PUR hits higher grades, deeper below existing resource

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 63,058,856 PUR shares and 6,571,428 PUR Options, and the Company’s staff own 533,334 PUR shares at the time of publishing this article. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time.

Today, our small cap exploration company Pursuit Minerals (ASX:PUR) announced the completion of its first deep drill hole on its lithium brine project in Argentina.

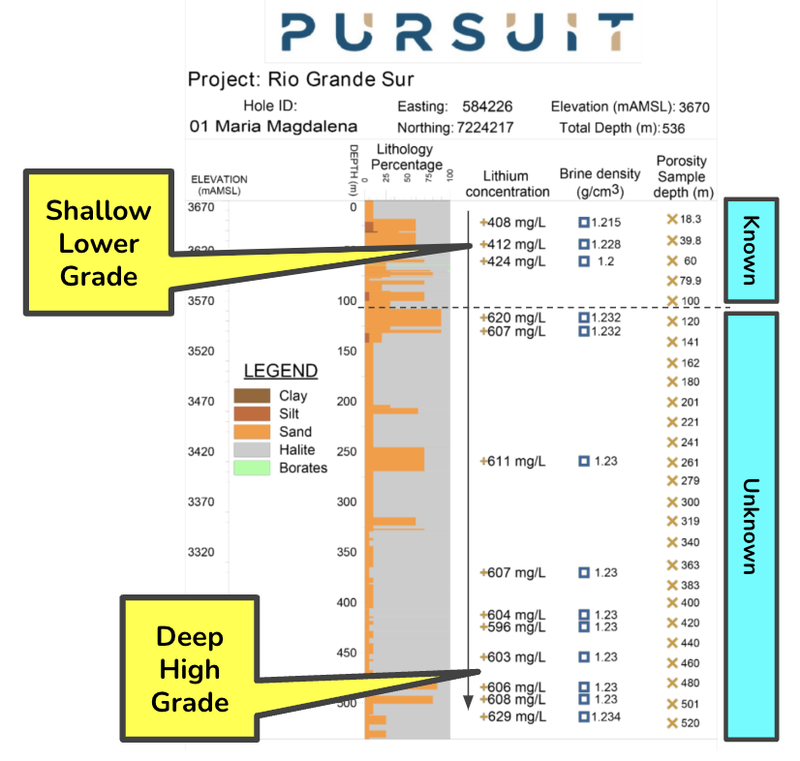

Today’s drill results demonstrated 600 mg/L averages from 115m all the way down to 555m.

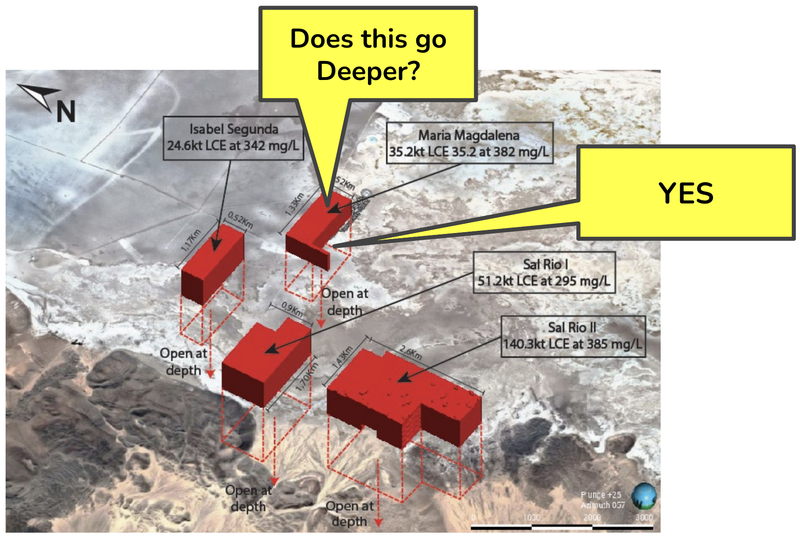

PUR already has an existing JORC resource at its project of 251.3 kt @ 351 mg/L, but that was only from historical shallow drilling to depths of 100m.

PUR wanted to test the theory that there is higher grade lithium deeper down - so it drilled a hole 560m deep.

Turns out yes, PUR has hit high-grade lithium underneath the area of already known mineralisation.

That JORC resource is now expected to grow in size, with higher grades.

And there’s a second hole which is about to be drilled as the crew shifts to the new drill location.

The kicker here is that PUR already has a lithium carbonate extraction pilot plant (that they acquired last year) and reckon that first samples will be produced in the coming months.

(on full ramp up this plant can produce 250 tonnes of lithium carbonate per annum.)

PUR also says that offtake discussions are advanced with multiple requests for product samples from potential offtake partners.

Now we just need PUR’s next drill holes to deliver some more exceptional results to lead to a material upgrade to PUR’s JORC resource.

The JORC resource upgrade is due by the end of the year... a rebound in the lithium price at the same time would be very helpful...

PUR recently completed a capital raise so they have the money to execute on the forward work program.

PUR is now capped at less than $11M after a $2.5M capital raise at 0.35c a couple of weeks ago.

(we participated in this placement at 0.35c to average down our Initial Entry Price into PUR in anticipation of an eventual lithium rebound in the medium term - with tax loss selling PUR is now trading at 0.3c).

Here’s why today’s “600 mg/L” lithium concentration result is interesting when compared to other Argentine brine projects:

- In June 2024, the Solaroz Lithium Project in the Olaroz Salar approx. 200km north of PUR was acquired for US$63M ($98M). Solaroz holds a JORC resource of 3.3mt LCE at 305mg/L.

- In December 2023, Argentine company Tecpetrol, a company led by Argentine billionaire Paolo Rocca acquired TSX listed Alpha Lithium whose main asset was the Tolilar Project approx. 50km north of PUR for $230M USD / $350M AUD. Tolilar holds an Ni 43-101 (foreign) resource of 2.1mt LCE at 242mg/L.

- Earlier this month it was reported in the AFR that Cleantec Lithium Plc was looking to list on the ASX via a $20M raise on a $100M valuation. Cleantec’s main project Laguna Verde holds a resource of 1.8mt LCE @ 208mg/L with grades up to 409mg/L.

PUR is capped at $11M - just a small fraction of the valuations mentioned above.

Whilst its early days for PUR with only one deep hole drilled, it is already yielding higher grades than all 3 projects supporting 100 million+ market caps / valuations.

Granted, this is only the first deep hole for PUR - and we would ideally want to see some thicker intercepts with those high grades to make things even more interesting - but what the above does show is the valuations that can be achieved with Argentinian lithium companies, even in a down market for lithium.

(we hope that by the time PUR finishes its drill campaign and hopefully delivers a materially upgraded JORC resource, that broader lithium conditions will have improved)

Context on today’s PUR drill results

So today’s news is what we wanted to see from the first deep drill hole, confirming the theory that PUR’s lithium project extends even deeper with higher grades.

Last year, PUR published a maiden JORC resource estimate of 251kt of Lithium Carbonate (LCE) at 351mg/L.

With no drilling done themselves.

This resource was based on shallow historical drill holes (down to around 100m) and geophysical surveys conducted over the project.

Earlier this year PUR commenced a 4 hole diamond drill program (which has now been extended to 6) with the goal to grow the size and grade of this resource.

PUR’s theory was that lithium mineralisation existed deeper in the project, at a higher grade.

Previous lithium projects in the area had similar stories, where lower-grade lithium existed closer to the surface and the high-grade good stuff was buried deeper below.

Today’s drilling results confirmed this theory with mineralisation extending at depth AND at a higher grade than the existing JORC resource.

The PUR backstory

PUR’s ground sits within the South American “lithium triangle”, which is home to some of the biggest lithium companies in the world and around ~60% of the world’s lithium reserves.

Specifically, PUR is located in Argentina - where president Javier Gerardo Milei has made supporting the lithium industry a focus of the country:

PUR’s project sits across a ‘salar’, or ‘salt lake’ in English.

These salars are the basis of the South American Lithium Triangle.

When it comes to brine projects, lithium grade is one of the key factors in determining their economic viability.

The higher the grade, the less volume of brine is needed to extract the same amount of lithium, which reduces the overall cost of production.

With the current drilling, PUR is looking to emulate what other companies have done on salars across Argentina - drill deeper looking for higher grade, thicker lithium brine reservoirs.

We’ve seen it play out before:

- Pastos Grande Salar: At Pastos Grande, holes drilled down between 90 and 180m had average lithium grades of 538mg/L. Holes drilled down to 365 to 620m depths had average lithium grades of ~641mg/L.

- TSX listed NOA Lithium: The project sits to the north of PUR and it intercepted lithium grades of ~433mg/L at depths of around 100m. Then after drilling to depths of ~300 to 400m started hitting grades of ~773mg/Li to ~925mg/L (source).

Today, PUR also proved that higher grade lithium existed at depth across its project with its first drill hole.

It found lithium at an average grade of ~600mg/L at depth - while its JORC resource sits at just 351mg/L.

There’s more drilling to come

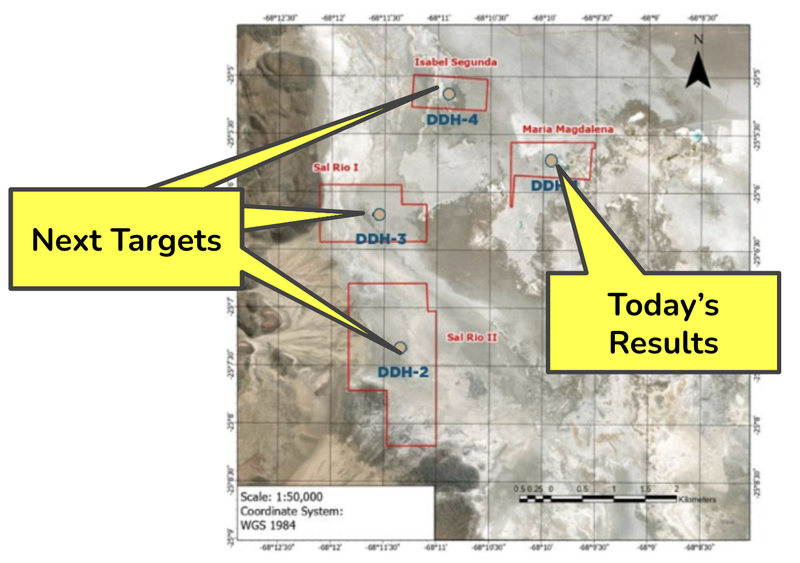

PUR still has three more targets to drill to test the mineralisation at depth and we are hoping to see similar (or better) results from these next holes.

Each hole sits on a different tenement, where PUR has licenses to explore for lithium:

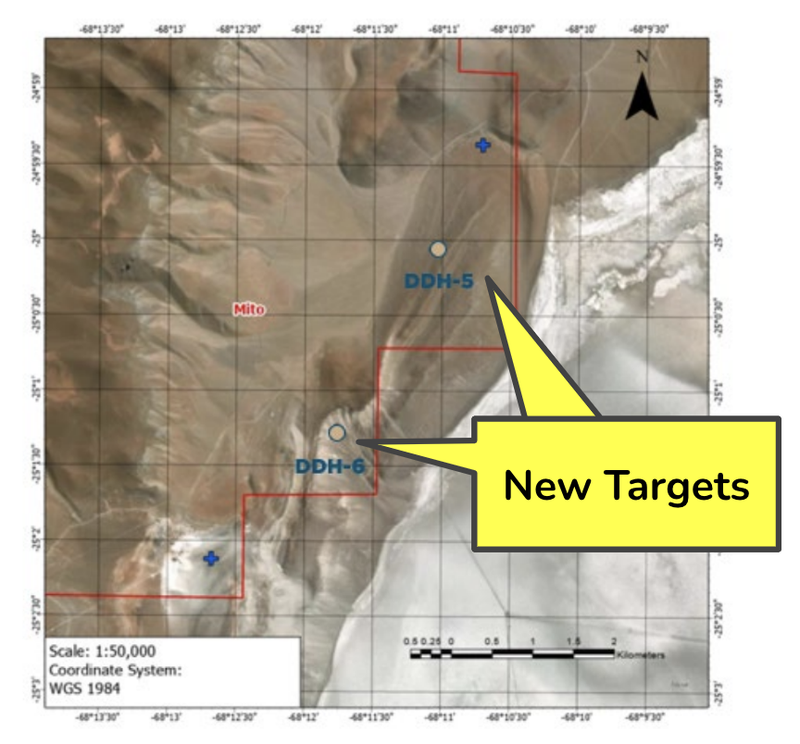

In a recent announcement PUR also noted that it will drill two more wells at its bigger exploration tenement just off the salar, called Mito:

Holes 5 and 6 at Mito are slightly different to the first four.

Where the first four holes sit on known lithium mineralisation (where PUR is looking to extend the resource at depth) these holes sit in areas of unknown mineralisation and outside of the JORC resource.

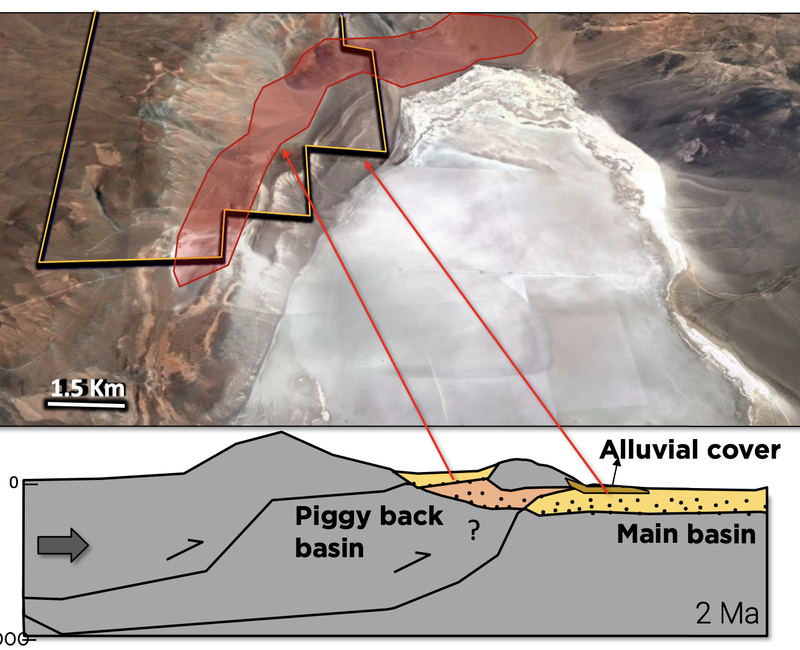

These holes are to test a “sub-basin” theory - that lithium exists at the margins of the salt lake.

This theory has been tried and tested across other salt lakes in South America’s lithium triangle, delivering additional lithium resources for those successful.

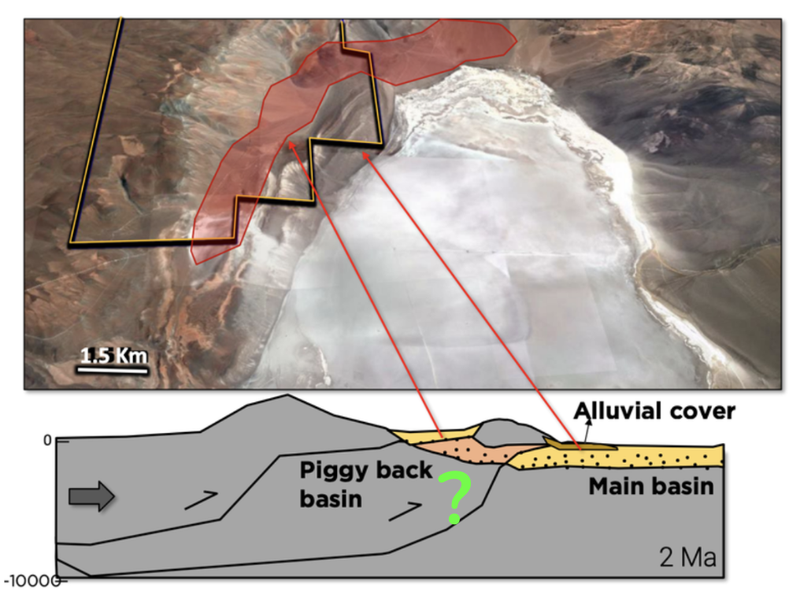

It involves drilling on the edges of a salt lake to see if the lithium aquifers extend deep underground in what is called a “piggyback basin”.

We view the “sub-basin theory” as the unexpected blue sky exploration equivalent for PUR.

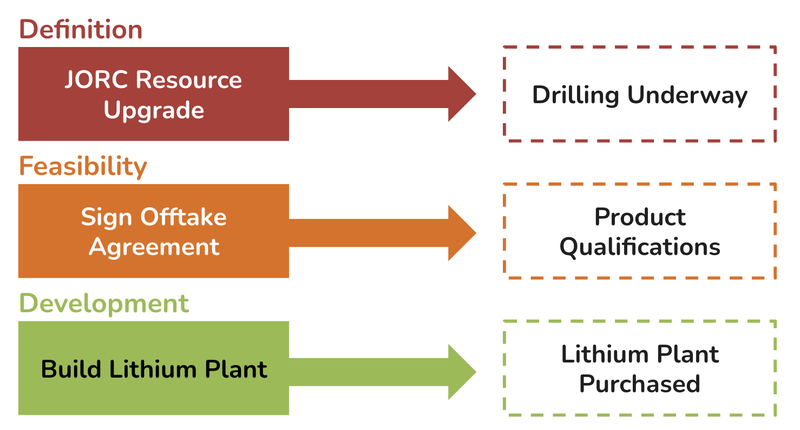

PUR aiming for JORC resource increase

PUR is trying to grow the size of its resource and fastrack its project through to development studies and ultimately, production.

The goal of this drill program is to gather valuable information about the lithium concentration of the project at depth.

PUR will use this information to publish and upgrade on its JORC resource, which we hope is published by the end of the year.

With a bigger resource, PUR will be able to set a benchmark from which the market can start to compare its project to other South American lithium brine players.

This will allow it to hopefully attract more capital at increasing higher valuations - like its peers.

IF PUR’s resource is big enough, we expect the company to move quickly towards development studies with the goal of becoming a lithium producer.

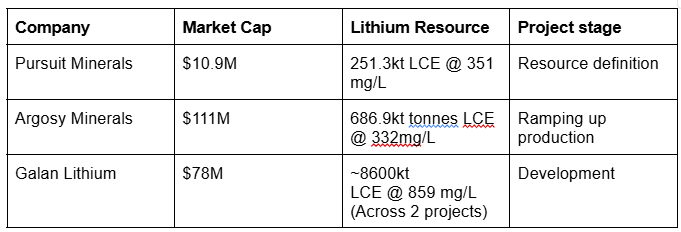

At the moment here is how PUR compares to two of its ASX-listed peers:

Growing the size and grade of its lithium resource is a key part of the PUR story, and we will be keeping a watch out on the JORC resource upgrade due at the end of the year.

Can PUR secure a buyer for its lithium?

While PUR is developing its resource, it is also looking to source an offtake agreement.

An offtake agreement is used by resource companies to sell a portion of the future production of the project, which helps provide potential financiers confidence in future project revenues.

PUR has already received multiple requests for product samples from potential offtake partners.

PUR has already purchased a lithium processing plant that on full ramp up can produce 250 tonnes of lithium carbonate per annum.

This is the first significant step in the development of a larger commercial operation.

PUR’s goals in sequence here are to:

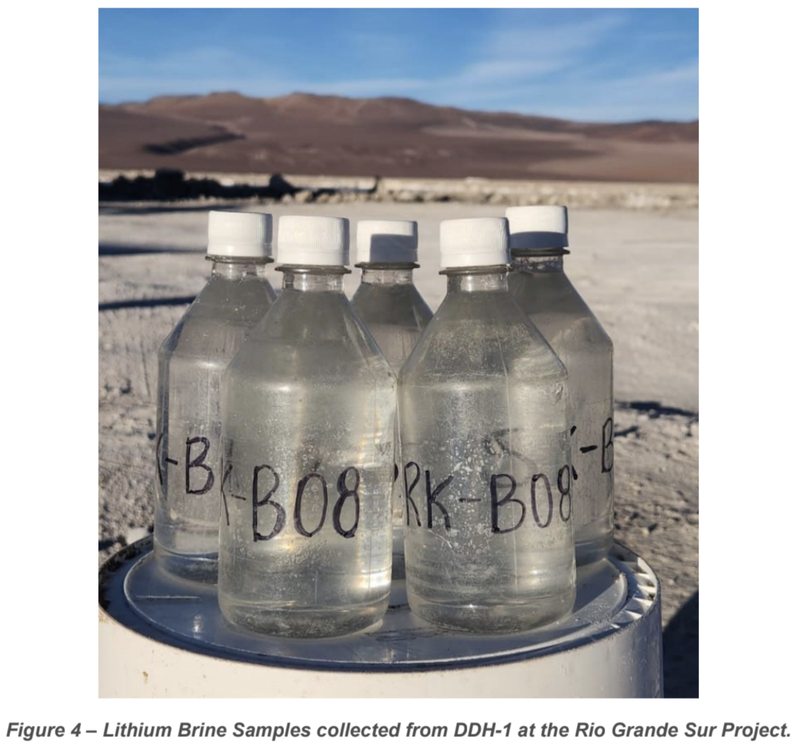

- Produce an initial sample batch using synthetic brine of approximately 50-10kg of product.

- Then evaporated brine, currently being sourced from the Stage 1 Drilling Program (you can see samples in the photo below) will be utilised to produce approximately 2 to 10 tonnes of Lithium Carbonate products, which is anticipated to be battery grade product.

- After this, PUR will consider relocating the Pilot Plant to site following the completion of construction and filling evaporation ponds to provide feed for the plant.

That sample lithium carbonate product can be used for product specifications and qualifications with offtakers.

Here is how PUR is advancing along the various milestones on the pathway to production:

This brings us to our Big Bet for PUR...

Our PUR ‘Big Bet’

“PUR increases the size and scale of its lithium project to a level that warrants putting it into production. We are hoping this re-rates the company to a market cap of >$1bn”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PUR Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

A deeper look into PUR’s drilling program

Today, PUR announced lithium concentrations from the deeper parts of its project.

The results were from 115m all the way down to 555m PUR had average lithium grades of around 600mg/L.

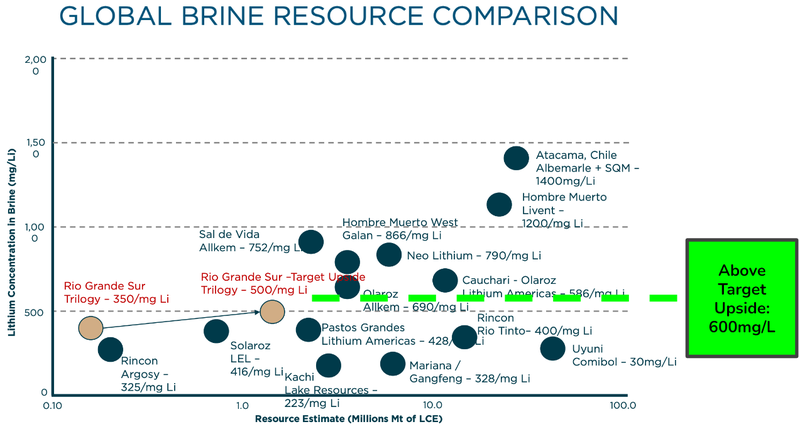

If you look at this chart put out by PUR in March last year, around the time that the company acquired the project, a resource of 600mg/L is well above the target upside set by the company at the time:

(Source)

It is important to note that these results only represent drilling over one part of PUR’s project; it will need to continue to find high-grade lithium at depths to upgrade its lithium resource at 600mg/L.

But, this is a very good start.

Key highlights from the results announced today include:

- High grade brine extends through to 555m.

- Between 100m and 130m a highly porous sandy unit was identified with very high-grade lithium. This could be the potential zone for a future pumping well. (This will become more relevant later down the track as PUR moves through to development studies).

- Still three more holes to be drilled to test the resource at depth.

- Still two more holes to test the “sub-basin” theory on PUR’s largest tenement.

PUR has been working on this drilling campaign for almost twelve months now.

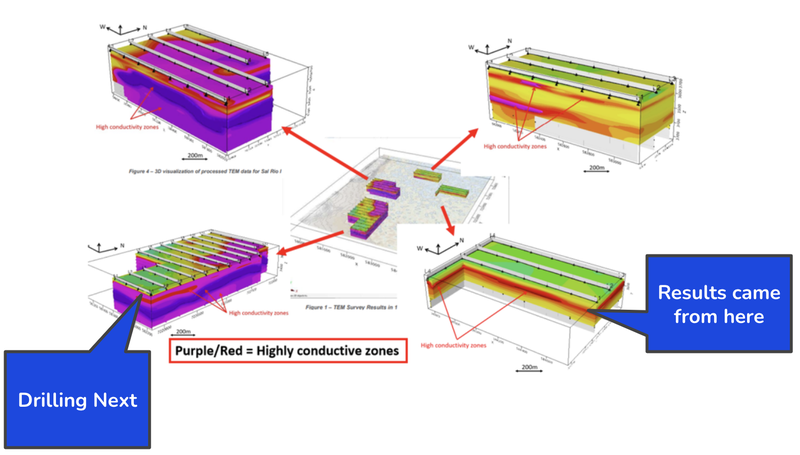

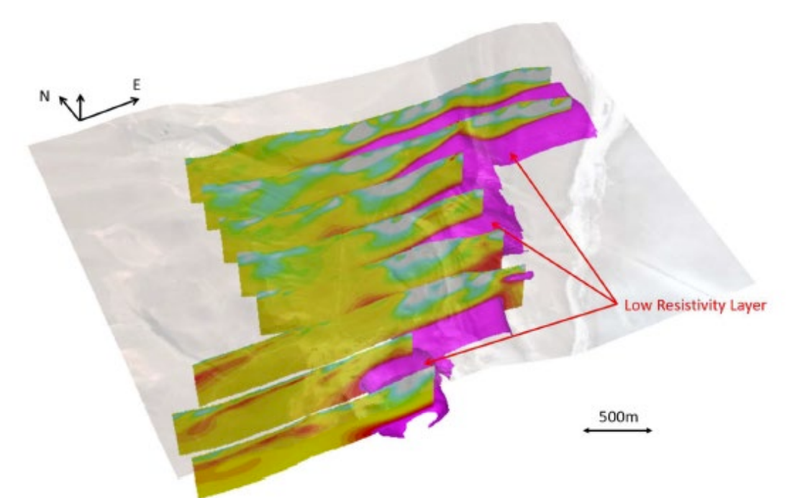

PUR first ran geophysical surveys (TEM and CSAMT) to try and work out what is going on underneath its ground.

The key objective with the geophysics was to try and find areas of high conductivity - The more conductivity at depth is ultimately a sign of where PUR is more likely to find lithium brines underground.

The first batch of data showed that there were high conductivity layers at depths well below the 200-300m mark:

These results came from the Maria Magalena tenement, which had a TEM profile that is typical of a “Salar Core”.

PUR’s next target is located on the margin of the Salar and the TEM profile also indicated a thick conductive layer (the deep purple bit).

Both are prospective for lithium brine.

But, as we know in mineral exploration there is only one way to find out... and that is to drill it.

Now that PUR has shown that its first target extends at depth we are hoping it is able to do so for the next three.

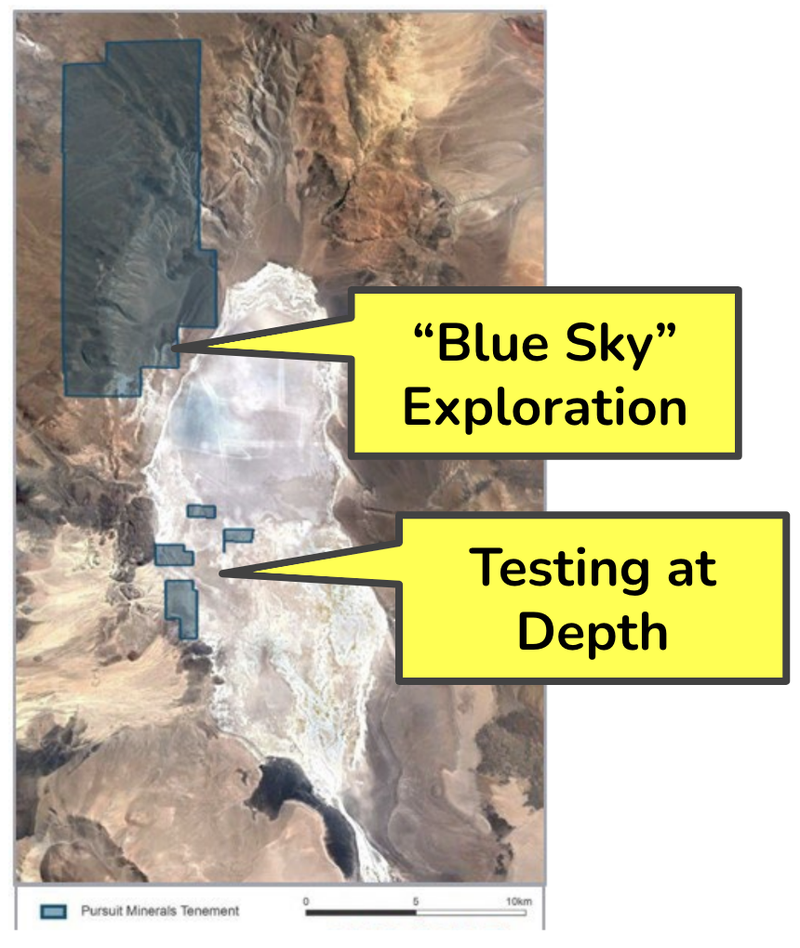

These targets sit as part of PUR’s existing JORC resource, but it also has two other targets that sit outside of the JORC resource which have “blue sky” potential.

Here is where PUR’s blue sky potential exists:

PUR’s largest tenement is least likely to have lithium, because it is not in a known area of the Salt Lake.

PUR has a theory that there could be a “piggyback basin” that has been obscured by rock sediment called an ‘alluvial cover’.

PUR ran geophysical studies on this area that showed at depth, there was potential for PUR to find even more lithium brines.

If PUR is able to find lithium here we think it is a big upside case that the market has yet to factor in.

Ultimately, these drilling results are a very good starting point for PUR and we hope lead to strong follow up results and eventually a maiden resource upgrade at the end of the year.

More on PUR’s Pilot Plant Production Facility

In May last year PUR acquired an existing lithium plant.

The cost of the acquisition was less than ~US $365K and it cost the original owners over ~US $3.6M to build.

Here are some photos of the facilities:

In March this year PUR updated the market with its plans for the plant, which was to produce an initial 2 to 10 tonnes of battery grade lithium carbonate from the samples used in the current drill program.

Once fully commissioned, the pilot plant should be able to produce at a rate of ~250 tonnes of LCE per annum.

The purpose of these initial samples are for use in offtake, where PUR has mentioned that it has received “several expressions of interest”.

Offtake agreements can and do take time, however we think that PUR is doing all of the right things to prepare its project for an offtake agreement should it build a big enough resource and at a high enough grade to justify moving through to production.

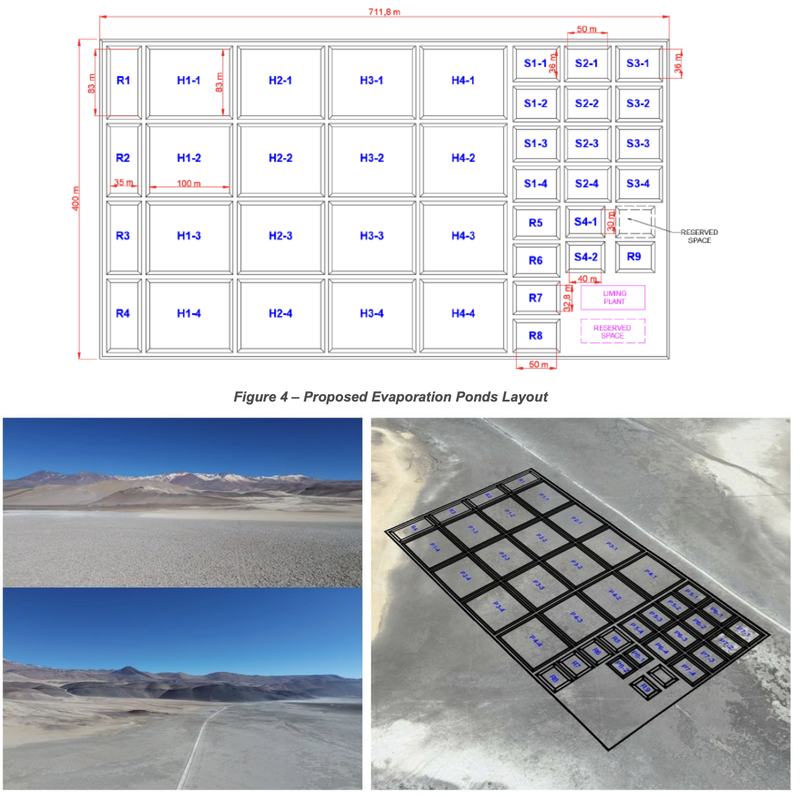

In that announcement PUR also gave us a first look at its development strategy, with proposed evaporative pond locations for the project.

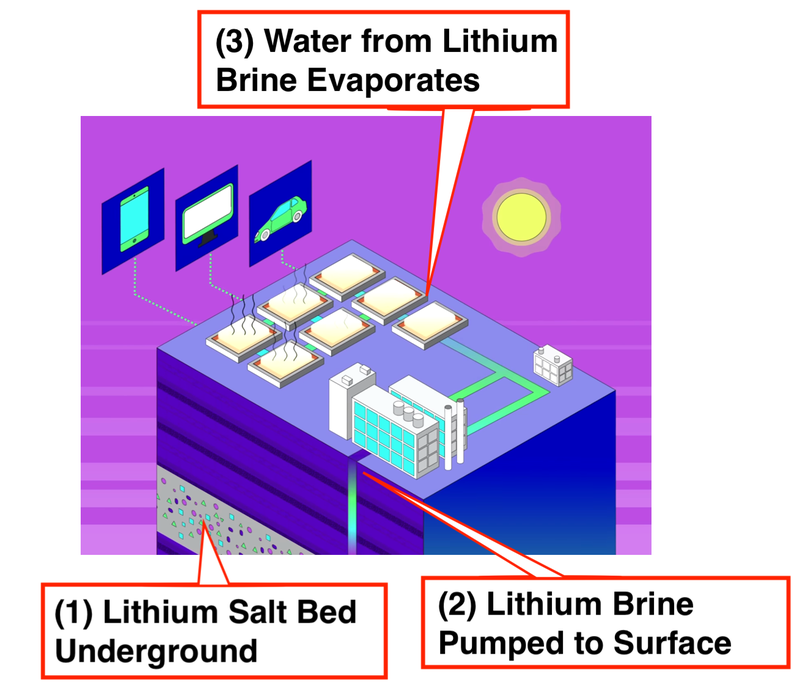

Unlike hard rock lithium projects, which are more akin to traditional mining, PUR’s project is a brine-based project.

Instead of being found in pink spodumene cores, the lithium exists deep underground in an aquifer (underground water) that needs to be pumped up to the surface.

This brine is then spread across things called evaporation ponds and then, in the hot arid conditions only available in South America, the water evaporates away leaving just the valuable lithium.

Here is what it looks like:

If you would like to learn more about brine projects read: The different types of lithium projects explained.

Although it is nice for investors to get a sneak peak into the development scenario for PUR, it is still very early stages for the company and the key focus is on upgrading the JORC resource.

That said, it does show the intent from PUR’s management to move quickly towards production on all aspects of the mining feasibility journey.

What’s happening with lithium in Argentina?

We think Argentina is one of the best places to be developing a lithium resource right now.

Traditionally, lithium has come from only a select few jurisdictions - Chile, Australia, China.

But Argentina is rapidly positioning itself to become one of the next major lithium producing countries along with Brazil.

As we highlighted higher up, i’s leading to some interesting transactions and proposed transactions for Argentinian lithium companies - all at significant premiums to PUR’s current market capitalisation:

Transaction #1: In June 2024, ASX-listed Lithium Energy’s Solaroz Lithium Project in the Olaroz Salar approx. 200km north of PUR was acquired for $US63M ($98M).

Solaroz holds JORC resource of 3.3mt LCE at 305mg

Transaction #2: In December 2023, Argentine company Tecpetrol, a company led by Argentine billionaire Paolo Rocca acquired TSX listed Alpha Lithium whose main asset was the Tolilar Project approx. 50km north of PUR for US$230M ($350M).

Tolilar holds an Ni 43-101 resource of 2.1mt LCE at 242mg

Transaction #3 (proposed): Earlier this month it was reported Cleantec Lithium Plc was looking to list on the ASX with and indicative market cap of $100M. Cleantec’s main project Laguna Verde holds a resource of 1.8mt LCE @ 208mg/L with grades up to 409mg

Obviously PUR has a lot of work to do to catch up to these companies on a resource and valuation basis - but it does show the valuations that can be achieved with Argentinian lithium companies, even in a down market for lithium.

Here’s what we’re looking for next from PUR...

What is next for PUR?

🔄 Maiden Drill Program

PUR still has five more targets to drill under this program. Here are the milestones we see the company achieving over this time:

✅Drill first target

✅Results for first target

🔲Drill targets 2, 3 and 4

🔲Results for targets 2, 3 and 4

🔲Drill targets 5 and 6

🔲Results for targets 5 and 6

Note, in order to maintain the resources for drill targets 5 and 6 PUR decided to delay the pumping well to test brine flow rates.

This pumping well is an important part of the PUR story and will be part of the second drilling program.

🔲 Publish an Upgraded JORC Resource

PUR has already published a maiden JORC resource estimate of 251kt of Lithium Carbonate (LCE) at 351mg/L.

It also has a foreign resource estimate of 2.1Moz of LCE at 370mg/L.

We want to see PUR upgrade its JORC resource by the end of the year.

🔄 Commission Pilot Plant & Offtake Agreements

PUR has mentioned that they are in discussions with potential offtake partners.

We want to see the company commission between 2 and 10 tonnes of battery grade lithium carbonate for qualification purposes and offtake agreements.

🔲 Environmental Permitting

PUR requires environmental permits to construct its evaporative ponds on site. Successfully getting these permits will be a big milestone for PUR.

What could go wrong?

Resource Definition Risk

Drilling and defining a JORC Resource is always risky.

It is possible that PUR fails to deliver any good drill results, or find higher grade lithium at depth, from its current round of drilling and cannot improve the JORC resource above the 2.1Moz foreign estimate over the project.

Commercialisation Risk

Lithium brine projects are highly dependent on different variables like weather, flow rates to surface and the variability of grades in the brines.

There is always a risk that PUR’s project doesn't meet the levels required for its project to be operated commercially.

Funding / Dilution Risk

For PUR, this risk materialised.

Volume on the stock and the company’s share price has dwindled over the six months and with the company unable to deliver any material results before running out of capital.

PUR raised A$2.5M at 0.35 cents with a two for one option, which was well down from the 1.8 cent raise done twelve months ago diluting existing shareholders (like us).

However, now that the company has more cash in the bank and with more drilling on the horizon, we are hoping that the company can now deliver some material results to re-rate the share price upwards.

How does today’s PUR news impact our Investment Memo?

Today’s news is positive in terms of one of the key reasons we Invested in PUR, in that the drilling at depth confirmed that there is plenty of exploration upside at PUR’s project:

Exploration upside

Most of the drilling in the Rio Grande salar (salt lake) has been down to depths of ~100m. Lithium mineralisation is interpreted to extend down to depths of ~500m in depth leaving plenty of exploration upside for PUR to chase.

Commodity price risk

Lithium is currently trading at all time-highs. There is always a risk that the market interest for lithium decreases and in turn appetite to invest in companies like PUR decreases.

Unfortunately we’ve seen lithium prices shed ~80% of their peak value since we Invested in PUR, which is likely contributing to the prolonged decline of PUR’s share price and is an example of commodity price risk materialising.

We try to participate in placements during down-cycles to average down our entry price in anticipation that commodity prices will cycle up again eventually.

Our PUR Investment Memo

Along with the key risks, our PUR Investment Memo provides a short, high-level summary of our reasons for Investing.

The Investment Memo details:

- Key objectives we want to see PUR achieve

- Why we Invested in PUR

- What are the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.