PNN has started drilling its Brazil rare earths asset, with historic hits of 60m+ at 8%+ TREO. Also up to 2% MREO (the robots, AI and military ones)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,338,223 PNN Shares and 4,399,786 PNN Options at the time of publishing this article. The Company has been engaged by PNN to share our commentary on the progress of our Investment in PNN over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Two years on from export bans on rare earths - two years for western companies to work on building out new supply chains...

and China still controls ~90% of the world's rare earth magnet supply chain.

For the heaviest, most valuable rare earth elements like dysprosium and terbium, China controls ~98-99% of refined supply.

Those rare earths are the ones that go into magnets for missiles, drones, EVs, robots and AI data centres.

The US still hasn’t solved its rare earths supply chain problem.

China’s temporary pause on those 2024 export bans ends in November - not long now...

To try to find a solution, the US has turned to Brazil - home to the world's second biggest rare earth reserves (behind only China).

Here is what the Wall Street Journal reported last week:

(source)

The US has so far committed more than US$565M to Brazilian rare earths projects and just last month, USA Rare Earths agreed to pay US$2.8BN for a producing rare earths mine in Brazil.

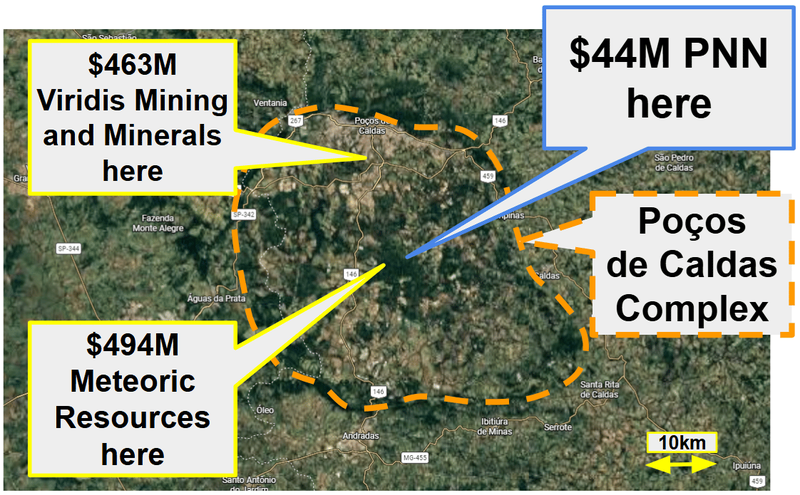

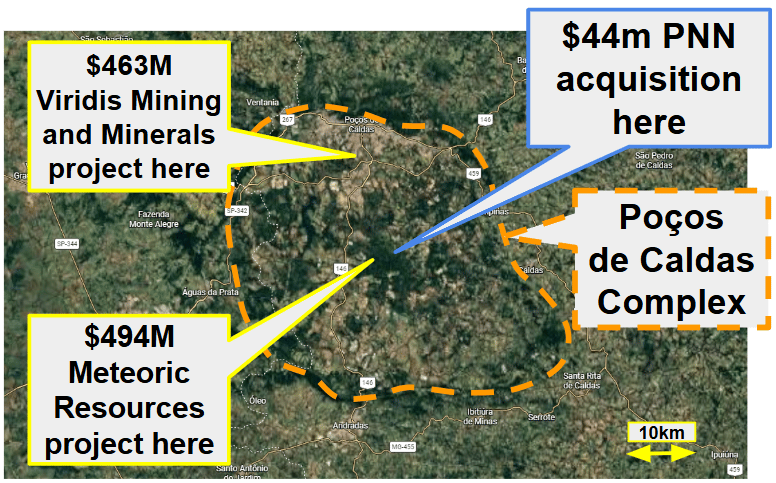

Most of the activity is centred around one region in Brazil - Poços de Caldas.

Precisely where our Investment, the $44M capped Power Minerals (ASX:PNN)’s project sits.

PNN acquired this new project in this global rare earths hot spot back in March.

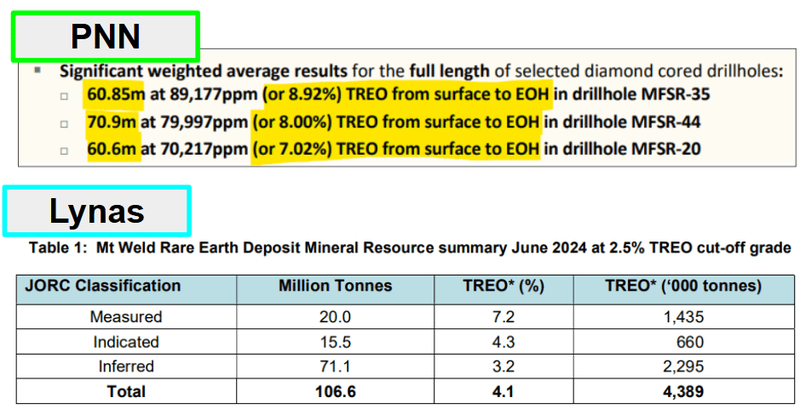

PNN’s project has multiple 60m+ drill intercepts where grades are above 8% TREO - from surface all the way down to the end of holes (ending in mineralisation).

Those are some of the highest grade rare earths we have seen on the ASX.

PLUS it's got up to 2% MAGNETIC rare earths grades too - the ones that go into robots, drones, fighter jets, AI datacentres etc, like the ones we mentioned above.

The WSJ article named two ASX listed companies ~$463M Viridis and ~$494M Meteoric.

$44M capped PNN’s project is in the same neighbourhood as both of those companies:

(source)

And today, PNN started drill testing this project:

(source)

PNN’s new project is relatively advanced because a high grade rare earths discovery has already been made.

The project has ~156 holes drilled into it (50 diamond holes and ~106 auger holes).

(The project has no JORC resource estimate defined... yet - that’s what PNN’s current drill campaign is all about)

Again, PNN’s project has multiple 60m+ drill intercepts where grades are above 8% TREO - from surface all the way down to the end of holes (ending in mineralisation).

AND a few smaller 2m intervals where grades are as high as 24.13% TREO - those are some of the highest grade hits we have seen from any rare earth project on the ASX.

(see all the drill results in PNN acquisition announcement here)

To get an idea of just how strong those grades are - US listed $14BN MP Materials’ mine in California has an average grade of 5.90% TREO (one of the highest grade rare earth mines in the world).

Of course, MP has an actual mine and a well defined resource at that grade - PNN has only got a few historical drill holes demonstrating high grades - we don't yet know the full extent of PNN’s high grade resources yet.

(Probably a big part of the reason PNN is only capped at $44M right now and MP is a $1BN heavyweight.)

Whilst its early days for PNN, at this point we do know that its project is geologically comparable to MP Material’s Mountain Pass mine.

The announcement on acquisition said, “The primary rare earth mineralisation identified is hosted in bastnäsite, comparable to the producing Mountain Pass Mine (USA)”.

(source)

(We hope that means the metwork/processing risk - which is always a risk for rare earths projects - is somewhat addressed)

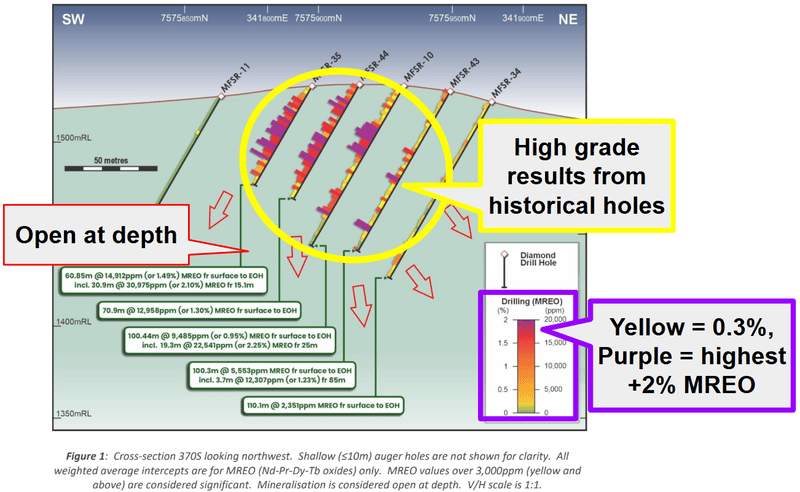

The big kicker for PNN’s asset is the Magnet Rare Earth Oxide (MREO) grades on the project.

PNN's project has hits with MREO grades above 2% and even one 60.85m hit averaging 1.49% MREO.

(source)

The four magnet rare earths - neodymium, praseodymium, dysprosium and terbium - account for more than 80% of the market value of all rare earths.

They are the ones that go into humanoid robots, drones, jet fighters, missile guidance systems, naval propulsion, next-gen submarine sonar, AI data storage, displays and quantum computing.

We listened to an interview with PNN’s CEO Alistair Stephens where he said:

“I thought it was the ratio (% MREO of the TREO), then I looked a bit closer and went oh hang on, that’s the actual grade, I was like oh my god that’s 40 to 50% of the TREO grade is tied up as MREO”

“That’s huge, that’s a massive ratio”

You can check out that part of the interview here

Alistair knows his rare earths well too - he was Managing Director of Arafura Resources between 2004 and 2009 (Arafura are now capped at $1.5BN) AND most recently was CEO of Lindian Resources (now capped at $1.6BN).

Both are big rare earths success stories on the ASX.

And now he recently joined PNN as CEO to drive this new asset forward in the same way he built value at his previous gigs.

So if the grades are strong enough for Alistair to double take, it could also get the market going once PNN proves size/scale on the project.

We are hoping that happens with this current round of drilling.

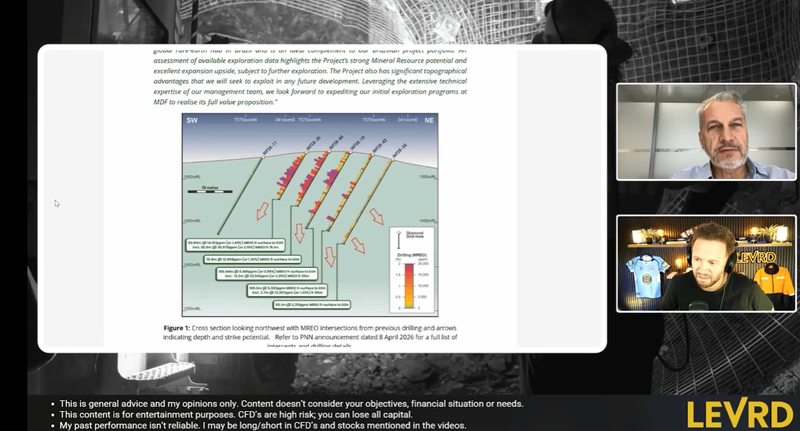

As mentioned earlier, the project has only had ~50 serious diamond holes drilled into it - and everything intercepted is open in all directions:

(source)

PNN’s project also has a special type of permit - meaning the project can be developed a lot quicker

PNN’s project also sits on a rare type of Brazilian mining title called a "Manifesto de Mina".

These Manifestos are a legacy title from the 1930s that functions as a full, granted mining licence - with no expiry date.

No renewals or waiting years for a mining lease to be granted.

Sounds almost too good to be true, but it isn’t, it is actually a thing.

From a regulatory standpoint, the only material thing PNN needs to do to mine the project is get environmental approvals.

Otherwise, PNN gets full unencumbered access to the project for whatever it wants, when it wants, all year round.

PNN also owns the land outright, so there is literally nothing holding up drilling work on the asset.

(this is why PNN was able to move from acquisition to drilling in a matter of weeks)

PNN completed the acquisition in April and is already drilling right now.

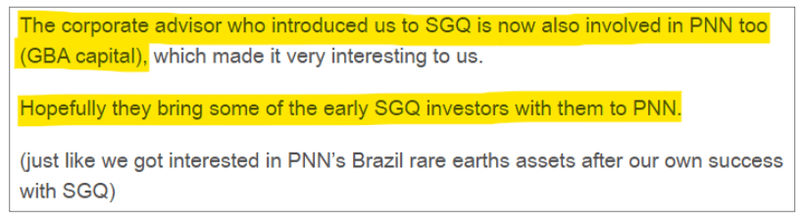

PNN is starting to remind us of St George Mining (ASX:SGQ)

The way PNN has acquired this new project feels eerily similar to the rare earths origins of SGQ which acquired an advanced stage rare earths asset in Brazil back in August 2024.

We first Invested in PNN following the corporate advisor who got us into SGQ.

Here is what we said when we first Invested in PNN:

(source)

Now that SGQ has become the $435M capped beast that it is today and is trading millions of dollars in volume a day (and just went into a trading halt for a capital raise - wonder who is coming in), we are hoping that some of the winners from SGQ go out looking for “SGQ 2.0”.

Which we hope leads them to PNN.

A big reason why we think PNN could become SGQ 2.0 for us is because of the way PNN has structured its deal.

PNN’s acquisition will end up costing a total of ~$25.4M (a mix of cash, milestone payments and shares, and there is ~$19.4M remaining).

Which sounds like a big chunk of cash when you consider PNN’s current market cap is ~$44M (fully diluted).

But that was very similar to how SGQ structured its deal.

When SGQ initially acquired its asset, the market was somewhat taken aback by the price it was paying for the asset.

There was even a period of suspension where the company had to iron out the initial funding to pay for the asset.

14 months later, SGQ rallied from ~2.5c to a high of 18c and the company pulled off a $72.5M mega raise, cornerstoned by one of Australia’s richest people, mining magnate Gina Rinehart's private investment vehicle Hancock Prospecting.

Today SGQ trades at ~10c per share.

SGQ was one of our best performers in 2025 - sitting at a peak share price rise of 620% for us at one point:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

There was a lesson we took away from that SGQ deal - sometimes the more expensive acquisitions are expensive for a reason.

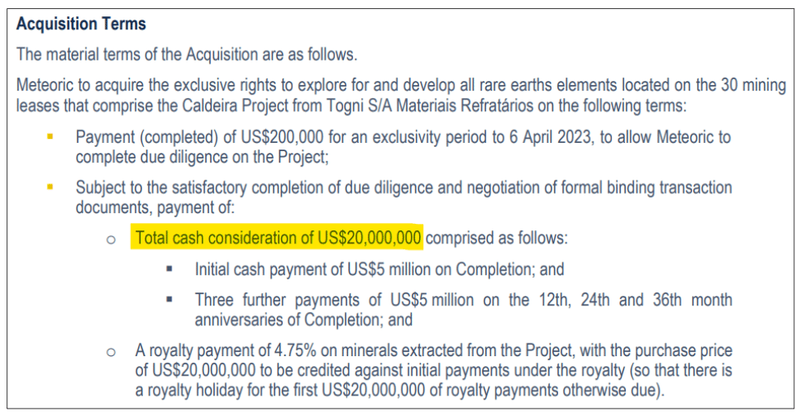

Another example is PNN’s neighbour - Meteoric Resources which paid $20M cash in total for their asset:

(source)

Only 12 months after acquiring the asset Meteoric’s share price was up 1,837%.

Now, 3 years later the company has defined a large ionic clay rare earth system and trades at a market cap of $494M.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

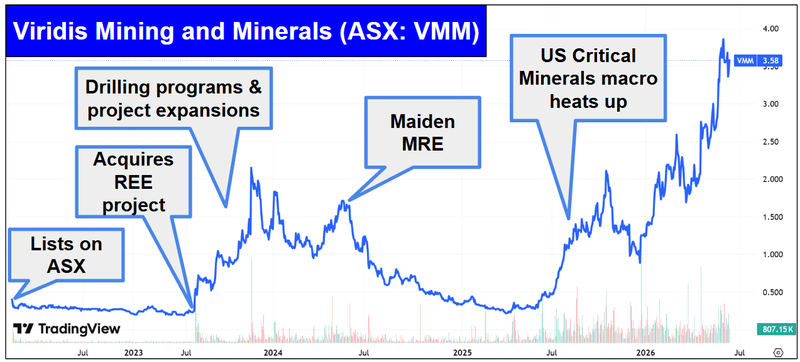

The other one in the region is Viridis Mining & Minerals which IPO’d at 20c and ran all the way as high as $4.03 per share (up 1,915% at its peak).

Today Viridis is capped at $463M.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The difference between those two examples is that PNN’s asset (for now) has a different mineralisation style. (source)

Viridis and Meteoric’s projects are both considered “ionic clay” deposits, which are known to contain higher concentrations of “heavy rare earths”.

Yes - heavy rare earths... the type that's harder to find and used in applications such as AI, quantum computing and autonomous warfare... and China currently controls supply).

BUT PNN has explicitly mentioned that a part of its project could also be prospective for ionic clay style rare earths.

So the hard rock mineralisation is the primary target and we essentially get the ionic clay upside for free.

PNN has explicitly said it would “prioritise the examination of this potential” at some point.

(source)

Very early days for PNN on the ionic clay potential.

But we like that the project has this exploration optionality - especially for discovering two types of deposits the ASX understand well and knows how to value:

- Hard rock mineralisation similar to $14BN MP Materials, and

- Ionic clay mineralisation similar to ~$463M Viridis and ~$494M Meteoric.

Now with drilling underway we should learn more about the asset pretty soon.

IF the results prove and extend the historic results we think the market could re-rate PNN quickly - especially when there are direct peer comps, listed on the ASX nearby.

No guarantees of course, this is small cap investing, things can and do go wrong.

Our PNN Big Bet:

"PNN proves up a major high-grade rare earths resource in Brazil and re-rates 1,000% from our Initial Entry Price - via development, strategic investment or acquisition"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Power Minerals

Keep reading to see our full PNN Investment Memo which lays out:

- What PNN does

- The macro theme for PNN

- Our PNN Big Bet

- Why we are Invested in PNN

- What we want to see PNN achieve

- The key risks to our Investment Thesis,

- Our Investment Plan

Before we get to those, here is a quick overview of 11 reasons why we Invested in PNN:

11 reasons why we are Invested in PNN

1. Rare earths as an exposure to AI and Robotics

Rare earths are a group of 17 metals, a small group of them - neodymium, praseodymium, dysprosium and terbium - are used to make the strongest permanent magnets on earth.

Those magnets are in EV motors, wind turbines, robots, drones, fighter jets, guided missiles, smartphones and the cooling systems of AI data centres.

There are no commercial substitutes.

An F-35 contains ~400kg of rare earth materials. A single EV uses 1-2kg of rare earth magnets. A humanoid robot is expected to use more.

(source)

2. PNN's project is advanced stage (an existing discovery)

PNN’s project has passed the exploration stage with ~156 holes drilled into it.

It has already had 50 drill holes for a total of over 4,000m of diamond core drilling AND 106 holes for a total of 846.5m of auger drilling.

The existing discovery de-risks the asset from an exploration perspective and gives PNN something to expand.

3. PNN’s project has some of the highest rare earth grades we have seen on the ASX

Historic drilling at Morro do Ferro returned 60.85m at 8.92% TREO, 70.9m at 8.00% TREO and 100.44m at 4.99% TREO - all from surface to the end of the hole.

For context $18BN Lynas Rare Earths project (which is the highest grade on the ASX) has a resource with an average grade around ~4.1% TREO.

4. The grades are rich in the rare earths that actually matter

PNN’s due diligence confirmed MREO values up to 3.53% of whole rock - and one hole averaged 1.47% MREO over its entire 60.85m length, a higher magnet rare earth grade than the total rare earth grade of many deposits globally.

The four magnet rare earths (MREO) - Nd, Pr, Dy, Tb - account for more than 80% of the market value of all rare earths.

They are the ones that go into humanoid robots, drones, jet fighters, missile guidance systems, naval propulsion, next-gen submarine sonar, AI data storage & displays.

5. PNN’s project has a special type of mining title - “Manifesto de Mina"

A "Manifesto de Mina" is a legacy Brazilian mining title with no expiry date that already grants the right to mine, with only environmental permitting required to move to production. (source)

PNN also owns the freehold land above the deposit, so there are no third-party landholders to negotiate with.

We think the special type of license means IF PNN can define a large enough resource to put the project into production it can get to a decision point a lot quicker than other rare earths projects globally.

6. Geology analogous to the world’s highest grade operating rare earths mine

PNN says that its project's mineralisation is hosted in bastnäsite - the same well-understood mineral processed for decades at MP Materials' ~A$14BN Mountain Pass operation in California.

That gives the metallurgical workstream a meaningfully better starting point than most early-stage rare earths projects.

(source)

7. Next door to two ASX rare earths success stories

Morro do Ferro is in the Poços de Caldas complex alongside the ~$494M capped Meteoric Resources and the ~$463M capped Viridis Mining & Minerals.

PNN is capped at ~$44M.

We think that with some drilling, PNN can close the gap to its neighbours (assuming exploration is successful).

(source)

8. We have had success Investing in Brazil before

Brazil has an established mining industry - Minas Gerais (the state where PNN’s project sits in) literally translates to "General Mines" - the state was founded on mining and has hosted it for over 300 years.

This is not a frontier jurisdiction. The workforce, the drilling contractors, the labs, the infrastructure and the regulator all exist at scale.

Some of our biggest wins have come from companies with projects in Brazil (both of them also being in Minas Gerais):

- Latin Resources - which made a lithium discovery in Brazil and went from ~3c to a high of ~45c per share - at its peak LRS returned 2332% for us. Eventually the company was taken over by Pilbara Minerals in a deal worth ~$560M.

- St George Mining (ASX: SGQ) - We Invested in SGQ at 2.5c when it first acquired its rare earths project in Brazil. At its peak SGQ was up 620% for us - now it trades at 11c per share - still 340% above our Initial Entry Price.

9. Brazil matters for US critical minerals independence

China still controls ~90% of the world's rare earth magnet supply chain.

For the heaviest, most valuable rare earths like dysprosium and terbium, China controls ~98-99% of refined supply.

The US is pouring capital into Brazil to try and solve its domestic rare earth supply chain dependency issue.

Brazil is home to the world's second biggest rare earth reserves (behind only China).

So far committed more than US$565M to Brazilian critical minerals projects and just last month US listed USA Rare Earths agreed to a US$2.8BN takeover of a producing rare earths mine in Brazil. (source)

Both of PNN's Brazilian projects sit in states (Minas Gerais and Goiás) that have been in talks to sign critical minerals cooperation agreements with the US. (source)

We think more of these type deals between the US and Brazil are possible for rare earths assets.

10. The "SGQ 2.0" set-up

PNN's deal has a lot of similarities to the deal our Investment SGQ did for its asset in 2024.

SGQ paid a similar amount for its project AND the same corporate advisor behind SGQ is behind PNN.

SGQ re-rated from ~2.5c to a high of 18c and is now capped at ~$435M.

We are hoping some of the capital from people who had a winner with SGQ finds its way into PNN as it proves out its asset.

11. PNN’s project also has Ionic clay optionality

Parts of PNN's ground trend toward its neighbours' ionic clay deposits - the style of rare earths mineralisation the ASX understands well with PNN’s two neighbours - $463M Viridis and $494M Meteoric.

IF PNN defines an ionic clay resource on top of its existing discovery then it could all of a sudden draw comparisons to its project and that of Viridis and Meteoric.

Ultimately, we are hoping a combination of the reasons above lead to PNN delivering our Big Bet as follows:

Our PNN Big Bet:

"PNN proves up a major high-grade rare earths resource in Brazil and re-rates 1,000% from our Initial Entry Price - via development, strategic investment or acquisition"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Power Minerals

Investment Memo: Power Minerals Ltd (ASX:PNN)

Opened: 15-Jun-2026

Shares Held at Open: 7,338,223

Options Held at Open: 4,399,786

What does PNN do?

Power Minerals (ASX:PNN) owns 100% of advanced stage rare earths project in Brazil.

The project sits on a "Manifesto de Mina" mining title which has no expiry date and requires only environmental permits to put into production.

The project has some of the highest grade rare earth drill intercepts we have seen of any company listed on the ASX.

What is the macro theme?

China controls ~90% of the world's rare earth magnet supply chain and has placed the most valuable magnet rare earths behind export restrictions.

Especially - neodymium, praseodymium, dysprosium and terbium.

The four magnet rare earths that make up >80% of the market value of all rare earths used in magnets for EVs, robots, drones, defence systems and AI data centre hardware.

Brazil is home to the world's second largest rare earth reserves - we think the US will lean into Brazilian rare earth project to secure its own supply chains.

Our Big Bet for PNN

"PNN proves up a major high-grade rare earths resource in Brazil and re-rates 1,000% from our Initial Entry Price - via development, strategic investment or acquisition"

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Why are we Invested in PNN?

- Rare earths as an exposure to AI and Robotics

- PNN's project is advanced stage (an existing discovery)

- PNN’s project has some of the highest rare earth grades we have seen on the ASX

- The grades are rich in the rare earths that actually matter

- PNN’s project has a special type of mining title - “Manifesto de Mina"

- Geology analogous to the world’s highest grade operating rare earths mine

- Next door to two ASX rare earths success stories

- We have had success Investing in Brazil before

- Brazil matters for US critical minerals independence

- The "SGQ 2.0" set-up

- PNN’s project also has Ionic clay optionality

What do we expect PNN to deliver?

Objective #1: Drilling at rare earths project (Morro do Ferro)

We want to see PNN drill out its project and extend its deposit at depth and along strike.

Milestones

- ✅ Acquisition completed

- ✅ Drilling started

- 🔲 First assay results

Objective #2: JORC resource for rare earths project (Morro do Ferro)

We want to see PNN define a maiden JORC resource estimate for its project in Brazil.

Milestones

- 🔲 PNN to test the ionic clay potential of the project

- 🔲 Metallurgical testwork results

- 🔲 Resource drilling completed

- 🔲 Maiden JORC Mineral Resource Estimate

Objective #3: Permitting and development progress (Morro do Ferro)

We want to see PNN complete environmental permitting and move the project closer to development.

We are also hoping to see the project attract corporate/strategic or offtake interest either from inside the US or internationally.

Milestones

- 🔲 Environmental permitting

- 🔲 Economic/development studies

- 🔲 Corporate/strategic/offtake interest

Objective #4: Progress at PNN’s other Brazilian rare earths/niobium project (Santa Anna)

We want to see PNN spend most of its time/capital on its main asset (Morro De Ferro) but would also like to see its other asset move to at least a maiden JORC resource.

Milestones

- 🔄 Maiden resource estimate preparation

What could go wrong?

Exploration risk

All of Morro do Ferro's headline grades were drilled by previous owners, mostly in shallow holes. The project has no JORC resource yet. IF PNN's drilling fails to confirm the historic grades, or the deposit doesn't extend, the investment thesis takes a direct hit and we would expect the share price to re-rate lower.

Metallurgical risk

High grades mean nothing if the rare earths can't be economically extracted. Bastnäsite is well understood, but every deposit's metallurgy is unique - recoveries, impurities and processing costs could be a lot higher than other well understood deposits making it challenging to develop the asset.

Funding & dilution risk

PNN has staged acquisition payments of up to ~$25.4M ahead of it, plus drill programs across multiple projects. As a pre-revenue explorer, future raises are likely - potentially at a discount, diluting existing shareholders.

Commodity price / macro risk

Rare earths equities are running on geopolitics. A durable US-China trade detente, or a public failure of US-Brazil minerals cooperation, could pull sentiment (and capital) out of the sector quickly - hitting early-stage explorers hardest.

Permitting & jurisdiction risk

The Manifesto title removes mining-licence risk, but environmental permitting is still required to develop the project. Regulatory changes, permitting delays or political shifts in Brazil could slow the path from drilling to development.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking PNN's share price with it. Junior explorers typically fall harder than the broader market in risk-off periods.

What is our investment plan?

We are Invested in PNN to see it progress its project toward development.

PNN sits in our Catalyst Hunter Portfolio.

Our plan is to hold PNN in line with our Trading Blackout and hold conditions for the Catalyst Hunter Portfolio - which we hope is enough time to see PNN to move towards either development, strategic investment or acquisition (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

Check out the detailed hold conditions for our Catalyst Hunter Portfolio here.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.