Our Key Takeaways from VUL’s PFS - What will the VUL share price do next?

Vulcan Energy Resources Ltd (ASX:VUL, FRA:6KO) is our top ASX pick to ride the global Electric Vehicle Boom of the next decade.

VUL today is one step closer to producing Zero Carbon LithiumR in Europe, and supply to EU battery makers.

For us, a stock like this comes along once in a lifetime.

VUL’s phenomenal run has seen it evolve into a Tesla-like share price story on the ASX - a market favourite that just keeps rising and rising on the back of the hottest global investing theme in decades:

The Electric Vehicle Boom.

And like Tesla, just when you think VUL can’t go any higher - it does... again, and again, and again.

VUL is the largest holding in our portfolio.

VUL has just released its much anticipated Pre Feasibility Study, and it’s a big one.

In this note, we will talk about our four key takeaways from the PFS, what VUL is going to focus on next and what we think the VUL share price could do from here.

First, our key takeaways from the PFS:

Key Takeaway #1:

The first thing that jumped out after opening the PFS announcement, is the enormous...

Net Present Value of €2.25 Billion (that’s $3.55 Billion AUD).

This is AFTER tax.

$3.55BN AUD is way bigger than we were expecting, especially given that at around $5/share, VUL is valued under $400M.

The top global lithium producers are capped at $32BN, $24BN, $17BN and $9BN dollars - more on this further down.

While there will be dilution for VUL shareholders to raise the cash needed to develop their project over time, we are excited by the potential for VUL to reach a multi billion dollar valuation like other producers.

Keep in mind there is no local lithium production in Europe... yet.

Earlier this week we discovered that influential German investment analysts Der Aktionär have set a share price target on VUL of €6 (that's A$9.50).

Key Takeaway #2:

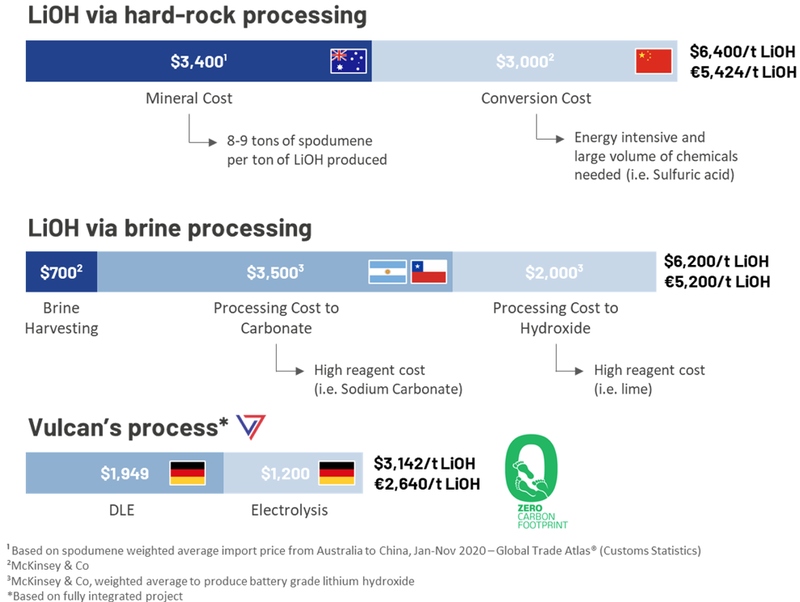

The second thing we noticed is that VUL’s Opex (operating expenses) to pull out one tonne of Zero Carbon LithiumR Hydroxide is €2,640 per tonne.

This means VUL has:

Opex per tonne lower than any current operation globally

Key Takeaway #3:

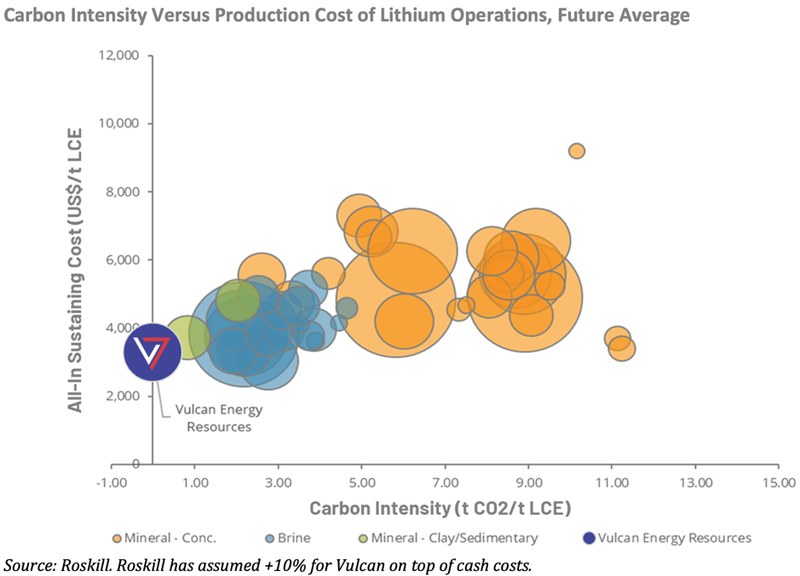

In addition to the lowest financial operating cost, VUL will also have the lowest CO2 footprint of any lithium operation globally: ZERO!

Last month, the EU announced new regulations on the carbon footprint of EV batteries. In the coming years, there will be regulatory limits on carbon generated in their production. Batteries with the highest carbon footprint will be banned.

The EU is aiming for carbon neutrality by 2050.

VUL’s world first Zero Carbon Lithium is exactly what governments, battery makers, and EU focused funds are looking for.

You can see VUL sits at the very lowest of carbon intensity and production costs on this curve:

Key Takeaway #4

The fourth thing we noticed is that to build this operation it’s going to require €1.74BN. We believe VUL is in a perfect “sweet spot” to secure this financing:

- Lithium Price is forecast to enter boom territory in the coming years and has already started rising.

- EV adoption ramping up in Europe (EV sales up 66% year on year) and globally.

- There is currently no local supply of lithium in Europe. 80% of global supply is controlled by China. The EU is desperate for its own supply of this critical metal.

- European Union is deploying cash to drive the EV sector forward, is banning combustion engines, and has generous policies for battery investments.

- Fund managers, investment banks and green funds are looking to put cash to work in this low interest rate and fiscal stimulus environment.

But most importantly: Remember EIT InnoEnergy?

VUL is one of only two lithium projects financially and administratively backed by EU-group EIT InnoEnergy, which is the founder and steward of the European Battery Alliance, that counts among its members the most significant financiers of battery metals, battery and electric vehicle projects in Europe including the European Investment Bank.

Remember that InnoEnergy liked VUL so much they actually invested in VUL (announced July 8th 2020) - this means InnoEnergy will be even more motivated to help secure VUL’s CAPEX financing through their extensive European network.

InnoEnergy has placed VUL on its Business Investment Platform, through which it is further assisting VUL with conversations with European financiers.

The size and location of the deposit, together with other strong project fundamentals, in the middle of large end users associated with European electric vehicles that is driving lithium demand, makes the project a strategic asset - as evidenced by the large interest shown in the Project by public/private banks, financiers, end users and large lithium specialist companies to-date, as stated by VUL in their announcement today.

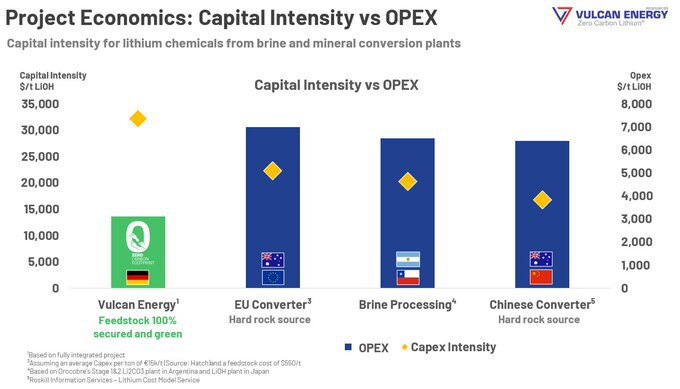

Here is the capital intensity versus opex other types of lithium production - showing VUL will have a higher CAPEX, but much lower OPEX operation relative to industry peers.

VUL will uniquely also produce geothermal energy, providing stable revenue with the high fixed feed in tariff in Germany, a key industry differentiator.

So where to from here?

2021 is shaping up to be another transformative year for VUL.

The PFS has set the stage for the company’s next phase of growth.

Key milestones to look out for in the year ahead are:

- Start of the Definitive Feasibility Study (DFS), which will build on the PFS. This is the next big step toward production, firming up the project economics further still and presenting the investment case to financiers;

- Scaling up of Lithium Extraction test work and piloting;

- Securing all important offtake agreements - this is when customers agree to buy future Zero Carbon Lithium produced by VUL.

All of the above will contribute to de-risking the project and securing the finance to bring VUL’s project into the world.

So what will the VUL share price do now?

VUL is our largest holding and we intend to maintain a position over the coming years.

The world is clearly at the beginning of a global boom in Electric Vehicles, and has undoubtedly pivoted to green and sustainable investments.

You can see it every day across all forms of media and news.

The heavyweights of the lithium industry are capped at billions of dollars - Ganfeng Lithium Co Ltd is capped at $32BN, Albemarle - $24BN, Tianqi Lithium - $17.4BN, while SQM is capped at $9BN (figures are all in $AUD).

Aspiring producer VUL was capped at less than $0.4BN just prior to today

None of these multi billion companies are Zero Carbon LithiumR producers like VUL is planning to be - Zero Carbon LithiumR is what the European Union desperately needs.

So what could the VUL share price do now?

No one really knows, but hopefully it will keep doing what it’s been doing as a standout performer and the Electric Vehicle Theme favourite of the ASX.

Just look at Tesla (NASDAQ:TSLA) - the NASDAQ favourite and the USA’s poster child of the EV boom.

People were surprised to see Tesla’s share price rise from $88 in January 2020 to $180 in February...

and then $300 in July... then $400 by August...

And now Tesla is over $850...

Holders continue to hold, and those Tesla short sellers just get burned again and again...

We are in the midst of an EV boom which could go for the next few years, and are backing market favourite VUL to continue to deliver.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.