zinc, 40 g/t gallium and 1,500 ppm (0.15%) germanium.

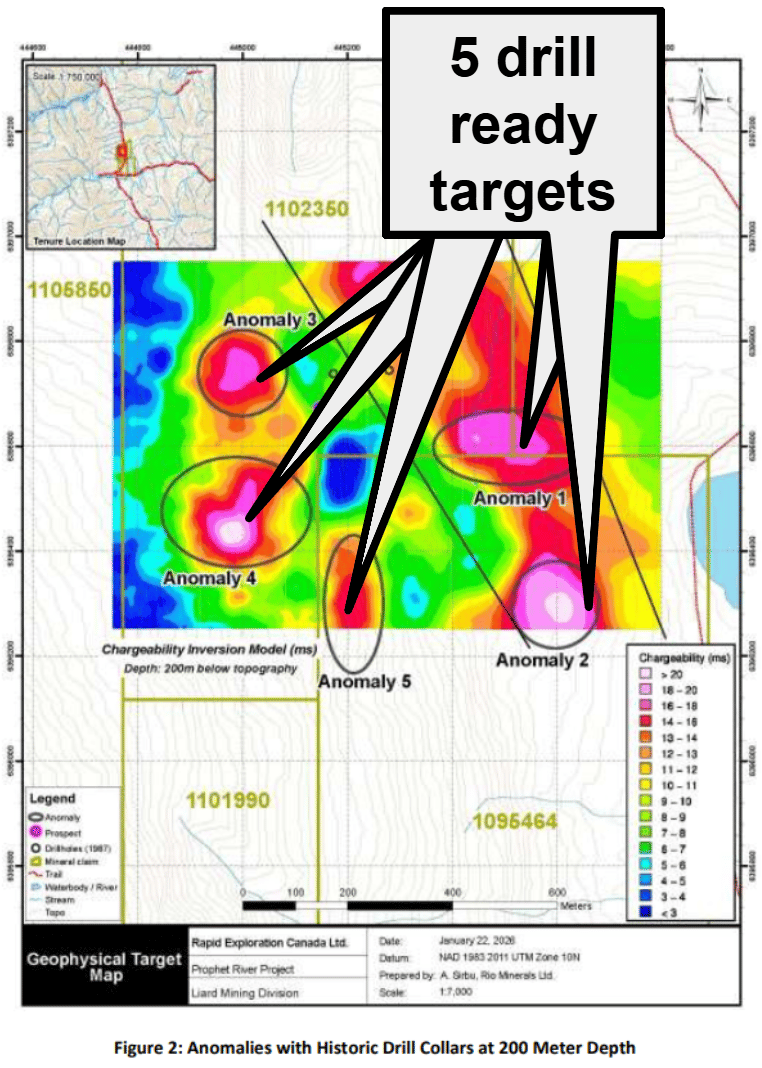

Over the last 12 or so months RCM has quietly mapped, run geophysical surveys and surface sampled the project.

Now RCM has FIVE drill ready targets based on geophysical surveys that line up with those high grade surface samples.

(source)

Wait... isn’t RCM a silver stock?

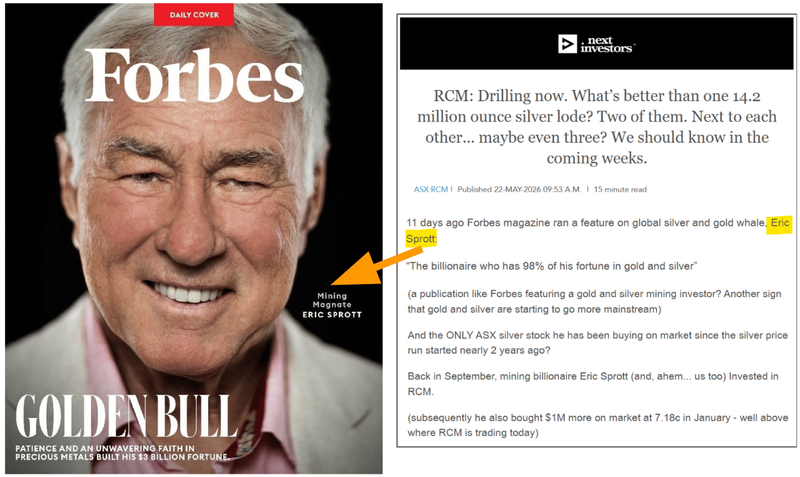

Avid RCM followers might be wondering... isn't RCM a silver stock, majority owned by billionaire silver investor Eric Sprott?

(the one of which he bought an additional ~A$1M on market at ~7.18c per share in January?)

(source - our prior RCM article)

Yes...

The NSW silver asset was the main driver for our Investment in RCM, where it is currently drilling 15,000m.

RCM has three projects in NSW with ~67M ounce silver equivalent JORC resource estimate, and wants to grow this to 100M ounces.

(We added RCM to our Portfolio because we think silver is going to go on a generational run, taking ASX silver stocks with it)

Silver’s up 14% from its lows over the last few trading days.

So while we wait for silver to find its base and start running again we ALSO now get to see RCM have a crack at a critical mineral discovery on RCM’s gallium/germanium project in Canada.

We think that a new critical minerals discovery in Canada - IF big enough - could attract strategic funding from the US - especially now that the US has committed to funding “Allied projects” through its Defense Production Act (Title III).

Like Canadian Fireweed Metals' who received US$15.8M for its tungsten project in Canada from that specific Defense Production Act (Title III) program.

(source)

And Canada is fast-tracking permit reviews of critical minerals projects tied to defence and semiconductors. (source)

Is that why RCM now has its drill permits in place as of today?

In a few months we should know if RCM has got a discovery big enough to get the attention of US government capital deployers.

Another reason we think exploration success on this asset can really get things going for RCM is because of the Eric Sprott factor.

Why we think Sprott’s RCM holding matters even more now

We keep coming back to Eric Sprott with RCM.

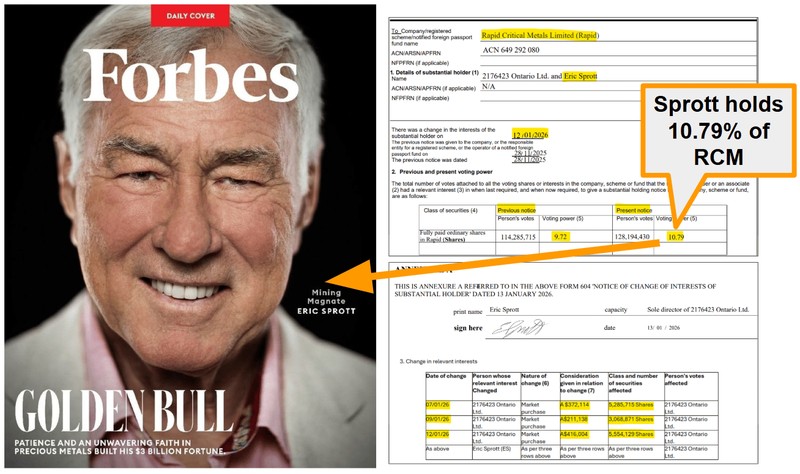

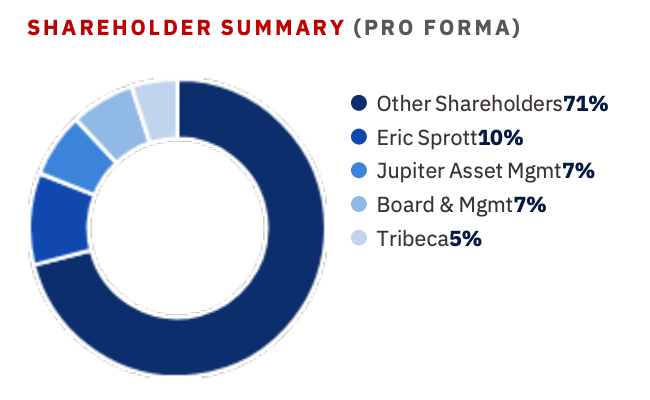

Sprott is one of RCM’s biggest individual shareholders owning 10.79% of the company, including personal holdings.

The thing is, Eric Sprott rarely ever ventures into the ASX, let alone a microcap like the $40M capped RCM.

He is usually too busy buying lazy $100M+ positions in North American giants like Hycroft (which we happen to own some of too).

Over in North America, retail investors have dedicated X (the social media platform formerly known as Twitter) accounts tracking his live holdings or any other stocks he buys/sells.

(the below X post is not financial advice, we are simply showing an example of the online global army that follow Eric Sprott’s moves)

(source)

Which means any company Sprott invests in automatically shows up on the radar of thousands of investors all across North America.

A bunch of investors who would probably never hear of a tiny ASX small cap otherwise...

It’s sort of like the more niche version of being a company Elon Musk has invested in.

Anyone into investing knows Elon Musk, and as a result have heard of SpaceX (and even a lot of those who don't care about the markets).

So when SpaceX goes public - they don't mind dabbling in the IPO.

The same thing happens for a company Eric Sprott invests in (except on a smaller scale and limited to the mining/precious metals bulls... for now - but that Forbes cover we saw above is another example of more people finding out).

Read more about the power of distribution/marketing in our “meme stock reactivation” thesis here: The reactivation thesis: When meme stocks awaken.

The basic gist of all of this is that if a stock becomes well known amongst a big audience - any good news can re-rate the stock more than it would have with no audience.

Pretty intuitive stuff - fill the stadium with an audience and then kick a few goals...

SO ... IF RCM gets lucky and makes a discovery... there will hopefully be a bigger, Sprott-o-sphere driven North American following (as well as on the ASX) looking at RCM who may want a piece of it.

Then Sprott buying MORE RCM on market in January (~A$1M at ~7.18c per share) - well above where RCM trades today becomes a thing the market talks about.

Then the market does more DD and sees that he is not alone on the register either:

- Eric Sprott - ~10.79%

- Jupiter Asset Management (UK resources fund) - ~7.29%

- Tribeca Investment Partners (Australia's largest natural resources fund) - ~5%

And a gallium-germanium discovery in North America is instantly “backable”.

(source)

Obviously we are thinking pretty far ahead here and we have made a number of leaps in assumptions on how a crowd of investors might think - there’s no guarantee any discovery gets made and how the market will react.

Right now RCM hasn’t even started drilling its critical minerals asset yet - but we think now is the right time to be thinking about it given the drill permits are in and a rough timeline for drilling has been set.

Meanwhile the rig continues to turn on its NSW silver asset..

Here's some ideas on how RCM could re-rate over the next 3-6 months

Another reason we think RCM could re-rate into good news is because RCM has a fairly strong balance sheet.

RCM had ~$8.8M in cash and listed stock in Iris Metals at 30 April 2026. (source)

That should give RCM more than enough cash to get the drilling done on its silver projects in NSW and have a crack at the Canadian asset without having to stop for a capital raise.

That means anyone who wants exposure will need to step in and buy on market.

Here are the three catalysts we think can trigger the need to step in on market:

- The silver price - If silver does what we (and Sprott) think it can - pushing toward US$150/oz and beyond - the whole thin pool of ASX silver names re-rates.

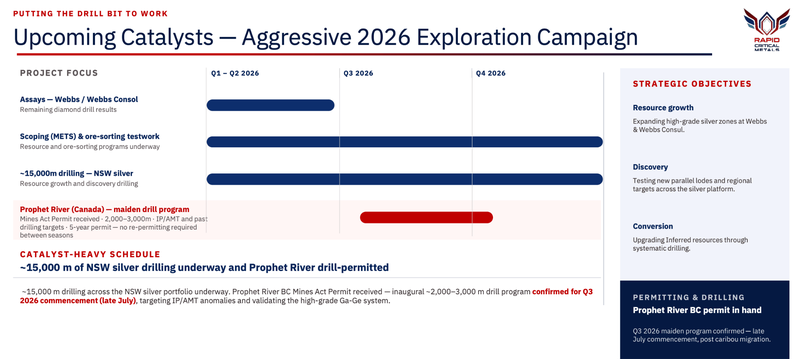

- Silver drill results + the scoping study - RCM is drilling now (more on the drilling in a second) AND has a scoping study running across all three NSW silver projects, targeted for completion this quarter (i.e. due any week now).

- After today a shot at a North American critical minerals discovery inside the next few months.

Our RCM Big Bet:

“RCM expands its existing silver resource through new discoveries into a silver bull market and re-rates by over 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RCM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

More on RCM’s Australian silver projects

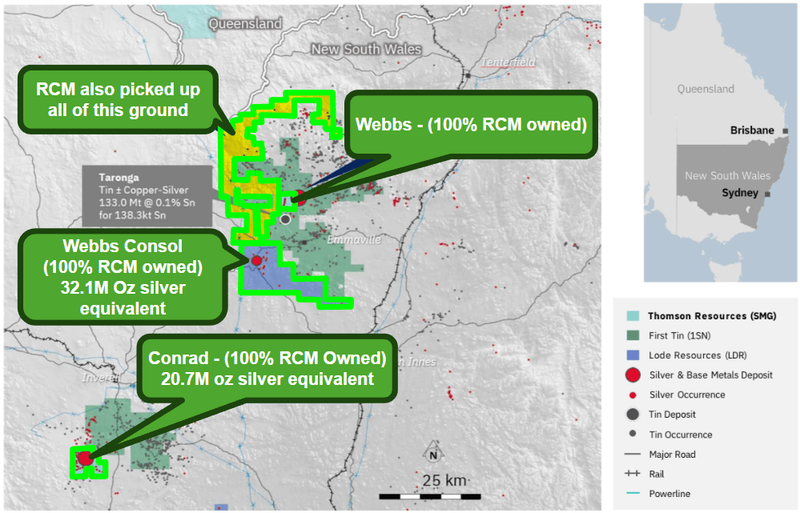

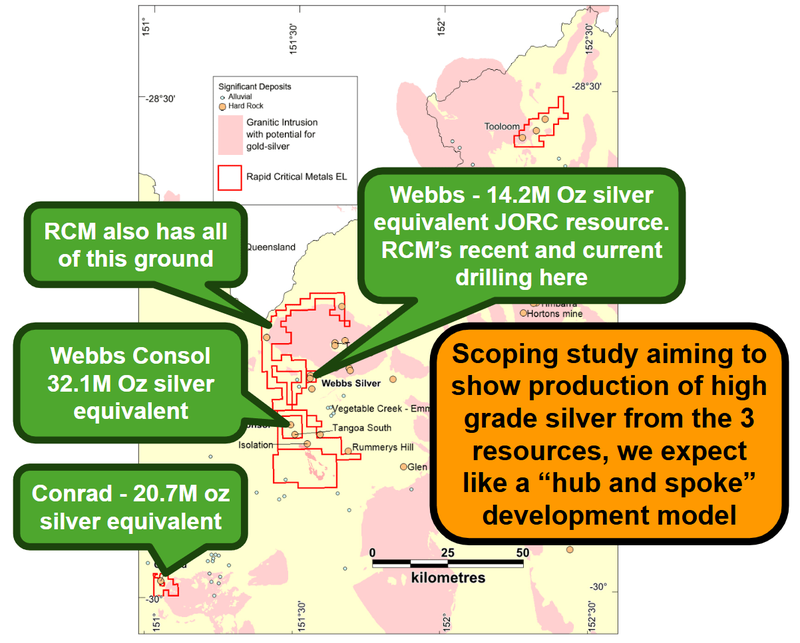

As mentioned earlier, RCM had three projects with a combined 67M ounces of silver equivalent JORC resources (estimated):

(source)

RCM has a goal of getting to 100 million ounces of silver equivalent resources across the projects with more drilling and/or land acquisitions.

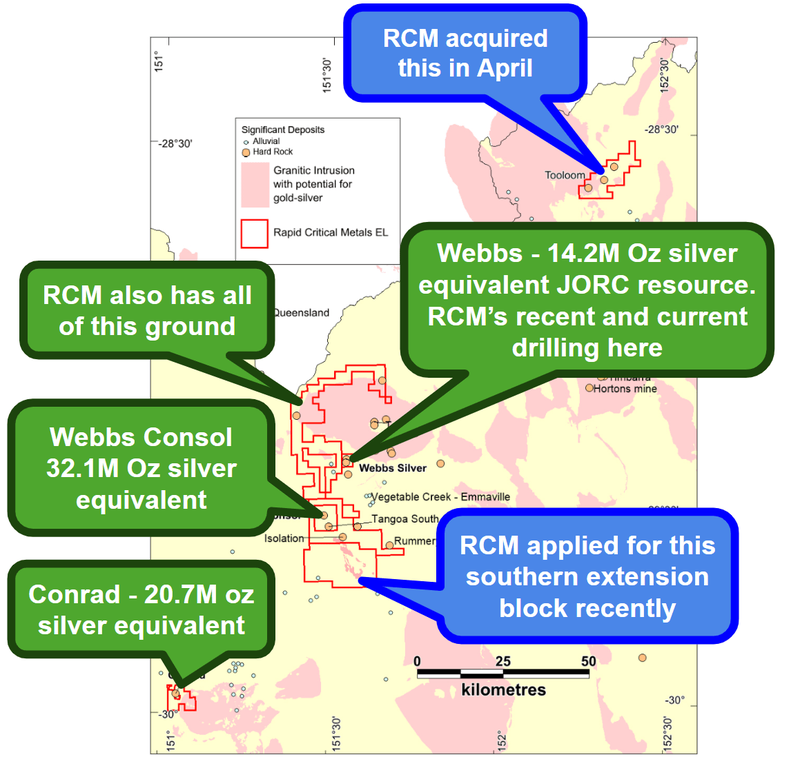

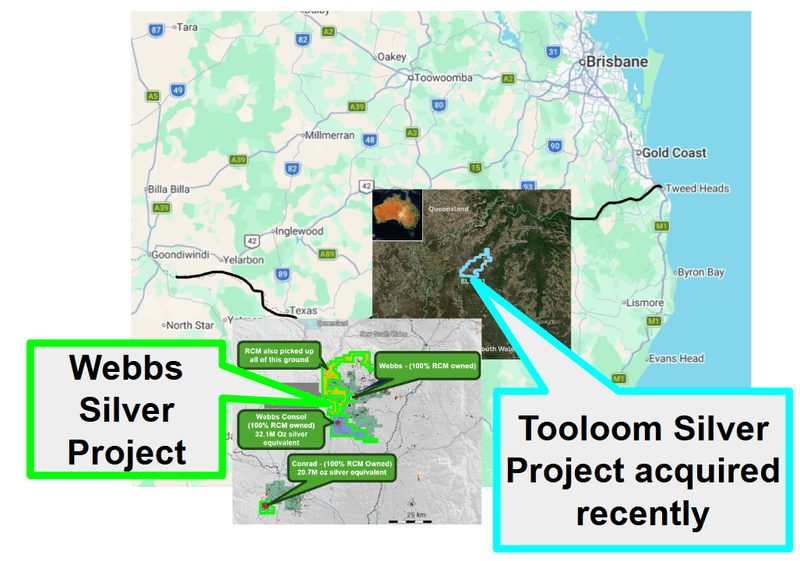

In April RCM acquired an 80% interest in another asset ~100km north-east of its existing NSW projects. (source)

That new asset has rock chips up to 1,660g/t silver, 80 historic silver workings across 21km of strike and mining activity between 1887 and 1925.

None of which has been drilled before.

Here is everything RCM holds:

(source)

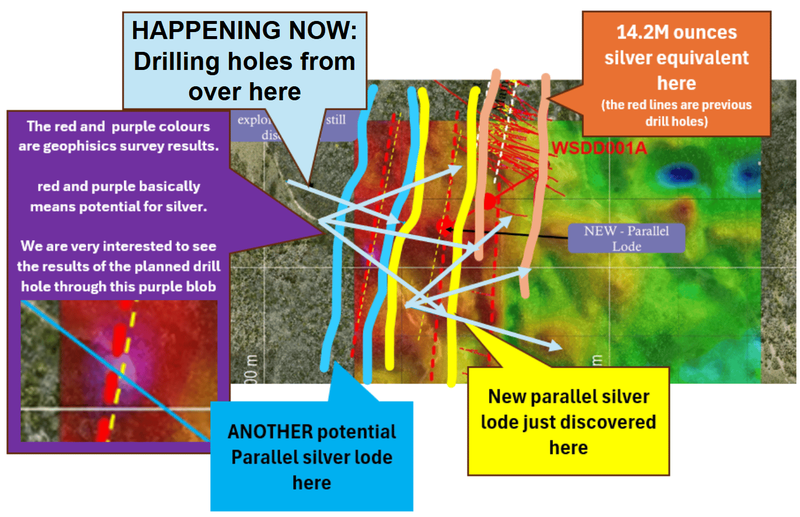

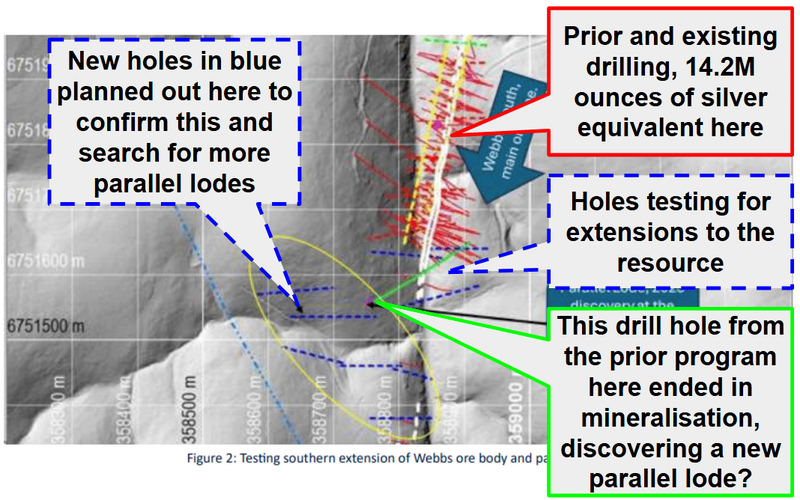

RCM is drilling at Webbs right now:

We covered the last round of drill results in our last note in December.

The standout hit from that program was 2.6m at 136 g/t silver equivalent.

Small in size, but importantly, the hole had ended in mineralisation.

So the question hanging over RCM since December was whether or not RCM clipped the edge of a big new silver system.

OR if it was just an isolated bit of silver mineralisation in the rock.

Here is the image we had in our December note for what we wanted to see next:

(source)

RCM’s current drill program is designed to do two things:

- Test extensions of the new parallel structure - southern corner of the project

- Extend the existing resource - along the south

The best part is the current drilling will happen from the opposite angle to that first program.

So we will definitely learn a lot of new things about the project this time around:

(source)

RCM also has a scoping study incoming

While we wait for drill results another thing we are looking forward to is the scoping study RCM is doing across all three of its silver projects in NSW.

RCM started the study in late January 2026 and it’s targeted for completion this quarter (source).

(this quarter ends June 30 - so the study is due any week now.)

Because all three of RCM's silver projects sit fairly close to each other, the study is looking at a model where the company processes all three projects’ ore at one central facility.

(source)

We think the scoping study could be a catalyst because so far, RCM has been valued as an explorer.

The market hasn’t really been given any sense of the economics of a potential mining operation across the three projects.

The scoping study will be the first time RCM publishes a meaningful look at how its three NSW silver projects might actually be developed and what they might be worth in NPV terms.

We should also see some numbers on operating costs and CAPEX.

The two numbers we'll be looking out for from the study:

- The CAPEX number - how much it costs to build the project

- The NPV - and especially the sensitivity tables at different silver prices

And of course the sensitivity of the project to silver prices (how the NPV changes with higher silver prices).

RCM will probably have to plug in a conservative price assumption to their model - but if we can see the sensitivity tables we can start to see what the economics look like at Eric Sprott’s predicted US$300 per ounce silver price.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Rapid Critical Metals

What’s next for RCM?

(source)

🔄 Gallium/Germanium drilling in Canada

We want to see RCM lock in a rig and start drilling the project.

The drilling window in that part of the world usually starts about now and runs through to October/November, before the winter months kick in.

So ideally we see that project drilled inside this current drilling window.

RCM expects drilling to start in “late July” with assays due next quarter.

🔄 Silver drilling in NSW (Webbs project)

With the first of two rigs now turning at Webbs, we want to see RCM extend the existing resource at Webbs to the south.

And drill out the parallel structure theory.

The ideal scenario would be a confirmed NEW discovery to the west and extensions to the existing resource to the south.

🔄 Target generation on newly acquired asset

On the asset RCM acquired today we want to see the company complete LiDAR surveys, surface sampling and geophysics.

Ultimately, we want to see the historic results validated and then a bunch of drill targets ranked from most interesting to least ahead of a drill program on the project.

🔄 Scoping study across projects in NSW

We also want to see RCM complete a scoping study for its projects in NSW - this will be the first time we get a sense of the potential economics of the projects 67M ounce silver equivalent resource base.

What are the risks?

The biggest risk for our RCM Investment right now is "exploration risk".

RCM just got its 15,000m drill program underway.

There is no guarantee that any of it returns economic results.

Poor exploration results would negatively impact RCM's share price especially with the amount of capital that would be spent on a two rig, 15,000m program.

Exploration risk

There is no guarantee that RCM's upcoming drill programs are successful. RCM may fail to find economic silver resources, in which case we would expect the share price to re-rate lower.

Source: "What could go wrong" - RCM Investment Memo 17 Sep 2025

Other Risks

Like any early-stage exploration company, RCM carries significant risk, here we aim to identify a few more risks.

With a 15,000-metre drilling campaign underway in NSW, RCM is facing a period of high cash burn to fund its multi-rig operations.

This aggressive exploration schedule means the company may require further capital raises in the future, risking shareholder dilution.

The upcoming scoping study will outline the project economics, including expected development CAPEX and ongoing operating costs. If these figures are higher than the market anticipates, it could heavily impact the projected net present value of the assets.

RCM's ambitious target of building a 100-million-ounce resource is highly dependent on favorable silver macro trends.

A sharp downturn in global silver prices would significantly harm the economics of a potential mining operation and compress the company's valuation.

While the Canadian project shows exceptionally high-grade surface and rock chip samples, the five drill targets are currently based on early geophysics.

There is always an inherent risk that the upcoming drilling campaign fails to replicate these high grades at depth or prove continuous, commercially viable mineralisation.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RCM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our RCM Investment Memo where you will find:

- What does RCM do?

- The macro theme for RCM

- Our RCM Big Bet

- What we want to see RCM achieve

- Why we are Invested in RCM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.