RCM: Drilling now. What’s better than one 14.2 million ounce silver lode? Two of them. Next to each other... maybe even three? We should know in the coming weeks.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,213,572 RCM Shares at the time of publishing this article. The Company has been engaged by RCM to share our commentary on the progress of our Investment in RCM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

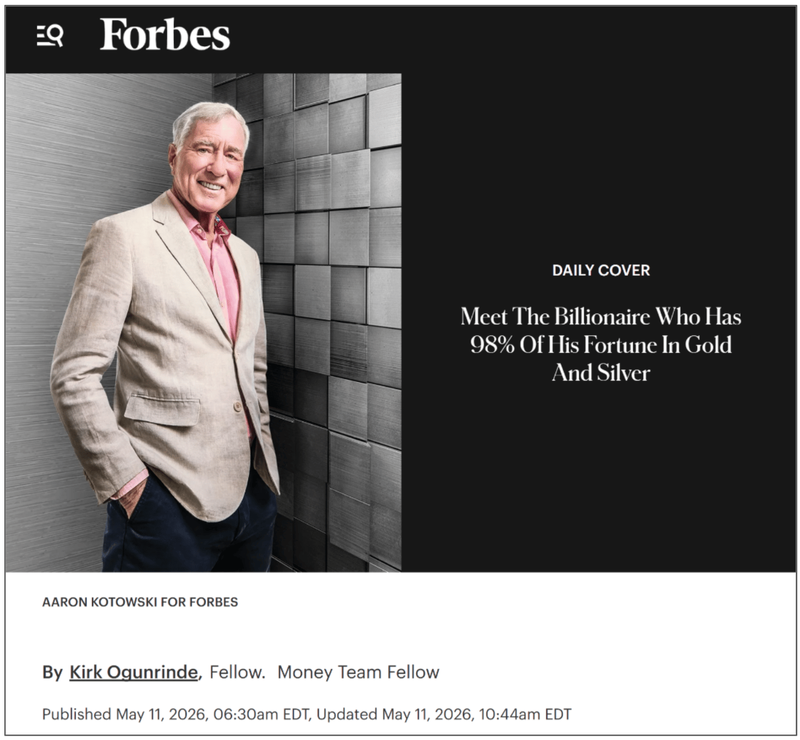

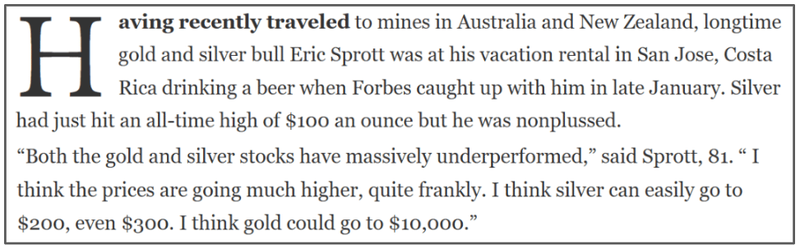

11 days ago Forbes magazine ran a feature on global silver and gold whale, Eric Sprott:

“The billionaire who has 98% of his fortune in gold and silver”

(Source)

(a publication like Forbes featuring a gold and silver mining investor? Another sign that gold and silver are starting to go more mainstream)

And the ONLY ASX silver stock he has been buying on market since the silver price run started nearly 2 years ago?

Back in September, mining billionaire Eric Sprott (and, ahem... us too) Invested in RCM.

(subsequently he also bought $1M more on market at 7.18c in January - well above where RCM is trading today)

We think silver is going to at least US$150/oz.

Eric thinks it's going even higher.

And at 81 years of age (with 50+ years of gold and silver mining investment experience) he has seen quite a few precious metals cycles.

So we both added Australian silver explorer and developer RCM to our Portfolios.

(Of course, Sprott and us could be wrong in our silver thesis - commodity prices can be fickle and are impossible to predict with any certainty. This is small cap speculative investing and anything can happen.)

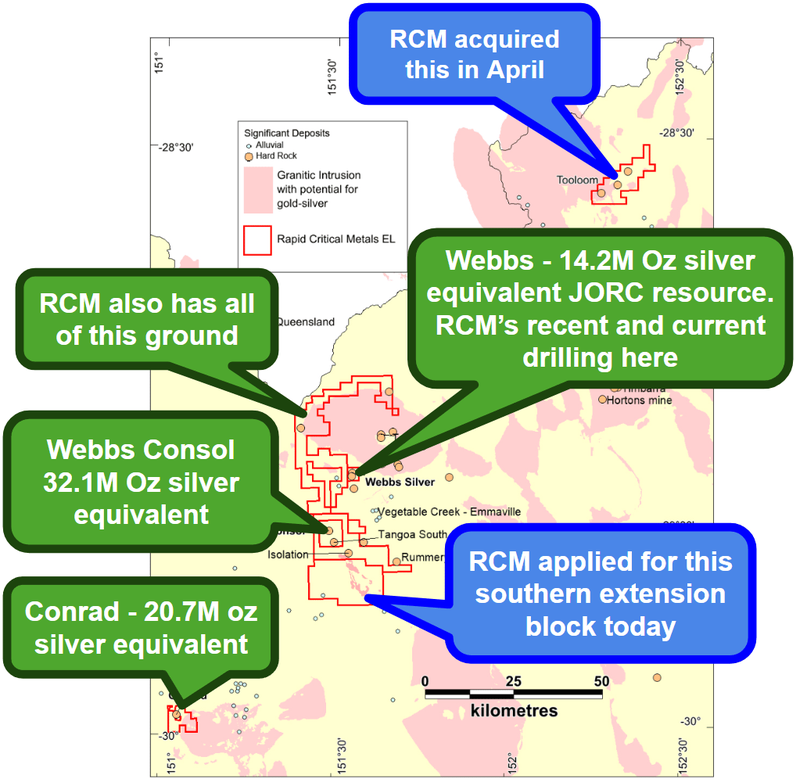

RCM has 67 million ounces of silver equivalent resources across all its NSW silver projects, and wants to get this number to 100M oz silver equivalent.

(Silver is currently trading at US$76 per oz)

RCM can get to its 100M oz target via drilling and making new discoveries and/or land acquisitions (RCM has been doing both over recent months).

Today RCM confirmed it has started drilling again - read the announcement here.

And it could rapidly grow its silver resource with this current drilling campaign - here’s how:

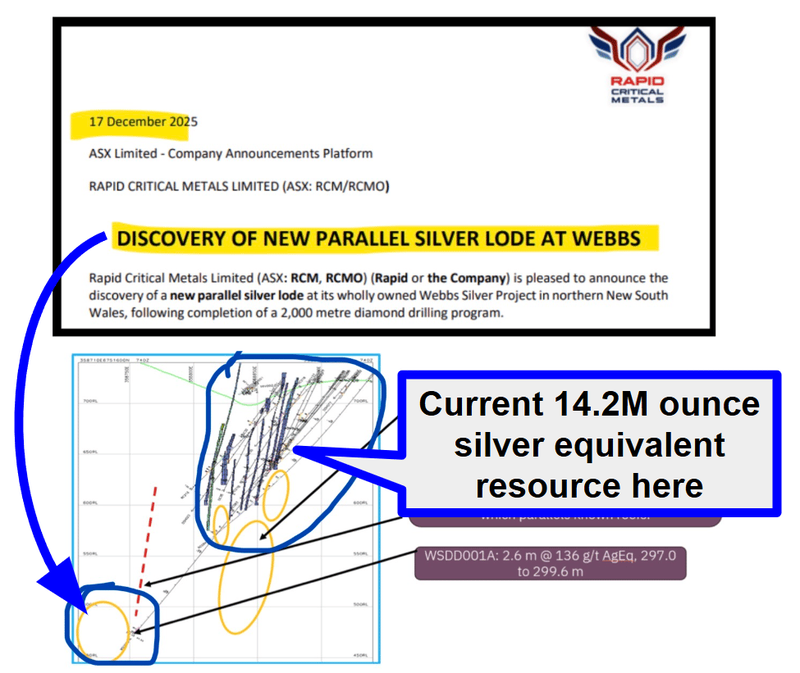

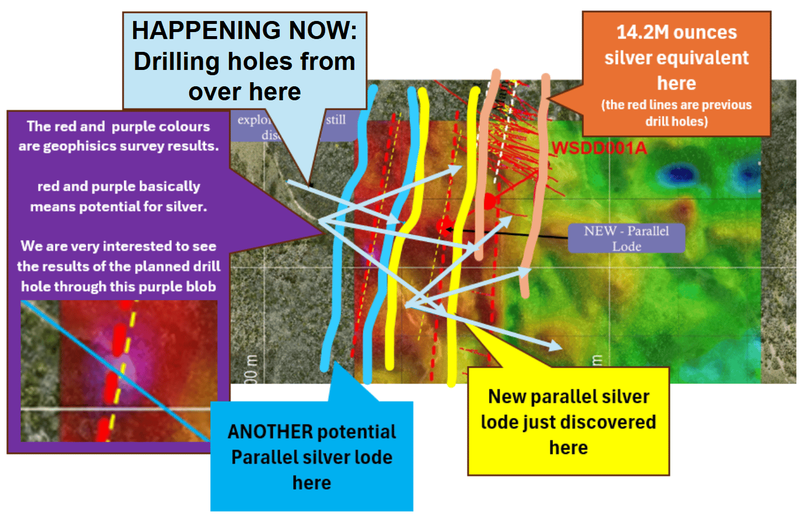

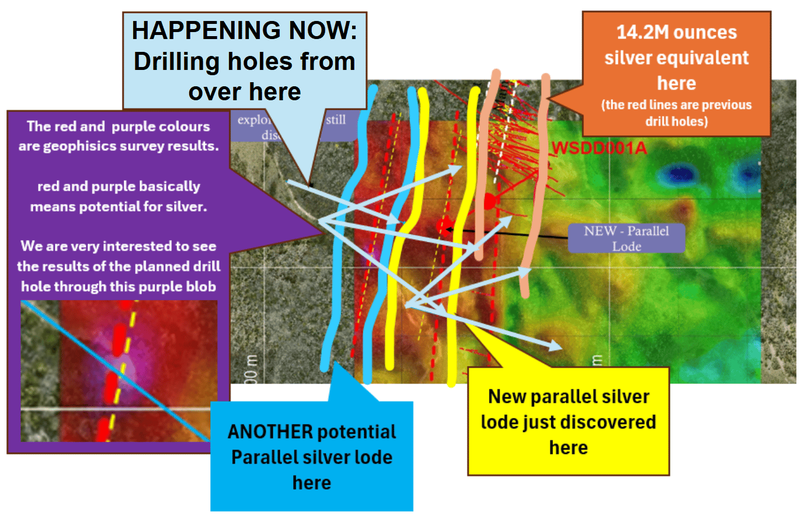

~Six months ago, RCM drilled next to its existing Webbs 14.2M oz JORC silver equivalent resource.

That existing resource comes from just one silver lode alone.

(A “lode” is mining speak for a highly mineralised chunk of ore)

During that recent drilling, RCM clipped the edge of what could be a totally new parallel silver system.

RCM hit 2.6m at 136 g/t silver equivalent with the hole ending in mineralisation - a solid clip.

But because the hole ended in mineralisation, we don't know how big it is - it's unfinished business.

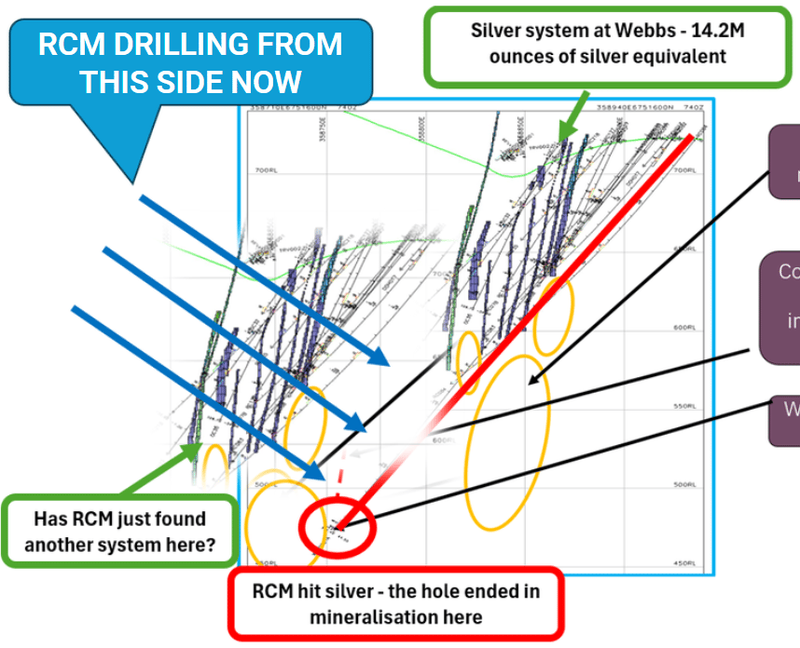

Today RCM announced it has commenced drilling into it from a new position and angle that will allow the drill bit to pass through the (predicted) guts of this new parallel lode.

Is this potential new lode of similar size to the 14.2M oz silver equivalent resource nearby?

Is it bigger?

Are there more parallel lodes?

What we want to see next:

Confirmation of a repetition of RCM’s 14.2Moz silver equivalent high grade silver lode.

Confirmation of the possibility that there could be EVEN MORE repeating lodes.

AND the silver price going to US $150 per oz.

All in the next couple of months, please.

Is that too much to ask?

Followed by more drill results on RCM’s other targets.

(no guarantees of course, there’s a very low chance of all of these events happening in that amount of time)

We can see how RCM can get to its 100Moz target with some drilling success.

Plus RCM's recent organic land expansion has created ~12km of strike between two high-grade silver deposits at each end.

Most of the corridor between them is completely undrilled - so RCM’s upside comes from filling in the gap plus extending the known lodes at depth/along strike.

Like RCM is aiming to do with the drilling that started today.

So how big could this new parallel silver lode be?

RCM is now drilling into (what could be) the guts of its new parallel silver lode to find out.

Today RCM confirmed that drilling is underway (the first of two rigs has started drilling)

Here is an image of the clipped lode:

(source)

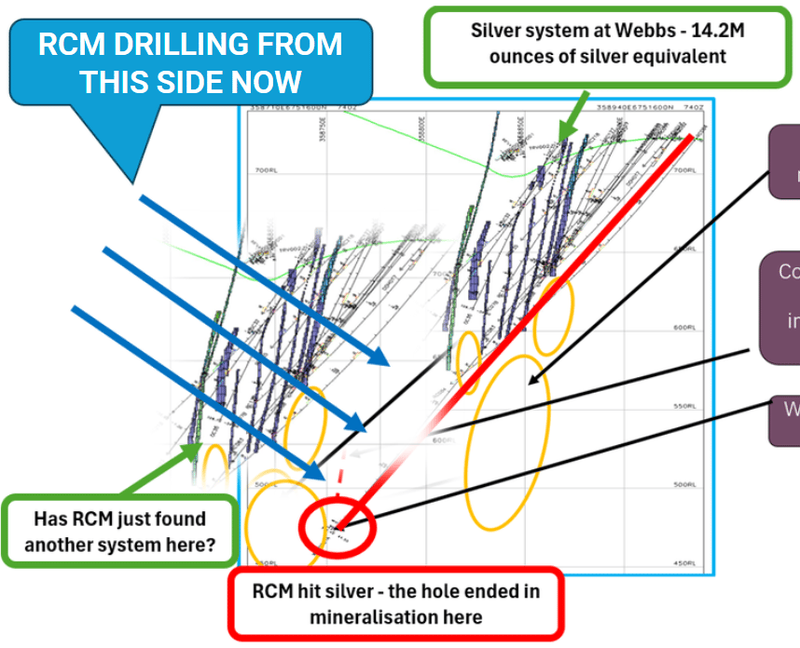

Today, RCM started drilling that structure to the west - coming at it from a completely different angle (optimised to make sure we hopefully find out what’s there).

The ultimate win from that structure to the west would be a repeat (or something bigger than) the Webbs deposit - something like in the image we made below:

(source)

We Invested in RCM back in September 2025 alongside two big institutions and THE global silver and gold whale (and now Forbes magazine cover star) Eric Sprott.

Who combined now own ~25% of RCM:

- Tribeca Investment Partners (~7.2%) - Australia's largest natural resources fund

- Jupiter Asset Management (~7.29%) - UK active resources fund

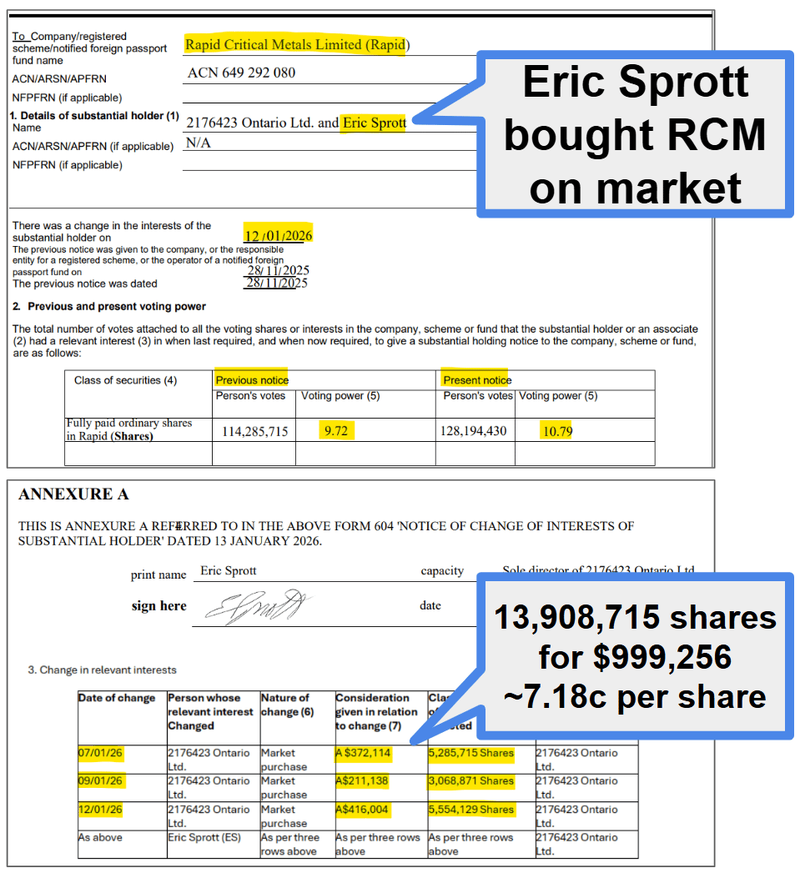

And... billionaire silver bug Eric Sprott who owns 10.79% of RCM.

Yes... THE Eric Sprott... here he is again on a recent Forbes article:

(source)

Sprott initially came into RCM at the same round as us - when RCM raised $14M at 3.5c per share in September last year.

But he didn't stop there, in January he bought MORE RCM on market.

As far as we could find (yep we asked a bunch of AI platforms), RCM is the only ASX listed silver stock we have seen on the ASX that Eric Sprott himself has been buying on market and bought more of.

He bought another 13.9 million RCM shares on market in January at an average price of ~7.18c per share

That’s ~$1M, at prices well above where RCM trades today at 3.9c per share.

That took Sprott’s holding from 9.72% to 10.79%.

(source)

Perhaps this was around the time of the Forbes interview when the 81 year old legend was sinking a beer chatting to the Forbes journo about his multi-billion dollars precious metals fortune:

(source)

If he is right and silver goes to $200-300 per ounce then 7.18c/share for RCM might end up looking cheap...

(of course he could be wrong as well)

Another interesting fact - those January buys from Sprott all happened after RCM discovered the potential parallel silver lode at its Webbs deposit last year.

Remember today RCM started drilling that same zone - this time going in from the west.

We should find out what that hit last year was all about in the coming weeks.

We always look forward to a good new drill campaign following up a discovery.

Where the company returns to the field after having had time to look at what it discovered.

Then put in a big drill campaign to see how big the find really is.

(Sprott must too with that $1M buying spree in January)

(source)

Now we get to see RCM run a 15,000 metre drill program right next to its existing 14.2M oz silver equivalent JORC resource at Webbs.

(Across its three NSW projects RCM has a ~67M ounce silver equivalent JORC resource)

We are hoping to see RCM drill out a big parallel system on par (or bigger) than what’s at Webbs.

As mentioned earlier the ultimate win would be a repeat (or even something bigger than) the Webbs deposit:

(source)

RCM has one rig going right now and a second rig incoming pending approvals.

So RCM should be able to drill this thing out fairly quickly.

How did RCM get to where we are today?

We covered the last round of drill results in our last note in December.

The standout hit from that program was 2.6m at 136 g/t silver equivalent.

Small in size, but importantly, the hole had ended in mineralisation.

So the question hanging over RCM since December was whether or not RCM clipped the edge of a big new silver system.

OR if it was just an isolated bit of silver mineralisation in the rock.

Here is the image we had in our December note for what we wanted to see next:

(source)

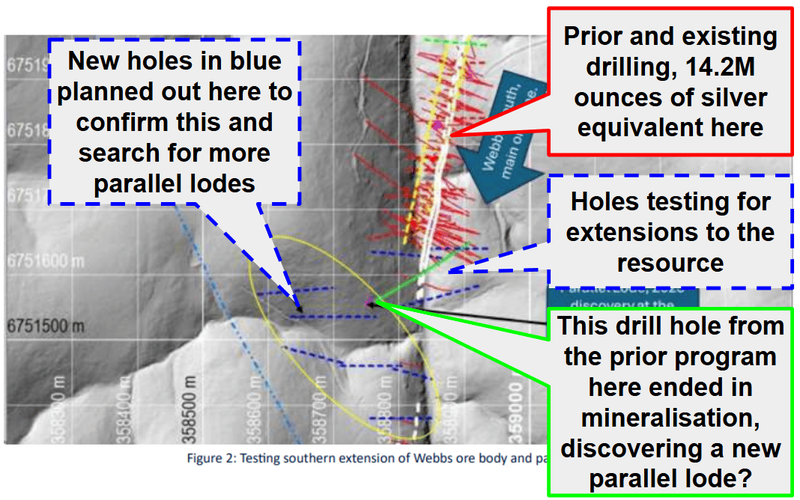

RCM’s initial drill program is designed to do two things:

- Test extensions of the new parallel structure - southern corner of the project

- Extend the existing resource - along the south

The best part is all of the drilling will come from different angles to that first program.

So we will definitely learn a lot of new things about the project this time around:

(source)

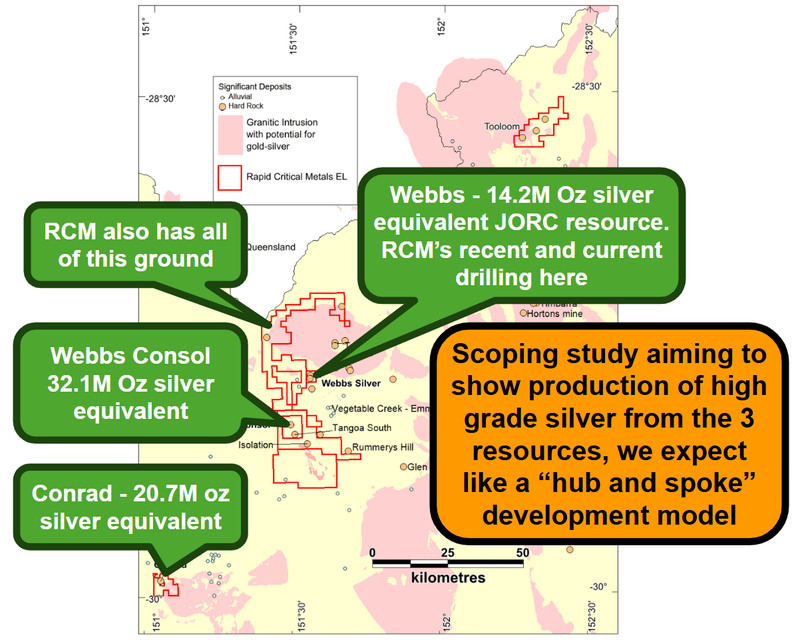

RCM also has a scoping study incoming

While we wait for drill results another thing we are looking forward to is the scoping study RCM is doing across all three of its silver projects in NSW.

RCM started the study in late January 2026 and it’s targeted for completion this quarter (source).

(this quarter ends June 30 - so the study is due any week now.)

Because all three of RCM's silver projects sit fairly close to each other, the study is looking at a model where the company processes all three projects ore at one central facility.

(source)

We think the scoping study could be a catalyst because so far, RCM has been valued as an explorer.

The market hasn’t really been given any sense of the economics of a potential mining operation across the three projects.

The scoping study will be the first time RCM publishes a meaningful look at how its three NSW silver projects might actually be developed and what they might be worth in NPV terms.

We should also see some numbers on operating costs and CAPEX.

The two numbers we'll be looking out for from the study:

- The CAPEX number - how much it costs to build the project

- The NPV - and especially the sensitivity tables at different silver prices

And of course the sensitivity of the project to silver prices (how the NPV changes with higher silver prices).

RCM will probably have to plug in a conservative price assumption to their model - but if we can see the sensitivity tables we can start to see what the economics look like at Eric Sprott’s predicted US$300 per ounce silver price.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

RCM is going for a 100M ounce silver equivalent resource base

As mentioned earlier, RCM had three projects with a combined 67M ounces of silver equivalent JORC resources:

(source)

RCM’s plan is to grow the resource across the projects with more drilling and/or land acquisitions.

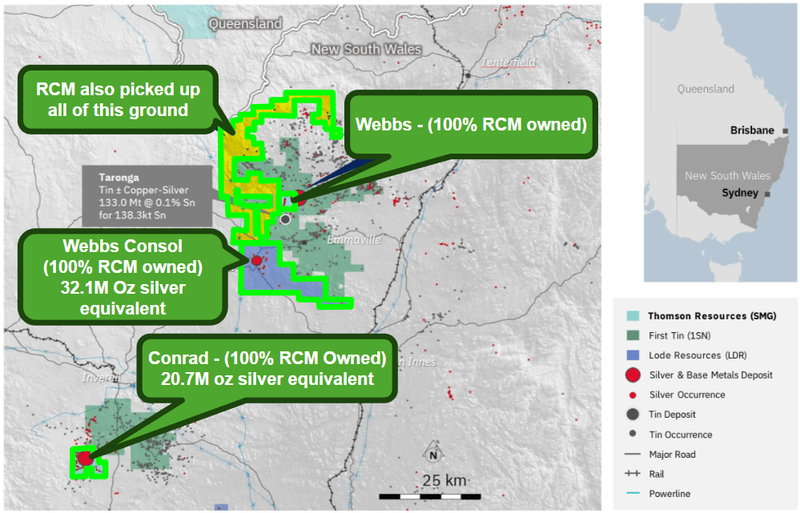

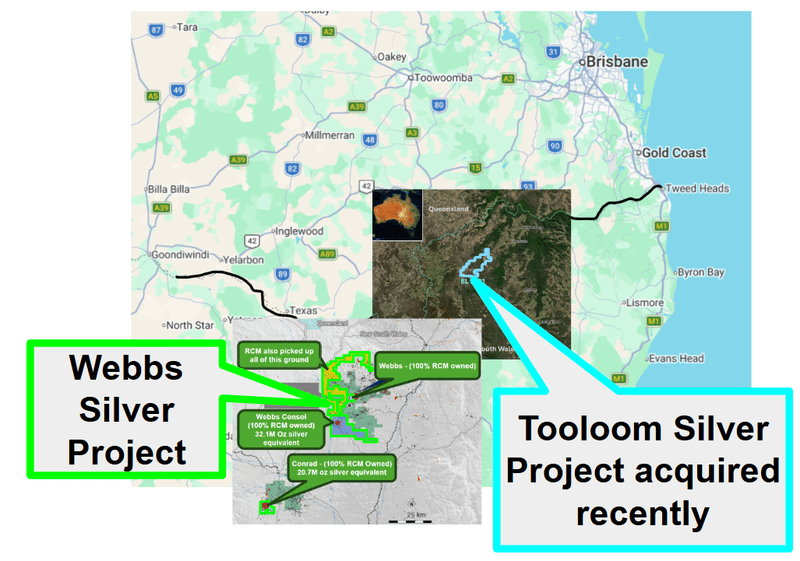

In April RCM acquired an 80% interest in another asset ~100km north-east of its existing NSW projects. (source)

That new asset has rock chips up to 1,660g/t silver, 80 historic silver workings across 21km of strike and mining activity between 1887 and 1925.

None of which has been drilled before.

Today, RCM added another bit of ground - the natural extensions to its Webbs project - a solid move ahead of the drilling to the south.

IF anything big is hit to the south - RCM will have already locked up the ground in that direction.

Here is everything RCM holds:

(source)

10 reasons why we Invested in RCM

Below are the key reasons why we Invested in RCM from our initiation note on 17th September 2025.

1. RCM has an estimated 67M ounces of high grade silver equivalent JORC resource estimates. We think it can grow bigger.

Across all its nearby projects, RCM will have an estimated ~67M ounces of high grade silver equivalent JORC resources.

With capital to put into drilling now, we think RCM can multiply this resource with new discoveries and by extending its existing discoveries.

🚨UPDATED: RCM’s target is to get to 100M ounces of silver equivalent resources (JORC resource estimates). (source)

2. We like silver

Silver is now at 14 year highs, and we think it’s about to go on a once in a generation run to new all time highs (no guarantee of course).

🚨Update: When we first Invested in RCM the silver price was ~US$42 per ounce.

Now silver is trading at US$76 per ounce.

3. There are very few silver exposures on ASX

There are very few silver names on the ASX. If silver runs, there could be a lot of capital chasing silver exposure in only a handful of names. This scarcity could mean valuations run from where they are now.

4. Silver stocks on the ASX (like RCM) are cheap relative to other exchanges

We think silver is misunderstood on the ASX and as a result, silver companies are not being valued in line with peers on North American exchanges.

We think that a big silver bull run could change that very quickly.

5. RCM is relatively cheap compared to other ASX listed silver stocks

RCM trades at an EV/silver equivalent JORC resource estimate of ~$0.38 (following the settlement of RCM’s latest acquisition).

NSW peer Silver Mines trades at a ~$1 per silver equivalent ounce.

This is before any of the exploration upside is factored into RCM.

🚨Update: RCM now trades at an EV/silver equivalent JORC resource estimate of ~$0.466.

Silver mines currently trades at an EV/silver equivalent JORC resource estimate of ~$0.968.

6. We are Investing alongside Tribeca, Jupiter Asset Management and Eric Sprott

We have had success Investing alongside Tribeca (with Locksley Resources) and Jupiter Asset Management (with Mithril Silver and Gold).

Eric Sprott is also one of the most well known silver investors in the world.

We are following them all into RCM.

🚨Update: Eric Sprott has increased his stake in RCM with ~$1M in buying on market at ~7c per share.

He now owns 10.79% of RCM himself.

7. We know two of RCM’s projects really well

We were previously Invested in RCM’s Webbs and Conrad projects through a previous Investment (TMZ) which we held when silver was <US$25 per ounce.

TMZ back then hit a market cap >$50M.

Unfortunately, TMZ made a few errors and the company ended up suspended for years, and despite an attempted re-listing, it eventually sold its assets to RCM for a $6.5M cash and shares deal. We still hold a position in that unlisted vehicle now called SMG (ex TMZ) but unfortunately not sure what will happen to that.

Now with silver at US$42+ per ounce we think the same assets could be valued much higher in the current corporate vehicle (RCM).

8. We like the recent acquisition RCM completed

RCM just acquired a neighbouring deposit, adding a 32M ounce silver equivalent JORC resource estimate to its overall resource base.

9. Exploration upside (project area now 26x bigger)

We like the recent addition of ground around the newly acquired asset and RCM’s existing Webbs deposit.

The project area is now ~26x bigger and RCM will fully own the geological trend in between its two deposits.

None of this area has been drilled systematically - RCM plans to change this over the coming months.

10. Critical Metals “Side asset” in Canada could also come good

RCM also owns 100% of a germanium/gallium project in Canada. The project is at a very early stage, but previous drill holes have shown some of “the highest germanium grades globally”.

We didn’t Invest in RCM for this asset, however it could become a dark horse in RCM’s Portfolio of projects.

Ultimately we are hoping the reasons above contribute to RCM delivering our Big Bet as follows:

“RCM expands its existing silver resource through new discoveries into a silver bull market and re-rates by over 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RCM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for RCM?

🔄 Webbs drilling

With the first of two rigs now turning at Webbs, we want to see RCM extend the existing resource at Webbs to the south.

And drill out the parallel structure theory.

The ideal scenario would be a confirmed NEW discovery to the west and extensions to the existing resource to the south.

🔄 Target generation on newly acquired asset

On the asset RCM acquired today we want to see the company complete LiDAR surveys, surface sampling and geophysics.

Ultimately, we want to see the historic results validated and then a bunch of drill targets ranked from most interesting to least ahead of a drill program on the project.

🔄 Scoping study at Webbs project in NSW

We want to see RCM complete a scoping study for its projects.

🔄 Conrad and Webbs Consol resource upgrades

We want to see RCM grow the existing JORC resources at both its Conrad and Webbs Consol silver projects through step-out and infill drilling.

What are the risks?

The biggest risk for our RCM Investment right now is "exploration risk".

RCM just got its 15,000m drill program underway.

There is no guarantee that any of it returns economic results.

Poor exploration results would negatively impact RCM's share price especially with the amount of capital that would be spent on a two rig, 15,000m program.

Exploration risk

There is no guarantee that RCM's upcoming drill programs are successful. RCM may fail to find economic silver resources, in which case we would expect the share price to re-rate lower.

Source: "What could go wrong" - RCM Investment Memo 17 Sep 2025

Other Risks

Like any early-stage exploration company, RCM carries significant risk, here we aim to identify a few more risks.

With a 15,000-metre drilling campaign underway, RCM is facing a period of high cash burn to fund its multi-rig operations.

This aggressive exploration schedule means the company may require further capital raises in the future, risking shareholder dilution.

The upcoming scoping study will outline the project economics, including expected development CAPEX and ongoing operating costs. If these figures are higher than the market anticipates, it could heavily impact the projected net present value of the assets.

RCM's ambitious target of building a 100-million-ounce resource is highly dependent on favorable silver macro trends.

A sharp downturn in global silver prices would significantly harm the economics of a potential mining operation and compress the company's valuation.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RCM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our RCM Investment Memo where you will find:

- What does RCM do?

- The macro theme for RCM

- Our RCM Big Bet

- What we want to see RCM achieve

- Why we are Invested in RCM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.