Our New Investment: Power Minerals Ltd (ASX: PNN)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,186,000 PNN Shares and 3,675,500 PNN Options at the time of publishing this article. Some shares and options are subject to shareholder approval. The Company has been engaged by PNN to share our commentary on the progress of our Investment in PNN over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our latest Investment is Power Minerals Ltd (ASX:PNN).

PNN just announced the acquisition of a heavy rare earths project in California, USA.

US critical metals is a rapidly emerging investment theme.

Here are some news articles from just the last 36 hours:

We have had some early success in the US critical minerals thematic this year so far:

- Locksley Resources Ltd is currently up 400% from our Initial Entry Price

- Resolution Minerals Ltd is currently up 223% from our Initial Entry Price.

(not to mention the ASX gorilla of the US critical metals theme Dateline Resources, which we are unfortunately NOT invested in. Dateline is up 100x for the lucky souls that owned it as early as March this year)

(Past performance is not an indicator of future performance)

Rare earth elements are critical for modern technologies, including electronics, medicine and military applications like F35 fighter jets, Tomahawk missiles and the advanced magnets needed for motion in AI robots...

(yep, apparently AI robots will fight the wars of the future).

The US is suddenly scrambling for domestic rare earths supply, because China dominates global production and processing and has started withholding supply from the USA for leverage in various geopolitical spats...

PNN’s new USA project is prospective for HEAVY rare earths.

(Source: Today’s PNN announcement HREO = Heavy Rare Earths Oxides)

(Heavy Rare Earth Elements (HREEs) are rarer, more valuable, and are used in high-temperature magnets and defense)

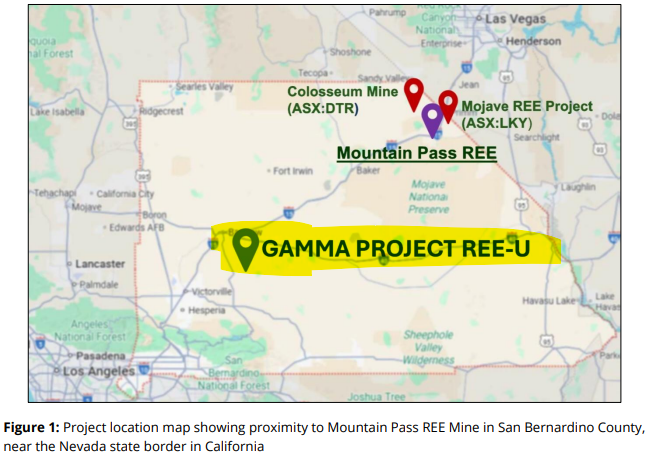

PNN’s new asset sits ~195km (a couple of hours drive) from the only rare earths mine and aspiring rare earths magnets producer in the USA, the $20BN MP Materials.

MP Materials is currently producing mostly LIGHT rare earths.

(The strategic uses we listed above need both light AND heavy rare earths)

Earlier in the year, MP received US$400M from the US Department Of War and signed a US$500M deal with Apple to 10X its magnet production facility.

Immediately after that the Wall Street Journal reported that “as MP scales up magnet production it will need to acquire more heavy rare earths than are available” at its own mine:

(Source)

A genuine new heavy rare earth dominant discovery in the USA could be extremely valuable because it is the less common, more valuable suite of rare earths.

This is where we hope PNN will deliver some exploration success on their heavy rare earths project in California... a short drive away from MP Materials mine.

However it is very early days for PNN on this asset, there’s a lot of work to do.

The US has even been reported to be looking abroad for rare earths supply...

Before today’s new project acquisition - PNN already owned a Brazilian rare earth project where the company is drilling right now.

We also like Brazil rare earths assets, where we have had success with SGQ, a stock up over 500% in the last 9 months:

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The corporate advisor who introduced us to SGQ is now also involved in PNN too (GBA capital), which made it very interesting to us.

Hopefully they bring some of the early SGQ investors with them to PNN.

(just like we got interested in PNN’s Brazil rare earths assets after our own success with SGQ)

We continue to hold a large position in SGQ - in fact it’s one of our biggest positions.

SGQ has the largest and highest-grade carbonatite-hosted rare earth deposit in South America and second highest grade rare earths deposit globally in the Western world.

(we hope the SGQ share price keeps running and some of that attention and capital trickles down into PNN)

PNN recently released drill results from its Brazilian rare earths project.

PNN says “drilling is ongoing” so we could see more results come in over the coming weeks.

A few weeks ago PNN also said that its theory that its project was hosted in a hard rock carbonatite intrusion had been “validated”.

(Source)

The market didn’t really react to the news - but it definitely caught our attention...

Hard rock carbonatites are the same host structures that host $20BN MP Materials’ project, $19.5BN Lynas Rare Earths core asset and our Investment SGQ’s...

IF PNN can prove its Brazil project sits on a similar structure and has high enough grades it could be game on for its Brazilian rare earths asset.

(More on the Brazilian rare earths asset in a second...)

PNN just raised $4.1M at 10c, so they now have enough cash to progress both USA and REE projects.

We Invested in today’s PNN raise... and so did Tribeca Investment Partners.

Tribeca is a large resource specialist fund - so to see them come into an explorer like PNN is a good validation signal for us on our own Investment.

We have also had some success lately in stocks which Tribeca has also recently invested in:

- Locksley Resources - which is one of our most recent big wins, which at its peak was up 626% from our Initial Entry Price.

- Advance Metals, which is up over 200% from our Initial Entry Price.

- Rapid Critical Metals, which is up over 100% from our Initial Entry Price.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Today we are adding PNN to our Catalyst Hunter Portfolio, where we add our higher risk, higher reward, early stage exploration investments.

With PNN’s new US rare earths project, we want to see them roll out the “US critical metals play book”, which essentially runs like this:

- Bring on US government lobbyists to go for US critical minerals funding,

- OTC listing for exposure to US investors

- Get on the radar of US investors

- and maybe even some high profile appointments to strengthen the in-country team.

If PNN can attract attention of the deep capital pools in the US and the strength of capital flows into US critical metals projects, we hope PNN can get up to a much higher valuation.

We want to see PNN take advantage of these market dynamics and to raise enough cash to eventually make a discovery that is material for its market cap...

OR the US critical metals theme capital flows push PNN’s market cap to a point where it's able to use its balance sheet to pick up more advanced assets, also in the US...

(sort of like JBY did with their US gold “starter project” that allowed them to trade up to a market cap that was big enough to acquire a much larger silver project with a fully built processing plant)

Later in today’s note we will share our updated PNN Investment Memo which will cover:

- What PNN does

- The macro theme for PNN

- Our PNN Big Bet

- What we want to see PNN achieve

- Why we are Invested in PNN

- The key risks to our Investment Thesis,

- Our Investment Plan

But before that, here is a summary of the 10 reasons why we Invested in PNN.

10 reasons why we Invested in PNN

1. PNN has a US critical minerals project

PNN’s US project is 195km away from A$20BN MP Materials. More importantly, it's got heavy rare earth exploration potential (the less common and more valuable type of the rare earth materials). Both types of rare earth are needed for advanced magnet production the USA is seeking to onshore.

2. Strong macro theme #1: Capital is flowing into US critical metals macro thematic

We think PNN’s US rare earths project could attract increased capital flows into PNN.

We have seen this play out in other stocks where they list on the OTC, attract US attention and eventually capital.

3. PNN has a REE project in Brazil

PNN also has a rare earths asset in Brazil that we think could mirror a project that the market is really liking right now (SGQ’s project)

4. Strong macro theme #2: Capital is flowing into Brazilian rare earths projects looking for “the next SGQ”

We have had success with Brazilian rare earths assets before with SGQ which is up 500% in the last 9 months, and there will be investors who have made cash (and ones who missed SGQ) looking for “the next SGQ”. We think some of this cash could come into PNN.

(the past performance is not an indicator of future performance)

5. IF PNN attracts capital and re-rates to a valuation high enough it could acquire more advanced assets

IF PNN can attract enough capital with its current portfolio of assets, it can use its re-rated valuation to acquire more advanced assets.

6. We are Investing alongside Tribeca Investment Partners

Tribeca has come into three of our recent Investments - LKY (up 626% at its peak), AVM (up 250% at its peak) and RCM (up 151% at its peak).

We like their approach to resources investing and they have deep pockets.

The past performance is not an indicator of future performance.

7. We think it's the right time in the bull market cycle to get some exposure to exploration stocks

We think it's the right time to get set in junior explorers with new assets.

We think the next 6-9 months will see institutional capital finally coming back into the exploration sector after years of a capital drought.

We expect those capital inflows to increase the valuation of explorers with projects in the right commodities and the right parts of the world (like rare earths in the US or Brazil).

8. PNN also has advanced assets in an out of favour sector

PNN has advanced lithium projects in Argentina with one of them even having a Preliminary Economic Assessment done that shows an after-tax Net Present Value of US$308.8M.

We think that IF sentiment improves in the lithium sector these assets could justify PNN’s current valuation.

9. Uranium free kick on the new US project

All of the old exploration was focused on uranium - mind you that old drilling found uranium over at least 2km with grades as high as 1.3% in drilling and 1.786% in rock chips.

10. Gold free kick on the new US project

PNN’s new US asset was initially explored for gold. We could see PNN go back and look at the gold potential of the project.

Ultimately, we want to see PNN achieve our Big Bet which is as follows:

Our PNN Big Bet:

“PNN makes an economic discovery on either of its US or Brazilian rare earths projects and re-rates 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Our PNN Investment is centred around three macro thematics

Macro theme #1: Capital flowing into US exploration (PNN’s new US rare earths project)

We are seeing a wave of ASX listed juniors with US assets pop up and all of them are being re-rated and being given cash to explore.

Again, we want to see PNN take advantage of these market dynamics and raise cash to eventually make a discovery that is material for its market cap...

OR the capital flows push PNN’s market cap to a point where it's able to use its balance sheet to pick up more advanced assets, also in the US...

(sort of like our 2025 Next Investors Small Cap Pick of the Year, James Bay Minerals did with their US “starter project, then last week acquiring an advanced USA silver project)

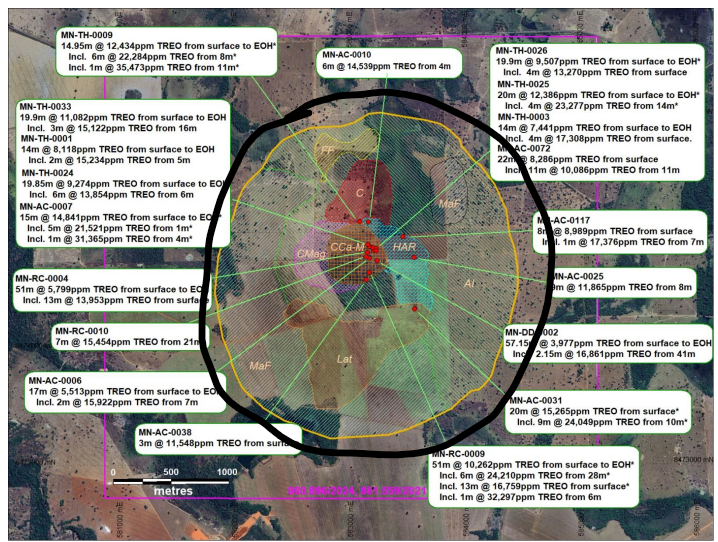

PNN’s new US project is in California - and it is going for heavy rare earths.

(but it is also be prospective for gold and uranium... we also like uranium and are patiently waiting for the uranium price to explode):

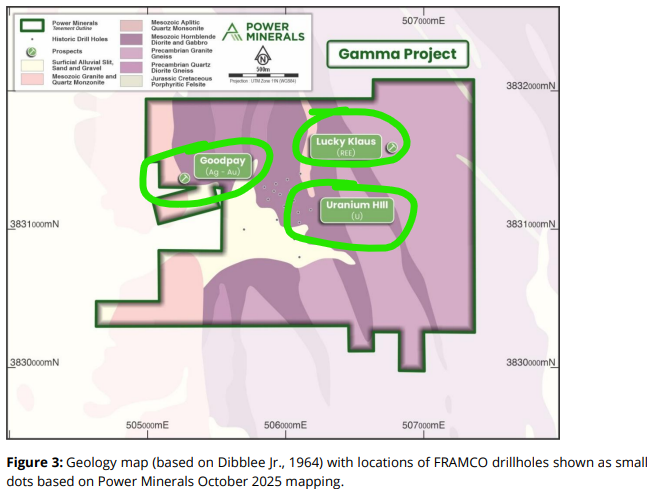

The project hasn’t been properly explored since the 1960s and 1970s, largely untouched since then.

Just recently, prospectors found rare earths, sampling as high as 2% TREO, split 50/50 light and heavy rare earths.

A good start and definitely prospects we want to see PNN run further work on as part of assembling drill targets in the future.

(Source: Today’s PNN announcement HREO = Heavy Rare Earths Oxides)

At the moment, the strike length of rare earths mineralisation is unknown...

It is very early days on the project, and we are most definitely in the “pre discovery” risky exploration phase - but that also means there is exploration upside.

Heavy rare earths are why we are here...

MP Materials (195km away) has recently received:

- A US$400M direct investment from the Pentagon into MP Materials.

- A US$500M offtake deal between Apple and MP Materials.

- A US$1BN loan commitment from JP Morgan & Goldman Sachs for MP Materials.

Most of MP Materials’ new cash is earmarked for “10xing its magnet facility” - they are literally calling it “the 10x Facility”.

Aside from delivering US onshore rare earths processing capacity, it will also create a big hungry plant which is (as the Wall Street Journal reported) going to need to ‘acquire more heavy rare earths’ which MP’s current mine just isn't able to provide:

(Source)

Which means MP will need a heavy rare earths feedstock...

Ideally from within the USA...

Heavy rare earths are critical components of advanced military technology like Tomahawk missiles and F35 jets... (and AI robots)

MP’s mine predominantly produces light rare earths, and a heavy rare earths supply outside of China is very hard to find.

This is a key part of the reason we are Invested in PNN and why a discovery by PNN could become valuable, so close to a A$20BN capped “potential buyer” of what’s found...

(again, early days - we are getting ahead of ourselves here, lets see PNN at least put a few drill holes down first)

We also note there is some gold and uranium history on the project - these could also become a big part of the story.

(this is the same as MP Materials mine - it was also previously prospective for gold and uranium until a rare earths discovery was found)

The last round of exploration on PNN’s new project was testing for uranium over at least 2km with drill results as high as 1.14% in drilling and 1.786% in rock chips...

As for gold, PNN said in today’s announcement the Gamma project was “initially explored for gold”.

Here are the three separate target areas on the project:

(Source)

Macro theme #2: Capital flowing into “the next SGQ”? (PNN’s Brazilian rare earths project)

One of the best performers in our Portfolio this year has been St George Mining (ASX: SGQ).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We still hold a large position in SGQ - in fact it's one of our biggest positions.

SGQ has the largest and highest-grade carbonatite-hosted rare earth deposit in South America and second highest grade REE deposit globally in the western world.

Despite being the second highest grade REE deposit in the world, SGQ trades at a discount to its REE peers... (fingers crossed the SGQ share price keeps running).

Our thinking here is that a lot of investors would have made money on SGQ (and hopefully will continue to do so).

And anyone who was in SGQ will be looking for a “SGQ 2.0” to add to their portfolio.

(some will have missed out on the first rally in SGQ’s share price too - those investors will be even hungrier for an opportunity at an “SGQ 2.0”).

Being Invested in SGQ means we have been monitoring other rare earths projects in Brazil that are in ASX listed names.

PNN’s Brazilian rare earths project was one of those that caught our attention.

There are a few minor similarities between the two projects, albeit SGQ is more advanced.

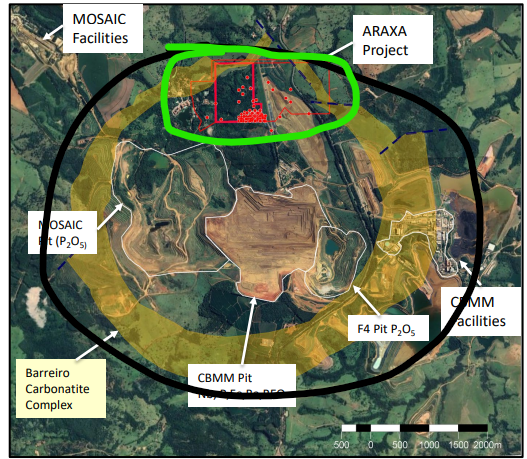

SGQ owns a section of a carbonatite complex (next door to the biggest niobium mine in the world owned by the giant (and private) CBMM, who owns most of the complex).

(Source)

PNN owns an entire complex - so if it can confirm that the rare earths sit inside a big carbonatite it could be a game changer for the company.

(Source)

At the moment, shallow holes near the surface show rare earths and PNN just recently said that its theory of a hard rock intrusion has been “validated”.

(Source)

Now we just need to see some deeper drilling and confirmation of a carbonatite at depth and it could be game on for PNN.

Anything is possible here, and in 12 months time we could be looking at a project that is ranking up there with SGQ’s...

But like any decent small cap ASX explorer, there’s a few more assets in the background...

Macro theme #3: Advanced assets in an out of favour sector (PNN’s lithium assets)

OK yes, no one cares about lithium right now - but that could change in the future.

PNN has a combined 714,864 tonne lithium carbonate equivalent (LCE) JORC resource estimate across three lithium assets in Argentina.

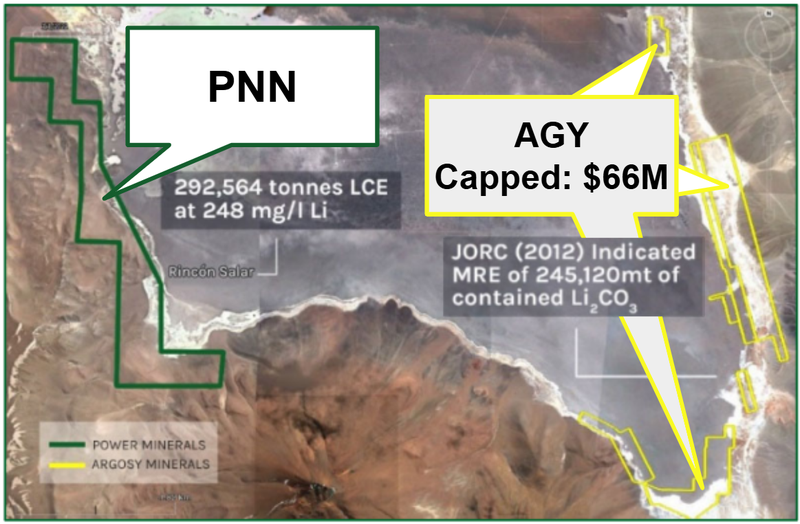

The first project sits on the fringes of the same salar where ASX listed Argosy Minerals and Rio Tinto have projects.

This is PNN’s most advanced asset, with a Preliminary Economic Assessment (PEA) done back in 2023 with a post-tax NPV of US$308.8M based on capital expenditure of US$216.55M.

(Source)

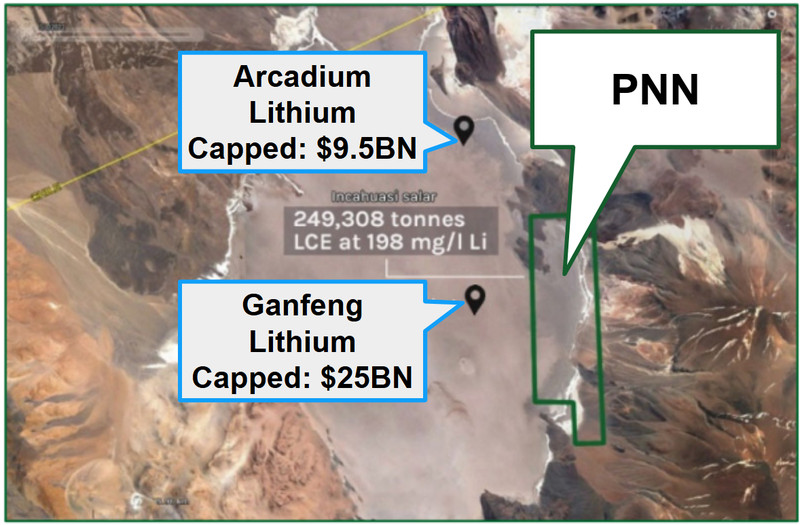

PNN’s second lithium project is on the eastern fringes of the Incahuasi Salar, immediately adjacent to Ganfeng Lithium Co. Ltd.’s project.

That project has a 249,308 tonne LCE JORC resource estimate.

(Source)

Both of these assets at the height of the 2020-2021 lithium bull run would have been worth 10s of millions of $ (if not in the hundreds of millions)...

But the world is different now and lithium is out of favour... for now.

What we like about these assets is that PNN has done deals on them to get them advanced by partners without having to spend any money on them during the down cycle in the lithium sector.

IF (or when?) sentiment turns, these could come back as big parts of PNN’s portfolio of assets.

Investment Memo 1: Power Minerals (ASX:PNN)

Memo Opened: 08-10-2025

Shares Held: 7,186,000

Options Held: 3,675,500

What does PNN do?

Power Minerals (ASX:PNN) owns a portfolio of exploration projects including:

- Rare earths in California, USA - early stage project where PNN is exploring for light and heavy rare earths in California 195km away from America’s only rare earths producing mine Mountain Pass owned by MP Materials.

- Rare earths in Brazil - PNN is aiming to unlock a hard rock carbonatite hosted rare earths discovery similar to two of the biggest operating rare earth deposits in the world owned by Lynas Rare Earths and MP Materials projects.

- Lithium in Argentina - PNN’s most advanced assets with a combined 714,864kt LCE JORC resource estimate across three projects.

What is the macro theme behind PNN?

Critical minerals and US-based projects are attracting attention and capital.

Trump is now looking to adopt pandemic-era level urgency to boost critical minerals production in the US.

With Trump signing Executive Orders to encourage US domestic critical metals production, fast track permitting and providing funding for mining projects private interest and capital has followed into the sector.

PNN has exposure to:

- Rare earths - a set of niche minerals used in the production of magnets for various military applications and AI.

- Lithium - a critical component for lithium-ion batteries, leveraged to electrification, energy storage and electric vehicle update.

Our PNN Big Bet

“PNN makes an economic discovery on either of its US or Brazilian rare earths projects and re-rates 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PNN Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 10 Reasons We Invested in PNN

- PNN has a US critical minerals project

- Strong macro theme #1: Capital is flowing into US critical metals macro thematic

- PNN has a REE project in Brazil

- Strong macro theme #2: Capital is flowing into Brazilian rare earths projects looking for “the next SGQ”

- IF PNN attracts capital and re-rates to a valuation high enough it could acquire more advanced assets

- We are Investing alongside Tribeca Investment Partners

- We think it's the right time in the bull market cycle to get some exposure to exploration stocks

- PNN also has advanced assets in an out of favour sector

- Uranium free kick on the new US project

- Gold free kick on the new US project

What do we want to see PNN do next?

Objective 1: Target Generation on US rare earths project

We want to see PNN sample, map and run geophysics on its US asset to identify priority drill targets.

Milestones:

🔲 Mapping and sampling (soil and rock chips)

🔲 Geophysics

🔲 Drill targets confirmed

Objective 2: Drilling on PNN’s US rare earths project

After PNN has identified priority drill targets, we want to see the company drill the project.

Milestones:

🔲 Drill permitting

🔲 Drilling

Objective 3: Macro objectives

We want to see PNN go after fast tracked permitting and non-dilutive funding opportunities that are available for US critical minerals projects.

Milestones:

🔲 Fast-tracking permitting

🔲 Non-dilutive US critical minerals funding opportunity applications

Objective 4: Drilling at Brazilian rare earths project

We want to see PNN drill out and define a maiden JORC resource estimate in Brazil to enable comparison to peers.

Milestones:

🔲 Geophysics/Geochemistry work

🔄 Drilling starts

🔄 Drilling results

🔲 Maiden JORC resource estimate

Objective 5 (Bonus): PNN uses its market cap to acquire more advanced assets

This one would be an unexpected surprise to the upside (depending on what assets PNN can acquire).

What are the risks?

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should rare earths prices fall, this could hurt the PNN share price.

Permitting Risk

PNN will need to get permitting in order for its rare earths project in the US. If this permit is delayed or rejected it may be a drag on the PNN share price.

Funding risk/dilution risk

As a pre-revenue small cap company, PNN is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, PNN could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking PNN’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other risks

PNN is an early-stage explorer with projects in the USA, Brazil, and Argentina. None are producing, and there is no certainty exploration will lead to an economic discovery.

The company’s value is highly exposed to sentiment in the rare earths and lithium markets. Prolonged weakness in these commodities could affect funding access and share price performance.

As a pre-revenue small cap, PNN depends on capital raisings to advance its projects. Any new equity issues may dilute existing shareholders, and financing may not always be available on favourable terms.

Multi-jurisdiction operations bring permitting and regulatory risks, including possible delays or policy changes that could affect project timelines.

Finally, general market or sector downturns could impact PNN’s share price regardless of company progress.

Investors should consider these risks carefully and seek professional advice before investing.

What is our Investment Strategy?

We are adding PNN to our Catalyst Hunter Portfolio.

Our plan is to hold PNN in line with our Trading Blackout and hold conditions for the Catalyst Hunter Portfolio.

PNN is an early stage, small cap, high risk, high reward Investment.

In 12 months, a discovery on either of two rare earths projects OR a bull market in the lithium space will mean our Investment in PNN pays off.

There is no guarantee PNN finds anything of value, but if they do then we would hope to see its share price re-rate to a level multiples of our Initial Entry Price.

If none of the three scenarios happen, then we fully acknowledge that we may be down on our Investment.

Check out the detailed hold conditions for our Catalyst Hunter Portfolio here.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.