Pantera (PFE) set to unleash the heli-rig - first drilling starts next week.

Yesterday, our junior exploration investment Pantera Minerals (ASX:PFE) announced its maiden drill event in the north of WA will start next week.

PFE will be drilling 5 diamond drill holes targeting an outcropping of hematite (iron ore) mineralisation that is interpreted to sit on the contact of the “Yampi Formation” - hopefully that outcropping points to deeper mineralisation...

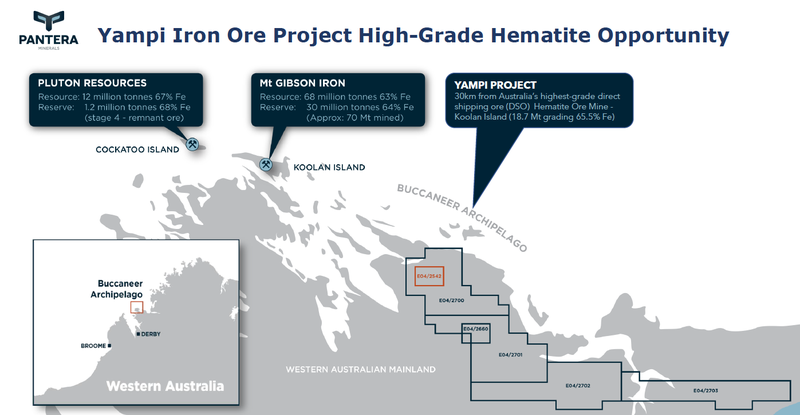

PFE has announced approval of its Program of Works, detailing the next steps for its Yampi Iron Ore Project. PFE’s iron ore project is next door and along strike from Australia’s highest grade direct shipping ore hematite mine, the $550M capped Mt Gibson’s Koolan Island in Western Australia.

We participated in PFE’s IPO to raise $7M at 20 cents per share back in early August.

We like PFE’s main asset - it is a barely explored, potential high-grade and high-tonnage iron ore exploration project in WA, located just kilometres from Mt Gibson Iron’s existing infrastructure on nearby Koolan Island.

While the iron ore price has taken a beating over recent months, long term we think the world is still going to need a lot of iron ore, which bodes well for the iron ore price and the value of any discoveries.

We also like that PFE’s maiden drilling programme has arrived so soon after listing, which could deliver a market re-rate on success. PFE also has a few other WA exploration assets which it can work up in the future to add value.

With the $7M IPO completed, PFE has plenty of funds to execute its exploration strategy. We will get our next look at PFE’s current cash balance in the quarterly report due at the end of this month.

As an early stage explorer, PFE is a high-risk, high-reward play. We’re hopeful that the company can find out more about the mineralisation at Yampi through this upcoming drilling campaign. Ultimately we think if PFE can prove up a decent resource, PFE could be appealing for a producer to acquire.

With an enterprise value of under ~$15M, we believe there is plenty of upside should the rigs encounter more hematite (iron ore) in the coming weeks.

Our investment strategy for early stage explorers like PFE is to invest early and wait out the months of pre-drill prep work, top slice (sell a small portion) into the drilling campaign and hold a position through the first batch of results.

PFE has been a lot faster than usual to get to drilling. Our plan is to sell about 20% of our total position over the next three months if the PFE price runs up during the first drilling campaign, holding the rest of our position for the first 5 drill results and beyond into PFE’s next program of drilling work.

We think PFE’s chances of success are better than your typical explorer, we covered this in more detail in our original report when we added PFE to our portfolio a few months ago, but here is a quick summary:

- Yampi’s large, unexplored land holding with more exploration licences under application.

- Never been drilled, despite proximity to what is arguably the best hematite real-estate (Koolan Island - 18.7 Mt grading 65.5% Fe, 70Mt already mined) in Australia.

- Abundant high grade hematite mineralisation identified, with high grade/low impurity (clean) ore grab samples assayed over 50km2.

- High Iron (Fe) grades in samples up to 68% - These are grab samples that have been taken over 50km2. Good early signs here, however grab samples are just glimpses until drilling can happen and we can get a better understanding of the grades.

- Any discovery would NOT be a stranded asset - Yampi is 4km from deep-water access, and 25km by road to Mount Gibson’s Koolan Island mine. “Stranded assets” that sit long distances from transport infrastructure can often be a major issue with iron ore discoveries - haulking bulk materials is expensive. PFE doesn’t appear to have this issue.

- Any discovery could be attractive to existing producers, given rich grades of nearby deposits.

- Tight capital structure, meaning that if successful, positive market-re-rate much more likely. PFE has 68.5 million shares on issue with ~ 44% of shares escrowed. Noting there are a few options out there which may dilute the upside - there are 29 million options that have an exercise price of 25c.

Always keep in mind that exploration investing is risky and only invest what you are comfortable to lose.

With regard to its tenement holdings, PFE has been granted exploration licence E04/2542, covering an area of 20 square kilometres. PFE has also applied for four exploration licences to the south and south-east of E04/2542.

So let’s unpack the announcement in more depth.

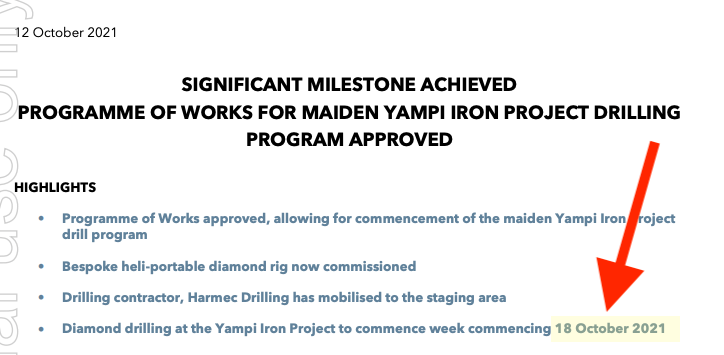

Yesterday PFE provided details of its approved Program of Works for its Yampi project, opening the lid to how they can determine the real potential for their flagship asset.

Firstly, what caught our attention within their announcement was the image of the much awaited bespoke, heli-portable diamond rig. The rig has been commissioned, and is now in Derby, about 140km south of Yampi, awaiting mobilsation to site.

Sometime next week, we anticipate the rig to arrive on site, and this is where the real action begins.

We will be putting pressure on the company management to provide a video of the helicopter dropping the rig onto site - here is our last PFE article where we comment on the heli-rig process.

Five holes are initially planned, to determine if the geology and high grade from surface sampling exists at depth. The program will also provide samples for metallurgical test work, to see if Yampi is consistent with that of the nearby Koolan Island ore - rock-chip geochemistry already confirms the potential for beneficiable ore and possible direct shipping ore (DSO).

All up, we are looking at a 6 week programme incorporating the drilling. Then we expect it will take another 8 weeks for the labs to return the assay results. So by late January, we should have initial drill results, providing a clearer idea of just what PFE has in its hands at Yampi.

Depending on the grade and consistency of the assay results, PFE would be looking at options ranging from an initial resource (outsized result, best case), exploration target (good result, probably the most likely scenario) through to moose pasture (equals nothing. Worse case).

We think PFE will need to run many more drill programs to gain a really solid understanding of the mineralisation before a discovery success.

As you can tell, we like the asset, but what about the people behind unlocking its potential.

We like that PFE’s Head of Exploration is Nick Payne. Nick has worked for large multinationals such as BHP and AngloGold, but arguably of most significance is his previous role as senior exploration geologist and exploration manager for Mount Gibson Iron Ltd, where he was responsible for exploration at the Koolan Island Iron Ore Project.

Yes - the same project just up the road from Yampi. There are not many people better equipped, with his local geological knowledge and experience, to head PFE’s exploration campaign than Nick.

Leading PFE’s management team as CEO is Matthew Hansen — one of the first indigenous Australian chief executives of an ASX company. Hansen has been instrumental in the progress of large companies across multiple commodities, including Australia’s largest gold producer in Northern Star Resources as well as nickel miner Western Areas. As a lawyer who has completed in-house roles with Newmont and Rio Tinto, Hansen has vast experience in areas such as indigenous affairs and native title, as well as broader regulatory requirements. He has worked on both sides of the table, negotiating on behalf of traditional owners and representing mining companies.

On that note, we liked hearing from the team that a good relationship with the land’s traditional owners has already been established.

As for the market, iron ore spot prices are north of US$135/t at present, enjoying a 45% climb over the past 3 weeks. It has been quite a volatile ride for this key steel input - breaking all-time records in May when spot prices exceeded US$230/t, then sinking to a 14-month low of US$93/t last month - and now heading back up again.

China’s steel production caps and the recent Evergrande debt crisis has eroded some confidence for iron ore demand growth of late, as has the view that China may want to slow steel production ahead of next year’s Winter Olympics to inhibit pollution. We believe that the higher grade iron ore devoid of impurities will be preferred as China’s long-term steel input of choice, which bodes well for PFE if they can deliver a resource at Yampi.

Iron ore is wedded to steel production, and this won't be changing anytime soon. That's why we like to have exposure to this commodity via an early stage explorer like PFE.

Here is what we are looking for PFE to achieve in the coming months, along with our investment milestones:

Yampi Project (Main Bet - Iron Ore)

✅ Heli-Drill Rig Commissioned

✅ Permitting

🔄 Heli-Drill Rig Mobilised to drill site

🔲 5 Hole Drill Programme Commenced

🔲 5 Hole Drill Programme Complete

🔲 Assay Results hole 1

🔲 Assay Results hole 2

🔲 Assay Results hole 3

🔲 Assay Results hole 4

🔲 Assay Results hole 5

🔲 New Exploration Targets Announced

🔲 New Milestones Identified and Added

🔲 [FUTURE] Prove Iron ore resource

PFE Investment Milestones

✅ Initial Investment: @20c - Majority escrowed for 2 years

✅ Initial Investment: @20c - Non escrowed

🔲 Increase Investment

🔲 Increase Investment

🔲 Price increases 500% from initial entry

🔲 Price increases 1000% from initial entry

🔲 Price increases 2000% from initial entry

🔲 12 Month Capital Gain Discount

🔲 Free Carry - Non escrowed

🔲 Take Some Profit - Non escrowed

🔲 Hold remaining Position for next 2+ years - Escrowed portion

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.