Pantera to re-enter wells for lithium brine as oil major neighbour Exxon starts pre-sales of lithium.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 9,666,862 PFE shares and 2,994,167 PFE Options at the time of publishing this article. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time.

Oil supermajor ExxonMobil is making the Smackover Basin the centrepiece of its lithium business in the USA.

Just last week Exxon signed an MOU with EV battery maker SK On to sell them ~100k metric tonnes of lithium from the Smackover Basin, to be used in batteries manufactured inside the US.

(Source)

Our exposure to the Smackover is the ~$11M capped, early mover, Pantera Minerals (ASX:PFE).

PFE was in the Smackover before Exxon moved into the region via its takeover of Galvanic Lithium for >US$100M...

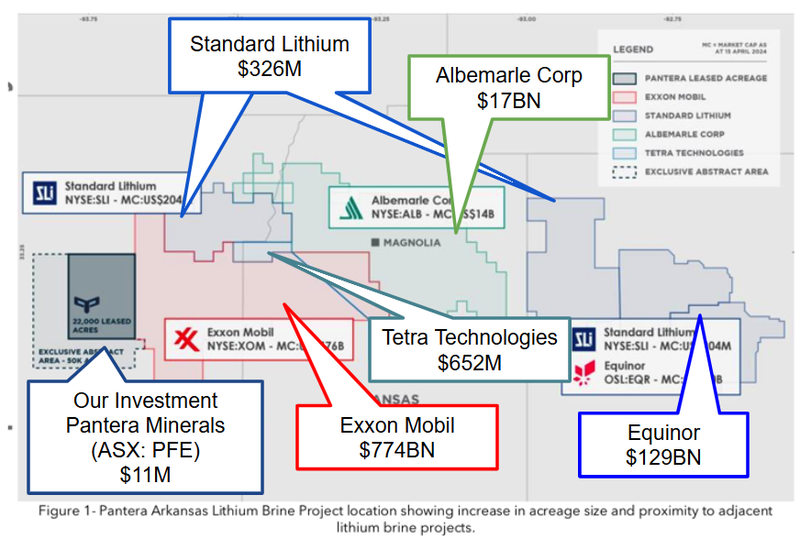

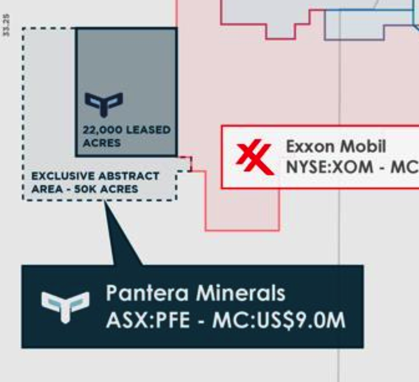

PFE has been steadily increasing its land position in the Smackover Basin over the past 12 months, now with 22,000 leased acres.

Even though it's a tiny company, PFE has been able to secure so much ground, mainly via an exclusive deal it signed before the landrush in the Smackover.

It's now punching far above its weight in the Smackover.

PFE is now the largest acreage holder in the Smackover outside the five established players - Exxon, Albemarle, Tetra, Equinor, and Standard Lithium...

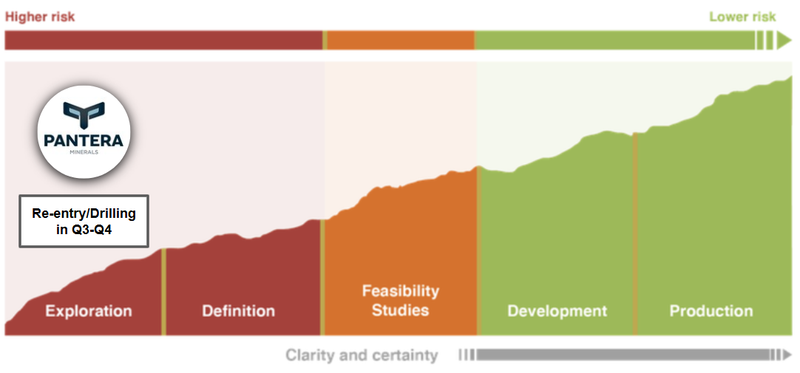

In the coming months, PFE’s plan is to:

- re-enter an old oil and gas well,

- sample for lithium, and

- put together a maiden JORC resource for its project.

The well re-entry is expected to happen this quarter...

We are hoping that with some lithium samples in hand, and some evidence of the viability of lithium extraction on its ground, PFE may be able to deliver a long awaited re-rate of its share price.

The JORC resource estimate that comes after will be the major catalyst for PFE.

Post-resource is typically when majors like Exxon or Equinor start to look at a project because it is de-risked from an exploration perspective.

With interest in the Smackover increasing (especially from the oil supermajors) it will be interesting to see if they show any interest in the company then.

The Smackover and US lithium brines are getting a lot of market interest...

Despite all of the negative sentiment around the lithium industry, Exxon seems to be going hard and fast with its Investments - Exxon’s plan is to be producing lithium by 2027.

Esteemed lithium analyst Joe Lowry had a lot to say about Exxon’s movements in the Smackover saying that he thinks the “Smackover is where the US will have brine & DLE success”...

Here is a tweet from him & an episode from his podcast where he speaks to the Standard Lithium folks:

(Source)

(Source)

It's not just Joe and Exxon who seem to rate the Smackover either...

$129BN Equinor also did a deal with Smackover “junior” Standard Lithium back in May.

(Source)

Here is an article from The Economist which summarises the move from oil majors into lithium - we think it's definitely worth a read:

(Source)

Following the big oil money... we think the Smackover is going to be one of the centrepieces of the US lithium Industry and our lithium exposure to the region is PFE.

PFE is the only ASX listed small cap with ground in the Smackover.

PFE is also trading at a fraction of the market caps the bigger players in the region trade at:

- Exxon Mobil - capped at ~$774BN

- Equinor - capped at ~$129BN

- Albemarle - capped at ~$17BN

- Standard Lithium - capped at ~$326M

- Tetra Technologies - capped at ~$652M

- Pantera Minerals (ASX:PFE) - capped at ~$11M

Despite the tiny market cap, as we noted above, PFE is currently the largest acreage holder outside the five established players - Exxon, Albemarle, Tetra, Equinor, and Standard Lithium...

Putting aside the oil giants, we think PFE’s market cap is lagging behind other ‘pure’ lithium players in the region because its project is at a much earlier stage - PFE is pre-resource definition.

Our PFE Investment Memo - why did we Invest?

You can read our Investment Memo in the link below. This memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

Our most recent Investment Memo on PFE was written in March 2024.

Read our PFE Investment Memo here.

In our PFE Investment Memo, you can find the following:

- What does PFE do?

- The macro theme for PFE

- Our PFE Big Bet

- What we want to see PFE achieve

- Why we are Invested in PFE

- The key risks to our Investment Thesis

- Our Investment Plan

How is PFE progressing against our Investment Memo?

Since PFE entered the Smackover Basin, it has focused more on expanding its landholding than on exploration work, in order to get ahead of its peers in the “land grab”.

Last month it hit a milestone of 22,000 leased acres. It has an exclusive abstract area of 50,0000 acres.

Increasing its acreage was was one of the key objectives we wanted to see PFE deliver in our March 2024 PFE Investment Memo.

PFE has already delivered a couple of acreage increases since then.

Objective #1: Rapidly increase acreage in Smackover Formation

PFE, is aiming to rapidly grow its footprint in the Smackover Formation. This could make the company attractive to majors in the area or another company looking to gain exposure to the region. To do this PFE will need to continue leasing acreage quickly.

Milestones

✅ 10,000 acres leased

✅ 15,000 acres leased

✅ 20,000 acres leased

☐ +25,000 acres leased

Source: PFE Investment Memo 4th March 2024

When it comes to lithium brine production, establishing a large landholding is important, however we think the market might be waiting to see some exploration results from PFE before it starts to value its project appropriately.

By exploration results, we mean going underground, getting some lithium samples, confirming porosity, permeability, and determining how easy it would be to extract lithium from its acreage.

Based on its June ASX announcement, PFE should now be getting closer to finalising sub-surface work - which is a precursor to picking the best historic well for re-entry.

PFE is planning on its first well re-entry this quarter.

The main target for the year is to get to a maiden JORC resource estimate for its project in Q4 of this year.

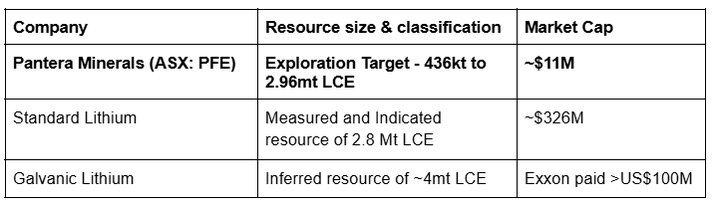

PFE already has an exploration target of 436,000 to 2,966,000 tonnes of Lithium Carbonate Equivalent (LCE).

However the JORC resource estimate should provide a firmer benchmark for investors to compare PFE’s resource to others in the market.

We are Invested in PFE to see it work through the typical exploration/definition process and get its project up to a similar stage as its regional peers.

Eventually we hope the market takes note of what PFE has and re-rates its market cap higher.

What stage PFE is at relative to its regional peers

Most of PFE’s regional peers are in the feasibility/definition stages.

In November last year Exxon drilled its first well and expects to have its projects producing lithium carbonates by 2027.

Standard and Equinor's project is already in the advanced feasibility stages.

Tetra recently completed definition work on its resource and now has Exxon in its corner which will mean they can start moving a lot quicker developing their projects...

As for PFE, right now the company has leased ~22,270 acres inside a 50,000 acre AOI “Area Of Interest” - the AOI is basically the area PFE has rights to negotiate leases in.

Across that 50,000-acre ground position, PFE has already estimated a JORC lithium exploration target of 436,000 to 2,966,000 tonnes of Lithium Carbonate Equivalent (LCE).

PFE's work between now and Q4 of this year will be to try to put together a maiden JORC resource estimate for its ground.

As we flagged above, we think the JORC resource estimate will be a big catalyst for PFE, as it will give the market a metric to compare to PFE’s neighbours.

Our view is that IF PFE can put together a resource estimate somewhere in the middle of its exploration target (436kt to 2.96mt LCE), then its market cap could re-rate higher, as the market will have something to compare PFE against its regional peers.

Here is how PFE looks relative to some of its neighbours right now (excluding the giant companies with dozens of assets, preventing a meaningful valuation of their Smackover assets):

Over the next ~ six months, PFE plans to re-enter an old oil and gas well, sample for lithium, and upgrade its exploration target into a maiden JORC resource.

We think the JORC resource estimate will be a major share price catalyst for PFE because it will de-risk the company’s project from an exploration perspective.

Post-resource is typically when majors like Exxon or Equinor start to consider a project, so it will be interesting to see if they show any interest in the company then.

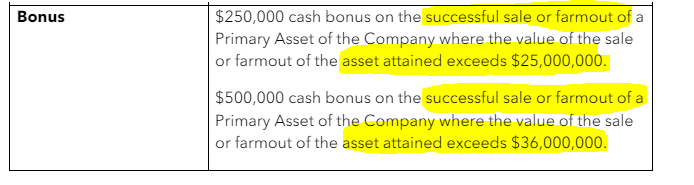

Interestingly, we noticed after market yesterday that PFE’s MD incentives are also set up for some sort of deal of this sort...

We are Invested in PFE to see it work up its project and hopefully achieve our Big Bet which is as follows:

Our PFE Big Bet:

“PFE to return 10x by making a discovery and defining a deposit significant enough to move into development studies”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PFE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

How the recent macro news relates to our PFE Investment Memo:

Reason we Invested #1: PFE right next door to $643BN Exxon

Exxon reportedly spent >US$100M acquiring its project and just started drilling its first well 6 weeks ago with a view of getting to first production by 2027.

Source: PFE Investment Memo 4th March 2024

Since our Memo, Exxon has laid out its production plans and announced that it expects to be producing lithium by 2027.

Exxon has also signed an MOU with battery maker SK On which would see Exxon’s lithium end up in EV batteries manufactured in the US.

As Exxon develops its Smackover projects we think it increases the look through value of other projects in the region - including PFE’s.

Reason we Invested #2: Surrounded by (much) bigger players

PFE is also in the same neighbourhood as $25BN Albemarle, $383M Standard Lithium, $790M Tetra Technologies.

Source: PFE Investment Memo 4th March 2024

Since our memo, oil major Equinor entered the Smackover by doing a deal with Standard Lithium.

More capital in the Smackover and players with deeper pockets coming in means anyone with ground already leased - like PFE - should theoretically see increases to the value of their assets.

Once Exxon entered the basin, we thought it would be a game changer for the region - given the amount of capital Exxon could throw at bringing projects into production.

Our expectation was always to see other corporates (big and small) move into the region by either dealing with the existing players in the region or like PFE - by staking new ground.

So far, the deals done have been by the oil supermajors - Exxon and Equinor.

We expect there to be more investor interest, mainstream media coverage and corporate deals as Exxon gets closer to first production from its project (now expected in 2027).

All of this activity helps PFE and the value of its Smackover Basin acreage.

We think the above two reasons are still a key part of our PFE Investment Memo and we expect to see more newsflow from the company’s regional peers over the coming years.

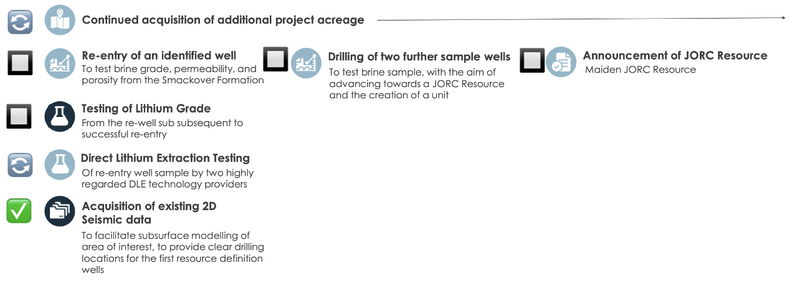

What’s next for PFE?

Below is a list of the key catalysts PFE is working toward, from a recent investor presentation the company put out.

(Source)

In the short-term we want to see PFE deliver the following two catalysts:

Re-enter a well 🔲

The first step toward converting its exploration target into a maiden JORC resource will be to re-enter historic oil & gas wells that sit on its acreage.

The goal for the re-entry programs will be to see how much lithium sits in the ground, the concentrations and how easy it is to extract (permeability/porosity).

DLE test 🔲

The re-entry will bring up samples which PFE can then send off to DLE (Direct Lithium Extraction) tech partners.

If PFE continues making progress along these milestones, we think it should move closer to achieving our ultimate upside case for our PFE Investment.

What are the risks?

Through to the end of this year the key risk we are most conscious of is “Exploration Risk”, which we highlighted in our PFE Investment Memo:

Exploration risk

PFE has said it intends to secure a lithium brine sample on the company’s acreage - there is no guarantee that lithium bearing brines are found or the brines are of economic concentrations.

Alternatively, if brines are found, they could contain contaminants that reduce or eliminate the value of PFE’s brines.

Source: PFE Investment Memo 4th March 2024

PFE is planning a re-entry program where it will be sampling for lithium brines on its acreage.

If this were to happen the market would likely re-rate PFE’s share price lower, discounting the lithium potential of the ground PFE holds.

This is just one of the many risks to our Investment Thesis - we list more risks in our PFE Investment Memo here.

Our PFE Investment Memo

Below is our Investment Memo for PFE, which provides a short, high-level summary of our reasons for Investing.

In our PFE Investment Memo, you can find the following:

- What does PFE do?

- The macro theme for PFE

- Our PFE Big Bet

- What we want to see PFE achieve

- Why we are Invested in PFE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.