NTI clinical data in hand - now entering “deal making” mode

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,020,000 NTI shares and 350,000 NTI Options at the time of publishing this article. The Company has been engaged by NTI to share our commentary on the progress of our Investment in NTI over time.

49 deals with disclosed values totalling US$13.2BN - in one year alone.

That’s for biotech deals involving rare neurological diseases in 2023.

Over the last few years Neurotech International (ASX:NTI) has been gathering a significant amount of clinical evidence that its product NTI164 is effective in treating multiple neurological disorders in children.

It’s now ready to take it to market.

Over the last 9 months NTI delivered positive clinical trial data from for three different neurological disorders.

NTI is now ready to find deeper pocketed partners that have the balance sheets to fund additional clinical trials in the US, Europe and Asia, and steer through the regulatory pathways to get a product into patients hands.

Securing a commercial partner to fund (and share in the upside) of its treatment offshore would be a major catalyst for NTI.

Multi-billion dollar deals can happen for small biotechs.

Neuren Pharmaceuticals signed a US$1BN global license deal for its product, with a 10-20% royalty on sales. This was for one rare indication only - Rett Syndrome.

That commercial deal helped drive Neuren from a $100M capped stock to a peak market cap above $3BN.

NTI has proven in Phase II trials that its product is safer and just as effective as Neuren’s product for treating Rett Syndrome...

Jazz Pharma paid US$7.2BN for the developer of a cannabinoid product called Epidolex - forecast to deliver US$1BN in sales this year after delivering US$731M in 2022.

Like Epidolex, NTI’s product is cannabinoid derived...

While it shops around the opportunity to bring its product to market offshore, here in Australia NTI will be working towards provisional approvals with the local TGA.

A provisional registration pathway can save up to 2 years of development, and potentially make NTI's product eligible for reimbursements.

NTI remains well funded for this strategy, with $11.6M in the bank at the end of last quarter.

Its current balance sheet gives it the financial breathing room to shoot for a partnering deal with a bigger partner to take care of overseas markets, and also removes the ‘near term cap raise’ / ‘how will they ever fund this’ suspicion that dogs a lot of pre-revenue small cap biotechs.

This is the strategy that NTI will be adopting over the next 12 months - pursue partners for overseas work, while it focuses 100% on the Australian market.

In this note we will cover:

- what we think of NTI’s strategy going forward,

- what we look forward to - in our new NTI Investment Memo, and;

- Evaluate the past ~12 months of our NIT Investment, relative to our first NTI Investment Memo.

It's been almost a year since we Invested in NTI. And it has accomplished A LOT in that time...

NTI’s primary treatment / lead product is a cannabinoid derived biopharmaceutical called NTI164.

Since we first Invested in September 2023, NTI has has delivered three successful clinical trials for its lead product:

- PANDAS/PANS - Phase I/II trial showed clinically significant and meaningful improvements in clinical function, with excellent safety and tolerability over 12 weeks”

- Rett Syndrome - Phase I/II trial had an excellent safety profile compared to the leading drug DAYBUE, as well as clinically significant efficacy results that continued to improve over time.

- Autism Spectrum Disorder - Phase II trial showed that after 12 weeks of receiving NTI’s product patients with severe ASD improved to the point where symptoms are present but barely noticeable.

With these results in hand NTI is now moving into the next phase of bringing its product to market.

NTI’s strategy can be broken down into two distinct parts:

- Secure a cashed-up partner to support the global development of NTI164 (US, Europe and Asia).

- Progress NTI164 in Australia locally through to commercialisation through accelerated regulatory pathways.

Think globally, act locally...

There are quite a few milestones that NTI will need to achieve in order to progress both of these strategies.

First will be the pre-clinical toxicology and pharmacokinetic trials which are needed for regulatory applications, and then it will be the Orphan Drug Designation applications across the EU/US for PANDAS/PANS and Rett Syndrome.

NTI is funded to achieve these milestones with $11.6M in the bank at the end of last quarter, which gives the runway it needs to execute on this strategy over the next 12 months.

The big surprise catalyst for NTI over the coming months would likely be a global partnership deal that shares costs (and upside) to progress offshore development...

(because ultimately, that’s where the big money is - and it could come at any time...)

Armed with data - NTI is aiming for a global partner

NTI will look to complete FDA Investigational New Drug (IND) approval for at least one of its targeted neurological disorders.

IND approvals essentially give the greenlight for more studies - so they are important.

To do this NTI will look for a strategic partner to support the funding of further trials and drug commercialisation.

NTI is in a very strong position to negotiate a deal because of the strong data and results it has collected over the last 12 months.

Transaction licence? Equity investment? M&A?

This week NTI said that the partnership could take various forms.

A big “out of the blue” partnership deal for a global market would be an unexpected catalyst that re-rates NTI’s share price higher.

We have seen these types of partnering deals act as catalysts for other biotech companies in our Portfolio.

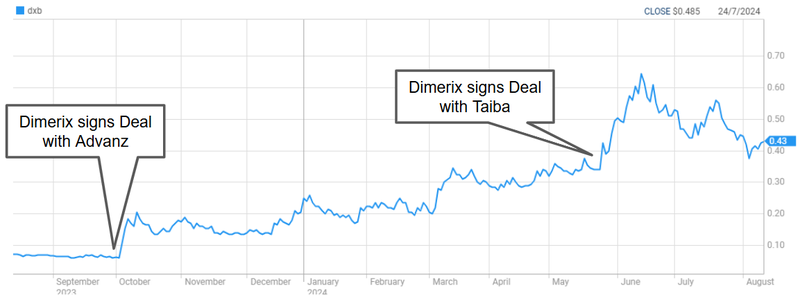

Dimerix was trading at just 6 cents when it announced a $230M commercialisation deal with Advanz Pharma in Europe, Canada, Australia and New Zealand.

Dimerix’s market cap before that deal was ~$24M - at its peak it hit ~$330M.

See our coverage of that Dimerix news here: DXB signs $230M Commercialisation Deal for ~20% of the global market

DXB’s share price spiked on the news, and the company’s value has gone on to climb to a peak of 60 cents after a second commercialisation deal was announced with Taiba covering parts of the Middle East.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

A licensing deal was also a cornerstone of the Neuren Pharmaceuticals story - taking the company from a ~$100M market cap to a peak of ~$3.3BN in the space of 3 years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But it's not just smaller companies chasing bigger ones - Big pharma is also in the market for deals that work for its shareholders too.

And this week we read in the Wall Street Journal that after years of spending tens of billions of dollars on massive acquisitions, the really big end of town is starting to look at smaller opportunities... which are sub “$5BN” (still massive for us small cap ASX investors...)

Perhaps if big pharma is looking to pay less than $5BN for deals, it might come looking over to Australia for new deal flow?

There’s always plenty of deal making action in the biotech/pharma industry, and we are very keen to see what NTI can pull off.

Of course these deals do take time - soliciting bids, negotiations, nailing deal structures, then finally executing on a deal...

... and they can often come out of the blue (like they did with Dimerix) - catching the market off guard.

So while it has the clinical data in its hands, NTI could take some time to secure a deal.

Like most investing, this is a game of patience.

The good thing is that NTI does not intend to “go it alone” overseas on what can be quite expensive endeavours - this will preserve its precious cash and minimise shareholder dilution... to be in the best possible shape for a (hopefully) company making offshore partnership deal.

External validation for biotech companies come in two forms, either through a large commercial deal (like the one Dimerix signed) or through regulatory approval.

Ultimately, smaller shareholders that aren’t trained doctors or scientists (like us) can only make assumptions about the results that the company publishes.

Whether the product is able to be commercialised depends on the regulator and ideally a large commercial biotech with deep technical and distribution capabilities.

From a local perspective, NTI will look to appease the Australian regulator and secure a fast tracked pathway to production for one of its target conditions.

This is the second part of its two pronged approach.

NTI’s local Australia strategy

Here in Australia, NTI will look to follow the provisional registration pathway set out by the TGA (the drug regulatory body in Australia) for one of its target conditions.

A provisional pathway allows NTI to save years of time and millions of dollars.

NTI will seek approval for PANDAS/PANS and Rett Syndrome first.

NTI expects pre-submission meetings with the TGA to start in Q2 2025 with applications planned in 2H of 2025.

The TGA registration process takes approximately ~220 working days so the big news could be at some point in 2026.

This choice was made because PANDAS/PANS and Rett Syndrome are rare neurological diseases that could be eligible for “orphan drug status” in Australia and around the world.

Side note - what are orphan drugs again?

Orphan drugs are treatments developed for rare diseases that affect a small number of people.

Governments provide incentives to pharmaceutical companies to encourage the development of orphan drugs, as these diseases would otherwise be neglected due to the small potential market size.

Some key incentives for orphan drug designation include:

- Fast tracked approvals: Companies may not need to complete a full Phase III clinical trial to get the product to market.

- Market exclusivity: Once approved, an orphan drug gets 7 years of market exclusivity in the US and 10 years in Europe.

- Orphan drug pricing: Orphan drugs can be priced at higher levels to incentivize development, with the average price around $32,000 per patient per year in the US (paid by governments/insurers).

Back to NTI’s work in Australia...

Relative to the global market Australia is a lot smaller when it comes to Total Addressable Market size BUT progress with approvals here in Australia is likely to have flow on effects around the world.

And we think there is still a meaningful market for these products within Australia:

Ultimately, we think that NTI has a very good opportunity to execute on its forward strategy, and although the risk points for the company move away from “clinical trial risk” to “deal and regulatory risk”, there are plenty of catalysts to look forward to for the company, and it has the cash to deliver on them.

Given the company’s new strategy has been outlined this week, we have created a new Investment Memo for NTI to track this next stage of development.

Our new NTI Investment Memo

Today we will be launching our new NTI investment Memo where you can find:

- What does NTI do

- What is the macro theme

- Why we are Invested in NTI

- Our long term Big Bet - what we think the upside Investment case for NTI is.

- The key objectives we want to see NTI achieve

- The key risks to our Investment thesis

- Our Investment Plan

We will also be doing a retrospective review of our first NTI Investment Memo, checking to see how the company performed against our expectations. That retro is further down in today’s article.

Investment Memo: Neurotech International (ASX:NTI)

Opened: 14-Aug-2024

Shares Held at Open: 8,020,000

Options Held at Open: 350,000

What does NTI do?

Neurotech International (ASX:NTI) is a clinical stage biotech company.

NTI aims to treat rare and severe neurological disorders predominantly in children.

NTI’s primary treatment is a cannabinoid derived biopharmaceutical called NTI164.

NTI is seeking to prove that NTI164 is a both safe and effective treatment for disorders such as Autism Spectrum Disorder, Rett Syndrome, PANDAS/PANS and Cerebral Palsy.

NTI is advancing clinical trials to gather evidence, and is exploring global partnership opportunities to bring its product to market.

What is the macro theme?

Biotech investing can be rewarding from both a human perspective (saving lives, patient outcomes improving) and financial perspective (company making scientific breakthroughs can deliver big returns).

NTI is focussed on neurological disorders mostly in children, across potential orphan drug indications for rare conditions, such as Rett Syndrome as well as disorders that have larger total addressable markets such as Autism Spectrum Disorder (ASD).

Our NTI Big Bet

“NTI re-rates to a +$500M market cap by successfully advancing one or more of its clinical trial programs through to regulatory approval, partnership/licensing and/or is acquired by a large pharmaceutical company”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our NTI Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in NTI?

Clinical trials have demonstrated that NTI’s product helps treat neurological disorders

- PANDAS/PANS - Phase I/II trial showed clinically significant and meaningful improvements in clinical function, with excellent safety and tolerability over 12 weeks.

- Rett Syndrome - Phase I/II trial had an excellent safety profile compared to the leading drug DAYBUE, as well as clinically significant efficacy results that continued to improve over time.

- Autism Spectrum Disorder - Phase II trial showed that after 12 weeks of receiving NTI’s product patients with severe ASD improved to the point where symptoms are present but barely noticeable.

Targeting Orphan Drug Designations (ODD) for rare diseases

We like NTI’s strategy of focusing on Orphan Drug Designations for rare diseases. These treatments have a small patient pool because diseases are rare. Due to this, there are significant unmet needs, and treatments attract premium pricing.

Successful orphan drug treatments are highly valued by the market.

NTI following the multi-billion dollar Neuren Pharmaceuticals playbook

ASX listed Neuren Pharmaceuticals has grown more than 3,000% (~$100M market cap to a peak market cap of ~$3.3BN) off the back of commercialising its treatment for the rare disease Rett Syndrome.

NTI is trying to replicate Neuren’s path to success through its own orphan targets.

Potential for “out of the blue” global markets commercialisation deal

NTI is on the hunt for a commercial partner to develop its product NTI164 overseas (US, EU, Asia).

Any partnership or commercialisation deal will significantly defray the financial and clinical risk for the company, and is a large potential catalyst for the company if signed.

Successful biotech fund, Merchant Group, has a substantial position in NTI

Merchant Group became a substantial shareholder of NTI with a 5.01% stake when NTI was trading at ~9 cents and has recently been adding to its position in the company. As of March 2024 Merchant owns 7.12% of NTI.

We have followed Merchant Group’s investments closely and successfully Invested in a number of them (DXB, ALA, NTI, IIQ).

We like the fund’s long term approach to investing (like us) and we like to follow the fund into biotechs in particular given its past success.

NTI Management track record

NTI’s Executive Director is Dr Tom Duthy, who is also Chairman of Arovella Therapeutics, another one of our Portfolio Companies, which grew from a low of 2 cents to a high of 18 cents.

Tom was also the head of corporate development for Sirtex Medical before its $1.9BN takeover in 2019.

We like to follow management that has delivered for us in the past.

Large addressable market for Autism treatment

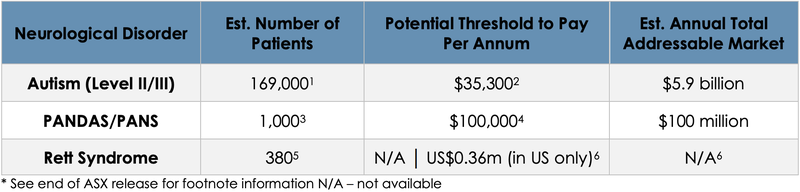

Aside from Autism Spectrum Disorder (ASD) costs the Australian taxpayer $5.9 billion each year through the NDIS.

It is responsible for over 30% of the NDIS spending each year because ASD affects 1 in 100 children.

This is a big market for NTI to target and if it can develop a commercial solution it will be able to capture significant value.

What do we expect NTI to deliver?

Objective #1: Orphan Drug Designation & progress with FDA

NTI164 has shown very promising results in clinical trials so far. Over the next 12 months NTI will aim to grow the global profile of its lead product NTI164 through attaining orphan drug status for certain conditions, and various preclinical studies.

These are all important for the ultimate goal of an IND grant from the FDA.

Milestones

🔲 Orphan drug status Rett Syndrome (US)

🔲 Orphan drug status Rett Syndrome (Europe)

🔲 Orphan drug status PANDAS/PANS (US)

🔲 Orphan drug status PANDAS/PANS (Europe)

🔲 Investigational New Drug (IND) application (FDA)

🔲 IND granted with the FDA

Objective #2: Secure a global partner for NTI164

We want to see NTI advance commercialisation initiatives and, ideally, accelerate them. This could be a source of additional capital for the business to fund offshore trials and advance regulatory requirements.

Milestones

🔲 Licensing/partnership agreement

🔲 Partnership on global clinical strategy

🔲 Potential M&A deal (Strategic equity investment?)

Objective #3: Commercialise NTI164 in Australia

We want to see NTI complete precursor toxicology/PK studies and lodge provisional registration applications with the TGA for PANDAS/PANS and Rett Syndrome.

Milestones

🔲 Complete toxicology trials

🔲 Complete pharmacokinetic (PK) trials

🔲 Pre-submission meeting with the TGA

🔲 Application for provisional pathway

🔲 Provisional pathway granted

Objective #4: Cerebral Palsy Clinical Trials

NTI intends to launch a Phase I/II clinical trial for Cerebral Palsy in 2H CY2024. We see this as a source of additional upside for NTI over the long term.

Milestones

🔲 HREC Approval and TGA clearance

🔲 First patient recruited

🔲 Completion of patient recruitment

🔲 Last patient dosed

🔲 8-week results

🔲 12-week results

What could go wrong?

Regulatory risk

There are a number of key regulatory hurdles that NTI will need to clear.

This includes but is not limited to IND applications with the FDA, orphan drug status, provisional approval for fast tracked commercialisation with the TGA.

There is no guarantee that these regulatory approvals will be granted and if they are rejected it will be a big setback for NTI.

Partnership risk

NTI is looking to bring on a partner to help fund its clinical trial work globally.

These deals can take a long time and delays do happen.

There is no guarantee that NTI finds a suitable partner, or if the deal that NTI ends up securing meets market expectations in terms of value.

Clinical trial risk

It is important to be aware that clinical trials can be unsuccessful.

Here are some of the standard risks that are associated with biotechs that are undertaking clinical research:

- Patient recruitment is delayed or fails

- Ethics approval is delayed or fails

- Clinical trial cost blowouts

- The drug/treatment is not considered safe for human consumption (usually established in Phase I)

- The drug or treatment is ineffective at treating the particular disease (usually determined by clinical trial results in Phase II and Phase III)

- The design of the trial is such that the regulatory body does not approve the drug/treatment

There is a chance that one or more of NTI’s clinical trials fail to meet their primary or secondary endpoints, meaning the treatments fail to satisfy the criteria of the studies. Any clinical trial results, if negative, could hurt the NTI share price.

Competition risk

NTI will need to move quickly to establish its presence in the market. If progress is slow, alternative treatments could emerge hurting NTI’s prospects.

Funding risk

Pre revenue biotech companies regularly need to raise capital to fund their growth ambitions. Capital raises can cause dilution to existing shareholders.

As a pre-revenue company, NTI will likely need to raise capital at some stage in the future, potentially at a discount to the prevailing market prices to secure funding. This will be contingent on clinical trial results and broader market sentiment (see next risk).

Market risk

Broader market sentiment for small pre-revenue biotechs could deteriorate and the sector as a whole trades lower, taking NTI’s share price with it.

Alternatively, the entire equities market could sell down as well.

What is our investment plan?

Our Investment Plan for NTI is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of any of the clinical trial results, a macro triggering event or any other unknown reason, we may look to sell up to ~20% of our holding. See our general disclosure policy for more details.

Our NTI Investment Memo #1 retro

Investment Memo: Neurotech International (ASX:NTI) - CLOSED

Opened: 18-Sep-2023

Closed: 14-Aug-2024

Shares Held at Open: 8,400,000

Shares Held at Close: 8,020,000

What does NTI do?

Neurotech International (ASX:NTI) is a clinical stage biotech company.

NTI is advancing clinical trials targeting rare and severe neurological disorders predominantly in children.

NTI’s primary treatment is a cannabinoid derived biopharmaceutical called NTI-164. NTI is seeking to prove it is a both safe and effective treatment for disorders such as Autism Spectrum Disorder, Rett Syndrome, PANDAS/PAN and Cerebral Palsy.

What is the macro theme?

Paediatric neurological disorders are not getting as much attention from biotech companies as they should, but luckily there are government incentives for companies developing treatments for these disorders.

The impact to families who have children with these disorders is significant and society more generally bears a large cost in supporting these families. Moreover, some treatments can have bad side effect profiles or suboptimal efficacy.

NTI’s clinical trials are for disorders of the brain and spinal cord, mostly in children, across potential orphan drug indications for rare conditions, such as Rett Syndrome as well as disorders that have larger total addressable markets such as Autism Spectrum Disorder (ASD). Both avenues to market for NTI164 could prove lucrative, assuming the trials are successful.

As is often the case, biotechs that successfully complete clinical trials can generate sustained re-rates as positive data comes out, regulatory approvals are granted and commercialisation agreements are made.

We think that companies that can improve on existing standards of care across both safety and efficacy will attract capital in the market due to their ability to improve both quality of life and health economics.

Macro Sentiment [Very Strong]

NTI is leveraged to two key investment thematics, “orphan drugs” (specifically for neurological diseases in children) and “autism”. Both of these macro thematics have been strong in the last twelve months.

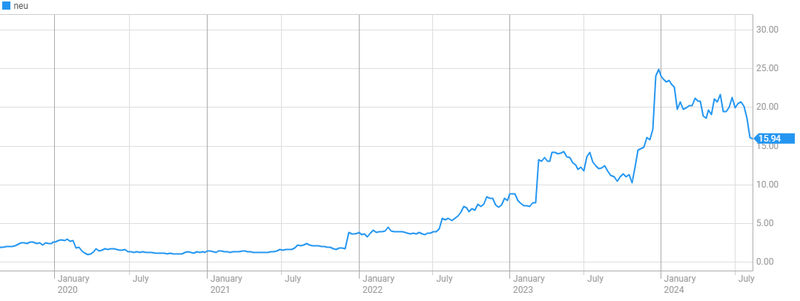

Leading orphan drug company Neuren published first sales for its DAYBUE product of US$66.9M in the quarter. The company’s share price is up even higher than when we first invested in NTI, showing the huge market attention and demand for the product.

Also within the last 12 months, autism, and its cost to the $42BN NDIS, has been under the spotlight with the Australian Federal Budget highlighting that reforms may be needed to reduce this cost. This however means that children that rely on the NDIS may not have access to the care that they need, highlighting the importance of a treatment like NTI164

Why did we invest in NTI?

NTI has significant material newsflow in the next 6-12 months across 3 trials

Clinical trial results are massive share price catalysts for biotechs. NTI has three different trials completing over the next 12 months. One of them is expected in the next couple of weeks.

NTI is targeting “orphan” diseases - treatments that are highly valuable

NTI is currently targeting PANDAS/PANS and Rett Syndrome, which are potentially eligible for orphan drug designation. The average price for an orphan drug is US$32,000 per year per patient and government approvals to market are fast tracked.

Grade = A

NTI delivered on all three catalysts that were forecast for the company. The results of these catalysts were also positive with the company now able to move through to the next stage of development.

NTI is following the same strategy as the $1.4BN capped Neuren

Neuren Pharmaceuticals’ share price re-rated by more than 1,300% (~$100M market cap to $1.4BN market cap). Neuren developed a successful treatment for Rett Syndrome and is working on other orphan diseases. NTI is unashamedly trying to replicate Neuren’s path to success. We like this approach.

Grade = A

The Neuren story continues to grow. During our Memo period, Neuren's market cap hit ~$3.3BN, and NTI delivered clinical trial results from its Rett Syndrome trial. Ultimately, we remain Invested in NTI to see its value start to appreciate further toward Neuren.

Strong safety profile, is NTI’s treatment better than $1.4BN Neuren?

If NTI’s upcoming Rett Syndrome trial shows its treatment is SAFER than $1.4BN Neuren’s “claim to fame” Rett Syndrome treatment, we think NTI can take a big chunk of the market (and hopefully get to a similar $1.4BN market cap).

Grade = A

The results published from NTI’s Rett Syndrome trial showed that it was better than DAYBUE from a safety perspective. The efficacy data also showed similarly strong performance to DAYBUE.

Promising efficacy data at treating Autism, large addressable market

If NTI’s treatment is proven safe and effective for Autism Spectrum Disorder (ASD), we think it could become an important part of the overall care for ASD sufferers, which is 1 in 100 children.

Grade = A

NTI was able to replicate the strong results from its Phase I Autism with much success. Autism continues to grow in Australia, and its cost to the healthcare system has been strongly in the spotlight.

NTI Management track record

NTI’s Executive Director is Dr Tom Duthy, who is also Chairman of Arovella Therapeutics, another one of our Portfolio Companies, which grew from a low of 2 cents to a high of 10.5 cents between January and April 2023. We like to follow management that has delivered for us in the past.

Grade = A

NTI’s executive director Dr. Tom Duthy did what he said he would do on time and on budget. Once all of the trial data were published Duthy pulled the trigger on a meaningful $10M raise at 10 cents. This was at a peak market price for NTI, which provided minimal dilution for existing shareholders.

Successful fund, Merchant Group has a substantial position in NTI

Merchant Group became a substantial shareholder of NTI with a 5.01% stake when NTI was trading at ~9 cents. We have followed Merchant Group’s investments closely and think the fund has a keen eye for high potential biotechs given its past history of success.

Grade = A

Merchant added to its position during our Memo period and now owns 7.12% of NTI which reinforces this reason.

What do we expect NTI to deliver?

Objective #1: Rett Syndrome clinical trials

NTI is currently undertaking a Phase I/II trial that will test the safety and efficacy of NTI’s treatment for a rare genetic neurological and developmental disorder called Rett Syndrome.

This is the same disease that Neuren Pharmaceuticals commercialised a treatment for which helped take Neuren to a ~$1.4BN market cap.

NTI’s trial is aiming to improve on Neuren’s results across safety and efficacy, after dosing the first patient in this trial in August 2023.

Milestones

✅ Last patient dosed for Phase I/II

✅ Results (anticipated Q1 CY2024)

Grade = A

The results published from NTI’s Rett Syndrome successfully passed the primary endpoint. The results also showed that NTI164 had a much better safety profile compared to the market leading product DAYBUE and the efficacy was relatively similar.

Objective #2: Autism Spectrum Disorder (ASD) clinical trials

After a successful Phase I/II trial demonstrated the safety of NTI’s treatment in 2023, and showed promising signs on its efficacy, NTI launched a larger Phase II/III trial for ASD.

We expect NTI to complete recruitment for this trial before the end of 2023.

Milestones

✅ Completion of patient recruitment (H2 CY2023)

✅ Last patient dosed

✅ Results (Q1 CY2024)

🔲 52 week results

Grade = A

The results of the Autism trial passed the primary endpoint. Data that was published beyond the 8 week mark showed that the patients continued to improve.

Anecdotal evidence out of the trial was extremely positive. We think that these were excellent results.

Objective #3: PANDAS/PANS clinical trial

This Phase I/II clinical trial is testing the safety and efficacy of NTI’s treatment for a rare paediatric neurological disorder sometimes associated with Streptococcal infections called PANDAS/PANS.

Milestones

✅ Results (mid-late September CY2023)

Grade = A

The PANDAS/PANS trial showed clinically significant and meaningful improvements in clinical function, with excellent safety and tolerability over 12 weeks. This is exactly what we wanted to see from this initial trial.

Objective #4: Cerebral Palsy clinical trials

NTI intends to launch a Phase I/II clinical trial for Cerebral Palsy in 2H CY2023. We see this as a source of additional upside for NTI over the long term.

Milestones

🔲 HREC Approval and TGA clearance

🔲 First patient recruited

🔲 Completion of patient recruitment

🔲 Last patient dosed

🔲 Results

Grade = C

These trials appear to have been delayed by a year and are now scheduled to commence in 2H of 2024. We suspect this may have been a prudent move to preserve cash and focus on the other key clinical trials that were ongoing over the period.

Objective #5: Advance commercialisation through licensing/partnerships

We want to see NTI advance commercialisation initiatives at this early stage, and ideally accelerate these initiatives pending clinical trial results. This could be a source of additional capital for the business.

Milestones

🔲 Sign a licensing/partnership agreement with another larger company

Grade = C

This has not eventuated yet - but now that NTI is armed with meaningful clinical data we are optimistic for some kind of partnership deal in the next 12-18 months.

What could go wrong?

Clinical trial risk

It is important to be aware that clinical trials can be unsuccessful.

In particular, there are some standard risks that are associated with biotechs that are undertaking clinical research:

- Patient recruitment is delayed or fails

- Ethics approval is delayed or fails

- Clinical trial cost blowouts

- The drug/treatment is not considered safe for human consumption (usually established in Phase I)

- The drug or treatment is ineffective at treating the particular disease (usually determined by clinical trial results in Phase II and Phase III)

- The design of the trial is such that the regulatory body does not approve the drug/treatment

There is a chance that one or more of NTI’s clinical trials fail to meet their primary or secondary endpoints, meaning the treatments fail to satisfy the criteria of the studies. Any clinical trial results, if negative, could hurt the NTI share price.

Risk = Mitigated

All three clinical trials met the primary endpoint. The next stage will be to see if NTI can replicate these in larger studies.

Competition risk

NTI will need to move quickly to establish its presence in the market. If progress is slow, alternative treatments could emerge hurting NTI’s prospects.

Risk = Unchanged

Funding risk

Pre revenue biotech companies regularly need to raise capital to fund their growth ambitions. Capital raises can cause dilution to existing shareholders.

NTI will likely need to raise capital at some stage in the future, potentially at a discount to market prices to secure funds. This will be contingent on clinical trial results and broader market sentiment (see next risk).

Risk = Mitigated

NTI conducted a $10M raise at 10 cents per share, mitigating the funding risk in the short / medium term.

NTI is funded for the upcoming period of planned newsflow.

Market risk

Broader market sentiment for small pre-revenue biotechs could get worse and the sector as a whole trades lower, taking NTI’s share price with it. Alternatively, the entire market could sell down as well.

Risk = Unchanged

What is our investment plan?

Our Investment Plan for NTI is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of any of the clinical trial results, a macro triggering event or any other unknown reason, we may look to sell up to ~20% of our holding. See our general disclosure policy for more details.

Grade = B

We Top Sliced a small portion of our position at an average sell price of $0.074, above our Initial Entry Price.

We then went on to add to our position in the $0.10 raise, which is now underwater - not ideal but hoping in the long term NTI’s share price will appreciate.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.