PNN starts 10,000m rare earths & niobium drill program - maiden resource due this quarter

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,793,000 PNN Shares and 3,685,500 PNN Options at the time of publishing this article. The Company has been engaged by PNN to share our commentary on the progress of our Investment in PNN over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The US Vice President, JD Vance, last week gave a speech at the Critical Minerals Ministerial - with 50+ countries in attendance and said:

“critical minerals and rare earths are essential for our most advanced technologies and will only become more important as AI, robotics, and other emerging technologies continue to advance"

No rare earths, no AI humanoid robots...

The US needs rare earth supply and according to the US geological survey itself, Brazil has the biggest reserves outside of Asia. (source)

The US has already started funding Brazilian rare earth projects - and the media keeps hinting at a potential rare earths deal between Brazil and the US...

Brazil becoming strategically important to the US as a critical mineral hotspot is exactly what we want to see happen for our Investment Power Minerals (ASX:PNN).

PNN owns 100% of a rare earths/niobium block that covers the entirety of an interpreted carbonatite intrusive.

Carbonatites are the type of structures that host the world’s biggest operating rare earths projects.

MP Materials’ Mountain Pass mine in California is a hard rock carbonatite deposit.

Lynas’ Mount Weld in Western Australia is a hard rock carbonatite deposit.

And the mine currently responsible for producing ~80% of the world’s niobium (also in Brazil) is a hard rock carbonatite deposit...

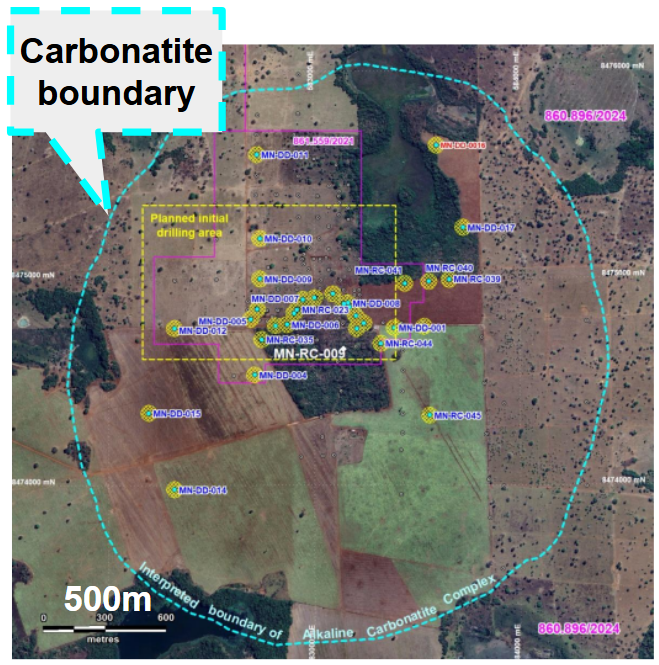

PNN holds all of the ground covering what it is interpreting as a “carbonatite intrusive complex”:

PNN has spent the last ~8 months poking shallow holes into the project, hitting intercepts like ~51m with 1.16% rare earth oxide grades (from surface). (source)

And just last week PNN started drilling with a heavier rig capable of testing targets at depth.

Over the next few months, we will have assay results from the deeper holes...

Eventually putting all of that data into a maiden resource on the project “in the current quarter”. (source)

Here are the rigs in action:

(source)

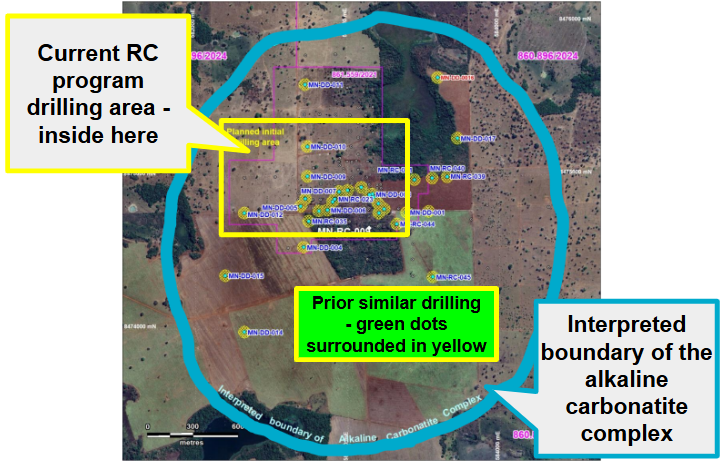

We have been looking forward to this because it will mean PNN can test for - at depth extensions to the rare earths intersected by the shallow holes...

AND we can get a better sense of what sits inside PNN’s “carbonatite complex”:

(source)

With the RC drilling we want to see PNN drill deep and extend all of those shallow hits...

So far, a large part of the ~5.8km^2 carbonatite is untested so there is potential for a substantial deposit to be uncovered IF the deeper drilling comes in.

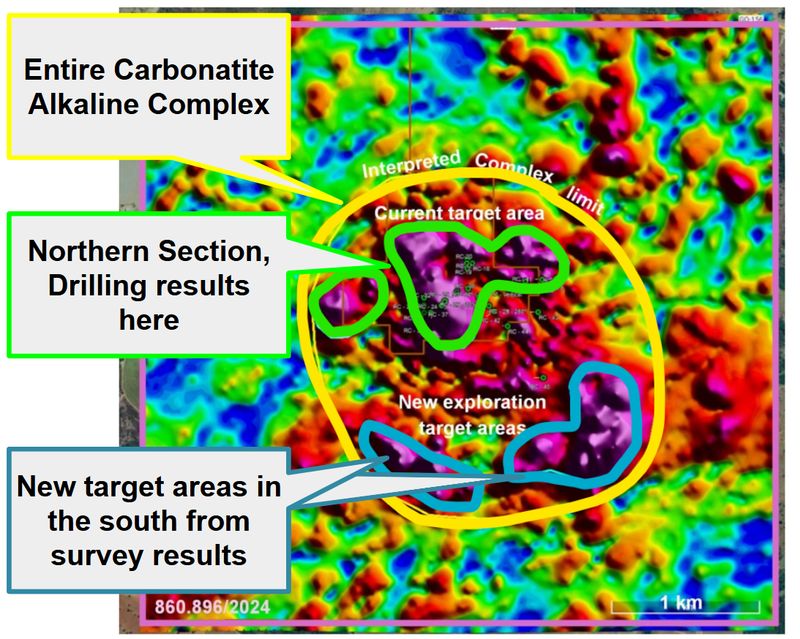

This is one of the main reasons we like this project is because, IF PNN’s exploration model is proven correct, then the company holds the ground that covers the entire carbonatite complex.

IF the drilling from the current program in the northern section comes in, PNN can move down lower into the newly mapped targets to the south to see if the rare earths/niobium sit uniformly across the whole carbonatite complex:

(Source)

We are Invested in PNN to see it emulate SGQ’s success

We have had success Investing in hard rock rare earth/niobium exploration in Brazil before.

Last year one of the best performing companies in our Portfolio was St George Mining (ASX: SGQ).

SGQ went from our Initial Entry Price of 2.5c to a high of ~18c per share late last year - up over 600% for us...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

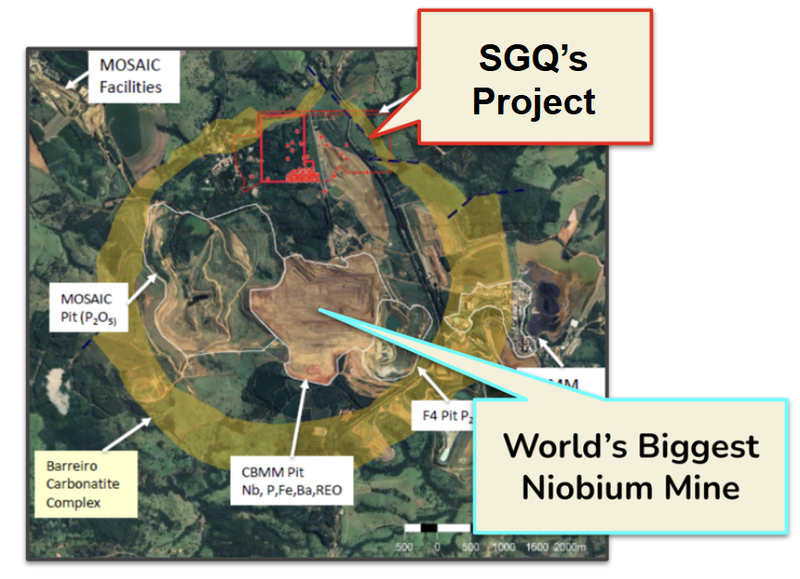

SGQ owns the largest and highest-grade carbonatite-hosted rare earth deposit in South America...

... and the second highest grade REE deposit globally in the Western world.

(SGQ even gets a mention in mainstream media articles when the topic of Brazilian rare earths/niobium is grabbing headlines) - this was from an article yesterday:

(source)

We are Invested in PNN to hopefully see it emulate SGQ’s success.

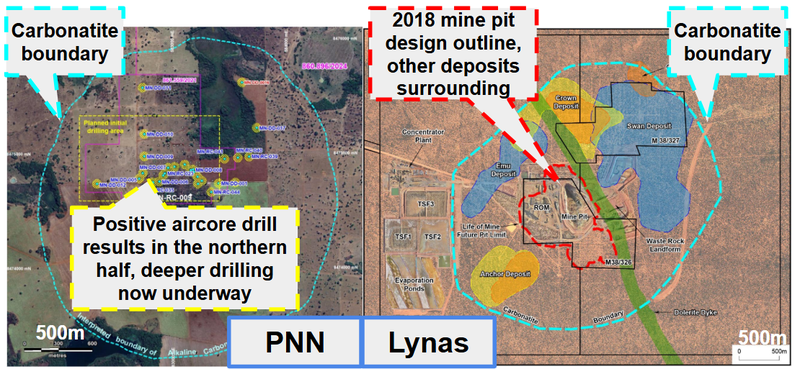

The reason we liked PNN’s project was because it sits in similar geology (hard rock carbonatite intrusive) and the group who introduced us to the project were also the ones who introduced us to SGQ.

Here is what SGQ’s project looks like (covering the northern end of the giant carbonatite that multi billion dollar CBMM is operating its mines from):

(source)

And here is PNN’s blocks covering the entire interpreted carbonatite intrusive:

(source)

SGQ’s project was a lot more advanced relative to PNN’s, and we are pretty conscious of there being a lot more exploration risk for PNN.

But IF the drilling can deliver high enough grades and the geology stacks up, we think PNN could also come good for us.

The main risks right now are grades and continuity - which is what we are hoping the current deeper drill program can de-risk.

Ultimately for PNN to achieve our Big Bet, we think the company needs to deliver strong drilling results from its Brazilian rare earths project:

Our PNN Big Bet:

“PNN makes an economic discovery on its US or Brazilian rare earths projects and re-rates 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

PNN also has an advanced stage lithium asset that we like

In our PNN initiation note back in October, we mentioned PNN had lithium assets that we thought could come good if the lithium cycle ever turns.

Since that note, lithium carbonate prices have gone from CNY~$73,000 to CNY~$160,500 (more than double):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

While we are mainly invested in PNN for its rare earth element (REE) project in Brazil...

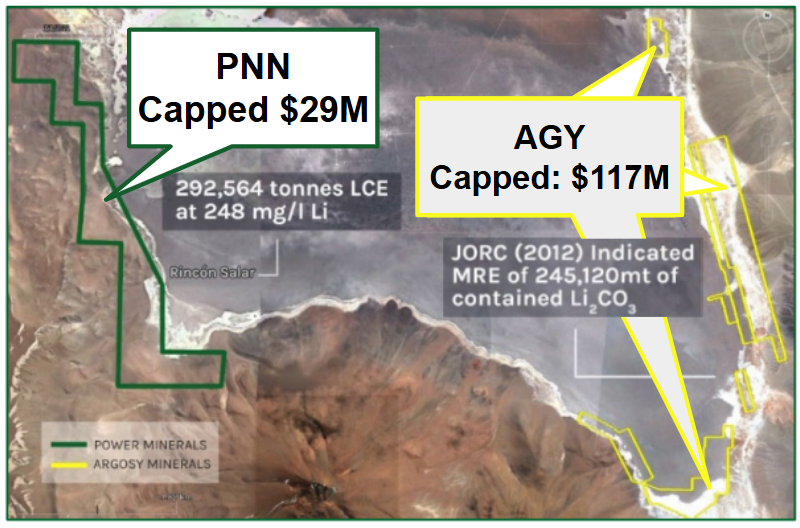

PNN’s lithium assets in Argentina have a combined 714,864 tonne lithium carbonate equivalent (LCE) JORC resource estimate.

The two most advanced are:

- (Rincon) A project in the same salar (salt lake) where ASX listed Argosy Minerals and Rio Tinto have projects - This is PNN’s most advanced asset, with a Preliminary Economic Assessment (PEA) done back in 2023 with a post-tax NPV of US$308.8M based on capital expenditure of US$216.55M.

And - A project on the eastern fringes of the Incahuasi Salar, immediately adjacent to Ganfeng Lithium Co. Ltd.’s project. That project has a 249,308 tonne LCE JORC resource estimate.

Back on January 14, PNN took back 100% control over its more advanced Rincon asset.

The project was previously under a Joint Venture deal that would have seen partner Navigate Energy earn a 59% interest in the project by investing US$4m.

The JV being cancelled means PNN now gets back to 100% ownership in the project.

And PNN confirmed that discussions are already underway “with potential new funding and development partners” to fast track the development of the project.

Including an engineering study for the project...

Here is where PNN’s asset sits relative to ASX Listed Argosy Minerals:

(Source)

Over the next few months, especially if lithium prices continue running, we could see some surprise positive catalysts out of PNN from this project too.

What’s next for PNN?

Drilling at Brazilian rare earths project

We want to see PNN run its deeper RC drilling and confirm that the rare earths and niobium continue at depth - beyond what the shallow auger drilling has defined to date. (source)

We also want to see PNN drill out and define a maiden JORC resource estimate in Brazil to enable comparison to peers, a maiden JORC resource estimate is expected this quarter. (source)

Here are the milestones we are tracking on PNN’s Brazilian rare earths project:

Milestones:

✅ Geophysics/Geochemistry work (geophysics results recently)

✅ Drilling starts (Auger drilling started, RC drilling commenced - today)

🔄 Drilling results

🔲 Maiden JORC resource estimate

Regain control of the Rincon lithium asset

PNN will now need to repay US$1M to the previous Joint Venture partner (Navigate Energy) by 28th of February to take 100% ownership of the Rincon asset.

(source)

We want to see that repayment gets made and PNN returns to 100% ownership before any other work is done on the project.

What are the risks?

PNN has drill results coming from its Brazilian rare earths project so a key risk in the short term is “exploration risk”.

The company’s Brazilian rare earths thesis relies on the geological interpretation that it sits on a large scale carbonatite intrusive.

While shallow drilling has been positive, there is no guarantee that the current deeper RC drilling will confirm mineralisation at depth or that the grades will be economic.

Carbonatites can be geologically complex, and if the "feeder system" isn't found, the scale of the project could be diminished.

IF the deeper drilling results don't return anything economic PNN’s share price could re-rate lower.

Another risk is “market risk” because rare earths stocks have been volatile over previous months.

There is a risk that a more permanent deal gets done between China and the US in the short term which eases the trade restrictions and momentum comes out of rare earths stocks.

If that were to happen PNN’s share price could be impacted negatively, especially because its projects are in the early exploration stages.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking PNN’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Source: “what could go wrong” - PNN Investment Memo 08-Oct-2025

Other risks:

Like any small cap exploration company, PNN carries significant risk, here we aim to identify a few more risks.

PNN has an immediate financial obligation regarding its Rincon lithium asset. To regain 100% control PNN must repay US$1M to its previous Joint Venture partner (Navigate Energy) by the 28th of February. PNN did hold ~A$3.75M in the bank at 31 December 2025 BUT it may need to raise more equity to make those outstanding payments.

PNN is now 100% responsible for the Rincon lithium project again.

While this offers more upside, it also means PNN bears 100% of the holding costs and development risks until a new partner is found. If lithium prices roll over or a new partner cannot be secured, the project could become a financial drain on the company.

Rare earths projects face significant metallurgical risks.

Even if PNN defines a large resource, the commercial viability depends on being able to extract the rare earths and niobium from the host rock economically. Hard rock carbonatite metallurgy can be complex and expensive compared to other deposit types.

Finally, PNN is exposed to sovereign risk in South America.

While Brazil and Argentina are currently favourable jurisdictions for mining, political and economic stability can fluctuate, potentially impacting permitting timelines or fiscal regimes.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PNN Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our PNN Investment Memo where you will find:

- What does PNN do?

- The macro theme for PNN

- Our PNN Big Bet

- What we want to see PNN achieve

- Why we are Invested in PNN

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.