ONE: share price going up - is this why?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,573,594 ONE Shares and the Company’s staff own 90,000 ONE Shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Looks like the market likes what our medical-tech Investment OneView Healthcare (ASX:ONE) has been cooking up over the last couple of months.

ONE’s share price has moved from a low of 16.5c in late October to ~40c now:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Today we will cover our “view” of what could be making the ONE share price keep moving up and up...

But first, a quick reminder of what ONE does.

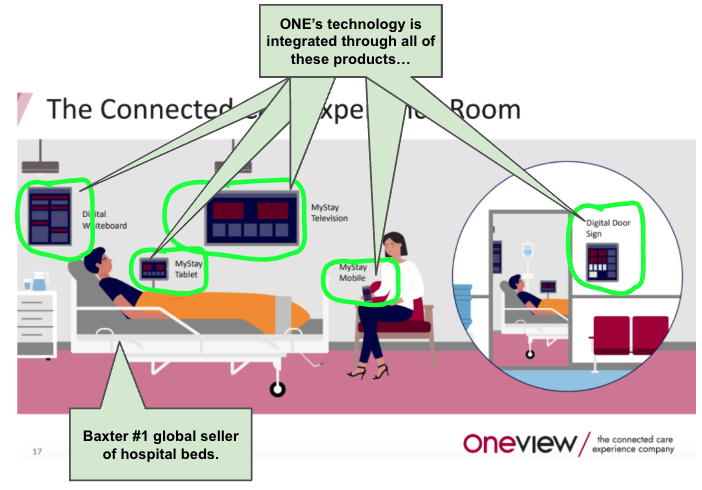

ONE sells technology to hospitals that improve the patient and care experience.

It connects the patient in the hospital bed to nurses, doctors, medical specialists, meal service, records, educational content, and entertainment.

ONE helps make hospitals run better and more efficiently.

(and for anyone that has been to or worked at a hospital, despite healthcare workers doing their best, it can be an incredibly inefficient place at times)

In February 2024 ONE launched a BYOD (“Bring Your Own Device”) offering named ‘MyStay’ Mobile.

Hooking into a patient’s own device makes it easier for hospitals to purchase and roll out ONE’s technology, because they don’t have to buy and install bedside tablets or upgrade their existing in-room TVs.

ONE also just launched a new AI virtual assistant - further reducing pressure on nurses’ time by answering commonly asked patient questions.

ONE makes money by selling its tech into hospitals - mostly on a “per hospital bed installation” for which they charge a recurring yearly license fee.

When we first invested in ONE back in March 2021 it had 9,000 contracted beds.

Most recently it has ~19,000 contracted beds (source), with 14,880 live “end-points” (source).

(an end-point refers to each individual device or interface through which their Care Experience Platform is deployed and accessed, like a TV, bedside tablet, mobile phone or digital whiteboard etc)

In June 2023, ONE signed a “Value-Added Reselling” agreement with US$10BN Baxter International (NYSE: BAX) - the biggest hospital bed provider in USA, with a 75% market share of 500,000 beds.

A good match given Baxter sells hospital beds to hospitals, and ONE sells the tech product that improves the experience in a hospital bed - a symbiotic relationship:

(source)

Under the “Value-Added Reselling” Agreement, the companies collaborate to integrate and sell the combined Baxter and ONE products.

Then the giant Baxter sales team sells the combined offering...

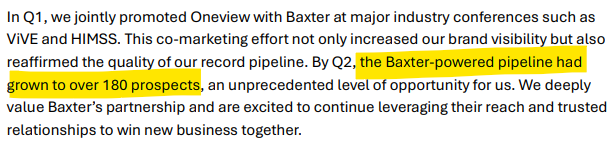

A few weeks ago, ONE CEO James Fitter said the Baxter driven pipeline of ONE sales had grown to 180 opportunities:

(source - read it here)

And as we saw with ROC, we just need that pipeline to start converting to deals for the major rerate...

OK, so what is making the ONE share price go up?

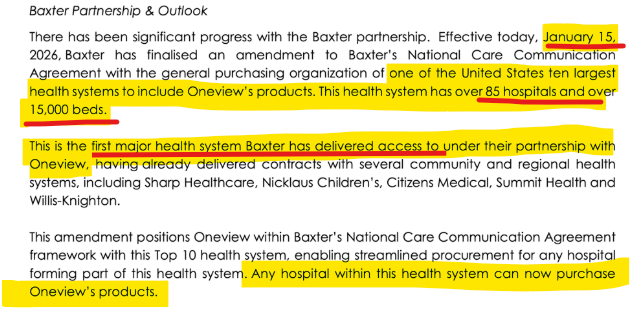

Reason #1: ONE was just added to the "approved tech to purchase" list at a major Baxter client with 15,000 beds

After many years of work and relationship building with Baxter, last week ONE announced Baxter had given them access to one of their key clients.

Baxter added ONE’s products to the “approved purchases menu” with a major US hospital network - 85 hospitals and 15,000 beds.

(Source)

ONE’s products are now on the approved list of things the hospital can buy, making the purchase and roll out of ONE much easier.

15,000 potential beds, they just need to choose ONE of the “approved add-on menu” for any of their 15,000 hospital beds.

Think of it, for example, like you being only ever allowed to eat food from Uber Eats, you are restricted to what restaurants are on the app.

And ONE just got onto this giant hospital network’s approved tech “menu”.

(we can’t stress how important this is - hospitals are notoriously hard to sell into)

Now over to the ONE and Baxter sales teams to encourage uptake and convert to contracted beds for ONE (ie annual recurring revenue).

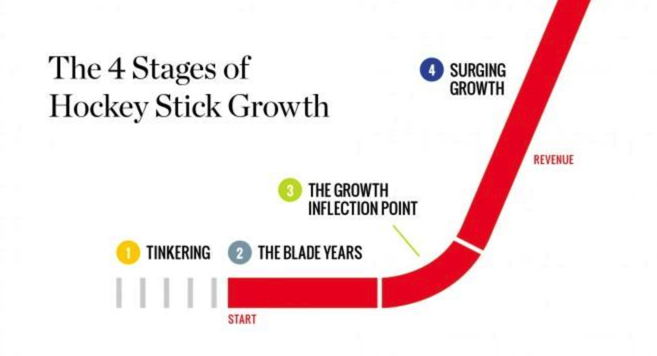

Reason #2: Market starting to believe Baxter agreement will lead to “hockey stick” revenue growth?

The market got excited when the Baxter reseller agreement was signed back in 2023.

But building trust, internal + external awareness and traction has taken a while.

ONE’s recent announcement that Baxter had allowed them into a major client hospital network is a huge vote of confidence in the partnership.

We have always believed the Baxter partnership could eventually lead to the “hockey stick ARR growth” we want to see that rerates our tech stocks.

(‘hockey stick growth’ can describe a business’s rapid, exponential increase in revenue after a long period of slow, flat, or linear growth - forming a curve that resembles a hockey stick... )

(Source)

So is the market starting to believe the Baxter agreement is going to deliver the hockey stick for ONE?

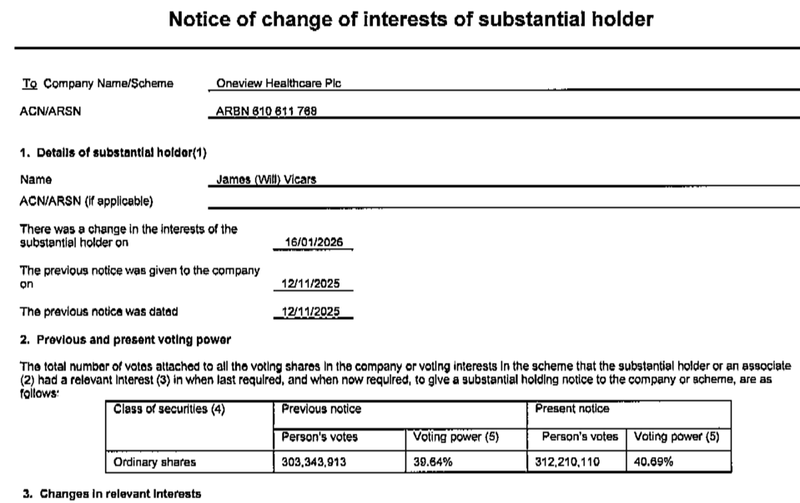

Reason #3: Major shareholder buying on market, now owns 40.69% of ONE

Will Vicars keeps increasing his holdings of ONE shares, now owning 40.69%.

Will Vicars is the Joint Chief Investment Officer at Caledonia, Australia’s largest and most private hedge fund, with billions of dollars of funds under management.

Vicars has been backing the company since 2013 when it was a private company.

In his role at Caledonia, Vicars has developed a reputation for identifying powerful commercial trends and themes in global markets and getting in early as they emerged.

Caledonia does not invest in many stocks - it places concentrated, high conviction bets - so it's interesting to see their co CIO so committed to ONE.

The fund’s strategy is to invest in high quality businesses “where long-term ownership is rewarded" - and typically has an investment horizon of 8 to 10 years.

All good news for our shared Investment in ONE.

Having major shareholders with a long term horizon and high conviction is a big plus for an emerging high growth technology company.

With Vicars continuing to buy ONE shares on market, that means there’s less and less free float for any other buyers to take up - less shares on market = higher ONE share price.

(Source)

Reason #4: Market likes ONE’s AI adoption into its products

ONE jumped on the Artificial Intelligence (AI) train very early, baking AI into its products and internal coding processes.

(ONE CEO James Fitter talks about how much ONE have been deploying AI into the business and products in this interview at around 10m30s - the whole thing is worth a watch for a general update on ONE too)

We have had success Investing in companies with deep knowledge in a niche domain that combine AI to solve problems in that domain.

(as opposed to many other “generalist” AI companies that make AI tools for broad application.)

Another one of our tech Investments Rocketboots (ASX: ROC) sells an AI-driven platform for retail and banking - analysing in-store camera feeds to optimise workforce, prevent theft/fraud at checkouts (like missed scans), and improve overall customer experience through automated insights and alerts for businesses.

With that AI driven solution to a very specific domain, ROC is up 108% in last ~5 weeks:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Another of our tech Investments, EchoIQ (ASX: EIQ), uses AI to analyse echocardiograms (heart ultrasound scans) to detect structural heart diseases, by identifying patterns and building 3D heart models.

Once again, an application of AI in a very specific domain. EIQ is up 84% in the last 3 weeks:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Maybe the market is starting to generally move into the “combining AI with deep domain expertise” theme?

Or maybe it’s all just a coincidence...

Or maybe we are good at picking tech stocks and should focus full time on tech investing?

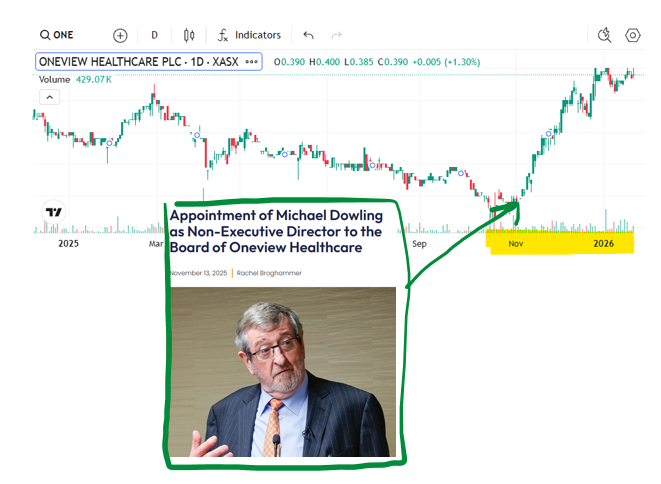

Reason #5: Epic new director Michael Dowling joins ONE board

In November, ONE added a new Non-Executive Director, Michael J. Dowling, CEO Emeritus of Northwell Health and Time Magazine 2025 top 100 Titans of health (read the announcement here)

(source)

Michael was President and CEO of Northwell Health for 23 years, so has decades of leadership experience in healthcare innovation.

Northwell Health is New York's largest healthcare provider, serving NYC, Long Island and Westchester.

(A “CEO Emeritus” is a former CEO who remains associated with a company in an honorary, advisory, or consultative capacity after retiring from the active role, retaining the prestigious title but not the day-to-day duties, signifying lasting respect and valuable experience.)

TIME Magazine named him a “Titan” on the 2025 TIME100 Health list, and he led Northwell to become the only health system on TIME’s 2025 Most Influential Companies list.

He has also been ranked on Modern Healthcare’s 100 Most Influential People in Healthcare list for 16 consecutive years, achieving the top spot in 2022.

We note that ONE’s share price run kicked off at around the time of Michael’s appointment...

Maybe he’s been telling his high profile health industry buddies to jump on board ONE?

(as customers OR even shareholders?)

Who knows...?

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Whatever the case, with Michael joining ONE as a Non Exec Director, ONE can benefit from his decades of experience and relationships in the USA healthcare industry.

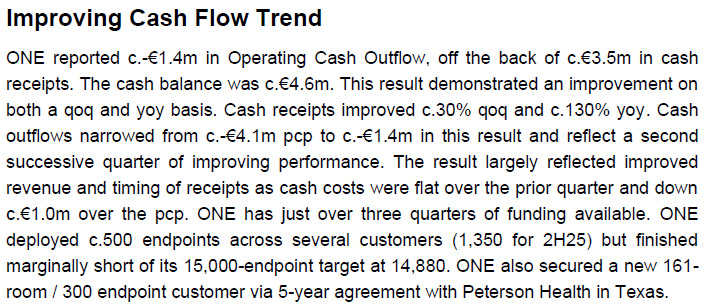

Reason #6: Revenue up and costs down

ONE put out its most recent quarterly last week, showing a net operating cash outflow of 1.4M euros (A$2.5M) during the quarter compared to 4.1M euros in the same quarter of the previous year.

Receipts from customers totalled 3.5M euros (A$6.3M), compared to 1.5M euros in the same quarter of the previous year.

So while ONE is not cash flow positive just yet, it's burning much less cash compared to last year, and its revenue has grown.

(and we could start seeing some of those 180 Baxter led opportunities in the ONE pipeline start coming through soon)

By the way, the Bell Potter analyst Martyn Jacobs who wrote the ONE report revised its price target up to 50c for ONE.

In summary

ONE’s recent share price performance likely comes down to some sort of combination of the above six reasons.

But in reality the main thing that is going to get the $295M market cap ONE to a multi billion dollar plus valuation is by rapidly growing its Annual Recurring Revenue (ARR).

This is what ASX market darling med-tech monster Pro Medicus has done over the last 10 years.

The main thing we are watching out for with ONE is how many new beds and hospitals the company’s technology is being deployed to, and how quickly.

(more AND faster annual recurring revenue growth is what makes tech stocks’ share prices re-rate)

It’s the “hockey stick” revenue growth that will convince the market to materially bid up the ONE share price.

(Source)

And we think the Value Added Reseller (VAR) agreement with Baxter is ONE’s most likely pathway to achieve the coveted “hockey stick growth”.

And after 3 years of working with Baxter there have been many positive signs showing the partnership is gaining traction:

- Agreement extended in 2024 (read our comments here)

- Plenty of co-marketing materials released on Baxter website and Social Media - read our comments here)

- Training of 100 plus Baxter sales team on ONE products

- A few new hospitals deals

- Increase from 139 Baxter led pipeline opportunities to 180

- And last week Baxter added ONE to the “approved products menu” of their major key client - 85 hospitals and 15,000 hospital beds

It looks like the Baxter-ONE partnership is gaining traction and we hope that 2026 is the year where it delivers the hockeystick ARR growth for ONE.

Our ONE Big Bet

“ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward annual recurring revenue) and be acquired by a large health tech provider.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

What are the risks for ONE right now?

The two key risks to our ONE Investment in the short term are “sales risk” and “funding risk”.

Sales Risk because there is no guarantee that ONE hits sales guidance that is in the market (and likely to be priced into the company’s valuation).

There is also a chance that the sales pipeline won't convert as quickly as we would like.

Large institutions like hospitals don’t tend to adopt new technology very often and the sales cycle can be long.

This feature of ONE’s customer base can cause delays in sales that drag out over a long time.

Macro factors in the market including a recession can cause a reduction in spending on new technology, affecting ONE’s ability to make sales.

Funding risk is also one thing we think could impact ONE’s share price in the near term.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE

- Why we Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.